Reports

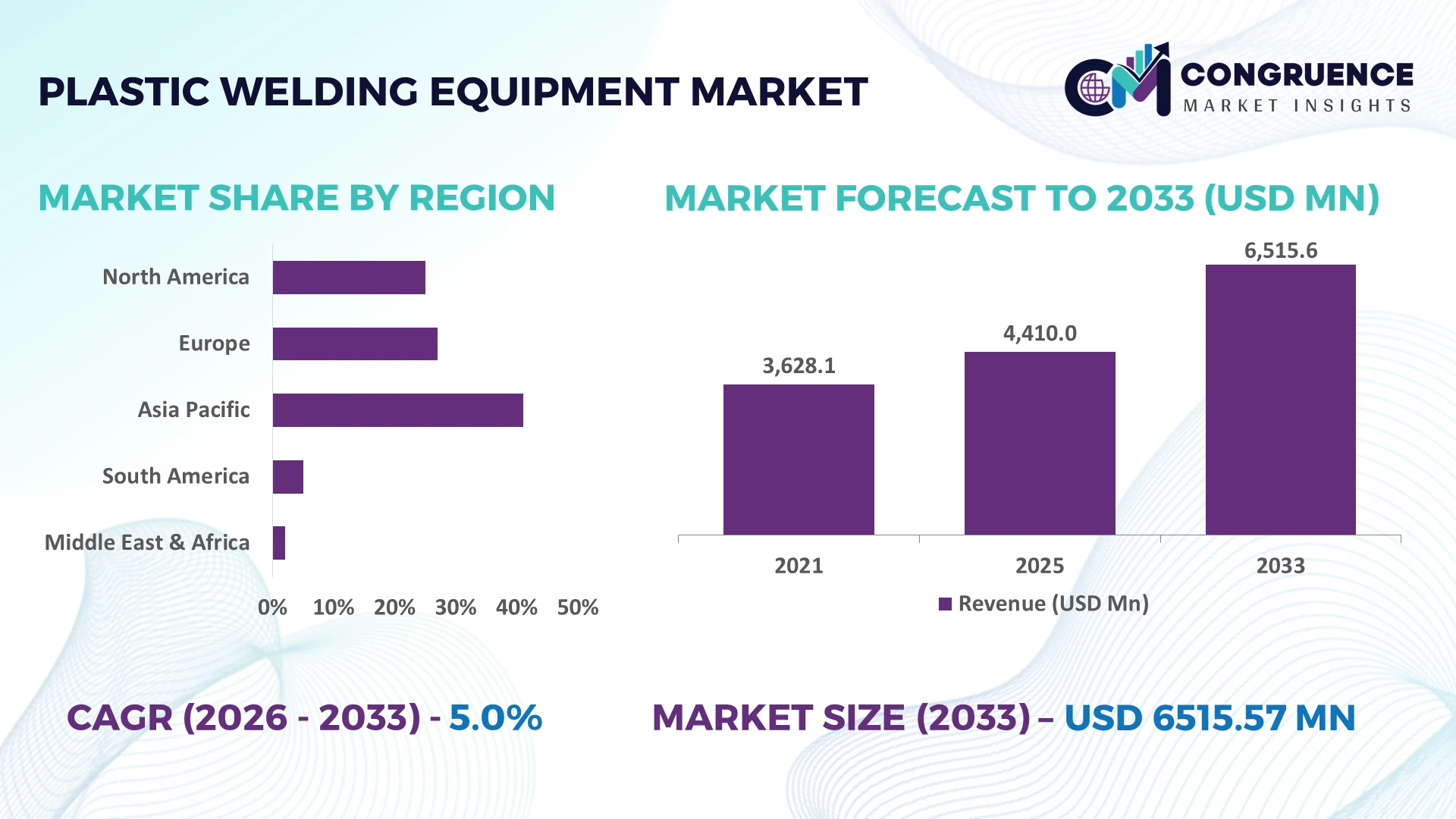

The Global Plastic Welding Equipment Market was valued at USD 4410 Million in 2025 and is anticipated to reach a value of USD 6515.57 Million by 2033 expanding at a CAGR of 5% between 2026 and 2033. Growing electrified vehicle production, medical-grade polymer manufacturing, and automated packaging lines are accelerating demand for high-precision plastic welding equipment with integrated process monitoring and energy-efficient operation.

China remains the dominant manufacturing hub, accounting for approximately 34% of global thermoplastic processing capacity, supported by large-scale automotive, electronics, and medical device production alongside continued industrial automation investments. Germany maintains stronger high-precision equipment penetration, with over 70% of industrial plastic joining systems integrated into advanced production environments. Ongoing supply-chain diversification following Red Sea shipping disruptions has further strengthened regional manufacturing resilience and equipment localization strategies.

Manufacturers prioritizing automation-ready, digitally monitored welding platforms and regional production footprints are positioned to strengthen long-term competitiveness across high-value industrial applications.

Market Size & Growth: USD 4410 Million in 2025, reaching USD 6515.57 Million by 2033 at 5% CAGR, driven by automated polymer processing and advanced manufacturing expansion.

Top Growth Drivers: EV component production (+24%), medical plastics demand (+18%), and automated packaging investments (+21%) continue accelerating equipment adoption.

Short-Term Forecast: By 2028, automated welding platforms improve production efficiency by 19% while reducing material waste by 14% across industrial facilities.

Emerging Technologies: AI-assisted quality inspection, ultrasonic automation, and digital process monitoring improve weld consistency by over 20% in high-volume manufacturing.

Regional Leaders: Asia-Pacific exceeds USD 2800 Million, Europe approaches USD 1700 Million, and North America surpasses USD 1300 Million through advanced industrial automation and regional expansion.

Consumer/End-User Trends: More than 62% of automotive and medical manufacturers prioritize precision plastic joining for lightweight, high-performance assemblies.

Pilot/Case Example: In 2025, an automated production upgrade improved welding cycle efficiency by 23% while reducing defect rates by 16%.

Competitive Landscape: Leading suppliers collectively control approximately 42% of the global market, with competition centered on automation, precision engineering, and digital integration.

Regulatory & ESG Impact: Energy-efficient welding systems reduce electricity consumption by nearly 18%, supporting stricter industrial sustainability and manufacturing compliance targets.

Investment & Funding: More than USD 1.2 Billion in manufacturing modernization supports automation partnerships, regional production expansion, and resilient supply-chain strategies.

Innovation & Future Outlook: Smart connected welding equipment, predictive maintenance, and closed-loop quality control accelerate next-generation industrial production across high-growth manufacturing sectors.

Plastic Welding Equipment Market demand continues expanding across automotive battery systems, medical device manufacturing, electronics assembly, and industrial packaging where precision joining is essential. AI-enabled quality monitoring and servo-controlled welding platforms improve process consistency by nearly 20%, while manufacturers increasingly regionalize production to strengthen supply-chain resilience amid evolving industrial regulations, creating a strong foundation for long-term strategic investment and competitive positioning.

Plastic welding equipment has become a strategic manufacturing asset as industries prioritize lightweight components, automated production, and consistent joining quality across automotive, healthcare, electronics, and packaging applications. Supply-chain restructuring after recent logistics disruptions has encouraged manufacturers to regionalize production and shorten equipment delivery cycles, while stricter product quality requirements are accelerating investment in digitally controlled welding systems capable of traceable, repeatable operations.

Modern servo-controlled ultrasonic welding equipment delivers approximately 22% higher process consistency while reducing energy consumption by nearly 18% compared with conventional pneumatic systems. Germany continues to lead precision manufacturing and digital integration, whereas China deploys larger production volumes through high-capacity industrial clusters serving electric vehicles and consumer electronics. Over the next two to three years, factory-level adoption of connected process monitoring is expected to exceed 45% among newly installed industrial welding lines, strengthening predictive maintenance and production visibility.

Medical device manufacturers deploying automated laser welding have reduced inspection time by nearly 20% while improving weld repeatability across high-volume production. Equipment suppliers are expanding localized engineering support, investing in software-enabled platforms, and forming automation partnerships to accelerate deployment. Companies combining intelligent process control, flexible manufacturing capabilities, and regional service networks will secure stronger competitive positioning as industrial production becomes increasingly digital and quality driven.

Rapid automation across manufacturing and increasing use of engineered thermoplastics are reshaping equipment procurement priorities. Electric vehicle production has expanded by more than 25% in several major manufacturing countries, while automated assembly lines have improved production throughput by nearly 20%. Japan and China continue investing in smart manufacturing facilities equipped with digitally controlled welding platforms to improve process repeatability. In response, equipment manufacturers are expanding automation portfolios, integrating machine vision, and partnering with robotics suppliers to deliver complete production cells. The strategic advantage increasingly lies in supplying flexible, high-precision welding solutions capable of handling multiple polymer grades while minimizing downtime and production variation.

Price fluctuations in electronic control systems and precision ultrasonic components continue affecting equipment manufacturing costs, with selected industrial components experiencing volatility exceeding 15% during procurement cycles. Many small manufacturers still operate legacy production lines where interoperability between older machinery and modern digital welding platforms remains below 40%. Germany and Italy face additional challenges from specialized component sourcing and extended lead times for high-precision assemblies. Companies are responding by localizing component procurement, negotiating long-term supplier agreements, and redesigning equipment around standardized modules. Strengthening procurement resilience has become essential for protecting margins and maintaining predictable production schedules.

Integration of artificial intelligence, machine connectivity, and real-time quality analytics is creating significant competitive opportunities beyond traditional equipment sales. Connected production systems reduce unplanned maintenance by approximately 25% while improving first-pass weld quality by nearly 18%. South Korea is accelerating smart factory adoption through industrial digitalization initiatives, encouraging manufacturers to deploy intelligent joining technologies. Equipment suppliers are increasing investment in software platforms, cloud-based diagnostics, and collaborative robotics partnerships to deliver value-added production ecosystems. The strongest opportunity lies in transitioning from standalone machinery toward digitally connected manufacturing solutions that generate recurring service and optimization revenues.

The growing complexity of connected production environments presents significant execution challenges for manufacturers deploying advanced welding technologies. Integrating welding equipment with enterprise manufacturing software increases implementation timelines by approximately 20%, while skilled industrial automation technicians remain in short supply across several manufacturing economies. The United States continues experiencing workforce constraints as demand for digital manufacturing expertise outpaces training capacity. Companies must strengthen engineering partnerships, invest in workforce development, and standardize communication protocols across production assets. Organizations that successfully integrate software, automation, and operator expertise will achieve superior deployment consistency, operational resilience, and long-term industrial competitiveness.

Smart Process Control Expansion Intelligent welding platforms with AI-assisted parameter optimization and inline quality monitoring are becoming standard across advanced production lines. More than 48% of newly installed industrial systems now incorporate digital process monitoring, reducing rework by approximately 17% and shortening production setup times by 15%. Manufacturers are expanding software capabilities and automation partnerships as labor shortages and stricter quality compliance accelerate factory digitalization.

Localized Manufacturing Footprints Supply-chain restructuring is driving equipment suppliers to establish regional assembly and service operations closer to industrial customers. Local sourcing initiatives have reduced component lead times by nearly 20%, while spare-part availability has improved by around 18% in key manufacturing hubs. Companies are restructuring distribution networks and increasing localized engineering support to strengthen operational resilience against logistics disruptions and geopolitical trade uncertainty.

Precision Welding for Medical Applications Medical device manufacturers are increasing deployment of laser and ultrasonic plastic welding to satisfy stricter validation and traceability requirements. Automated inspection systems improve weld consistency by nearly 21% while reducing manual inspection activity by approximately 16%. Equipment suppliers are responding through application-specific product development, validation partnerships, and integrated quality documentation for regulated manufacturing environments.

Energy-Efficient Equipment Adoption Industrial facilities are replacing conventional pneumatic equipment with servo-controlled welding technologies that lower electricity consumption by roughly 18% and improve cycle stability by 14%. Japan and Germany continue accelerating energy-efficient factory modernization, encouraging suppliers to redesign equipment around predictive maintenance, modular architecture, and lower operating costs. A less obvious shift is customer preference for lifecycle efficiency over initial equipment price.

Ultrasonic Welders remain the leading product category because they combine high production speed, repeatable weld quality, and seamless integration into automated manufacturing lines. Nearly 46% of high-volume plastic component assembly lines rely on ultrasonic technology due to short cycle times and minimal material consumption. Hot Plate Welders maintain strong demand for larger thermoplastic components requiring durable structural joints, while Vibration Welders continue serving automotive applications where high-strength weld integrity is essential. Manufacturers are strengthening ultrasonic product portfolios through digital controls, process analytics, and robotic integration.

Laser Welders represent the fastest-growing type as manufacturers prioritize precision joining for medical devices, electronics, and premium automotive assemblies. Adoption of laser-based systems has increased by approximately 19% across high-value manufacturing environments where minimal thermal distortion is critical. Spin Welders continue supporting rotational plastic assemblies with cost-efficient production performance. Equipment suppliers are expanding application engineering capabilities and investing in modular machine architectures, reflecting a strategic shift toward flexible production systems capable of serving multiple industrial sectors.

Automotive Components represent the largest application segment as manufacturers increasingly replace metal assemblies with lightweight thermoplastics to improve vehicle efficiency and simplify production. Approximately 41% of industrial plastic welding installations support automotive manufacturing, where consistent weld quality and automation compatibility remain essential. Packaging continues expanding through high-speed production requirements, while Industrial Manufacturing sustains demand for durable plastic assemblies across machinery and infrastructure applications. Equipment suppliers are scaling automation-ready platforms to support higher throughput and reduced quality variation.

Medical Devices are the fastest-growing application because stringent product validation, traceability, and contamination control requirements favor non-contact and precision welding technologies. Deployment of automated welding equipment within regulated medical production has expanded by nearly 18%, while Consumer Electronics manufacturers continue increasing adoption of compact precision systems for miniaturized assemblies. Companies are introducing application-specific welding platforms, integrated inspection technologies, and customized tooling to strengthen operational flexibility and capture specialized manufacturing opportunities.

Automotive remains the dominant end-user because large-scale vehicle manufacturing requires reliable, repeatable joining of lightweight polymer components across interior, exterior, and battery-related assemblies. Nearly 43% of industrial purchasing activity originates from automotive manufacturers investing in automated production cells and digital quality monitoring. Industrial Manufacturing follows with broad deployment across equipment production, while Electronics manufacturers continue increasing demand for compact, high-precision welding systems supporting miniaturized product designs. Equipment suppliers are expanding customized automation packages and long-term service agreements for high-volume manufacturers.

Healthcare is the fastest-growing end-user segment as regulated production environments require contamination-free joining, documented process validation, and consistent weld integrity. Automated equipment utilization within healthcare manufacturing has increased by approximately 20%, while Packaging companies continue modernizing production to improve speed and reduce operational waste. Vendors are strengthening market positions through application-focused engineering, localized technical support, strategic partnerships, and flexible equipment configurations tailored to specific production environments, reinforcing long-term customer relationships and operational efficiency.

Asia-Pacific accounted for the largest market share at 44% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a 6.4% CAGR between 2026 and 2033.

Advanced Manufacturing Automation Strengthens Industrial Competitiveness

North America maintains a strong position through advanced manufacturing infrastructure, widespread industrial automation, and high adoption of precision plastic joining across automotive, healthcare, aerospace, and electronics production. The region represents approximately 25% of global deployment, supported by continuous modernization of manufacturing facilities and increasing demand for digitally monitored welding platforms. More than 55% of newly commissioned industrial production cells integrate automated joining technologies with robotic handling and quality monitoring. Equipment suppliers continue expanding engineering partnerships and localized technical services to improve implementation speed while supporting reshoring initiatives and higher manufacturing resilience across critical industries.

United States Market Outlook: The United States leads regional demand through its large automotive, medical device, and industrial manufacturing base supported by advanced automation investment. More than 60% of large manufacturing facilities upgrading plastic assembly operations now prioritize digitally controlled welding equipment with integrated process monitoring. Domestic manufacturers continue expanding smart factory deployment, strengthening supplier partnerships, and investing in predictive maintenance capabilities that improve production consistency and operational flexibility.

Precision Engineering and Sustainable Production Drive Modernization

Europe remains a technology-driven market where precision manufacturing, sustainability objectives, and stringent industrial quality standards shape equipment investment decisions. The region accounts for nearly 23% of global market activity, with Germany, Italy, and France leading deployment across automotive, medical technology, and industrial engineering sectors. Factory modernization initiatives have increased installation of energy-efficient welding systems by approximately 18%, while manufacturers continue integrating digital quality assurance into automated production lines. Equipment suppliers are emphasizing modular system architecture, lifecycle efficiency, and long-term service partnerships to support increasingly sophisticated manufacturing environments.

Germany Market Outlook: Germany serves as the region's industrial technology leader with strong capabilities in automotive engineering, industrial machinery, and production automation. Approximately 70% of advanced polymer component manufacturing facilities operate highly automated assembly systems incorporating precision welding technologies. German manufacturers continue strengthening Industry 4.0 implementation through digital process validation, collaborative robotics, and intelligent production management, reinforcing their leadership in high-value manufacturing.

Large-Scale Manufacturing Accelerates Technology Deployment

Asia-Pacific dominates the market through unmatched manufacturing capacity, expanding electronics production, and rapid industrial automation across automotive, packaging, and consumer goods sectors. The region contributes approximately 44% of global market demand, supported by extensive production infrastructure and rising investment in intelligent manufacturing systems. Automated plastic welding deployment across major industrial facilities has expanded by nearly 22% as manufacturers improve productivity and product consistency. Companies continue increasing local equipment production, strengthening regional supply chains, and investing in smart manufacturing technologies to support export-oriented industries and domestic industrial expansion.

China Market Outlook: China remains the most influential country due to its extensive plastics processing ecosystem, automotive production scale, and electronics manufacturing leadership. Nearly one-third of global thermoplastic processing capacity is concentrated within the country, creating sustained demand for high-performance welding equipment. Chinese manufacturers continue expanding automation investment, integrating AI-enabled inspection systems, and strengthening domestic equipment development to improve production efficiency and reduce dependence on imported industrial technologies.

Industrial Diversification Supports Equipment Adoption

South America continues expanding plastic welding equipment deployment through automotive production, packaging modernization, and industrial manufacturing diversification. The region accounts for approximately 5% of global demand, with investment increasingly directed toward production automation and operational efficiency improvements. Manufacturing facilities implementing automated joining technologies have reported productivity improvements of nearly 15%, particularly in packaging and consumer product assembly. Infrastructure limitations and uneven industrial investment remain operational constraints, prompting equipment suppliers to expand distributor networks, localized maintenance capabilities, and technical training programs that improve long-term equipment utilization.

Brazil Market Outlook: Brazil leads regional demand through its established automotive, packaging, and industrial manufacturing sectors supported by expanding factory modernization initiatives. More than 45% of industrial automation investments within advanced manufacturing facilities include production equipment upgrades focused on improving quality consistency and reducing manual operations. Manufacturers continue strengthening local partnerships, expanding technical support capacity, and adopting flexible automation solutions suited to diverse production requirements.

Industrial Modernization Expands Manufacturing Investment

Middle East & Africa is experiencing increasing demand as governments diversify industrial production and strengthen domestic manufacturing capabilities beyond traditional resource sectors. The region represents approximately 3% of global market activity, supported by industrial parks, healthcare manufacturing expansion, and infrastructure modernization projects. Deployment of automated production technologies has increased by nearly 17% across selected manufacturing investments, while industrial diversification strategies continue encouraging adoption of advanced joining equipment. Equipment suppliers are responding through regional partnerships, technical service expansion, and localized engineering support to improve implementation efficiency and long-term operational reliability.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region's primary growth center through large-scale industrial diversification, manufacturing localization, and infrastructure investment programs. More than 20% of newly announced advanced manufacturing projects incorporate automated production technologies supporting plastics processing and industrial assembly. Companies continue expanding regional partnerships, workforce training initiatives, and localized engineering capabilities to strengthen domestic manufacturing competitiveness and improve technology adoption across industrial sectors.

The market is led by Herrmann Ultrasonics, Dukane, Branson, Leister Technologies, and Emerson, competing directly against regional equipment manufacturers and specialized automation integrators. The top five players collectively account for approximately 42% of global market activity, while regional suppliers compete aggressively through lower pricing and localized engineering support. Global leaders differentiate through digital process control, precision welding performance, and integrated automation, whereas cost-focused manufacturers emphasize delivery speed and customized tooling. Automated welding platforms improve production consistency by nearly 20%, while predictive maintenance features reduce unplanned downtime by approximately 18%, making technology the primary competitive lever over pricing alone. Companies are expanding application centers, strengthening robotics partnerships, integrating software capabilities, and increasing localized manufacturing to shorten delivery cycles by nearly 15%. Competition is shifting toward intelligent production ecosystems rather than standalone equipment, driving selective consolidation and stronger vertical integration across software, tooling, and service networks. High engineering expertise, application validation capability, and established customer relationships remain significant entry barriers. Winning requires automation leadership, application-specific innovation, rapid technical support, and scalable manufacturing execution.

Herrmann Ultrasonics

Dukane

Emerson

Leister Technologies

Bielomatik

Frimo Group

CEMAS Elettra

Sonics & Materials

Forward Technology

LPKF Laser & Electronics

Mecasonic

Rinco Ultrasonics

TELSONIC AG

KIEFEL GmbH

Advanced automation is redefining plastic welding equipment through AI-enabled process optimization, closed-loop quality control, and intelligent sensor integration. More than 48% of newly installed industrial systems now include digital monitoring capabilities that improve weld consistency by approximately 21% while reducing manual inspection requirements by nearly 16%. Automotive, medical device, and electronics manufacturers benefit most because traceability and repeatable production have become competitive procurement requirements rather than optional capabilities.

Laser welding, servo-controlled ultrasonic systems, and machine vision are replacing conventional pneumatic equipment across high-value manufacturing. Compared with legacy systems, digitally controlled platforms reduce energy consumption by approximately 18% and improve process repeatability by nearly 22%. Adoption of collaborative robotics continues increasing, with automated welding cells now representing about 40% of new precision production deployments. Technology providers offering integrated software, analytics, and automation platforms gain stronger competitive positioning than equipment-only suppliers.

Between 2026 and 2028, predictive maintenance, digital twins, and cloud-connected production management will become core differentiators. Manufacturers investing in interoperable production ecosystems are expected to reduce unplanned downtime by nearly 25% while accelerating production changeovers by approximately 20%. Companies acting early will strengthen operational resilience, lower lifecycle costs, and secure preferred supplier status across advanced manufacturing industries where intelligent production capabilities increasingly determine long-term competitiveness.

June 2024 Herrmann Ultrasonics hosted its Ultrasonic TECH DAYS, bringing together around 150 customers from five continents to showcase next-generation ultrasonic welding innovations focused on automation, sustainability, and process optimization, strengthening collaborative product development and customer engagement.

October 2024 Herrmann Ultrasonics introduced enhanced digital ultrasonic welding capabilities capable of recording more than 150 process parameters per weld through its DataRecorder G3 platform, enabling higher traceability and improved manufacturing efficiency for battery and plastics applications. Source: herrmannultrasonics.com

March 2025 Leister Technologies transferred its laser plastic welding business to Hymson Novolas AG, establishing a new Laser Technology Center in Switzerland and ensuring continuity for globally installed systems while sharpening Leister's strategic focus on core plastic welding technologies. Source: leister.com

February 2025 Herrmann Ultrasonics announced a new Tech Center in Monterrey, Mexico, featuring more than 150 m² of laboratory and application engineering space to support regional manufacturers with testing, training, and localized technical services, strengthening customer proximity and deployment capabilities. Source: herrmannultrasonics.com

The report provides comprehensive analysis across Hot Plate Welders, Ultrasonic Welders, Laser Welders, Spin Welders, and Vibration Welders, together with detailed assessment of Automotive Components, Medical Devices, Packaging, Consumer Electronics, and Industrial Manufacturing applications. It evaluates demand across Automotive, Healthcare, Packaging, Electronics, and Industrial Manufacturing end-users while examining competitive positioning across more than five major regional markets. Operational trends, automation adoption, digital manufacturing integration, and precision joining technologies are analyzed alongside deployment patterns exceeding 45% within advanced manufacturing environments.

The study delivers strategic intelligence covering technology evolution, production modernization, supply-chain transformation, and industrial automation between 2026 and 2033. It evaluates competitive benchmarking, regional investment priorities, enterprise expansion strategies, and innovation pipelines while highlighting emerging opportunities in smart manufacturing, AI-enabled process monitoring, laser welding, and connected production ecosystems. The report supports investment planning, product portfolio optimization, geographic expansion, partnership evaluation, and long-term competitive positioning through actionable, industry-focused market intelligence.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 4410 Million |

Market Revenue in 2033 | USD 6515.57 Million |

CAGR (2026 - 2033) | 5% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Herrmann Ultrasonics, Dukane, Emerson, Leister Technologies, Bielomatik, Frimo Group, CEMAS Elettra, Sonics & Materials, Forward Technology, LPKF Laser & Electronics, Mecasonic, Rinco Ultrasonics, TELSONIC AG, KIEFEL GmbH |

Customization & Pricing | Available on Request (10% Customization is Free) |