Reports

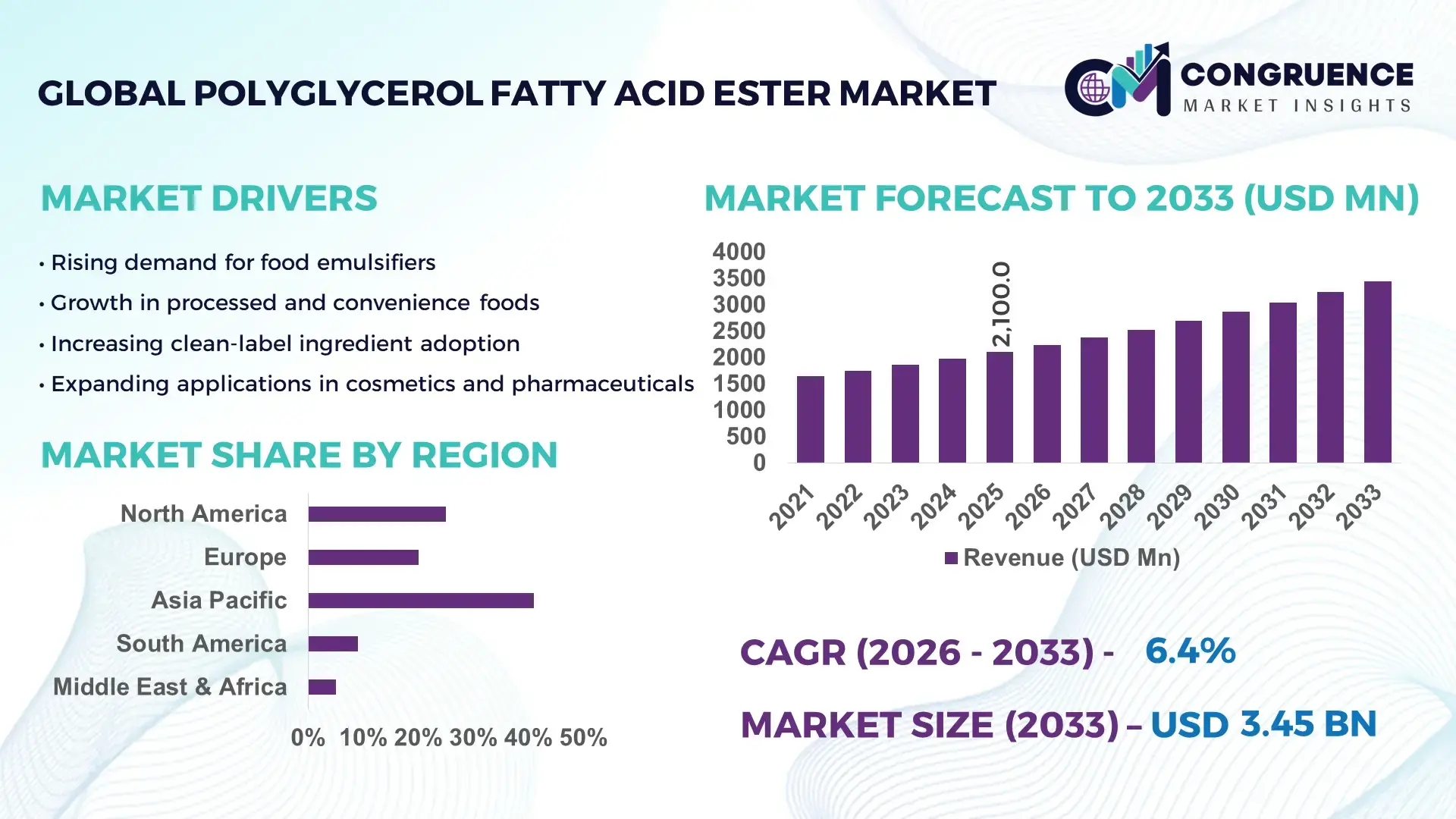

The Global Polyglycerol Fatty Acid Ester Market was valued at USD 2100 Million in 2025 and is anticipated to reach a value of USD 3449.46 Million by 2033 expanding at a CAGR of 6.4% between 2026 and 2033.

Rising adoption of clean-label emulsifiers in processed foods and cosmetics is accelerating demand, with polyglycerol esters delivering up to 18% improved emulsification stability compared to conventional mono- and diglycerides, directly influencing formulation efficiency and shelf-life optimization. Between 2024 and 2026, tightening food safety regulations across Asia and Europe, combined with raw material price volatility linked to palm oil supply constraints, have shifted procurement strategies toward diversified fatty acid sources and regionally integrated production hubs.

China leads the global market with approximately 32% production share, supported by over 40 large-scale manufacturing facilities and investments exceeding USD 250 million in food-grade emulsifier capacity expansion since 2023. The country’s strong processed food and personal care sectors contribute nearly 60% of domestic consumption, while export volumes have increased by 12% year-on-year due to competitive cost structures. In comparison, Europe holds around 24% share but focuses on high-purity, specialty-grade esters, achieving 15% higher pricing due to stringent regulatory compliance and advanced formulation technologies. Strategically, companies prioritizing raw material diversification, regional manufacturing integration, and high-performance formulations are positioned to secure long-term competitive advantage in this evolving global market.

Market Size & Growth: USD 2100M (2025) to USD 3449.46M (2033), CAGR 6.4%, driven by 22% rise in clean-label emulsifier demand across food processing.

Top Growth Drivers: Clean-label adoption (+22%), processed food expansion (+18%), cosmetic formulation demand (+15%).

Short-Term Forecast: By 2027, production efficiency improves by 12% due to process optimization and raw material blending strategies.

Emerging Technologies: Enzymatic esterification and automated blending systems enhance yield by 10–14% while reducing waste by 8%.

Regional Leaders: Asia-Pacific (~USD 1400M) with 30% export growth; Europe (~USD 900M) driven by premium formulations; North America (~USD 650M) with 20% demand in bakery applications.

Consumer Trends: 65% of food manufacturers now prioritize plant-based emulsifiers, increasing usage in dairy alternatives and baked goods.

Pilot Case: 2025 food processing project improved product shelf life by 16% using advanced polyglycerol ester blends.

Competitive Landscape: Top player holds ~14% share; key companies include 4–5 global manufacturers focusing on specialty emulsifiers.

Regulatory & ESG Impact: Compliance with clean-label standards reduced synthetic additive use by 19% across EU markets.

Investment & Funding: Over USD 400M invested since 2024 in capacity expansion and sustainable sourcing partnerships.

Innovation & Outlook: High-purity and multifunctional esters improve performance by 15%, supporting next-gen food and cosmetic formulations.

Food processing accounts for approximately 58% of total demand, followed by personal care at 27% and pharmaceuticals at 15%, reflecting strong cross-industry utilization. Recent innovations in enzymatic synthesis have improved product purity by 13%, while Asia-Pacific demand has risen by 20% due to expanding packaged food consumption. Increasing regulatory focus on sustainable sourcing is shaping supply chains, positioning bio-based emulsifiers as a strategic growth lever moving forward.

Polyglycerol fatty acid esters are rapidly becoming a critical battleground for formulation innovation, as food, personal care, and pharmaceutical companies accelerate the shift toward multifunctional, clean-label emulsifiers that directly influence product stability, cost efficiency, and regulatory compliance. This market is transforming competitive dynamics by enabling up to 20% improvement in product shelf stability while optimizing ingredient usage across high-volume applications.

Supply chains are shifting under pressure from palm oil sourcing volatility and tightening global labeling standards, forcing manufacturers to redesign procurement and production strategies. Enzymatic esterification technology improves efficiency by 15% while reducing cost by 10% compared to legacy chemical synthesis systems, enabling scalable and sustainable production. Asia-Pacific leads in volume, while Europe leads in innovation with over 28% adoption of high-purity, specialty-grade emulsifiers in regulated applications.

Over the next 2–3 years, processing efficiency is set to increase by 12%, driven by automation and advanced blending techniques. ESG alignment is emerging as a competitive lever, reducing compliance costs by 14% and improving export market access. A 2025 reformulation initiative in the bakery sector achieved a 17% reduction in additive usage while enhancing texture consistency. Capital allocation is accelerating toward bio-based inputs and regional manufacturing hubs, with companies expanding capacity and forming strategic partnerships. Competitive advantage will be defined by the ability to integrate sustainable sourcing, advanced processing, and high-performance formulations at scale.

The accelerating shift toward clean-label and plant-based formulations is forcing a structural transformation across the polyglycerol fatty acid ester market, with over 65% of global food manufacturers prioritizing naturally derived emulsifiers. This demand surge is directly increasing adoption in bakery and dairy alternatives, where performance consistency improves by 18% compared to traditional emulsifiers. Simultaneously, supply chains are being restructured due to global palm oil sourcing pressures, particularly following Southeast Asian export constraints in 2024, which triggered a 12% shift toward alternative fatty acid feedstocks. The cause-effect dynamic is clear: rising regulatory scrutiny and consumer preference are driving formulation upgrades, compelling manufacturers to expand production capacity and invest in high-purity processing technologies. Companies are responding by accelerating capital expenditure in enzymatic production facilities and forming supplier partnerships to secure diversified raw material inputs. This is not only stabilizing supply but also enhancing product differentiation, allowing firms to command premium pricing while optimizing operational efficiency in a highly competitive global market.

The market faces significant constraints from raw material dependency, particularly on palm-derived fatty acids, which account for nearly 70% of input costs and have experienced price fluctuations exceeding 25% in recent cycles. This volatility is compounded by supply concentration in Southeast Asia, where geopolitical trade adjustments and environmental regulations have tightened export availability. As a result, production costs have increased by 10–14%, directly impacting margins and limiting scalability for smaller manufacturers. Regulatory compliance adds another layer of complexity, with stringent purity and labeling requirements increasing processing costs by approximately 9% in high-regulation markets such as Europe. These constraints are forcing companies to rethink sourcing strategies and operational models. Leading players are mitigating risks through long-term procurement contracts, backward integration into raw material supply, and investment in alternative feedstocks such as synthetic or non-palm-based fatty acids. Additionally, process optimization and digital supply chain monitoring are being deployed to reduce exposure to price shocks and ensure consistent production output.

High-impact opportunities are emerging at the intersection of advanced food technology, personal care innovation, and pharmaceutical delivery systems, where polyglycerol esters offer multifunctionality and performance gains of up to 16%. The rapid expansion of plant-based foods, growing at over 20% adoption globally, is unlocking new demand for stabilizers that enhance texture and shelf life. At the same time, cosmetic formulations are integrating these esters to achieve 12% improved moisture retention and formulation stability. A key future signal lies in the adoption of precision fermentation and bio-based feedstocks, which are improving sustainability metrics by 15% while reducing dependency on volatile raw materials. Non-obvious upside is emerging in niche applications such as nutraceutical encapsulation, where emulsification efficiency directly influences bioavailability. Companies are positioning aggressively by expanding R&D capabilities, forming cross-industry partnerships, and investing in localized production ecosystems to capture emerging demand pockets and secure long-term market leadership.

Despite strong demand fundamentals, execution challenges are constraining the market’s ability to scale efficiently. Infrastructure limitations in emerging markets are restricting production expansion, with capacity utilization gaps of up to 18% due to inadequate processing facilities and logistics inefficiencies. Additionally, performance variability across different fatty acid sources can lead to inconsistency levels of 10–12% in end-product quality, creating formulation risks for manufacturers. A critical real-world pressure is the tightening of environmental and sustainability regulations, which are increasing compliance costs by nearly 11% while simultaneously requiring traceability across supply chains. These challenges directly impact long-term growth consistency and profitability, particularly for companies lacking integrated production systems. To remain competitive, manufacturers must invest in advanced processing technologies, strengthen quality control mechanisms, and build strategic partnerships across the value chain. Solving these execution gaps will determine which players can sustain growth and maintain competitive positioning in an increasingly demanding global market.

18% shift toward enzymatic processing is reshaping production efficiency. Manufacturers are replacing chemical synthesis with enzymatic esterification, improving yield consistency by 15% and reducing by-product waste by 10%. Adoption has crossed 35% in large-scale facilities, driven by tighter food safety norms. This shift is optimizing batch cycles and lowering reprocessing costs, pushing companies to retrofit plants and scale bio-catalytic capabilities.

22% increase in multi-functional formulations is redefining product design. Demand for single-ingredient emulsifiers delivering stabilization, texture, and shelf-life enhancement has surged, reducing formulation complexity by 14%. Over 40% of new product launches now integrate multi-functional PGFE blends. Companies are restructuring R&D pipelines to prioritize high-performance variants, accelerating time-to-market and reducing ingredient dependency across applications.

16% regional demand shift toward Asia-Pacific is forcing supply realignment. Localized production has increased by 12% as companies respond to logistics disruptions and import cost pressures observed during recent global trade adjustments. This is reducing lead times by 9% and strengthening regional supply resilience. Firms are expanding manufacturing bases and forming regional supplier alliances to stabilize operations.

13% rise in contract manufacturing is transforming business models. Outsourced production now accounts for nearly 28% of total output, enabling cost reductions of 11% and faster scaling. Mid-sized companies are leveraging this model to enter high-spec markets without heavy capital investment. This trend is redefining competitive dynamics, with partnerships replacing traditional capacity ownership.

The polyglycerol fatty acid ester market is structured across types, applications, and end-users, with demand concentrated in performance-driven and regulatory-compliant segments. Food-grade and emulsifier-based types dominate due to high integration in food processing, accounting for over 55% of total usage. Application-wise, food emulsification and bakery segments lead, supported by consistent demand for texture and shelf-life optimization. End-user concentration remains strongest in the food and beverage industry, contributing nearly 60% of total consumption, while cosmetics and pharmaceuticals are emerging as high-value segments. Demand is shifting toward multifunctional and high-purity variants, driven by regulatory tightening and efficiency requirements. This segmentation highlights a clear transition from volume-driven to value-driven demand, requiring companies to align product development, capacity allocation, and go-to-market strategies with evolving industry needs.

PGFE Emulsifiers dominate the market with approximately 34% share, driven by their superior integration in food and cosmetic formulations, offering up to 18% improved stability and consistency. Their scalability and compatibility with clean-label requirements position them as the primary choice for large-scale manufacturers. In contrast, PGFE Stabilizers are the fastest-growing segment, expanding at an adoption rate exceeding 16%, fueled by rising demand in dairy alternatives and processed foods where texture control is critical. Food-Grade PGFE holds around 28% share due to strict regulatory alignment and widespread usage in consumables, while Industrial-Grade PGFE and PGFE Surfactants together account for nearly 38%, serving niche applications in chemical processing and specialized formulations. A clear shift is visible from traditional emulsifiers toward multifunctional stabilizer systems, as companies aim to reduce formulation complexity and enhance performance.

Businesses are responding by expanding emulsifier production capacity while investing in stabilizer-focused R&D to capture emerging demand. Strategic focus is shifting toward high-purity, application-specific variants, indicating where future investments are likely to generate the highest returns.

Food Emulsification leads with approximately 36% share, reflecting its essential role in maintaining product consistency across processed foods. This dominance is reinforced by its direct impact on shelf life and texture, improving formulation performance by up to 17%. Bakery and Confectionery follow closely, contributing around 22%, where demand is stable due to high consumption frequency and production scale. Cosmetics and Personal Care is the fastest-growing segment, expanding at over 18% adoption, driven by increased demand for plant-based and multifunctional ingredients that enhance skin absorption and stability. Compared to mature food applications, this segment reflects a shift toward premium, high-margin formulations.

Dairy Products and Pharmaceutical Formulations together account for nearly 42%, with steady growth supported by functional performance and regulatory compliance needs. Companies are adapting by tailoring product formulations for specific applications, scaling production for high-demand food uses while innovating for cosmetic and pharmaceutical niches.

The Food and Beverage Industry dominates with nearly 58% share, driven by high-volume consumption and dependency on emulsifiers for consistency and shelf life. Its scale and continuous production cycles make PGFE a critical input, ensuring stable demand. In contrast, the Nutraceutical Industry is the fastest-growing segment, with adoption increasing by over 19%, supported by rising demand for encapsulation and bioavailability enhancement. The Cosmetics and Personal Care Industry accounts for approximately 21%, focusing on high-performance and clean-label formulations, while the Pharmaceutical Industry and Chemical Manufacturing together contribute around 21%, serving specialized and regulated applications.

A clear contrast exists between the established, volume-driven food sector and the emerging, value-driven nutraceutical and cosmetic segments. Companies are responding by customizing product offerings, implementing tiered pricing strategies, and forming partnerships with end-users to co-develop application-specific solutions.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2026 and 2033.

Asia-Pacific leads in production scale with over 45% of global output and 30% lower manufacturing costs, driven by integrated supply chains and high-volume food processing demand. Europe holds approximately 26% share, leading in innovation with over 28% adoption of high-purity, regulation-compliant emulsifiers. North America captures nearly 22% demand, with rapid expansion fueled by clean-label reformulation trends and 18% higher adoption in premium food segments. A key structural shift is the relocation of production closer to end-use markets following recent global logistics disruptions, reducing lead times by 10%. Strategically, companies are balancing Asia-Pacific for scale, Europe for innovation, and North America for high-value growth positioning.

How are clean-label demands reshaping emulsifier adoption and production strategies?

North America accounts for approximately 22% of global demand, driven by strong adoption in processed foods and premium bakery segments. Clean-label reformulation is accelerating, with over 60% of manufacturers shifting toward plant-based emulsifiers, improving product transparency and compliance. Regulatory alignment with strict labeling standards is forcing companies to adopt high-purity PGFE variants, increasing processing costs by 9% but enhancing product differentiation. Execution-level shifts include automation in blending and formulation, improving efficiency by 12%. A notable move includes capacity expansion projects increasing domestic production by 15% to reduce import dependency. Enterprises prioritize consistency and regulatory compliance, making this region a high-value, innovation-driven market where companies invest to secure premium positioning.

What compliance-driven shifts are redefining formulation standards and product quality?

Europe holds around 26% of the market, with demand concentrated in Germany, France, and the UK due to advanced food processing and cosmetic industries. Stringent ESG and regulatory frameworks have increased demand for sustainable and traceable emulsifiers, with over 70% of manufacturers prioritizing certified raw materials. Compliance-driven production has raised operational costs by 10% but improved product quality benchmarks by 16%. Companies are adopting advanced purification and traceability technologies, with over 25% integration in large-scale facilities. A strategic shift toward bio-based inputs is reducing environmental impact by 14%. Enterprises operate on a quality-first model, making Europe a region that forces continuous innovation and regulatory alignment to remain competitive.

What factors are accelerating large-scale production and consumption efficiency?

Asia-Pacific dominates with over 41% market share, led by China and India due to strong manufacturing infrastructure and expanding processed food sectors. The region benefits from cost-efficient production, reducing operational expenses by nearly 20% compared to global averages. Execution-level shifts include localized manufacturing expansion, with production capacity increasing by 18% to meet rising domestic and export demand. Digital supply chain integration has improved delivery efficiency by 11%. A strategic move includes export growth of over 14%, supported by competitive pricing and large-scale production. Enterprises prioritize cost, scale, and speed, making this region essential for volume-driven expansion and global supply chain stability.

How are emerging industries balancing demand growth with infrastructure constraints?

South America contributes approximately 6% of the global market, with Brazil and Argentina leading due to expanding food processing industries. Demand is driven by rising consumption of packaged foods, increasing emulsifier usage by 13%. However, infrastructure limitations and import dependency have raised production costs by 12%, constraining scalability. Companies are shifting toward localized blending and distribution, improving supply responsiveness by 9%. A notable development includes regional partnerships boosting production capacity by 10%. Enterprises remain price-sensitive, prioritizing cost-effective solutions. This region presents a balanced opportunity, offering growth potential but requiring strategic navigation of infrastructure and cost constraints.

What infrastructure and investment shifts are driving industrial transformation?

The Middle East & Africa region accounts for nearly 5% of global demand, with key markets including the UAE and South Africa. Demand is linked to food processing and expanding personal care sectors, increasing usage by 11%. Investment in industrial infrastructure and import substitution strategies is driving transformation, with local production capacity rising by 9%. Execution-level shifts include adoption of automated blending systems, improving operational efficiency by 10%. Strategic partnerships and government-backed industrial projects have increased supply chain resilience by 8%. Enterprises focus on reliability and cost optimization, positioning this region as an emerging market with long-term strategic importance.

China – 28% share in the Polyglycerol Fatty Acid Ester market: Dominates due to large-scale production capacity, integrated supply chains, and strong processed food industry demand.

Germany – 12% share in the Polyglycerol Fatty Acid Ester market: Leads through high-purity product innovation, strict regulatory compliance, and advanced formulation technologies.

The competitive landscape is defined by global specialty chemical leaders competing with regional cost-efficient manufacturers and niche formulation innovators. Leading players such as BASF SE, Evonik Industries, DuPont Nutrition & Biosciences, Kerry Group, and Palsgaard collectively control approximately 48% of the market, competing directly on product performance, regulatory compliance, and supply chain reliability. Competition is intensifying across three fronts: technology-driven innovation delivering up to 15% higher formulation efficiency, cost optimization reducing production expenses by 10–12%, and supply chain integration improving delivery speed by 9%. Global leaders focus on high-purity, premium-grade esters, while regional players compete aggressively on pricing and localized supply advantages.

Strategically, companies are expanding production facilities, forming raw material partnerships, and investing in enzymatic processing technologies to enhance differentiation. The market is shifting toward vertical integration and sustainable sourcing control, creating barriers for new entrants due to high compliance and capital requirements. Winning in this market requires combining cost efficiency with advanced formulation capabilities and resilient supply chains, enabling players to outperform both premium innovators and low-cost competitors.

BASF SE

Evonik Industries AG

DuPont Nutrition & Biosciences

Kerry Group

Palsgaard A/S

Riken Vitamin Co., Ltd.

Mitsubishi Chemical Corporation

Lonza Group AG

Estelle Chemicals Pvt. Ltd.

Fine Organics Industries Ltd.

Guangzhou Cardlo Biochemical Technology Co., Ltd.

Sakamoto Yakuhin Kogyo Co., Ltd.

Enzymatic esterification is the current core technology reshaping production efficiency, delivering up to 15% higher yield consistency and reducing by-product formation by 10% compared to conventional chemical synthesis. Adoption has reached nearly 38% among large-scale manufacturers, particularly in food-grade applications. This shift is optimizing batch processing and lowering purification costs, enabling companies to improve margins while meeting stricter regulatory standards.

Emerging technologies such as continuous flow processing and AI-driven formulation systems are accelerating operational precision. Continuous systems improve throughput by 12% while reducing energy consumption by 9%, with deployment expanding across 25% of new facilities. AI-assisted formulation is enhancing emulsifier performance by 14%, enabling faster product customization. These integrations are allowing companies to reduce development cycles and respond rapidly to changing customer requirements, strengthening competitive positioning.

Disruptive advancements in bio-based feedstock processing and precision fermentation are redefining long-term scalability. Compared to legacy palm-based systems, these technologies reduce raw material volatility impact by 13% and improve sustainability metrics by 16%. Early adoption remains below 20%, but forward impact between 2026–2028 is significant as companies investing in these technologies gain supply chain control and premium market access. Competitive advantage is shifting toward players combining sustainable sourcing with high-performance processing, making immediate technology investment a critical strategic move.

March 2026 – BASF SE expanded its specialty emulsifier production line in Asia, increasing capacity by 18% to support rising food-grade demand. This move strengthens regional supply resilience and reduces lead times for key customers. [Capacity Expansion]

November 2025 – Palsgaard A/S launched a new enzymatic PGFE range delivering 12% higher emulsification stability, enhancing clean-label formulations for bakery applications. This innovation improves product consistency and reduces additive dependency. [Product Innovation]

July 2025 – Kerry Group entered a strategic partnership to co-develop plant-based emulsifier systems, improving formulation efficiency by 14%. The collaboration accelerates time-to-market for next-generation food solutions. [Strategic Partnership]

February 2024 – Fine Organics Industries Ltd. upgraded manufacturing processes, achieving a 10% reduction in energy consumption and improving output efficiency. This enhances cost competitiveness and sustainability positioning. [Process Optimization]

This report delivers comprehensive coverage of the polyglycerol fatty acid ester market across five core product types, five application areas, and five end-user industries, supported by detailed analysis across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It evaluates key technologies including enzymatic processing, continuous manufacturing, and bio-based feedstock integration, capturing adoption trends where advanced production methods have exceeded 35% penetration in large-scale facilities. The study also maps demand distribution, with food-grade applications accounting for over 55% usage and emerging segments such as nutraceuticals expanding at over 18% adoption.

Analytical depth is built through multi-layered insights covering over 10 major companies, regional production dynamics, and operational benchmarks such as efficiency gains of 12–15% through technology adoption. The report highlights evolving supply chain structures, regulatory impacts, and performance differentiation across segments. Strategic value lies in its ability to guide investment decisions, capacity expansion, and competitive positioning by identifying high-growth niches, technology shifts, and regional demand imbalances. With forward-looking coverage through 2033, it equips stakeholders to align with emerging opportunities, optimize resource allocation, and secure long-term market advantage.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 2100 Million |

|

Market Revenue in 2033 |

USD 3449.46 Million |

|

CAGR (2026 - 2033) |

6.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

BASF SE, Evonik Industries AG, DuPont Nutrition & Biosciences, Kerry Group, Palsgaard A/S, Riken Vitamin Co., Ltd., Mitsubishi Chemical Corporation, Lonza Group AG, Estelle Chemicals Pvt. Ltd., Fine Organics Industries Ltd., Guangzhou Cardlo Biochemical Technology Co., Ltd., Sakamoto Yakuhin Kogyo Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |