Reports

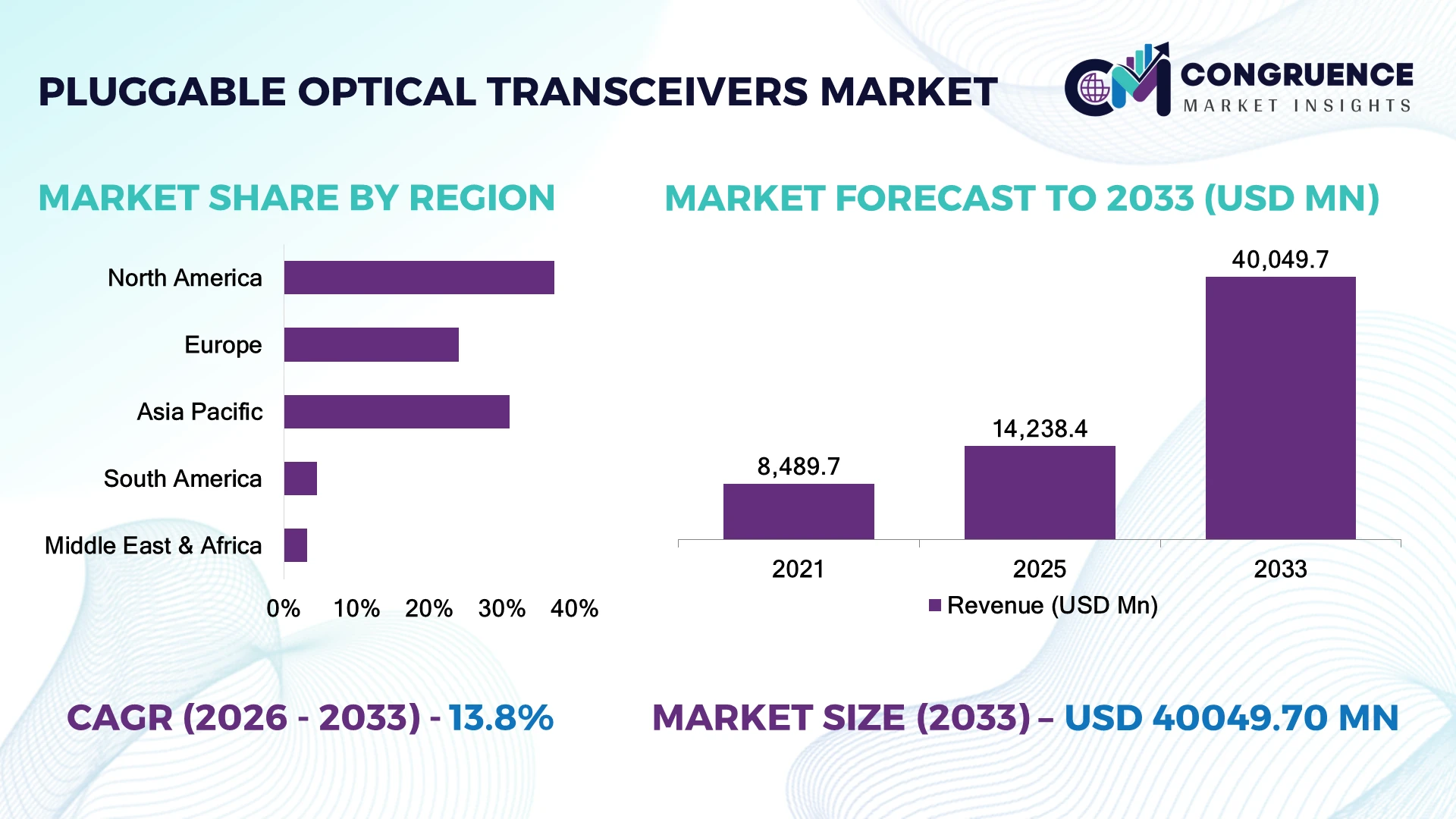

The Global Pluggable Optical Transceivers Market was valued at USD 14,238.4 Million in 2025 and is anticipated to reach a value of USD 40,049.7 Million by 2033 expanding at a CAGR of 13.8% between 2026 and 2033. Growing AI data center deployments, 800G network upgrades, hyperscale cloud expansion, and accelerating fiber infrastructure modernization are driving rapid adoption of high-speed pluggable optical transceivers.

The United States dominates the market with approximately 34% share, supported by hyperscale cloud operators, AI infrastructure investments, and advanced semiconductor ecosystems. More than 62% of newly deployed AI-ready data center interconnects utilize 400G and 800G pluggable optical modules. In comparison, China leads manufacturing capacity with nearly 48% of global optical transceiver production, benefiting from vertically integrated supply chains despite continuing geopolitical technology restrictions affecting advanced networking exports.

The market increasingly rewards suppliers capable of combining high-speed innovation, resilient manufacturing, and scalable optical networking solutions for next-generation digital infrastructure.

Market Size & Growth: USD 14,238.4 million in 2025 to USD 40,049.7 million by 2033 at 13.8% CAGR, driven by AI networking and hyperscale cloud expansion.

Top Growth Drivers: AI networking (+42%), 800G migration (+36%), cloud data center expansion (+31%).

Short-Term Forecast: By 2028, network power efficiency improves 18% while latency declines nearly 15%.

Emerging Technologies: 800G, 1.6T optics, silicon photonics, co-packaged optics accelerate deployment.

Regional Leaders: North America USD 14.1B, Asia-Pacific USD 13.6B, Europe USD 7.4B with expanding hyperscale adoption.

Consumer/End-User Trends: Nearly 69% of hyperscale deployments prioritize high-density pluggable optics.

Pilot/Case Example: 2026 AI cluster deployment improves network throughput by approximately 32%.

Competitive Landscape: Top supplier controls nearly 17%; Coherent, Innolight, Cisco, Lumentum, Broadcom remain influential.

Regulatory & ESG Impact: Energy-efficient optics reduce network power consumption by approximately 16%.

Investment & Funding: More than USD 4.8 billion supports photonics capacity expansion and strategic partnerships.

Innovation & Future Outlook: AI-driven optical networking and 1.6T modules redefine global high-performance connectivity.

Pluggable optical transceivers have become foundational for AI clusters, hyperscale cloud facilities, telecom backbone modernization, and enterprise data center upgrades. Silicon photonics integration and low-power DSP innovation improve transmission efficiency by approximately 24%, while diversified manufacturing strategies continue reducing supply-chain concentration risks. These technology shifts establish the foundation for the strategic market outlook discussed below.

High-speed optical connectivity has become a strategic infrastructure investment as AI computing, cloud-native applications, and ultra-low-latency networking redefine enterprise competitiveness. Operators are restructuring procurement strategies following supply-chain diversification initiatives and increasing investments in regional optical manufacturing. Demand is shifting beyond bandwidth expansion toward scalable, power-efficient networking platforms capable of supporting next-generation computing environments.

Modern 800G pluggable transceivers deliver approximately 38% higher bandwidth density while reducing energy consumption by nearly 22% compared with widely deployed 400G platforms. North America leads AI-driven deployments and advanced networking innovation, whereas Asia-Pacific maintains manufacturing leadership through large-scale photonics production and component integration. Over the next two to three years, adoption of 800G and early 1.6T modules is expected to accelerate across hyperscale facilities and carrier backbone networks.

Cloud operators increasingly deploy high-density optical interconnects to support GPU clusters, prompting suppliers to expand silicon photonics investment, strengthen manufacturing partnerships, and localize critical component production. Companies combining advanced optical design, manufacturing resilience, and rapid product commercialization will establish stronger competitive positioning as network infrastructure transitions toward AI-optimized, ultra-high-speed connectivity.

Rapid deployment of AI infrastructure and hyperscale cloud facilities is driving unprecedented demand for high-speed pluggable optical transceivers. Nearly 71% of newly commissioned AI data centers now deploy 400G and 800G optical interconnects, while advanced transceivers improve network bandwidth density by approximately 38% and reduce latency by nearly 19%. The United States continues expanding AI computing infrastructure through large-scale hyperscale investments, increasing procurement of high-performance optical modules for GPU clusters. This transition enables scalable, low-power optical connectivity while supporting exponential data traffic growth. Manufacturers are responding through silicon photonics investment, production capacity expansion, strategic DSP partnerships, and accelerated development of 1.6T pluggable platforms. A notable strategic shift is the growing preference for standardized pluggable architectures that shorten deployment cycles while simplifying future network upgrades.

Production of high-speed pluggable optical transceivers remains constrained by dependence on advanced DSP chips, indium phosphide lasers, and precision photonic packaging. Manufacturing lead times for certain 800G optical components remain approximately 18% longer than conventional modules, while advanced packaging increases production costs by nearly 16%. China's concentration in optical component manufacturing, alongside export controls affecting advanced semiconductor technologies, continues creating procurement uncertainty for global networking equipment suppliers. These structural limitations delay hyperscale deployment schedules, compress supplier margins, and complicate inventory planning. Companies are mitigating risk through regional manufacturing expansion, dual-sourcing strategies, long-term wafer agreements, and localized photonics assembly facilities that strengthen supply continuity and operational resilience.

Silicon photonics integration is creating significant opportunities for next-generation pluggable optical transceivers by improving bandwidth density, manufacturing efficiency, and power optimization. Approximately 59% of hyperscale operators are evaluating silicon photonics for future optical infrastructure, while integrated photonic architectures reduce module power consumption by nearly 21% compared with conventional designs. Japan continues investing in advanced photonics manufacturing and optical semiconductor innovation, strengthening commercialization of high-speed networking technologies. Vendors are increasing investment in co-packaged optics research, programmable optical engines, and strategic collaborations with cloud providers. An emerging opportunity lies in modular 1.6T transceivers that simplify network expansion without extensive switching infrastructure redesign, lowering long-term deployment costs for hyperscale operators.

Maintaining interoperability across diverse networking environments presents a long-term execution challenge as operators deploy higher-speed pluggable optical transceivers. Nearly 46% of enterprise networks continue operating mixed 100G, 400G, and 800G infrastructures, increasing integration complexity and extending deployment timelines by approximately 24%. Germany's industrial digitalization initiatives require seamless compatibility across multi-vendor optical networks, creating additional validation requirements for equipment suppliers. These challenges affect lifecycle management, operational consistency, and large-scale network modernization. Vendors must strengthen interoperability certification, firmware compatibility, optical diagnostics, and ecosystem collaboration while expanding software validation platforms and reference architectures. A decisive competitive advantage will belong to suppliers delivering standardized, vendor-neutral interoperability with simplified deployment across heterogeneous optical environments.

800G Deployment Accelerates Enterprise and hyperscale operators are rapidly transitioning to 800G optical transceivers, with deployment increasing approximately 41% and network throughput improving by nearly 35%. AI infrastructure expansion in the United States is accelerating upgrade cycles, prompting suppliers to expand manufacturing capacity, strengthen component partnerships, and optimize high-density module production for cloud-scale deployments.

Silicon Photonics Gains Momentum Silicon photonics adoption has expanded by approximately 33%, reducing module power consumption by nearly 20% while improving manufacturing scalability. Integrated photonic packaging simplifies high-speed transmission and lowers thermal constraints. Manufacturers are increasing automation, expanding photonic integration capabilities, and restructuring supply chains to support higher production efficiency and competitive differentiation.

AI Network Optimization Expands AI-driven optical network management improves traffic utilization by approximately 27% while reducing fault detection time by nearly 32%. Cloud operators increasingly deploy intelligent monitoring platforms that automate optical performance optimization. Vendors are integrating analytics software with pluggable modules, enabling predictive maintenance and improving network reliability across large-scale digital infrastructure.

1.6T Product Development Advances Development of 1.6T pluggable optical transceivers has accelerated, with prototype validation improving bandwidth density by approximately 45% while reducing rack-level power requirements by nearly 17%. Early hyperscale qualification programs are encouraging suppliers to strengthen semiconductor partnerships, automate assembly processes, and prepare manufacturing ecosystems for next-generation optical networking deployments.

QSFP28 transceivers accounted for approximately 34% of the market in 2025, maintaining leadership through broad deployment across 100G Ethernet infrastructure, hyperscale data centers, and carrier backbone networks. The form factor delivers an optimal balance of bandwidth density, interoperability, and deployment cost, enabling operators to modernize existing switching environments without significant hardware replacement. More than 64% of enterprise network upgrades continue utilizing QSFP28 because of its mature ecosystem, proven reliability, and compatibility with large installed network bases. Suppliers are strengthening product portfolios through lower-power DSP integration, improved thermal management, and enhanced interoperability validation to maximize lifecycle performance.

QSFP-DD represents the fastest-growing segment as AI infrastructure, cloud providers, and high-performance computing environments rapidly transition toward 400G and 800G optical networking. SFP and SFP+ remain strategically important for enterprise access, industrial networking, and legacy infrastructure, while OSFP continues expanding within ultra-high-density AI clusters requiring superior thermal efficiency. Approximately 41% of newly announced hyperscale optical deployments now prioritize QSFP-DD and OSFP platforms, prompting manufacturers to expand silicon photonics partnerships, automated production capacity, and next-generation optical module development to strengthen long-term competitiveness.

According to findings published by the Ethernet Alliance during 2025, hyperscale operators continue accelerating deployment of 400G and 800G Ethernet ecosystems, reinforcing demand for next-generation pluggable optical transceiver form factors across AI and cloud infrastructure.

Data centers accounted for approximately 46% of the market in 2025, making them the leading application due to continuous expansion of hyperscale cloud facilities, AI computing clusters, and high-performance storage networks. Large-scale deployments require low-latency, high-bandwidth optical interconnects capable of supporting dense switching architectures and increasing east-west traffic. Advanced pluggable optical transceivers improve bandwidth utilization by nearly 32% while reducing rack-level power consumption by approximately 18%, making them essential for next-generation digital infrastructure. Vendors continue expanding silicon photonics integration, automated optical testing, and manufacturing capacity to support increasing deployment volumes.

5G telecommunications infrastructure represents the fastest-growing application as operators expand fiber backhaul, edge computing, and transport network capacity. Enterprise networking and high-performance computing continue generating stable demand through campus modernization and AI-enabled workloads, while internet exchange points strengthen deployment of ultra-low-latency optical connectivity. Nearly 37% of recent optical networking projects combine cloud data center and edge network architectures, encouraging suppliers to develop scalable transceiver families with simplified interoperability, higher port density, and flexible deployment across multiple networking environments.

Industry analysis presented by the Optical Internetworking Forum (OIF) during 2026 highlighted continued expansion of interoperable 400ZR and 800ZR optical networking deployments, accelerating pluggable transceiver adoption across cloud and carrier infrastructures.

Cloud service providers held approximately 43% of the market in 2025, driven by continuous expansion of hyperscale data centers, AI computing clusters, and global cloud networking infrastructure. Their large-scale deployment requirements, high port density, and continuous bandwidth upgrades make them the largest buyers of advanced pluggable optical transceivers. More than 68% of newly commissioned hyperscale switching infrastructure now incorporates 400G or higher optical modules, encouraging suppliers to develop customized transceiver platforms, long-term supply agreements, and integrated validation services that support rapid deployment.

Telecom operators represent the fastest-growing end-user segment as nationwide fiber expansion, 5G transport modernization, and edge computing deployments accelerate optical network investment. Large enterprises, internet exchange providers, and government organizations continue modernizing mission-critical networking infrastructure with higher-speed optical connectivity. Approximately 29% of supplier investments now target operator-specific product customization, localized technical support, and strategic ecosystem partnerships, allowing vendors to strengthen long-term customer relationships while addressing evolving bandwidth and operational requirements across diverse deployment environments.

A 2025 enterprise networking assessment published by the Telecom Infra Project (TIP) indicated that hyperscale cloud providers and telecommunications operators remained the largest adopters of high-speed pluggable optical networking technologies, driven by AI infrastructure expansion and large-scale network modernization initiatives.

North America accounted for the largest market share at 37.2% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.1% between 2026 and 2033.

AI Infrastructure Investment Reinforces High-Speed Optical Network Leadership

North America remains the largest regional market, supported by hyperscale cloud expansion, AI data center deployment, and continuous upgrades to high-capacity optical networking infrastructure. The region contributes approximately 37% of global demand, with leading cloud providers accelerating migration toward 400G and 800G optical interconnects. Nearly 72% of newly commissioned AI-ready data centers deploy high-speed pluggable optical transceivers as standard networking infrastructure, improving bandwidth density and operational efficiency. Ongoing investment in domestic semiconductor manufacturing and advanced photonics strengthens supply resilience, while networking vendors continue expanding manufacturing partnerships, optical module validation programs, and silicon photonics integration to support enterprise-scale deployments.

United States Market Outlook: The United States dominates regional demand through its concentration of hyperscale cloud operators, AI infrastructure developers, and advanced networking equipment manufacturers. More than 68% of North America's hyperscale optical networking deployments originate from U.S.-based facilities, supported by expanding GPU clusters and cloud campuses. Companies continue strengthening domestic optical manufacturing, packaging capabilities, and long-term procurement agreements to secure high-speed connectivity for next-generation digital infrastructure.

Network Modernization Strengthens Optical Connectivity Investments

Europe maintains a strong market position through accelerated fiber network upgrades, cloud infrastructure expansion, and enterprise digital transformation initiatives. The region accounts for approximately 24% of global demand, supported by growing adoption of high-speed optical networking across telecommunications, research networks, and industrial digitalization projects. Nearly 61% of newly deployed metro optical infrastructure incorporates pluggable transceiver technologies supporting 400G migration and higher network efficiency. Equipment manufacturers continue investing in energy-efficient optical modules, automated testing platforms, and localized engineering support to strengthen competitiveness.

Germany Market Outlook: Germany leads the regional market through its advanced industrial networking ecosystem, telecommunications infrastructure, and enterprise digital manufacturing initiatives. Major data centers and industrial operators continue upgrading high-capacity optical backbone networks, while nearly 44% of large enterprise network modernization projects incorporate next-generation pluggable optical transceivers. Suppliers are expanding regional engineering centers and optical integration capabilities to support complex enterprise networking requirements.

Manufacturing Scale and Cloud Expansion Accelerate Market Momentum

Asia-Pacific represents the fastest-growing regional market due to its extensive optical component manufacturing base, expanding hyperscale cloud infrastructure, and large-scale 5G deployment. The region contributes approximately 31% of global market demand while accounting for nearly half of worldwide optical transceiver manufacturing capacity. More than 66% of newly established cloud facilities across key economies are designed around 400G-ready optical architectures. Continuous investment in photonics manufacturing, semiconductor packaging, and fiber infrastructure strengthens regional competitiveness while supporting global supply chains.

China Market Outlook: China serves as the region's largest production and consumption hub through vertically integrated optical component manufacturing, large domestic cloud providers, and extensive telecommunications investment. Approximately 48% of global optical transceiver manufacturing capacity is concentrated in China, supported by advanced photonics production ecosystems. Domestic manufacturers continue expanding silicon photonics capabilities, automated assembly facilities, and export-oriented production to strengthen competitiveness across international networking markets.

Telecom Infrastructure Upgrades Drive Optical Deployment

South America is experiencing steady adoption of pluggable optical transceivers as telecom operators modernize backbone networks, expand fiber connectivity, and increase cloud infrastructure investment. The region contributes approximately 4.6% of global demand, with network operators prioritizing higher-capacity optical transport for enterprise and consumer broadband services. Optical network deployment across major metropolitan corridors has increased by nearly 18%, improving bandwidth availability while supporting digital transformation initiatives. Infrastructure limitations and dependence on imported networking equipment continue influencing deployment costs, encouraging suppliers to strengthen regional distribution and technical support capabilities.

Brazil Market Outlook: Brazil leads regional demand through its extensive telecommunications infrastructure, expanding cloud data center ecosystem, and nationwide fiber deployment programs. Nearly 43% of South America's hyperscale data center capacity is concentrated in Brazil, encouraging higher adoption of advanced pluggable optical transceivers. Vendors continue strengthening channel partnerships, technical certification programs, and local inventory management to improve supply continuity and customer responsiveness.

Digital Infrastructure Investments Expand High-Speed Connectivity

The Middle East & Africa market is advancing through accelerated digital infrastructure investment, hyperscale data center development, and nationwide fiber broadband expansion. The region represents approximately 3.2% of global demand while increasing deployment of high-capacity optical transport networks supporting cloud services, smart cities, and enterprise digitalization. Around 22% of recently announced digital infrastructure projects incorporate advanced optical networking technologies to enhance transmission efficiency and scalability. Vendors are expanding regional partnerships, optical integration capabilities, and technical service networks to strengthen long-term market presence.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through sustained investment in hyperscale data centers, digital economy initiatives, and international connectivity infrastructure. Advanced cloud facilities and carrier-neutral data centers continue increasing deployment of 400G optical networking platforms, with optical infrastructure investments expanding by approximately 20% across strategic technology zones. Equipment suppliers are strengthening regional engineering support, solution integration, and ecosystem partnerships to address rising enterprise and cloud networking requirements.

Competition is led by Coherent Corp., Lumentum Holdings, Cisco Systems, Broadcom, and Accelink Technologies, with the top five players collectively controlling approximately 56% of the global market. Global technology leaders compete through silicon photonics, DSP integration, and hyperscale partnerships, while Asian manufacturers challenge primarily on manufacturing scale and cost efficiency. Competition increasingly centers on performance-per-watt, delivery speed, and supply reliability rather than pricing alone. Vendors offering 1.6T-ready platforms deliver nearly 22% lower power consumption, while vertically integrated manufacturers shorten production lead times by approximately 18% and improve delivery reliability by around 15%. Companies are expanding photonics capacity, partnering with cloud providers, integrating critical optical components, and accelerating AI-focused product roadmaps. Competitive momentum is shifting toward silicon photonics and co-packaged optics, raising technology and capital barriers for new entrants. Winning increasingly requires advanced optical integration, secure component supply, rapid qualification cycles, and deep hyperscale customer relationships.

Coherent Corp.

Lumentum Holdings Inc.

Cisco Systems, Inc.

Broadcom Inc.

Accelink Technologies Co., Ltd.

Eoptolink Technology Inc., Ltd.

InnoLight Technology

Applied Optoelectronics, Inc.

Fujitsu Optical Components Limited

Sumitomo Electric Industries, Ltd.

Source Photonics Holdings (Cayman) Limited

Intel Corporation

Silicon photonics has become the defining technology for next-generation pluggable optical transceivers by combining photonic integration with advanced CMOS manufacturing. Approximately 58% of newly developed hyperscale optical modules incorporate silicon photonics, improving power efficiency by nearly 20% while increasing bandwidth density. AI-ready cloud infrastructure is accelerating deployment of 800G and early 1.6T transceivers, encouraging suppliers to integrate advanced DSPs, automated optical calibration, and compact thermal management for higher operational efficiency.

Compared with conventional discrete optical architectures, integrated silicon photonics platforms reduce component count by approximately 30% and improve manufacturing consistency by nearly 25%. Co-packaged optics, 3 nm and emerging 2 nm DSP technologies, and 224G electrical lanes are becoming key differentiators for suppliers targeting AI clusters. Technology leaders such as Coherent, Lumentum, Broadcom, and Marvell benefit through stronger hyperscale design wins, while vertically integrated manufacturers achieve faster qualification and improved supply resilience.

Between 2026 and 2028, commercial deployment will increasingly shift toward 1.6T transceivers, programmable coherent optics, and AI-optimized optical engines. More than 45% of hyperscale operators are expected to evaluate 1.6T migration programs during this period, creating opportunities for vendors investing in silicon photonics, advanced packaging, and automated manufacturing. Companies that accelerate innovation today will secure long-term supply agreements, improve deployment scalability, and strengthen competitive positioning as optical networking becomes the foundation of AI infrastructure.

March 2026: Coherent demonstrated next-generation 1.6T and 3.2T pluggable optical transceiver technologies featuring multiple silicon photonics and InP architectures for AI data centers, expanding support for diverse DSP platforms and future 12.8T networking ecosystems. Business impact: strengthens leadership in next-generation AI optical connectivity. Source: Coherent

March 2026: Marvell introduced the industry's first 1.6T ZR/ZR+ pluggable solution with a 2 nm coherent DSP, enabling secure AI data-center interconnects and lower-power long-haul optical networking. Business impact: accelerates commercial adoption of ultra-high-speed coherent pluggable optics. Source: Marvell

March 2025: Coherent showcased a silicon photonics-based 1.6T-DR8 transceiver using Marvell's 3 nm DSP, reducing projected power dissipation by more than 20% compared with existing architectures. Business impact: improves AI data-center energy efficiency and increases deployment readiness. Source: Coherent

February 2025: STMicroelectronics announced commercialization of a silicon photonics chip co-developed with Amazon Web Services for AI data-center optical transceivers, with production planned in France. Business impact: strengthens Europe's integrated photonics manufacturing ecosystem and future transceiver supply chain. Source: Reuters

The report provides comprehensive analysis of the global Pluggable Optical Transceivers market across major types, applications, end-users, and regional markets, covering evolving deployment patterns between 100G, 400G, 800G, and emerging 1.6T technologies. It evaluates demand across data centers, telecommunications, enterprise networking, and high-performance computing while assessing adoption by cloud service providers, telecom operators, enterprises, and government organizations. Regional assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with country-level strategic insights for major technology hubs.

The study further examines competitive positioning, technology evolution, silicon photonics integration, coherent optics, advanced DSP platforms, supply-chain developments, and interoperability trends. More than 50% of the analysis focuses on emerging AI-driven networking deployments and next-generation optical connectivity, enabling stakeholders to evaluate expansion opportunities, investment priorities, product strategies, partnership potential, competitive benchmarking, and long-term market direction across the 2026–2033 forecast period.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 14,238.4 Million |

|

Market Revenue in 2033 |

USD 40,049.7Million |

|

CAGR (2026 - 2033) |

13.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Coherent Corp., Lumentum Holdings Inc., Cisco Systems, Inc., Broadcom Inc., Accelink Technologies Co., Ltd., Eoptolink Technology Inc., Ltd., InnoLight Technology, Applied Optoelectronics, Inc., Fujitsu Optical Components Limited, Sumitomo Electric Industries, Ltd., Source Photonics Holdings (Cayman) Limited, Intel Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |