Reports

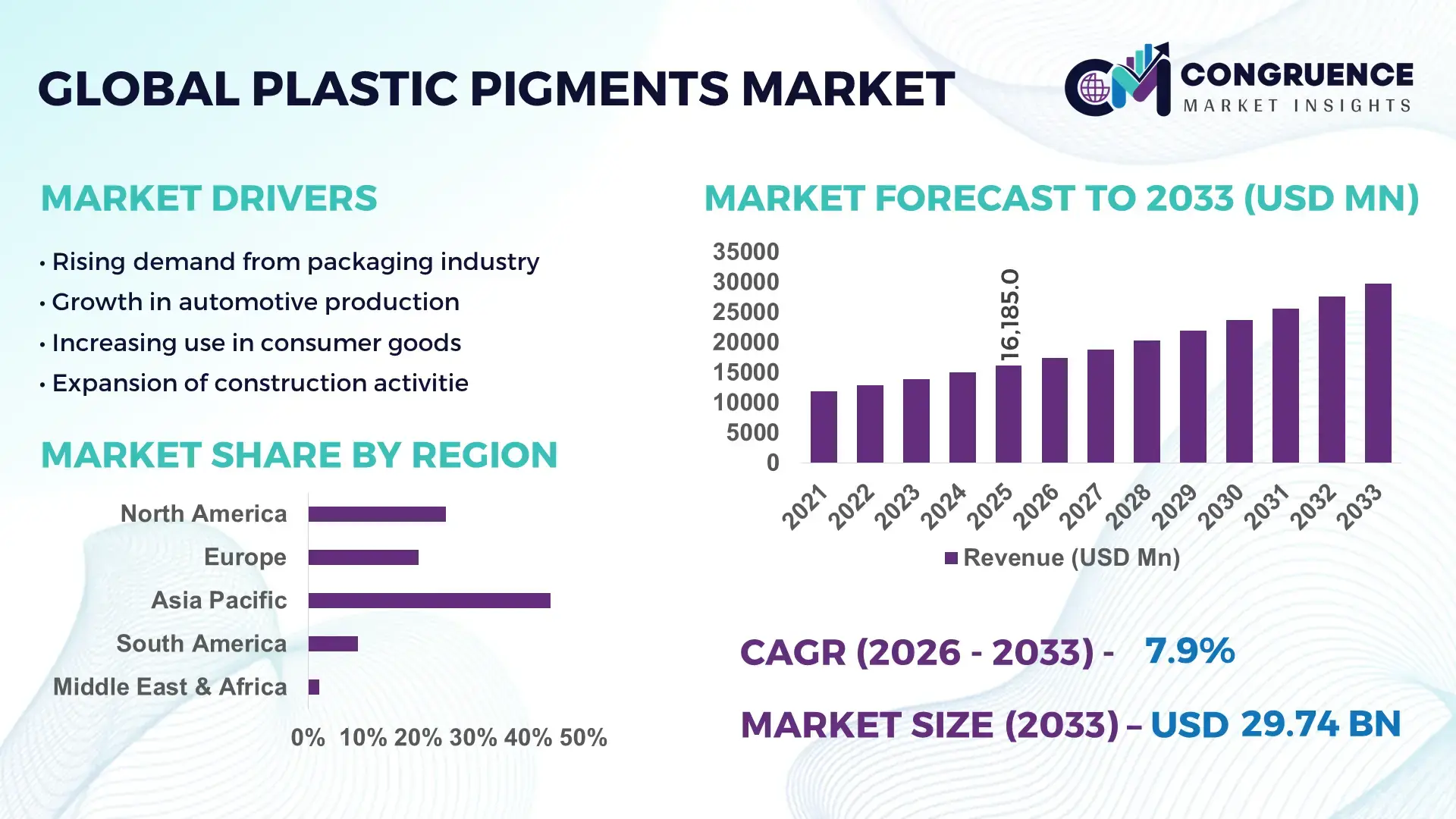

The Global Plastic Pigments Market was valued at USD 16185 Million in 2025 and is anticipated to reach a value of USD 29736.11 Million by 2033 expanding at a CAGR of 7.9% between 2026 and 2033. The growth is primarily driven by rising demand for high-performance plastics across packaging, automotive, and construction industries.

China remains the dominant country in the plastic pigments market, supported by its extensive polymer manufacturing ecosystem and strong export-oriented production capacity. The country produces over 35% of the world’s plastics, with pigment consumption closely tied to packaging and consumer goods applications, which account for more than 40% of domestic pigment usage. Investments exceeding USD 5 billion in advanced polymer processing zones and pigment dispersion technologies have strengthened its manufacturing capabilities. Additionally, China’s automotive sector, producing over 26 million vehicles annually, significantly contributes to pigment demand for durable and UV-resistant plastic components. Technological advancements such as nano-dispersion pigment processing and high-temperature resistant colorants are increasingly being adopted, improving production efficiency by approximately 18% and enhancing product durability.

Market Size & Growth: Valued at USD 16185 Million in 2025, projected to reach USD 29736.11 Million by 2033 at a CAGR of 7.9%, driven by expanding packaging and automotive applications.

Top Growth Drivers: Packaging demand growth at 32%, automotive lightweighting adoption at 27%, and construction plastics usage increase at 24%.

Short-Term Forecast: By 2028, advanced pigment dispersion technologies are expected to reduce processing costs by 15% and improve color consistency by 20%.

Emerging Technologies: Nano-pigments, bio-based pigments, and high-performance UV-resistant colorants are transforming product innovation.

Regional Leaders: Asia-Pacific projected at USD 13 billion by 2033 with strong manufacturing demand; Europe at USD 7.8 billion with sustainability-driven adoption; North America at USD 6.5 billion driven by advanced polymer technologies.

Consumer/End-User Trends: Packaging accounts for over 38% of usage, followed by automotive at 22% and construction at 18%, with increasing preference for recyclable and eco-friendly pigments.

Pilot or Case Example: In 2024, a polymer manufacturer improved pigment dispersion efficiency by 21%, reducing material waste by 17% through AI-driven mixing systems.

Competitive Landscape: Market leader holds approximately 14% share, with key players including major global pigment and chemical manufacturers.

Regulatory & ESG Impact: Stringent environmental regulations are pushing adoption of low-VOC and heavy metal-free pigments, with compliance rates exceeding 60% in developed regions.

Investment & Funding Patterns: Over USD 2.3 billion invested in sustainable pigment technologies and recycling-compatible colorants in recent years.

Innovation & Future Outlook: Integration of smart pigments and recyclable polymer-compatible colorants is expected to redefine product performance and sustainability benchmarks.

The plastic pigments market continues to evolve with strong contributions from packaging, automotive, and construction sectors, which collectively account for over 75% of total demand. Recent advancements in organic pigments and bio-based alternatives are reducing environmental impact while maintaining performance standards. Regulatory pressures across Europe and North America are accelerating the shift toward heavy metal-free pigments, while Asia-Pacific leads in consumption due to rapid industrialization. Emerging trends such as digital color matching systems and AI-driven pigment formulation are improving production accuracy and reducing waste, positioning the market for sustained innovation and efficiency gains.

The plastic pigments market holds strong strategic relevance as industries increasingly prioritize product differentiation, sustainability, and material efficiency. Advanced pigment technologies such as nano-pigments deliver nearly 25% improvement in color dispersion compared to conventional pigment formulations, enhancing product aesthetics and durability. This performance advantage is particularly critical in sectors like automotive and consumer electronics, where visual quality and resistance to environmental factors are key competitive differentiators. Asia-Pacific dominates in production volume due to its extensive polymer manufacturing base, while Europe leads in sustainable pigment adoption, with over 65% of enterprises transitioning toward eco-friendly and recyclable pigment solutions. The increasing regulatory focus on environmental compliance has accelerated innovation in low-VOC and non-toxic pigment formulations, with companies committing to reduce hazardous pigment content by up to 40% by 2028.

In the short term, by 2028, AI-driven pigment formulation and automated dispersion technologies are expected to improve production efficiency by 20% while reducing raw material waste by 15%. These advancements are enabling manufacturers to achieve consistent quality at scale while minimizing operational costs. For example, in 2024, a leading manufacturing hub in Germany achieved a 19% reduction in energy consumption through the integration of smart pigment processing systems, demonstrating measurable sustainability gains.

From an ESG perspective, firms are aligning with circular economy goals, targeting up to 50% recyclability in pigment-compatible plastics by 2030. This includes innovations in bio-based pigments derived from renewable sources, which are gaining traction across packaging applications. The plastic pigments market is increasingly positioned as a critical enabler of product innovation, regulatory compliance, and sustainable material development, reinforcing its role as a foundational pillar for resilient and future-ready industrial growth.

The growing demand for high-performance plastics across industries such as automotive, packaging, and construction is a key driver of the plastic pigments market. In the automotive sector, lightweight plastic components now account for nearly 50% of vehicle volume, requiring durable and heat-resistant pigments. Similarly, the global packaging industry, which consumes over 40% of total plastic production, relies heavily on pigments for branding and product differentiation. Advanced pigments improve UV resistance by up to 30%, extending product lifespan and reducing material degradation. The increasing use of engineering plastics in electronics and medical devices further amplifies demand for specialized pigments with high thermal stability and chemical resistance.

Stringent environmental regulations regarding the use of hazardous chemicals and heavy metals in pigments are limiting market growth. Many traditional pigments contain substances such as cadmium and lead, which are being phased out due to health and environmental concerns. Compliance with regulations such as REACH and similar global standards has increased production costs by approximately 12–18% for manufacturers. Additionally, the transition to eco-friendly pigments often requires significant investment in research and development, as well as modifications to existing production processes. Limited availability of cost-effective sustainable alternatives further complicates adoption, particularly for small and medium-sized manufacturers.

The shift toward sustainable and bio-based materials presents significant growth opportunities for the plastic pigments market. Bio-based pigments derived from natural sources are gaining traction, with adoption rates increasing by over 20% annually in environmentally conscious markets. The development of recyclable and biodegradable pigment solutions is enabling manufacturers to align with circular economy initiatives. Additionally, advancements in nano-pigment technology are improving color strength and dispersion efficiency by up to 25%, reducing overall pigment usage. Emerging markets in Asia, Latin America, and Africa offer untapped potential due to increasing industrialization and rising demand for consumer goods, creating new avenues for market expansion.

Fluctuating raw material prices and ongoing supply chain disruptions present major challenges for the plastic pigments market. Key raw materials such as titanium dioxide and organic chemicals have experienced price volatility of up to 20% in recent years due to supply constraints and geopolitical factors. Transportation and logistics disruptions have further increased operational costs, impacting profit margins for manufacturers. Additionally, the dependency on a limited number of suppliers for specialized pigment components creates vulnerabilities in the supply chain. These challenges are compounded by the need to maintain consistent product quality and meet stringent regulatory requirements, making cost management and supply chain resilience critical priorities for industry players.

• Accelerated Shift Toward Eco-Friendly and Bio-Based Pigments: The adoption of environmentally sustainable plastic pigments has increased by over 28% in the past three years, driven by regulatory pressure and corporate ESG commitments. Approximately 62% of manufacturers in Europe have transitioned to heavy metal-free pigment formulations, while bio-based pigment usage in packaging applications has risen by 21%. These pigments reduce carbon emissions by nearly 18% compared to conventional alternatives, making them a critical component in sustainable plastic production strategies.

• Expansion of High-Performance Pigments in Automotive Plastics: High-performance pigments designed for heat resistance and UV stability are witnessing strong demand, particularly in the automotive sector where plastic usage has increased by 35% per vehicle. Advanced pigments now enhance UV resistance by up to 30% and extend product lifespan by nearly 25%. Electric vehicle production, which grew by over 40% globally in recent years, is further accelerating demand for specialized pigments used in lightweight and durable plastic components.

• Growth in Digital Color Matching and Smart Manufacturing Integration: The integration of digital color matching systems and AI-based pigment formulation tools has improved color accuracy by 22% and reduced production waste by 17%. Around 48% of large-scale manufacturers have adopted automated pigment dispersion technologies, resulting in process efficiency gains of up to 20%. These innovations are particularly prominent in North America and Asia-Pacific, where manufacturers are focusing on precision and cost optimization.

• Rising Demand from Packaging Sector Driven by E-Commerce Growth: The packaging industry accounts for over 38% of total plastic pigment consumption, with e-commerce growth contributing to a 26% increase in demand for visually appealing and durable packaging materials. Flexible packaging applications alone have seen pigment usage rise by 19%, while demand for recyclable packaging solutions incorporating advanced pigments has increased by 23%, reflecting shifting consumer preferences and regulatory requirements.

The plastic pigments market is segmented based on type, application, and end-user, each contributing distinctively to overall industry performance. Organic and inorganic pigments dominate the type segment, driven by their varied functional properties and cost-effectiveness. Applications are largely concentrated in packaging, automotive, and construction, which collectively account for more than 70% of total pigment usage. End-user industries such as consumer goods, automotive manufacturing, and building materials show varied adoption rates depending on regional industrialization and regulatory frameworks. Increasing demand for sustainable materials and high-performance plastics is influencing segmentation dynamics, with bio-based pigments and advanced applications gaining traction. The segmentation landscape reflects a balanced mix of mature and emerging segments, enabling diversified growth opportunities across global markets.

The plastic pigments market by type is primarily categorized into organic pigments, inorganic pigments, and specialty pigments. Organic pigments currently account for approximately 46% of total adoption, while inorganic pigments hold around 34%. However, specialty pigments, including high-performance and effect pigments, are gaining traction rapidly and are expected to surpass 30% adoption by 2033 due to their advanced properties such as thermal stability and UV resistance. Organic pigments lead the segment due to their superior color strength, brightness, and adaptability in packaging and consumer goods applications. These pigments enhance color vibrancy by nearly 25% compared to inorganic variants, making them highly preferred in aesthetic-driven industries. In contrast, inorganic pigments are valued for durability and resistance to extreme environmental conditions, particularly in construction and automotive applications. Specialty pigments are the fastest-growing type, expanding at an estimated CAGR of 9.8%, driven by increasing demand for high-performance plastics in automotive and electronics sectors. These pigments offer improved heat resistance by up to 35% and extended product lifecycle by 20%, making them suitable for advanced industrial applications. Other pigment types, including effect pigments and functional additives, collectively contribute around 20% of the market, serving niche requirements such as anti-counterfeiting and conductivity.

The application segment of the plastic pigments market is dominated by packaging, automotive, construction, and consumer goods industries. Packaging accounts for approximately 38% of total application share, while automotive contributes around 22%. However, construction applications are expanding rapidly and are expected to surpass 25% adoption by 2033 due to increasing infrastructure development globally. Packaging leads the segment due to its extensive use in flexible and rigid plastic formats, where pigments enhance branding and product differentiation. Pigment usage in packaging has increased by 26% in response to rising e-commerce activities and consumer demand for visually appealing products. Automotive applications rely on pigments for both aesthetic and functional purposes, with plastic components accounting for nearly 50% of vehicle volume. Construction is the fastest-growing application segment, expanding at an estimated CAGR of 8.7%, driven by increased use of colored plastic materials in pipes, fittings, and insulation products. Pigments used in construction improve UV resistance by up to 28% and enhance durability in harsh environmental conditions. Other applications, including electronics and healthcare, collectively account for approximately 15% of the market, driven by demand for high-performance and specialized plastics.

The end-user segmentation of the plastic pigments market includes packaging manufacturers, automotive producers, construction companies, and consumer goods industries. Packaging manufacturers lead with approximately 40% of total market adoption, while automotive manufacturers account for around 24%. However, the construction sector is emerging as a key growth area and is expected to exceed 28% adoption by 2033 due to increasing infrastructure projects worldwide. Packaging remains the dominant end-user due to high consumption of plastics in food, beverage, and e-commerce sectors, with pigment demand rising by 26% alongside packaging production volumes. Automotive manufacturers utilize pigments to enhance both aesthetic appeal and functional performance, with plastic components forming nearly half of vehicle structures. The construction industry is the fastest-growing end-user segment, expanding at an estimated CAGR of 8.5%, driven by increased demand for durable and weather-resistant plastic materials. Pigments used in construction applications improve product lifespan by up to 30% and reduce maintenance requirements significantly. Other end-users, including electronics and healthcare sectors, collectively contribute around 16% of the market, with adoption rates increasing by 12–15% annually due to growing demand for specialized plastic components.

Region Asia-Pacific accounted for the largest market share at 45% in 2025 however, Region Europe is expected to register the fastest growth, expanding at a CAGR of 8.6% between 2026 and 2033.

Asia-Pacific’s dominance is supported by its production of over 55% of global plastics, with China and India collectively contributing more than 60% of regional pigment consumption. North America holds approximately 23% share, driven by advanced manufacturing and high adoption of specialty pigments, while Europe accounts for nearly 21%, supported by sustainability-driven regulations. South America and the Middle East & Africa together contribute around 11%, with increasing industrialization and infrastructure development. Packaging applications represent over 38% of total pigment demand globally, while automotive contributes approximately 22%, with Asia-Pacific leading in volume and Europe showing a 30% higher adoption rate of eco-friendly pigment technologies compared to other regions.

How are advanced manufacturing and sustainability initiatives reshaping demand patterns?

North America holds approximately 23% of the global plastic pigments market, with the United States accounting for over 75% of regional demand. The market is driven by strong adoption in packaging, automotive, and healthcare industries, where plastic consumption exceeds 70 million tons annually. Regulatory frameworks such as restrictions on heavy metal-based pigments have led to over 58% adoption of eco-friendly alternatives. Technological advancements, including AI-driven pigment formulation and automated dispersion systems, have improved production efficiency by nearly 20%. A key player in the region has invested in sustainable pigment solutions, achieving a 15% reduction in carbon emissions through advanced processing technologies. Consumer behavior reflects a preference for high-quality, durable, and recyclable plastic products, with over 62% of manufacturers prioritizing sustainable pigment integration in their production lines.

What factors are accelerating the transition toward sustainable pigment technologies?

Europe represents around 21% of the global plastic pigments market, with Germany, the United Kingdom, and France leading regional consumption. Regulatory bodies have implemented strict environmental standards, resulting in over 65% adoption of low-VOC and heavy metal-free pigments. The region’s focus on circular economy initiatives has increased the use of recyclable pigment solutions by 28%. Advanced technologies such as digital color matching and nano-pigment processing are widely adopted, improving product consistency by 22%. A leading regional manufacturer has introduced bio-based pigments that reduce environmental impact by 18%, aligning with sustainability goals. Consumer behavior in Europe shows a strong inclination toward environmentally compliant products, with over 70% of enterprises integrating sustainable pigments into their supply chains to meet regulatory and consumer expectations.

Why is rapid industrial expansion driving unprecedented pigment consumption?

Asia-Pacific dominates the plastic pigments market with over 45% share, driven by high production volumes in China, India, and Japan. China alone contributes more than 35% of global plastic output, while India’s plastic consumption has grown by over 12% annually in recent years. The region’s manufacturing sector continues to expand, with infrastructure investments exceeding USD 1 trillion supporting demand for plastic materials. Technological advancements such as nano-dispersion and automated pigment processing have improved efficiency by 18%. A major regional producer has increased production capacity by 20% through the adoption of advanced pigment technologies. Consumer behavior is influenced by rapid urbanization and e-commerce growth, with packaging demand increasing by 26%, making it the largest application segment in the region.

How are industrial growth and policy reforms influencing market expansion?

South America accounts for approximately 6% of the global plastic pigments market, with Brazil and Argentina leading regional demand. The region’s growth is supported by increasing investments in construction and packaging industries, with plastic usage rising by 14% in infrastructure projects. Government incentives aimed at boosting domestic manufacturing have led to a 10% increase in local pigment production capacity. Trade policies promoting exports have further strengthened the market. A regional manufacturer has implemented advanced pigment technologies, improving production efficiency by 16%. Consumer behavior reflects growing demand for cost-effective and durable plastic products, particularly in packaging and consumer goods sectors, where adoption rates have increased by 18% over the past three years.

What role do infrastructure and energy investments play in shaping demand?

The Middle East & Africa region contributes around 5% to the global plastic pigments market, with the UAE and South Africa emerging as key growth countries. Demand is driven by large-scale infrastructure and construction projects, with plastic usage in these sectors increasing by 20%. The region’s oil and gas industry supports raw material availability, enhancing pigment production capabilities. Technological modernization, including automated pigment processing systems, has improved efficiency by 15%. Trade partnerships and government initiatives promoting industrial diversification have boosted local manufacturing. A regional player has expanded its pigment production capacity by 12%, meeting rising demand. Consumer behavior varies across the region, with increasing preference for durable and weather-resistant plastic products, particularly in construction and packaging applications.

China – Plastic Pigments Market (35%): Dominates due to large-scale plastic production capacity and strong demand across packaging and automotive sectors.

United States – Plastic Pigments Market (18%): Leads with advanced manufacturing technologies and high adoption of sustainable and specialty pigments.

The plastic pigments market is moderately fragmented, with over 120 active global and regional competitors operating across various segments. The top five companies collectively account for approximately 38% of the total market share, indicating a competitive yet diversified landscape. Market leaders are focusing on strategic initiatives such as mergers, acquisitions, and partnerships to strengthen their global presence and expand product portfolios. Over 25 major product launches have been recorded in the past three years, primarily targeting eco-friendly and high-performance pigment solutions. Innovation remains a key differentiator, with companies investing nearly 12% of their annual budgets in research and development to enhance pigment performance and sustainability.

Collaborations between pigment manufacturers and polymer producers have increased by 18%, enabling integrated solutions for end-users. Additionally, digital transformation initiatives, including AI-based color matching and automated manufacturing systems, are being adopted by over 45% of leading companies to improve efficiency and reduce production costs. The market also shows a rising trend of regional players expanding into international markets, supported by competitive pricing and localized production capabilities. Sustainability remains a central focus, with more than 60% of key players committing to reducing environmental impact through the development of non-toxic and recyclable pigment solutions.

BASF SE

Clariant AG

DIC Corporation

Lanxess AG

Tronox Holdings plc

Kronos Worldwide Inc.

Ferro Corporation

Heubach Group

Sudarshan Chemical Industries Limited

Cabot Corporation

Huntsman Corporation

Venator Materials PLC

Technological advancements are significantly transforming the plastic pigments market, with a strong focus on performance enhancement, sustainability, and process optimization. One of the most impactful innovations is the development of nano-pigments, which offer up to 30% higher dispersion efficiency compared to conventional pigments. These ultra-fine particles improve color uniformity and reduce pigment consumption by approximately 15%, making them highly suitable for high-performance applications in automotive and electronics plastics. Digital color matching systems and AI-driven formulation technologies are gaining widespread adoption, with nearly 48% of large-scale manufacturers integrating automated pigment blending solutions. These systems improve color accuracy by 22% and reduce production waste by up to 17%, enabling consistent output across high-volume production lines. Additionally, smart manufacturing technologies, including real-time monitoring and predictive analytics, are enhancing operational efficiency by approximately 20%, particularly in advanced polymer processing facilities.

Sustainability-focused innovations are also shaping the market, with bio-based pigments and recyclable polymer-compatible colorants witnessing adoption growth exceeding 25% in environmentally regulated regions. New-generation pigments are designed to be heavy metal-free, reducing environmental impact by nearly 18% while maintaining performance standards. Furthermore, advancements in high-temperature resistant pigments have improved thermal stability by up to 35%, supporting their use in engineering plastics and electric vehicle components.

Another emerging trend is the integration of functional pigments, such as conductive and anti-microbial pigments, which add value beyond coloration. These pigments are increasingly used in healthcare and electronics applications, where demand has risen by over 20%. Collectively, these technological innovations are redefining product capabilities, enabling manufacturers to meet evolving regulatory requirements and performance expectations while improving production efficiency and sustainability outcomes.

• In April 2025, BASF SE expanded its sustainable pigments portfolio by introducing a new range of biomass-balanced organic pigments for plastics, enabling up to 30% reduction in product carbon footprint while maintaining identical performance characteristics. Source: www.basf.com

• In September 2024, Clariant AG launched its next-generation Hostaperm® pigments designed for high-performance plastic applications, offering improved heat resistance and enhanced dispersion efficiency by over 20%, supporting automotive and packaging industries with advanced color stability. Source: www.clariant.com

• In March 2025, Sudarshan Chemical Industries Limited completed the acquisition of Heubach Group’s global pigment operations, strengthening its global footprint across 19 sites and expanding its product portfolio in high-performance pigments for plastics and coatings. Source: www.sudarshan.com

• In November 2024, Lanxess AG announced the expansion of its iron oxide pigment production capacity in Germany, increasing output by approximately 15% to meet rising demand from construction and plastic applications, particularly for durable and weather-resistant pigment solutions. Source: www.lanxess.com

The Plastic Pigments Market Report provides a comprehensive analysis of key industry segments, technological advancements, and regional dynamics shaping the global market landscape. The report covers a wide spectrum of pigment types, including organic pigments, inorganic pigments, and specialty pigments, which collectively account for over 90% of total market utilization. It further examines application-specific demand across packaging, automotive, construction, electronics, and healthcare sectors, with packaging alone contributing more than 38% of total pigment consumption. Geographically, the report encompasses detailed insights across major regions, including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, representing 100% of global market activity. Asia-Pacific leads in production volume with over 45% share, while Europe demonstrates strong adoption of sustainable pigment technologies, exceeding 65% penetration in regulated markets. The report also highlights emerging regional markets where industrial growth and infrastructure development are driving increased pigment usage.

In addition to segmentation and regional analysis, the report focuses on technological innovations such as nano-pigments, AI-driven color matching systems, and bio-based pigment solutions, which are improving efficiency by up to 20% and reducing environmental impact by nearly 18%. It also explores niche segments, including functional pigments used in antimicrobial and conductive applications, which are gaining traction in specialized industries. The scope extends to analyzing end-user industries, supply chain dynamics, regulatory frameworks, and sustainability initiatives influencing market trends. By integrating quantitative insights with industry-specific analysis, the report delivers a structured and data-driven perspective, enabling stakeholders to make informed strategic decisions across production, investment, and market expansion initiatives.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

7.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

BASF SE, Clariant AG, DIC Corporation, Lanxess AG, Tronox Holdings plc, Kronos Worldwide Inc., Ferro Corporation, Heubach Group, Sudarshan Chemical Industries Limited, Cabot Corporation, Huntsman Corporation, Venator Materials PLC |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |