Reports

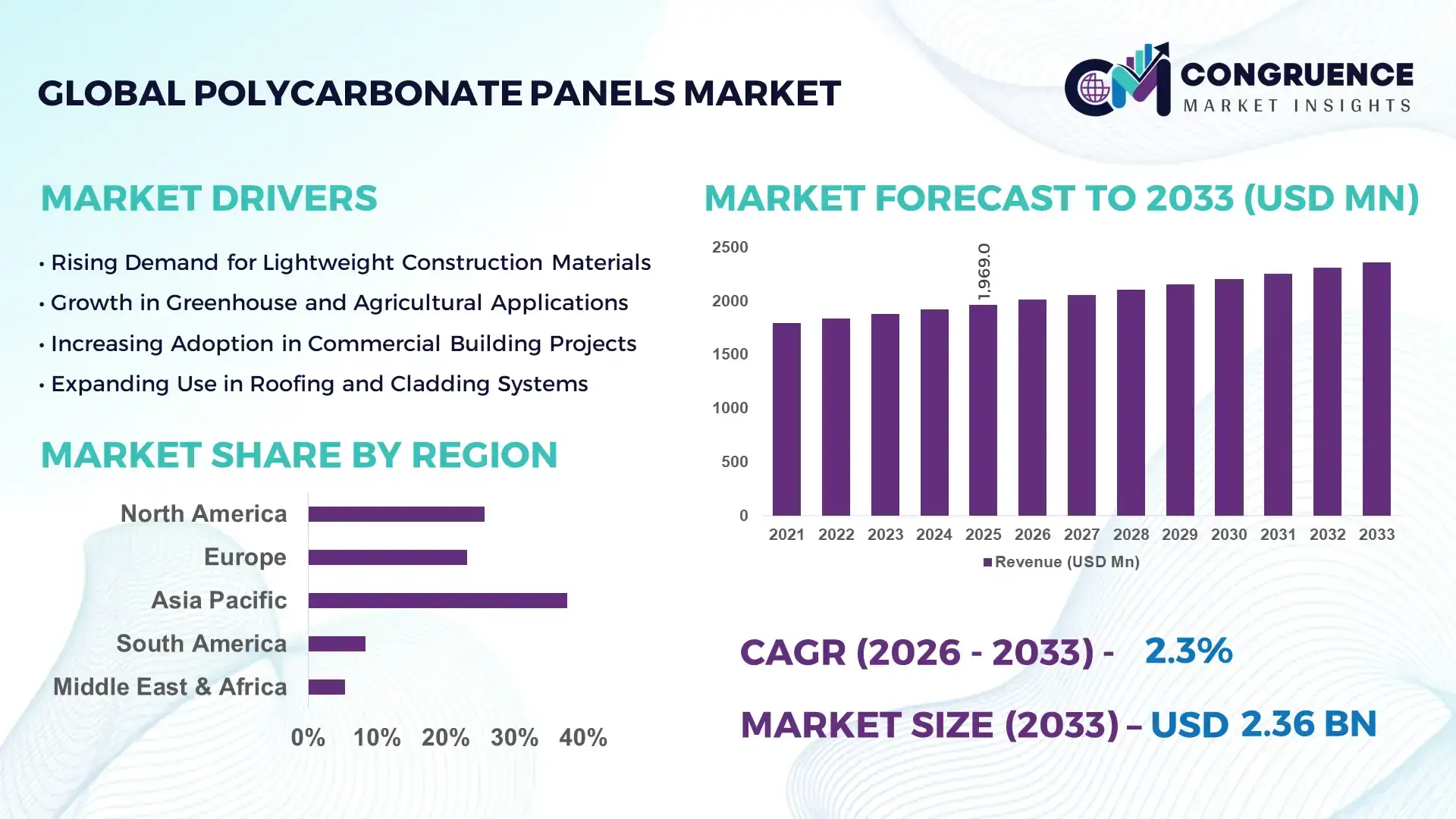

The Global Polycarbonate Panels Market was valued at USD 1969.04 Million in 2025 and is anticipated to reach a value of USD 2361.89 Million by 2033 expanding at a CAGR of 2.3% between 2026 and 2033. The steady expansion of construction, infrastructure modernization, and demand for durable transparent roofing solutions are key contributors to the market’s consistent growth trajectory.

China remains a major production hub for polycarbonate panels, supported by extensive manufacturing capacity and strong downstream demand from construction and industrial sectors. The country operates more than 2.5 million metric tons of annual polycarbonate resin production capacity, enabling large-scale panel fabrication for roofing, skylights, and greenhouse structures. Over 40% of industrial greenhouse installations in Asia utilize multiwall polycarbonate panels due to their high light transmission rates exceeding 80% and strong thermal insulation performance. Large-scale infrastructure investments exceeding USD 1 trillion in urban redevelopment and transportation facilities have also increased demand for impact-resistant roofing and facade materials. Chinese manufacturers have also adopted co-extrusion technologies that extend panel durability beyond 10–15 years, making the country a key manufacturing and technological center for advanced polycarbonate sheet products.

• Market Size & Growth: The global polycarbonate panels market reached USD 1969.04 million in 2025 and is projected to reach USD 2361.89 million by 2033, expanding at a CAGR of 2.3% due to rising adoption of lightweight, impact-resistant construction materials in commercial and industrial infrastructure.

• Top Growth Drivers: 38% increase in greenhouse installations using polycarbonate roofing, 32% growth in energy-efficient building material adoption, and 27% improvement in building insulation efficiency compared to traditional glass panels.

• Short-Term Forecast: By 2028, improved polycarbonate panel coatings are expected to reduce UV degradation by nearly 35% and increase panel lifespan by up to 20% in outdoor construction applications.

• Emerging Technologies: Multiwall polycarbonate extrusion, UV-protected co-extruded panels, and smart light-diffusing roofing systems are becoming widely adopted across modern architectural designs.

• Regional Leaders: Asia-Pacific is projected to reach USD 980 million by 2033 driven by infrastructure expansion; Europe is expected to approach USD 620 million with strong sustainable construction policies; North America may exceed USD 520 million due to demand in agricultural and commercial building sectors.

• Consumer/End-User Trends: Construction contractors, greenhouse developers, and industrial facility planners increasingly prefer polycarbonate panels for roofing, cladding, skylights, and noise-barrier installations due to their high impact resistance and 200 times stronger durability compared to glass.

• Pilot or Case Example: In 2024, a commercial greenhouse modernization project in the Netherlands replaced traditional glass roofing with polycarbonate multiwall panels, achieving a 22% reduction in energy consumption and 18% improvement in crop light distribution.

• Competitive Landscape: The market leader holds approximately 17% share, with major competitors including leading global chemical and polymer manufacturers and specialized panel producers supplying architectural and industrial applications.

• Regulatory & ESG Impact: Energy-efficient building codes and green construction certifications are encouraging the use of recyclable polycarbonate panels capable of reducing building heat loss by nearly 30%.

• Investment & Funding Patterns: More than USD 1.3 billion has been invested globally in polymer processing plants, extrusion technologies, and sustainable building materials over the past three years.

• Innovation & Future Outlook: Advances in anti-scratch coatings, high-clarity UV protection layers, and recyclable polycarbonate materials are expected to reshape building envelope technologies and support long-term sustainable infrastructure development.

Polycarbonate panels serve multiple industrial sectors including construction, agriculture, transportation, and signage manufacturing. Construction applications contribute nearly 55% of total market demand due to widespread use in skylights, roofing sheets, and facade glazing systems. Agricultural greenhouse structures account for approximately 25% of consumption, benefiting from high light diffusion and strong thermal insulation properties. Technological innovations such as double-layer multiwall structures and nano-coated UV protection are improving panel longevity and weather resistance. Environmental policies encouraging energy-efficient construction materials are accelerating adoption across Europe and North America, while urban infrastructure expansion in Asia-Pacific continues to support large-scale consumption of lightweight polymer-based building materials.

The Polycarbonate Panels Market has gained strategic importance within the global construction materials ecosystem as infrastructure modernization, sustainable building design, and climate-resilient construction increasingly rely on lightweight yet durable materials. Polycarbonate panels offer impact resistance nearly 200 times stronger than traditional glass while weighing approximately 50% less, making them suitable for roofing, skylights, facades, and greenhouse structures. These structural advantages allow builders and architects to improve energy efficiency while reducing material transportation and installation costs.

Technological innovation continues to reshape the industry’s competitive landscape. Multiwall polycarbonate panel technology delivers nearly 35% higher thermal insulation compared to conventional single-layer acrylic sheets. Similarly, UV-protected co-extrusion manufacturing techniques provide up to 40% longer service life compared to older polymer roofing materials. These performance improvements are driving adoption in energy-efficient building projects and modern agricultural infrastructure.

Regional dynamics also highlight distinct growth patterns. Asia-Pacific dominates global production volume due to large-scale polymer manufacturing clusters and rising infrastructure demand, while Europe leads in advanced adoption, with nearly 46% of commercial greenhouse projects using polycarbonate multiwall roofing systems. North America is witnessing rising installation rates in sports facilities, transit shelters, and commercial skylight structures where impact resistance and weather durability are critical. Over the next two to three years, digital manufacturing technologies and automated extrusion lines are expected to reshape production efficiency. By 2028, smart polymer processing technologies integrated with AI-based quality inspection systems are projected to reduce production defects by nearly 25% while improving material yield by 15%.

The global construction industry is rapidly shifting toward energy-efficient building materials, significantly increasing demand for polycarbonate panels in roofing, cladding, and skylight installations. Polycarbonate panels allow up to 85% natural light transmission while offering superior thermal insulation compared to conventional glass panels. This property helps reduce dependence on artificial lighting and HVAC systems in commercial and industrial buildings. In greenhouse agriculture, polycarbonate multiwall panels improve crop productivity by enhancing light diffusion and maintaining stable indoor temperatures. Studies show that multiwall panels can reduce heating energy requirements in greenhouses by nearly 20% compared to single-layer glass structures. Rapid expansion of protected agriculture, which now covers more than 500,000 hectares globally, has increased demand for advanced roofing materials. Urban infrastructure development is also contributing to the growth of the polycarbonate panels market. Modern transportation terminals, stadiums, and pedestrian shelters increasingly use impact-resistant polycarbonate roofing due to its ability to withstand hailstorms, strong winds, and heavy rainfall. As governments prioritize energy-efficient construction and green building certification programs, polycarbonate panels are becoming a preferred material across multiple large-scale infrastructure projects.

One of the primary limitations affecting the polycarbonate panels market is the volatility in polycarbonate resin and petrochemical raw material prices. Polycarbonate panels are produced using bisphenol-A and phosgene-based polymerization processes derived from petroleum feedstocks. Fluctuations in crude oil prices and disruptions in petrochemical supply chains often lead to inconsistent manufacturing costs for polycarbonate sheet producers. Over the past decade, raw material price variations have exceeded 25% in several global markets, creating uncertainty for manufacturers and construction companies planning large infrastructure projects. Such fluctuations increase procurement risks and can delay building projects that rely heavily on polymer-based construction materials. Additionally, alternative materials such as tempered glass, acrylic sheets, and fiberglass panels remain widely available in some markets. Although these materials offer lower durability compared to polycarbonate panels, their lower initial costs can influence purchasing decisions for small-scale construction projects. Supply chain disruptions, particularly during global logistics crises, have also affected resin availability, limiting production capacity and slowing expansion plans for polycarbonate panel manufacturing facilities.

Rapid expansion of protected agriculture worldwide presents a significant opportunity for polycarbonate panel manufacturers. Modern greenhouse structures rely on durable, transparent roofing materials capable of optimizing light distribution and maintaining controlled internal environments. Polycarbonate panels provide light transmission rates exceeding 80% while offering superior insulation compared to conventional glass coverings. Global greenhouse cultivation areas have expanded substantially, with countries in Europe and Asia investing heavily in climate-controlled farming infrastructure to ensure food security and improve crop yields. Polycarbonate panels enable improved light diffusion, which can increase crop productivity by up to 15% in certain greenhouse environments. Technological innovation in agricultural infrastructure is also encouraging the use of double-layer and triple-layer polycarbonate panels that provide enhanced insulation and impact resistance. These advanced panels reduce heating costs during winter months and protect crops from extreme weather conditions. As climate variability increases and demand for sustainable agriculture rises, greenhouse operators are expected to invest heavily in high-performance roofing materials, creating substantial long-term growth opportunities for polycarbonate panel manufacturers.

Environmental sustainability and polymer waste management have emerged as key challenges for the polycarbonate panels market. Although polycarbonate panels are highly durable and long-lasting, disposal and recycling processes remain complex due to chemical additives used in manufacturing. Large volumes of plastic construction materials are generated globally each year, and governments are increasingly introducing regulations aimed at reducing polymer waste. Recycling polycarbonate requires specialized facilities capable of separating coatings, UV protective layers, and other additives from the base polymer. In many developing regions, recycling infrastructure for high-performance engineering plastics remains limited. As a result, discarded polycarbonate panels may end up in landfills, raising environmental concerns among regulators and construction companies. Additionally, stricter environmental policies are encouraging manufacturers to adopt circular production models and increase the use of recycled polymer content. Developing recyclable panel systems while maintaining high transparency, durability, and impact resistance presents a technical challenge for manufacturers. Companies must invest in research and advanced polymer processing technologies to meet environmental compliance standards while maintaining competitive product performance.

• Rapid Expansion of Greenhouse Infrastructure: Global greenhouse cultivation has expanded significantly, surpassing 500,000 hectares of protected agriculture installations worldwide. Polycarbonate multiwall panels are increasingly used due to their ability to transmit more than 80% natural light while improving thermal insulation by nearly 25% compared to traditional glass roofing. In Europe alone, approximately 46% of commercial greenhouse structures now rely on polycarbonate roofing systems for improved crop yield stability. Agricultural technology programs in countries such as the Netherlands and Spain have increased investments in advanced greenhouse structures by over 30% during the past three years, accelerating demand for durable polycarbonate panels designed for climate-controlled farming.

• Adoption of Advanced UV-Protected Co-Extrusion Technology: Manufacturers are increasingly deploying UV-protected co-extrusion technologies to extend the operational lifespan of polycarbonate panels used in outdoor environments. New co-extruded panels can withstand prolonged exposure to ultraviolet radiation, maintaining structural integrity for more than 15 years while reducing degradation by nearly 40% compared to earlier polymer panel designs. Industrial construction projects in North America and Europe report a 28% increase in adoption of UV-resistant roofing panels due to their superior weather durability and reduced maintenance requirements in stadiums, transport hubs, and large commercial facilities.

• Growth in Energy-Efficient Building Materials: Energy-efficient construction is driving adoption of multiwall polycarbonate panels capable of reducing building heat transfer by approximately 30% compared to conventional transparent roofing materials. Modern multi-layer panels provide insulation values nearly 2.5 times higher than single-layer plastic sheets. In commercial construction projects, the integration of polycarbonate skylight panels has been shown to reduce daytime electricity consumption for lighting by nearly 18%. Sustainable building certification programs have encouraged builders to use recyclable polymer materials, increasing polycarbonate panel installations in energy-efficient office complexes and industrial warehouses by more than 22% in recent years.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the polycarbonate panels market. Approximately 55% of new building projects now integrate modular construction components to reduce construction time and labor costs. Pre-bent and precision-cut polycarbonate panels are increasingly prefabricated off-site using automated extrusion and CNC cutting machines, improving installation efficiency by nearly 30%. Demand for high-precision panel fabrication equipment has increased by more than 25% in Europe and North America, where construction companies prioritize faster project delivery timelines and higher structural consistency in prefabricated building components.

The polycarbonate panels market is segmented by product type, application, and end-user industries, reflecting the wide versatility of these high-performance polymer materials across multiple sectors. Product types include multiwall polycarbonate panels, solid polycarbonate panels, and corrugated polycarbonate panels, each designed to meet specific structural and environmental requirements. Multiwall panels are particularly valued for their strong insulation performance, while solid panels offer high transparency and impact resistance for architectural glazing systems. Application segmentation highlights the dominant role of construction and building infrastructure, where polycarbonate panels are widely used in roofing, skylights, facades, and industrial cladding. Agricultural greenhouse installations represent another significant application segment due to the material’s ability to diffuse light and maintain stable temperatures for crop cultivation. Additional applications include transportation infrastructure, safety glazing, noise barriers, and signage systems. End-user insights reveal strong adoption across construction companies, agricultural operators, industrial manufacturers, and transportation infrastructure developers. Growing infrastructure investment in emerging economies, combined with modernization of agricultural systems and increasing demand for durable building materials, is expanding consumption across all segments. The versatility, durability, and energy efficiency advantages of polycarbonate panels continue to drive their adoption across a diverse range of industrial and commercial environments.

The polycarbonate panels market includes several product types such as multiwall polycarbonate panels, solid polycarbonate panels, corrugated polycarbonate panels, and other specialized sheet configurations designed for specific architectural and industrial applications. Multiwall polycarbonate panels currently represent the leading segment, accounting for approximately 48% of global adoption due to their superior thermal insulation and lightweight structural design. These panels contain multiple internal chambers that trap air, enabling insulation performance nearly 2.5 times higher than single-layer plastic sheets. As a result, they are widely used in greenhouses, skylight roofing systems, and energy-efficient building envelopes. Solid polycarbonate panels account for nearly 28% of total installations and are commonly used in architectural glazing, safety barriers, and transparent roofing structures where high impact resistance and optical clarity are required. Corrugated polycarbonate panels hold approximately 17% of the market, particularly in industrial roofing and agricultural sheds where their structural rigidity and water drainage capabilities provide practical advantages.

Multiwall panels are also emerging as the fastest-growing product type, expanding at an estimated CAGR of around 4.1% due to rising demand for energy-efficient construction materials and greenhouse infrastructure. The remaining specialized polycarbonate sheet products, including anti-scratch and flame-retardant panels, collectively represent about 7% of the market and serve niche applications in industrial safety structures and transportation facilities.

Construction and building infrastructure represent the leading application segment in the polycarbonate panels market, accounting for approximately 52% of total installations worldwide. Polycarbonate panels are widely used for skylights, roofing systems, facade cladding, and industrial warehouse structures due to their high durability, weather resistance, and ability to transmit natural light. Compared to traditional glass materials, polycarbonate panels are nearly 50% lighter and up to 200 times more impact resistant, making them suitable for high-risk weather environments. Agricultural greenhouse applications account for roughly 27% of the market, with farmers and greenhouse developers relying on polycarbonate panels to maintain controlled growing environments. Multiwall panel structures improve internal temperature regulation and light diffusion, enabling crop yield improvements of up to 15% in controlled cultivation environments. Transportation infrastructure and industrial safety structures collectively contribute about 14% of market usage. Polycarbonate panels are used in transit shelters, noise barriers along highways, and protective barriers in industrial facilities due to their strong mechanical resistance.

Greenhouse agriculture is currently the fastest-growing application segment, expanding at an estimated CAGR of approximately 4.6% as global demand for climate-controlled farming increases. The remaining applications, including signage, sports stadium roofing, and commercial atrium structures, account for roughly 7% of total market demand.

Construction companies represent the leading end-user segment in the polycarbonate panels market, accounting for approximately 49% of total demand. Builders and infrastructure developers increasingly incorporate polycarbonate panels in commercial roofing systems, skylight structures, and facade designs due to their strong impact resistance and energy-efficient properties. Modern office buildings and industrial warehouses frequently utilize multiwall panels that improve insulation efficiency while maintaining high levels of natural daylight penetration. Agricultural operators represent the second-largest end-user group, accounting for nearly 30% of installations. Greenhouse growers and agricultural technology firms use polycarbonate panels to maintain stable environmental conditions and optimize crop productivity. Multiwall greenhouse panels can reduce internal temperature fluctuations by nearly 20%, making them ideal for controlled agricultural environments. Industrial manufacturing and transportation infrastructure sectors collectively account for approximately 15% of the market. These industries rely on polycarbonate panels for protective barriers, safety glazing, transit shelters, and noise barrier systems along highways and rail networks.

Agricultural greenhouse developers represent the fastest-growing end-user segment, expanding at an estimated CAGR of about 4.8% as global investments in protected agriculture increase. The remaining niche end-users, including sports facility developers, retail complexes, and signage manufacturers, together contribute around 6% of overall market demand.

Region Asia-Pacific accounted for the largest market share at 41% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2026 and 2033.

The Asia-Pacific polycarbonate panels market continues to expand due to large-scale construction activities and infrastructure modernization across China, India, Japan, and Southeast Asia. China alone represents nearly 48% of regional consumption, driven by high demand for industrial roofing panels, greenhouse structures, and urban transport shelters. India has recorded more than 12 million square meters of polycarbonate panel installations annually across commercial building projects and agricultural greenhouses. In North America, over 32% of commercial skylight installations now incorporate polycarbonate sheets due to their high durability and light transmission efficiency exceeding 80%. Europe holds approximately 27% of global installations, supported by energy-efficient building regulations and sustainable construction materials. Meanwhile, the Middle East & Africa and South America together contribute nearly 14% of global demand, largely fueled by infrastructure investments, stadium developments, and modern greenhouse agriculture projects.

How Is Sustainable Infrastructure Modernization Accelerating Adoption of Advanced Roofing Materials?

North America accounts for approximately 24% of the global polycarbonate panels market, supported by large-scale commercial construction, transportation infrastructure modernization, and advanced agricultural greenhouse projects. The United States dominates regional consumption with nearly 78% of North American demand, while Canada contributes about 14%, driven by agricultural greenhouse expansions exceeding 2,000 hectares of controlled cultivation facilities. Construction and architectural glazing industries are major demand drivers, with polycarbonate panels replacing glass in nearly 35% of newly installed skylight systems due to their superior impact resistance and lightweight properties. Government policies promoting energy-efficient buildings have accelerated the use of high-insulation multiwall polycarbonate panels capable of reducing internal heat transfer by nearly 30%. Digital construction technologies such as automated panel fabrication and 3D structural modeling are improving installation precision by approximately 20% across large commercial projects. A notable regional player, Palram Americas, has expanded its manufacturing capacity for multiwall polycarbonate panels used in stadium roofing and industrial buildings, increasing production output by nearly 15% in recent years. Consumer behavior across the region indicates higher adoption in industrial infrastructure, commercial real estate, and greenhouse agriculture sectors where durable, weather-resistant materials are increasingly prioritized.

How Are Sustainability Regulations Transforming Demand for Advanced Transparent Roofing Systems?

Europe represents nearly 27% of the global polycarbonate panels market, with Germany, the United Kingdom, France, and Italy serving as the primary demand centers. Germany alone accounts for approximately 31% of regional installations, driven by energy-efficient building regulations and strong adoption of lightweight polymer construction materials. The region’s strict sustainability frameworks encourage developers to adopt recyclable materials, with nearly 42% of new commercial building skylights incorporating polycarbonate panels due to their energy-saving properties. European greenhouse agriculture is another major demand segment, covering more than 210,000 hectares of controlled cultivation area across the Netherlands, Spain, and France. Polycarbonate multiwall panels are widely used in greenhouse roofing systems to improve light diffusion efficiency by nearly 18%. Regulatory initiatives supporting low-carbon construction materials have further strengthened market growth. A notable regional manufacturer, Brett Martin, has introduced advanced multiwall polycarbonate panels designed for high-performance architectural glazing and roofing systems. European consumers increasingly prioritize sustainable construction materials, recyclable polymers, and energy-efficient roofing technologies, leading to a steady rise in adoption across industrial facilities and modern office infrastructure.

What Is Driving Massive Industrial and Agricultural Adoption of Lightweight Polymer Panels?

Asia-Pacific is the largest regional market by volume, accounting for more than 41% of global polycarbonate panel consumption. China leads regional demand with nearly 48% of total installations, followed by India at approximately 18% and Japan at around 11%. Rapid urbanization and infrastructure development projects exceeding USD 1 trillion in combined investment across major economies have significantly increased demand for durable construction materials including polycarbonate roofing systems. The region has also seen rapid expansion of greenhouse agriculture, particularly in China and India, where more than 320,000 hectares of greenhouse cultivation facilities rely on advanced polycarbonate roofing to maintain stable temperature and humidity levels. Manufacturing innovation hubs in China, Japan, and South Korea are improving polymer extrusion technologies capable of producing panels with up to 200 times the impact resistance of glass. Regional manufacturers such as Gallina India have expanded their polycarbonate panel production lines to support growing infrastructure demand. Consumer behavior across the region shows strong adoption among industrial developers, agricultural producers, and urban infrastructure planners seeking cost-efficient and durable building materials.

How Is Infrastructure Expansion Creating New Demand for Impact-Resistant Building Materials?

South America accounts for approximately 8% of global polycarbonate panel installations, with Brazil and Argentina representing the largest markets. Brazil alone contributes nearly 52% of regional consumption, largely driven by commercial construction projects, sports infrastructure developments, and agricultural greenhouse installations. Argentina holds around 19% of regional demand, supported by expanding greenhouse vegetable cultivation covering more than 4,500 hectares of protected farming areas. Infrastructure modernization across urban transport systems has increased demand for polycarbonate panels used in transit shelters, pedestrian walkways, and noise barrier installations. Polycarbonate roofing systems are now used in approximately 22% of newly constructed bus terminals and stadium renovation projects across major cities. Regional trade policies supporting domestic polymer manufacturing have also encouraged investment in local panel fabrication facilities. Consumer adoption patterns indicate strong demand from agriculture, retail construction, and stadium infrastructure developers seeking durable materials capable of withstanding extreme weather conditions while maintaining high optical transparency.

Why Are Climate-Resilient Building Materials Becoming Essential for Modern Infrastructure?

The Middle East & Africa region contributes roughly 6% of global polycarbonate panel consumption, supported by major construction developments and climate-resilient infrastructure investments. The United Arab Emirates and Saudi Arabia together represent nearly 47% of regional demand, largely driven by large-scale commercial developments, airport terminals, and stadium roofing structures. South Africa accounts for approximately 18% of installations, particularly in agricultural greenhouses and commercial skylight applications. Extreme climate conditions across the region require materials capable of withstanding high temperatures exceeding 45°C, making UV-protected polycarbonate panels a preferred alternative to glass roofing. Urban development projects across the Gulf Cooperation Council countries have increased installation of transparent polymer roofing systems in commercial buildings by nearly 25% over the past five years. Regional construction firms are increasingly adopting digital design tools and prefabricated panel systems that reduce installation time by nearly 30%. Consumer behavior in the region shows strong demand from infrastructure developers, greenhouse agriculture operators, and retail mall builders seeking durable, lightweight roofing materials.

China – 29% share in the Polycarbonate Panels market: Strong manufacturing capacity and large-scale infrastructure construction projects drive high domestic consumption of polycarbonate roofing and greenhouse panels.

United States – 21% share in the Polycarbonate Panels market: Extensive commercial construction activity and advanced greenhouse agriculture drive strong demand for high-performance polycarbonate panels.

The polycarbonate panels market features a moderately fragmented competitive environment with over 80 active manufacturers operating across global and regional markets. The top five companies collectively control approximately 36% of the global market, while the remaining share is distributed among mid-sized regional manufacturers and specialized polymer sheet producers. Competition is primarily driven by product innovation, manufacturing capacity expansion, and strategic partnerships with construction material distributors.

Leading manufacturers are increasingly investing in advanced extrusion technology capable of producing multiwall panels with enhanced insulation properties and improved UV resistance. Several companies have introduced high-performance polycarbonate sheets with light transmission rates exceeding 85% while maintaining impact resistance up to 200 times stronger than glass. Industry participants are also developing recyclable polymer panel solutions that reduce environmental impact and support sustainable building practices.

Strategic collaborations between polymer manufacturers and construction material distributors have increased product availability across emerging markets. Mergers and joint ventures are also expanding global production capacity to meet rising demand from greenhouse agriculture and commercial infrastructure projects. In addition, companies are implementing automated manufacturing systems that improve production efficiency by nearly 20%, strengthening competitive positioning across large infrastructure and construction sectors.

Covestro AG

SABIC

Palram Industries Ltd.

Brett Martin Ltd.

Gallina S.p.A.

Plazit-Polygal Group

Arla Plast AB

Trinseo PLC

Exolon Group

Koscon Industrial S.A.

Technological innovation is transforming the polycarbonate panels market by improving structural performance, energy efficiency, and long-term durability of polymer construction materials. Modern multiwall polycarbonate panel technology now incorporates triple-layer and five-layer internal structures, which enhance thermal insulation and reduce heat transfer by up to 30% compared with single-layer polymer sheets. These advanced internal chambers trap air, creating a highly efficient insulating barrier for greenhouse roofs and commercial skylight systems.

UV-resistant co-extrusion technology has become a critical advancement in outdoor polycarbonate applications. Modern panels now include a protective UV layer that can extend product lifespan beyond 15 years, reducing material degradation by nearly 40% compared with earlier polymer roofing systems. This technology has significantly improved the performance of polycarbonate panels in high-temperature climates and high-UV exposure regions.

Automation and digital manufacturing are also reshaping production processes. Advanced extrusion lines now operate at speeds exceeding 20 meters per minute, enabling manufacturers to produce large-scale panels with consistent thickness tolerances below ±0.1 millimeters. Precision CNC cutting systems allow manufacturers to deliver pre-fabricated panels customized for modular construction projects, reducing installation time by nearly 30%.

Nanotechnology coatings are another emerging development in the market. Anti-scratch and self-cleaning coatings improve surface durability and reduce maintenance requirements for skylight panels used in large commercial buildings. Some next-generation coatings can reduce dust accumulation by approximately 35%, helping maintain optical clarity and natural lighting efficiency. Additionally, flame-retardant polycarbonate materials are being developed to meet strict building safety standards in commercial infrastructure projects, further expanding the application scope of advanced polymer panels.

• In March 2025, Covestro AG expanded its Makrolon® polycarbonate sheet portfolio with improved UV-resistant grades designed for architectural glazing and skylight applications. The new materials enhance weather durability and maintain high optical clarity under long-term outdoor exposure. Source: www.covestro.com

• In September 2024, SABIC introduced new LEXAN™ polycarbonate sheet solutions aimed at sustainable construction projects. The materials incorporate recycled polymer content and improved thermal insulation performance, supporting energy-efficient building designs and durable transparent roofing systems. Source: www.sabic.com

• In May 2024, Brett Martin Ltd. launched a new multiwall polycarbonate roofing system designed for commercial skylights and industrial buildings. The product features enhanced light diffusion and improved insulation properties, supporting sustainable building performance and natural lighting optimization.

• In November 2024, Palram Industries Ltd. introduced upgraded Sunlite® multiwall polycarbonate panels engineered for greenhouse structures and architectural roofing. The panels provide improved UV protection and high impact resistance while maintaining light transmission levels exceeding 80% for agricultural and commercial installations.

The Polycarbonate Panels Market Report provides a comprehensive analysis of global industry dynamics, focusing on key product categories, application sectors, geographic markets, and technological developments shaping the industry landscape. The report evaluates multiple product segments including multiwall polycarbonate panels, solid polycarbonate sheets, corrugated panels, and specialized engineered polymer panels designed for industrial and architectural applications. These product categories collectively support diverse industries ranging from construction and agriculture to transportation infrastructure and industrial safety systems.

The report examines application-based demand patterns across commercial construction, greenhouse agriculture, industrial roofing, skylight installations, transportation infrastructure, and noise barrier systems. Construction remains the largest application area with more than 50% of polycarbonate panel installations linked to commercial buildings, warehouses, and modern architectural structures. Agricultural greenhouse applications represent a rapidly expanding segment, with global greenhouse cultivation covering more than 500,000 hectares, many of which utilize polycarbonate roofing systems for light diffusion and temperature stability.

Geographically, the report analyzes market performance across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, covering over 25 key countries that represent major consumption hubs. The study highlights regional infrastructure investments, greenhouse agriculture expansion, and energy-efficient construction policies influencing market demand.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

2.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Covestro AG, SABIC, Palram Industries Ltd., Brett Martin Ltd., Gallina S.p.A., Plazit-Polygal Group, Arla Plast AB, Trinseo PLC, Exolon Group, Koscon Industrial S.A. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |