Reports

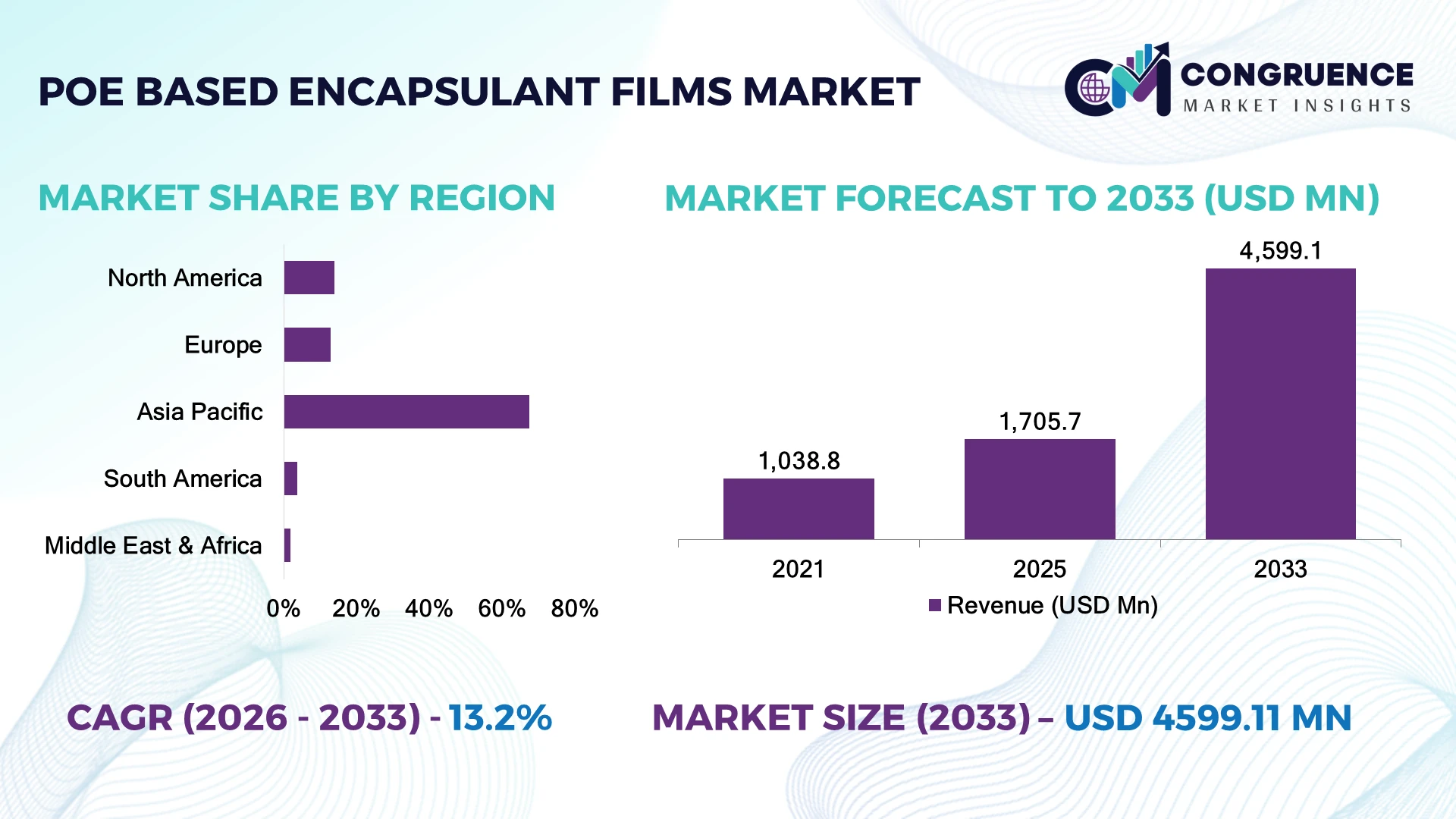

The Global POE-based Encapsulant Films Market was valued at USD 1,705.7 Million in 2025 and is anticipated to reach a value of USD 4,599.1 Million by 2033 expanding at a CAGR of 13.2% between 2026 and 2033. Growth is being driven by accelerating deployment of TOPCon and HJT solar modules, increasing bifacial photovoltaic installations, and rising demand for low-moisture, PID-resistant encapsulation materials.

China accounts for approximately 63% of global POE-based encapsulant film production capacity, supported by integrated photovoltaic manufacturing clusters, large-scale polymer processing, and sustained investments in high-efficiency solar module technologies. More than 72% of newly commissioned TOPCon module production lines in China utilize POE-based encapsulant films, while India is rapidly expanding domestic solar manufacturing under production-linked incentive programs. Ongoing supply-chain diversification following global trade realignments continues encouraging localized production and strategic capacity expansion across Asia.

Manufacturers investing in advanced film technology, regional production capacity, and integrated photovoltaic supply chains will secure stronger competitive positioning.

Market Size & Growth: USD 1,705.7 million in 2025, projected to reach USD 4,599.1 million by 2033 at 13.2% CAGR, driven by high-efficiency photovoltaic module deployment.

Top Growth Drivers: TOPCon adoption (+28%), bifacial module installations (+24%), and utility-scale solar expansion (+19%).

Short-Term Forecast: By 2028, encapsulation process efficiency is expected to improve by approximately 16% through advanced extrusion technologies.

Emerging Technologies: AI-enabled quality inspection, co-extrusion manufacturing, and ultra-low moisture barrier films enhance module reliability.

Regional Leaders: Asia-Pacific (~USD 2.8 billion), Europe (~USD 690 million), and North America (~USD 510 million) lead through manufacturing expansion and solar deployment.

Consumer/End-User Trends: Nearly 69% of high-efficiency photovoltaic modules increasingly adopt POE-based encapsulant films.

Pilot/Case Example: In 2026, automated co-extrusion lines improved production throughput by approximately 18% while reducing material waste.

Competitive Landscape: Leading manufacturers collectively hold nearly 54% market share through innovation, capacity expansion, and integrated supply chains.

Regulatory & ESG Impact: Low-carbon manufacturing initiatives reduce production emissions by approximately 14% while supporting clean-energy targets.

Investment & Funding: More than USD 1.2 billion has been committed toward encapsulant film expansion and photovoltaic material manufacturing.

Innovation & Future Outlook: Advanced multilayer films and next-generation encapsulation technologies continue strengthening global photovoltaic performance.

POE-based encapsulant films are witnessing stronger demand across TOPCon, HJT, and bifacial solar modules where moisture resistance and long-term durability directly influence energy output. Multilayer film innovations improve module reliability by approximately 20%, while localized photovoltaic material production is expanding amid evolving trade policies and resilient supply-chain strategies. These developments establish a strong foundation for the strategic assessment that follows.

POE-based encapsulant films have become strategically important as solar manufacturers transition toward higher-efficiency photovoltaic technologies requiring superior moisture resistance, electrical insulation, and long-term module reliability. Supply-chain diversification, domestic manufacturing incentives, and accelerating renewable energy infrastructure investments are reshaping competition, encouraging material suppliers to expand production capacity and strengthen regional manufacturing networks.

Compared with conventional EVA encapsulant films, advanced POE-based films reduce potential-induced degradation and improve moisture barrier performance by approximately 25%, extending module durability under demanding operating conditions. China continues leading manufacturing scale through vertically integrated photovoltaic production, while Europe emphasizes premium-quality materials and sustainability-focused module manufacturing. Over the next two to three years, nearly 45% of newly commissioned TOPCon and heterojunction production lines are expected to standardize POE-based encapsulation for high-performance solar modules.

A practical example is the expansion of automated multilayer film extrusion facilities designed to supply next-generation photovoltaic manufacturers with customized encapsulation materials. Companies are increasing investments in advanced polymer formulations, strategic partnerships with module producers, and regional manufacturing expansion to improve delivery reliability and product differentiation. Organizations capable of combining material innovation, manufacturing scale, and supply-chain resilience will secure lasting competitive advantages as next-generation solar technologies become the industry standard.

The rapid commercialization of TOPCon, HJT, and bifacial photovoltaic modules is accelerating demand for POE-based encapsulant films due to their superior moisture resistance and electrical insulation properties. More than 74% of newly commissioned TOPCon manufacturing lines now specify POE encapsulation, while bifacial module production has expanded by approximately 26% over the past year. China's continued investment in integrated photovoltaic manufacturing and supportive renewable energy policies are strengthening material demand across the value chain. This technology transition is improving module durability and lowering degradation rates, prompting encapsulant manufacturers to expand multilayer film production, establish long-term supply agreements with module producers, and invest in advanced polymer formulations to strengthen competitive positioning in premium solar applications.

POE-based encapsulant film production remains highly dependent on specialty polyolefin resins and advanced extrusion materials, exposing manufacturers to feedstock price volatility and procurement concentration. Raw material expenses account for nearly 62% of total production costs, while specialty polymer prices have fluctuated by approximately 14% during recent supply-chain adjustments. Dependence on limited global resin suppliers continues affecting production planning, inventory management, and contract pricing, particularly for manufacturers outside China. These structural constraints pressure operating margins and delay capacity expansion. Companies are responding through diversified procurement strategies, localized resin partnerships, and long-term purchasing contracts while optimizing film formulations to reduce material intensity without compromising photovoltaic module performance.

The emergence of tandem solar cells, perovskite-silicon modules, and advanced back-contact technologies is creating new opportunities for specialized POE-based encapsulant films. Approximately 32% of next-generation photovoltaic pilot projects are evaluating advanced multilayer encapsulation structures to improve moisture protection and long-term reliability. India is accelerating domestic photovoltaic manufacturing through policy incentives, encouraging localized encapsulant production and integrated material ecosystems. Automated co-extrusion technologies improve material utilization by nearly 17%, reducing production waste while supporting customized film architectures. Manufacturers are expanding R&D programs, collaborating with solar module developers, and investing in next-generation encapsulation platforms to address evolving efficiency requirements and secure long-term supply partnerships.

Expanding production while maintaining consistent optical transparency, cross-linking performance, and film uniformity remains a significant execution challenge. Nearly 13% of high-performance encapsulant batches require additional quality validation before commercial deployment, increasing manufacturing complexity. Automated inline inspection has been adopted by fewer than 45% of global production facilities, limiting process consistency during rapid capacity expansion. As solar modules transition toward larger wafer formats and higher power outputs, tighter performance specifications intensify manufacturing requirements. Companies must strengthen precision extrusion capabilities, digital process monitoring, workforce training, and advanced testing infrastructure to deliver consistent product quality while supporting large-scale photovoltaic manufacturing and maintaining long-term customer confidence.

High-Performance Film Adoption Solar manufacturers are rapidly replacing conventional encapsulation materials with advanced POE films for TOPCon and bifacial modules. More than 68% of newly installed high-efficiency production lines now utilize POE-based encapsulation, reducing moisture-related degradation by approximately 22%. Companies are expanding dedicated production capacity and strengthening module manufacturer partnerships to secure premium supply agreements as efficiency expectations continue rising.

Automation Reshapes Production Lines Automated co-extrusion, AI-assisted thickness monitoring, and digital quality inspection are improving manufacturing precision. Production throughput has increased by nearly 18%, while material defects have declined by approximately 15%. Labor availability and quality consistency pressures are encouraging manufacturers to modernize extrusion facilities and integrate intelligent process control systems for higher operational efficiency.

Localized Manufacturing Networks Trade diversification and evolving renewable energy policies are driving investment in regional encapsulant production. India and Southeast Asia have attracted increasing manufacturing projects, reducing average delivery times by approximately 16% and lowering logistics dependency by nearly 13%. Companies are establishing local converting facilities and strategic resin partnerships to improve supply resilience and customer responsiveness.

Recyclability Gains Strategic Focus Module manufacturers are increasingly evaluating encapsulant materials that support improved recycling compatibility without compromising durability. Advanced polymer formulations have reduced processing waste by approximately 14% while improving material recovery potential by nearly 11%. Companies are investing in sustainable resin technologies, circular manufacturing initiatives, and collaborative development programs to align future photovoltaic production with evolving environmental and lifecycle requirements.

Single-layer POE encapsulant films accounted for approximately 61% of the market in 2025, maintaining leadership through their cost-effective manufacturing, excellent moisture resistance, and compatibility with TOPCon and bifacial photovoltaic modules. Their straightforward processing, stable lamination performance, and scalability across utility-scale solar projects continue driving widespread adoption. Nearly 68% of standard high-efficiency module production lines utilize single-layer POE films because they provide reliable electrical insulation while minimizing potential-induced degradation. Manufacturers continue expanding extrusion capacity and improving polymer formulations to enhance optical transmission and long-term module durability.

Multi-layer POE encapsulant films represent the fastest-growing segment as next-generation HJT, back-contact, and tandem solar cells require enhanced encapsulation performance and customized multilayer structures. Hybrid encapsulation configurations remain relevant where manufacturers balance performance with production costs for specific module architectures. Around 27% of newly announced encapsulant capacity additions are dedicated to advanced multilayer technologies, reflecting stronger investment in premium photovoltaic materials. Companies are increasing R&D, strengthening partnerships with module manufacturers, and introducing customized multilayer solutions to support higher-efficiency solar technologies.

Industry assessments published during 2026 indicate that advanced photovoltaic module manufacturers are increasingly specifying POE-based multilayer encapsulation to improve long-term moisture protection and module reliability for high-efficiency cell architectures.

TOPCon solar modules accounted for approximately 46% of total demand in 2025, supported by rapid manufacturing expansion and increasing deployment of high-efficiency photovoltaic systems. POE-based encapsulant films are widely adopted in TOPCon modules because of their superior moisture barrier performance, lower ionic contamination, and excellent compatibility with advanced cell structures. Nearly 73% of newly commissioned TOPCon manufacturing capacity incorporates POE encapsulation as manufacturers prioritize long-term module reliability and reduced degradation. Film suppliers are expanding production capacity while optimizing formulations for faster lamination and improved optical performance.

Heterojunction (HJT) modules represent the fastest-growing application due to rising adoption of premium solar technologies requiring advanced encapsulation materials with superior electrical insulation. Bifacial modules and back-contact photovoltaic systems continue expanding as developers seek higher energy yields under demanding operating environments. Approximately 24% of new encapsulant product development programs now target HJT and tandem photovoltaic technologies. Manufacturers are investing in automated coating, customized film structures, and collaborative product development to address evolving performance requirements across advanced solar module platforms.

According to 2025 enterprise findings from the global photovoltaic industry, POE encapsulant films have become the preferred material for an increasing share of newly commissioned TOPCon and heterojunction production lines due to superior long-term module reliability.

Solar module manufacturers held approximately 79% of the market in 2025, reflecting their direct integration of POE-based encapsulant films into high-efficiency photovoltaic production. Large-scale manufacturers require consistent film quality, stable supply, and compatibility with automated lamination equipment to support high-volume operations. Nearly 71% of premium module production is supplied through long-term procurement agreements, encouraging encapsulant producers to expand manufacturing capacity, improve quality assurance, and develop customized film solutions aligned with evolving cell technologies.

Photovoltaic OEMs producing next-generation premium modules represent the fastest-growing end-user segment as investment accelerates in TOPCon, HJT, and tandem technologies. Research institutes and pilot-line developers continue evaluating advanced encapsulation materials for future commercial deployment, while contract module manufacturers remain strategically important for regional supply flexibility. Approximately 29% of supplier investments now focus on customized formulations, technical support, and joint product development with premium module producers. Companies are strengthening strategic partnerships, localized manufacturing, and application engineering capabilities to secure long-term positions across the evolving photovoltaic ecosystem.

Industry deployment reviews conducted during 2026 indicate that vertically integrated solar module manufacturers continue increasing procurement of advanced POE encapsulant films to improve module durability, manufacturing consistency, and long-term field performance.

Asia-Pacific accounted for the largest market share at 67.4% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 14.1% between 2026 and 2033.

Advanced Solar Manufacturing Strengthens Premium Encapsulation Demand

North America is expanding its position through rapid investments in domestic solar module manufacturing, utility-scale renewable energy deployment, and localized photovoltaic supply chains. The region accounts for approximately 14% of global demand, supported by increasing adoption of TOPCon and heterojunction modules requiring advanced POE encapsulant films. Nearly 48% of newly announced solar manufacturing projects in the United States include high-efficiency module production lines utilizing POE-based encapsulation materials. Manufacturers are strengthening long-term procurement agreements, investing in localized film conversion facilities, and collaborating with photovoltaic OEMs to improve supply resilience while reducing dependence on imported encapsulation materials. These developments are reinforcing regional competitiveness across advanced photovoltaic manufacturing.

United States Market Outlook: The United States leads regional demand through expanding solar manufacturing capacity, supportive clean-energy policies, and increasing deployment of utility-scale photovoltaic projects. More than 55% of recently commissioned domestic module production capacity is designed for TOPCon and other next-generation cell technologies requiring advanced encapsulation materials. Companies are expanding integrated supply partnerships, investing in automated lamination technologies, and strengthening domestic material sourcing to support large-scale solar manufacturing.

Sustainable Module Manufacturing Drives Material Innovation

Europe represents approximately 13% of global demand, supported by premium photovoltaic manufacturing, decarbonization initiatives, and stringent product quality standards. Solar manufacturers increasingly prioritize POE-based encapsulant films for their superior durability and compatibility with high-efficiency module architectures. Nearly 41% of premium photovoltaic production facilities have upgraded encapsulation processes to support next-generation cell technologies. Companies continue investing in sustainable polymer processing, advanced film engineering, and localized material partnerships to improve supply security while aligning with circular manufacturing objectives.

Germany Market Outlook: Germany remains Europe's strategic manufacturing hub for advanced photovoltaic technologies, supported by strong engineering capabilities and specialized materials expertise. Approximately 36% of the region's high-efficiency module manufacturing capacity is linked to German production facilities. Companies are expanding pilot manufacturing lines, investing in advanced encapsulation materials, and strengthening research partnerships focused on improving module longevity and operational efficiency.

Integrated Manufacturing Ecosystems Maintain Global Leadership

Asia-Pacific dominates the global market through vertically integrated photovoltaic manufacturing, extensive polymer processing infrastructure, and unmatched production scale. The region contributes approximately 67% of global demand while supplying the majority of POE-based encapsulant films used in TOPCon, HJT, and bifacial modules. More than 72% of newly commissioned encapsulant film production capacity during recent expansion cycles has been established within Asia-Pacific manufacturing clusters. Companies continue investing in automated co-extrusion facilities, upstream resin integration, and export-oriented production networks, strengthening operational efficiency and cost competitiveness across the global photovoltaic value chain.

China Market Outlook: China remains the industry's manufacturing powerhouse, accounting for more than 63% of global POE encapsulant film production capacity through highly integrated photovoltaic supply chains. Leading manufacturers continue expanding multilayer film extrusion facilities, increasing automation, and strengthening upstream polymer integration to support growing international demand. Continued investment in next-generation solar technologies reinforces China's long-term leadership in premium encapsulation materials.

Utility-Scale Solar Expansion Supports Material Demand

South America is experiencing steady demand growth as governments and private developers accelerate utility-scale photovoltaic installations across high-irradiance regions. The region contributes approximately 3.8% of global consumption, with increasing imports of advanced encapsulation materials supporting next-generation solar module deployment. Nearly 19% of recently commissioned utility-scale projects utilize high-efficiency module technologies requiring POE encapsulation. However, limited domestic material manufacturing continues to constrain regional supply independence. Companies are strengthening regional distribution networks, expanding technical partnerships, and improving inventory management to support project execution and minimize procurement delays.

Brazil Market Outlook: Brazil leads regional demand through its expanding solar generation capacity, favorable renewable energy policies, and large-scale photovoltaic investments. Nearly 47% of South America's utility-scale solar installations are concentrated in Brazil, encouraging suppliers to establish stronger local distribution capabilities and technical service networks. Continued expansion of domestic module assembly operations is creating additional demand for premium encapsulation materials.

Renewable Infrastructure Investments Accelerate Premium Material Adoption

The Middle East & Africa market is strengthening through expanding renewable energy investments, large-scale desert solar projects, and modernization of national energy infrastructure. The region accounts for approximately 1.8% of global demand, with increasing preference for POE-based encapsulant films in projects requiring enhanced heat and moisture resistance. Around 24% of newly planned utility-scale photovoltaic developments specify advanced encapsulation materials for improved long-term module performance under harsh environmental conditions. Companies are expanding regional supply partnerships, improving technical support capabilities, and strengthening logistics networks to support growing project pipelines.

Saudi Arabia Market Outlook: Saudi Arabia represents the region's most strategic market through ambitious renewable energy expansion, utility-scale photovoltaic investments, and localization initiatives supporting advanced energy manufacturing. More than 40% of large solar projects under development in the Gulf region are concentrated in Saudi Arabia. Suppliers are strengthening regional partnerships, expanding technical collaboration with EPC contractors, and positioning premium encapsulation materials to meet demanding desert operating conditions.

Competition is led by First, Sveck, Betterial, HIUV, and Cybrid, with the top five manufacturers collectively controlling approximately 76% of global encapsulant film shipments. First and Sveck compete through manufacturing scale, integrated supply chains, and product consistency, while Betterial and HIUV differentiate through advanced POE formulations and rapid overseas expansion. Cybrid strengthens its position through customized encapsulation solutions for premium TOPCon and heterojunction modules. Competition increasingly depends on technology, delivery reliability, and vertical integration rather than price alone. Automated co-extrusion improves production efficiency by nearly 18%, advanced multilayer films extend module durability by approximately 20%, and localized manufacturing reduces delivery cycles by around 15%. Companies are expanding overseas capacity, forming long-term supply partnerships with module manufacturers, and investing in next-generation encapsulation technologies. Rising qualification requirements for high-efficiency photovoltaic modules create significant entry barriers. Sustainable leadership requires innovation, manufacturing scale, supply security, and close integration with leading solar module producers.

First PV Material Co., Ltd.

Sveck Photovoltaic New Materials Co., Ltd.

Betterial Film Technologies

HIUV New Materials Co., Ltd.

Cybrid Technologies Inc.

Hangzhou First Applied Material Co., Ltd.

Guangzhou Lushan New Materials Co., Ltd.

Sinopont Technology Co., Ltd.

RenewSys India Pvt. Ltd.

Vishakha Renewables Pvt. Ltd.

STR Holdings, Inc.

Mitsui Chemicals, Inc.

POE-based encapsulant technology is advancing through multilayer co-extrusion, precision resin formulation, and AI-enabled quality inspection to meet the performance requirements of TOPCon, heterojunction, and back-contact solar modules. More than 70% of newly commissioned premium photovoltaic manufacturing lines incorporate advanced POE encapsulation, improving moisture resistance by approximately 25% while reducing potential-induced degradation. Automated inline inspection enhances production consistency by nearly 16%, enabling manufacturers to improve yield and shorten qualification cycles for high-efficiency module production.

Compared with conventional EVA encapsulation, advanced POE films deliver approximately 20% better long-term reliability and nearly 18% lower moisture permeability under demanding operating environments. Cross-linking optimization, multilayer architectures, and intelligent extrusion control are becoming competitive differentiators for manufacturers supplying premium photovoltaic modules. First, Sveck, Betterial, and HIUV benefit through stronger partnerships with TOPCon and heterojunction module producers, while vertically integrated suppliers gain operational advantages through stable resin sourcing and accelerated product development.

Between 2026 and 2028, encapsulation technology will increasingly focus on tandem solar cells, perovskite integration, recyclable polymer systems, and digital manufacturing platforms. Nearly 40% of planned production upgrades are expected to include intelligent process monitoring and advanced multilayer film technologies. Companies investing now will improve module performance, strengthen qualification success, enhance supply resilience, and secure preferred supplier status across next-generation photovoltaic manufacturing.

May 2025: RenewSys announced the addition of eight new encapsulant production lines, increasing planned manufacturing capacity to 30 GW across 19 lines. Business impact: strengthens global supply capability for EVA, EPE, and POE encapsulant films supporting high-efficiency solar modules. Source: RenewSys

August 2025: RenewSys signed a 700 MW POE encapsulant supply agreement with Kosol Energie for advanced solar projects in India. Business impact: reinforces long-term demand visibility and strengthens strategic partnerships within the domestic photovoltaic manufacturing ecosystem. Source: RenewSys

August 2025: HIUV announced accelerated international expansion through joint ventures in the United States and Turkey while targeting additional markets during 2025–2026. Business impact: improves localized manufacturing support and enhances global delivery capabilities. Source: pv magazine

November 2025: RenewSys secured a 1.1 GW POE encapsulant supply agreement with Kosol Energie covering deliveries through September 2026. Business impact: expands premium encapsulant adoption for high-efficiency module production and strengthens long-term production planning. Source: RenewSys.

The report provides comprehensive analysis of the global POE-based Encapsulant Films market across major product types, photovoltaic applications, end-user groups, and regional markets. It evaluates adoption across single-layer and multi-layer films, TOPCon, heterojunction, bifacial, and emerging tandem solar technologies while assessing procurement patterns among module manufacturers, OEMs, and research organizations. Regional analysis covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa with country-level competitive and operational assessments.

The study further examines advanced co-extrusion technology, multilayer encapsulation, automated quality inspection, polymer innovations, and evolving photovoltaic manufacturing strategies. More than 70% of premium solar module production trends evaluated in the report focus on high-efficiency cell architectures and advanced encapsulation requirements. The analysis supports investment planning, manufacturing expansion, supplier benchmarking, technology adoption, competitive positioning, and strategic decision-making for stakeholders participating in the global photovoltaic materials value chain between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1,705.7 Million |

|

Market Revenue in 2033 |

USD 4,599.1 Million |

|

CAGR (2026 - 2033) |

13.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

First PV Material Co., Ltd., Sveck Photovoltaic New Materials Co., Ltd., Betterial Film Technologies, HIUV New Materials Co., Ltd., Cybrid Technologies Inc., Hangzhou First Applied Material Co., Ltd., Guangzhou Lushan New Materials Co., Ltd., Sinopont Technology Co., Ltd., RenewSys India Pvt. Ltd., Vishakha Renewables Pvt. Ltd., STR Holdings, Inc., Mitsui Chemicals, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |