Reports

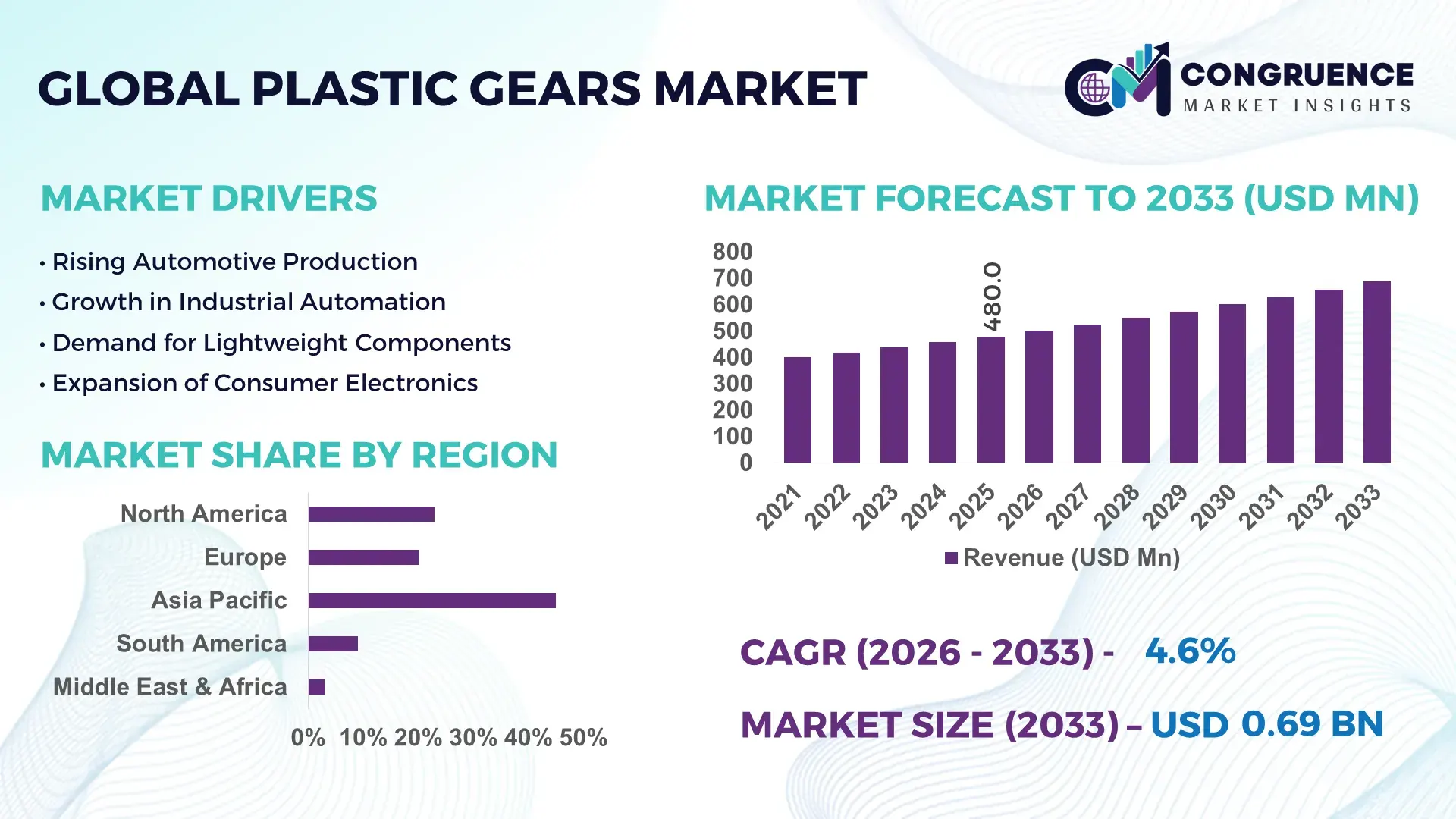

The Global Plastic Gears Market was valued at USD 480 Million in 2025 and is anticipated to reach a value of USD 687.85 Million by 2033 expanding at a CAGR of 4.6% between 2026 and 2033. Rising integration of lightweight engineering plastics in automotive actuators, medical devices, robotics, and precision consumer electronics is reducing component weight by nearly 35% compared to conventional metal gear systems while lowering lubrication and maintenance requirements.

China remains the dominant production and consumption hub, accounting for nearly 38% of global plastic gear manufacturing capacity in 2026, supported by large-scale investments in electric vehicles, industrial automation, and precision electronics. The country expanded high-performance polymer processing lines by over 18% since 2024, while automotive electronics output increased above 12% year-on-year. Compared to traditional die-cast metal gears, engineered plastic gears used in EV auxiliary systems deliver approximately 25% lower assembly weight and improved corrosion resistance, strengthening adoption across high-volume mobility and industrial applications.

Market Size & Growth: USD 480 Million in 2025 reaching USD 687.85 Million by 2033 at 4.6% growth, driven by lightweight automotive and industrial automation demand.

Top Growth Drivers: EV component integration expanded 21%, industrial robotics adoption rose 18%, and precision medical equipment demand increased 14% globally.

Short-Term Forecast: By 2027, advanced molded gear systems improve operational efficiency by 16% while reducing maintenance costs by nearly 11%.

Emerging Technologies: AI-assisted molding, carbon-fiber reinforced polymers, and automated micro-gear fabrication improved production precision by over 19%.

Regional Leaders: Asia-Pacific exceeds USD 280 Million with EV adoption growth, Europe crosses USD 160 Million through automation upgrades, and North America approaches USD 145 Million from medical device expansion.

Consumer/End-User Trends: Nearly 47% of OEMs shifted toward high-performance polymer gears for low-noise and corrosion-resistant applications.

Pilot/Case Example: In 2025, an automotive actuator project reduced assembly weight by 28% and improved component lifespan by 15% using reinforced plastic gears.

Competitive Landscape: Top manufacturers collectively control around 42% market share, with strong competition from precision engineering and automotive-focused suppliers.

Regulatory & ESG Impact: Industrial energy-efficiency mandates lowered lubricant dependency by 20%, accelerating adoption of recyclable engineering plastics.

Investment & Funding: More than USD 210 Million entered automated polymer gear manufacturing expansion projects between 2024 and 2026 amid supply chain regionalization.

Innovation & Future Outlook: High-temperature polymers, smart sensor-integrated gears, and additive manufacturing are reshaping advanced precision transmission systems globally.

Automotive applications contribute nearly 34% of global plastic gear consumption, followed by industrial machinery at 27% and consumer electronics at 19%, reflecting strong diversification across high-volume sectors. Advanced polyamide and PEEK-based gear systems improved thermal resistance by over 22% in recent product launches, supporting next-generation EV and robotics integration. Asia-Pacific continues to dominate demand, while European manufacturers accelerate sustainable material adoption under stricter industrial compliance frameworks. Growing investment in smart manufacturing and localized supply chains is expected to strengthen precision polymer component ecosystems and shape the next phase of strategic market expansion.

Plastic gears are rapidly transforming from low-cost mechanical substitutes into critical precision-engineering components supporting electric mobility, robotics, medical systems, and industrial automation. OEMs are accelerating adoption because engineered thermoplastics reduce component weight by nearly 35% and lower operational noise by over 20%, directly improving energy efficiency and equipment lifespan. The market is becoming strategically important as manufacturers optimize compact drivetrain architectures and automated assemblies requiring corrosion-resistant, low-maintenance transmission systems. Between 2024 and 2026, supply chain regionalization and stricter industrial efficiency standards forced companies to shift procurement toward localized high-performance polymer gear production platforms.

Carbon-fiber reinforced polymer gears improve efficiency by 18% while reducing production cost by 14% compared to legacy machined metal systems, reshaping competitive benchmarks across precision manufacturing. Asia-Pacific leads in production volume with nearly 46% manufacturing concentration, while Europe leads in advanced adoption and material innovation with over 31% penetration in automation-focused industrial applications. Over the next three years, automated micro-molding systems are expected to improve dimensional accuracy by 22% and reduce defect rates by 17%. Recyclable engineering plastics are also creating ESG-linked advantages through 15% lower lubrication dependency and stronger regulatory compliance access.

In 2025, a robotics actuator manufacturer improved assembly speed by 19% after integrating high-strength polyamide gear systems into lightweight automation modules. Major manufacturers are simultaneously shifting capital allocation toward precision polymer R&D, AI-assisted molding, and regionalized production expansion to secure long-term OEM contracts. Companies that combine advanced materials expertise, automation scalability, and sustainability alignment are positioning themselves to dominate the next generation of high-performance motion-control systems.

Automotive electrification, industrial automation, and compact medical equipment manufacturing are accelerating demand for lightweight plastic gear assemblies with higher durability and lower maintenance cycles. Engineered thermoplastic gears reduce component weight by nearly 35% and lower operational noise by over 20%, making them increasingly preferred in electric actuators, robotics, and consumer electronics. Global supply chain restructuring after Red Sea shipping disruptions pushed manufacturers toward localized polymer component sourcing, accelerating regional production investments. Industrial automation installations increased above 16% between 2024 and 2026, directly expanding demand for precision motion-control systems. In response, manufacturers are expanding automated injection molding capacity, forming strategic polymer partnerships, and investing in reinforced composite gear technologies to optimize scalability and secure long-term OEM integration contracts.

Dependence on specialty engineering polymers and concentrated resin supply chains is constraining production stability across the plastic gears market. Prices for high-performance polyamide and PEEK materials fluctuated by more than 18% during recent petrochemical supply disruptions, increasing procurement risk for precision manufacturers. Thermal deformation and load-bearing limitations also restrict adoption in high-torque industrial environments, where metal alternatives still outperform plastic systems by nearly 22% under extreme stress conditions. Logistics instability across Asian shipping routes further extended component lead times by approximately 14% during 2025. To mitigate operational risk, companies are diversifying resin sourcing, securing long-term supply agreements, and accelerating development of hybrid composite gear systems that improve heat resistance while reducing dependency on volatile specialty polymer markets.

Advanced composite polymers, AI-assisted molding systems, and micro-precision manufacturing are reshaping the next growth phase of the plastic gears market. High-temperature reinforced polymers improve wear resistance by nearly 27% while reducing lubrication requirements by 15%, creating new demand across electric mobility and collaborative robotics applications. Emerging economies in Southeast Asia and Eastern Europe are rapidly expanding localized automation infrastructure, increasing demand for lightweight precision transmission components. Additive manufacturing adoption in gear prototyping accelerated above 21% between 2024 and 2026, significantly shortening product development cycles. Companies are positioning for future dominance through regional manufacturing expansion, investment in recyclable engineering plastics, and integrated R&D ecosystems focused on smart actuator platforms, compact drivetrain systems, and high-efficiency industrial automation technologies globally.

Maintaining precision consistency, thermal durability, and large-scale production efficiency remains a major execution challenge for plastic gear manufacturers. Defect sensitivity in high-speed injection molding processes increases rejection rates by nearly 12% when dimensional tolerances exceed micro-level specifications, directly impacting automotive and robotics applications. Performance degradation under elevated temperatures continues limiting adoption in heavy industrial systems, where metal alternatives sustain nearly 25% greater torque reliability. Stricter sustainability compliance standards across Europe and North America are also forcing manufacturers to redesign materials and production workflows. Companies seeking long-term competitiveness must accelerate investment in automated quality inspection, advanced polymer engineering, and collaborative supplier partnerships while optimizing scalable manufacturing infrastructure capable of meeting precision, compliance, and durability expectations simultaneously.

“31% Faster Micro-Molding Cycles Are Reshaping Precision Gear Manufacturing.” Manufacturers are deploying AI-assisted injection molding systems that cut cycle times by 31% and reduce material wastage by 14% across high-volume production lines. Automated inspection platforms improved dimensional accuracy by nearly 18%, particularly in automotive actuator and robotics applications. Companies are restructuring manufacturing footprints closer to OEM assembly hubs after recent shipping disruptions increased lead-time sensitivity. This shift is optimizing throughput while forcing smaller suppliers to adopt digital quality-control systems to remain contract eligible.

“26% Growth in Reinforced Polymer Usage Is Redefining Gear Performance Standards.” Carbon-fiber and glass-reinforced thermoplastics now account for nearly 26% of advanced industrial gear production as manufacturers prioritize heat resistance and durability. Compared to conventional polyamide gears, reinforced variants extend operational lifespan by approximately 21% in compact drivetrain systems. Companies are rapidly scaling material partnerships and redesigning lightweight gear architectures to reduce lubrication dependency and meet stricter industrial efficiency standards emerging across Europe and Asia.

“22% Increase in Regionalized Production Is Shifting Global Supply Strategies.” Asia-Pacific remains the dominant manufacturing base, yet North American and European suppliers expanded localized precision molding operations by over 22% between 2024 and 2026. Companies are reducing cross-border procurement exposure while shortening delivery cycles by nearly 17%. A non-obvious industry shift is the growing preference for multi-source polymer contracts, allowing manufacturers to stabilize pricing volatility and maintain uninterrupted production consistency during raw material fluctuations.

“19% Rise in Smart Gear Integration Is Accelerating Functional Convergence.” Embedded sensor-compatible plastic gears increased deployment by 19% in robotics, healthcare devices, and automated consumer systems. Manufacturers are integrating lightweight transmission components with predictive maintenance capabilities to reduce downtime by nearly 13%. This operational convergence is redefining supplier competition, as OEMs increasingly prioritize vendors capable of combining precision molding, electronics integration, and low-noise performance within a single scalable production ecosystem.

The plastic gears market is segmented by type, application, and end-user, with spur gears and automotive components accounting for the largest demand concentration due to cost efficiency and high-volume integration. Automotive and industrial manufacturing collectively contribute over 52% of total consumption, supported by rising automation and lightweight component adoption. Demand is shifting toward helical gears, medical devices, and robotics applications, where noise reduction and precision performance improved adoption rates by nearly 18% between 2024 and 2026. Manufacturers are prioritizing reinforced polymers, micro-precision molding, and regionalized production strategies to capture emerging demand pockets while optimizing operational scalability and long-term OEM alignment.

Spur gears dominate the plastic gears market with nearly 38% share due to their low production cost, simple geometry, and high scalability across automotive actuators, consumer electronics, and industrial assemblies. Their widespread integration into high-volume manufacturing environments continues reinforcing structural dominance, particularly where compact design and cost-efficient torque transmission remain critical. However, helical gears are emerging as the fastest-growing segment, with adoption rising above 17% between 2024 and 2026 because of superior noise reduction and smoother load distribution in robotics and electric mobility systems. Compared to spur gears, helical variants improve operational stability by nearly 14% in precision automation environments, accelerating demand across advanced manufacturing applications.

Bevel gears, worm gears, and rack and pinion gears collectively account for approximately 41% of market demand, maintaining strategic relevance in angular motion transfer, compact steering systems, and controlled speed reduction applications. Companies are increasingly shifting product development toward reinforced helical and bevel gear platforms while expanding automated molding capacity for high-precision applications. Investment focus is moving toward advanced polymer composites and micro-gear manufacturing technologies, while conventional low-load gear systems face pricing pressure and margin compression across mature consumer applications.

“According to a 2025 report by an international mechanical engineering association, helical plastic gears were adopted by over 43% of advanced robotics manufacturers, resulting in nearly 16% improvement in motion precision and reduced acoustic vibration, reinforcing their growing strategic importance.”

Automotive components remain the leading application segment, accounting for nearly 33% of plastic gear demand due to large-scale integration in actuators, HVAC systems, seat adjustment mechanisms, and electric drivetrain auxiliaries. Demand concentration is driven by lightweighting requirements, reduced lubrication dependency, and rising electric vehicle production. Motion control applications are emerging as the fastest-growing segment, expanding by approximately 19% between 2024 and 2026 as industrial robotics and automated precision systems accelerate deployment globally. Compared to mature power transmission applications, motion control systems require higher dimensional precision and low-noise operation, forcing manufacturers to prioritize reinforced polymer engineering and micro-tolerance molding technologies.

Industrial machinery, consumer electronics, medical devices, and traditional power transmission applications collectively contribute over 54% of market consumption. Consumer electronics manufacturers are increasing adoption of compact precision gears to optimize device miniaturization, while healthcare equipment suppliers are integrating lightweight low-friction gear systems into diagnostic and surgical devices. Companies are responding through automation-focused production scaling, regional manufacturing expansion, and collaborative development partnerships with OEMs. Strategic demand is increasingly shifting toward high-performance precision applications where durability, acoustic performance, and operational efficiency directly influence long-term supplier competitiveness.

“According to a 2025 report by a global automation standards body, motion control applications were deployed across more than 58,000 industrial automation systems, improving operational accuracy by 18%, highlighting their rapid operational adoption.”

The automotive sector dominates end-user demand with approximately 36% share, supported by high-volume integration of lightweight gear assemblies across electric vehicles, interior automation systems, and thermal management platforms. Demand concentration remains strongest in Asia-Pacific manufacturing hubs where EV component localization and compact actuator deployment continue accelerating. Meanwhile, the robotics industry represents the fastest-growing end-user segment, with adoption increasing by nearly 21% between 2024 and 2026 as factories prioritize precision automation and low-noise motion systems. Compared to traditional industrial manufacturing, robotics applications require tighter dimensional tolerances and enhanced wear resistance, redefining product engineering priorities across the market.

Industrial manufacturing, electronics industry, healthcare, and aerospace applications collectively account for nearly 49% of total consumption. Healthcare and aerospace buyers are increasingly prioritizing high-performance engineered polymers capable of reducing maintenance frequency and minimizing vibration. Companies are targeting these segments through customized material formulations, long-term OEM agreements, and vertically integrated production strategies. Electronics manufacturers are also increasing procurement of micro-precision plastic gears for compact consumer systems, while industrial buyers continue emphasizing durability and cost optimization. Future demand is shifting toward application-specific engineering capabilities, forcing suppliers to differentiate through precision manufacturing, rapid prototyping, and advanced material innovation.

“According to a 2025 report by a global robotics manufacturing council, adoption among robotics industry manufacturers increased by 24%, with over 41,000 production systems implementing advanced plastic gear assemblies, leading to nearly 15% improvement in operational efficiency, indicating a strong shift in demand dynamics.”

Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.3% between 2026 and 2033.

Asia-Pacific dominates production scale and export-driven manufacturing, supported by high-volume automotive, electronics, and industrial machinery demand across China, Japan, and South Korea. Europe contributes nearly 27% of global demand and leads in advanced polymer innovation, sustainability-focused manufacturing, and precision automation adoption. North America holds approximately 21% market share while accelerating investment in robotics, electric mobility systems, and localized component sourcing. Regional supply chain restructuring following Red Sea logistics disruptions and stricter industrial efficiency mandates pushed manufacturers toward localized precision molding operations and multi-source polymer procurement strategies. Global companies are increasingly prioritizing Asia-Pacific for scale, Europe for high-performance engineering innovation, and North America for automation-focused expansion and resilient OEM partnerships.

North America accounts for nearly 21% of global plastic gear demand, driven by strong adoption across electric vehicles, industrial robotics, and healthcare equipment manufacturing. Automotive actuator systems and factory automation platforms remain the primary consumption hubs, while regional OEMs increasingly prioritize lightweight and low-maintenance transmission components. Supply chain regionalization accelerated after 2024 logistics disruptions, pushing manufacturers to expand localized molding and precision polymer processing capacity. Automated quality-control integration improved production efficiency by approximately 16% across advanced manufacturing facilities. Companies also increased investment in reinforced polymer gear platforms and robotics-focused component lines, with regional precision molding capacity expanding by nearly 14% between 2024 and 2026. Enterprise buyers increasingly favor suppliers offering rapid customization, short lead times, and vertically integrated production capabilities, reinforcing North America as a strategic hub for high-value precision manufacturing expansion.

Europe represents approximately 27% of global plastic gear demand, led by Germany, France, and Italy through advanced automotive engineering and industrial automation manufacturing. Stricter energy-efficiency regulations and sustainability compliance frameworks are accelerating adoption of recyclable engineering polymers and low-lubrication gear systems. Industrial manufacturers reduced lubricant dependency by nearly 18% through advanced polymer integration, while automated precision molding adoption increased above 15% across high-performance applications. Companies are restructuring product portfolios toward lightweight drivetrain systems and sensor-compatible gear technologies to meet tightening operational efficiency standards. Enterprise procurement behavior remains quality-focused and compliance-driven, favoring suppliers capable of delivering durable, low-noise, and environmentally aligned solutions. Europe continues forcing global manufacturers to accelerate material innovation, sustainable production redesign, and precision engineering capabilities to remain commercially competitive.

Asia-Pacific leads the plastic gears market with nearly 46% global demand concentration, supported by large-scale manufacturing ecosystems across China, Japan, South Korea, and India. The region dominates automotive electronics, industrial automation, and consumer electronics production, creating strong demand for lightweight precision gear systems. Localized component manufacturing and integrated polymer supply chains improved production turnaround times by approximately 19% between 2024 and 2026. Chinese manufacturers alone account for more than 38% of global precision plastic gear output, while regional export-oriented facilities expanded automated molding capacity by nearly 17%. Enterprise buyers prioritize cost efficiency, scalability, and rapid fulfillment, forcing suppliers to optimize high-volume production systems and regional distribution networks. Asia-Pacific remains strategically critical for companies pursuing manufacturing scale, supply chain resilience, and long-term OEM production partnerships globally.

South America contributes nearly 6% of global plastic gear demand, with Brazil and Argentina leading consumption across automotive assembly, agricultural machinery, and industrial processing equipment. Demand growth is increasingly linked to localized manufacturing modernization and replacement of metal components with lightweight polymer systems to reduce maintenance costs. However, limited advanced polymer processing infrastructure and imported resin dependency continue constraining production scalability and pricing stability. Regional manufacturers reduced component sourcing lead times by approximately 11% through localized supplier partnerships and small-scale automation investments. Enterprise buyers remain highly price-sensitive, prioritizing durable low-cost gear solutions over premium engineered variants. The region presents strategic opportunity for suppliers capable of balancing affordability, localized technical support, and operational flexibility while navigating infrastructure limitations and fluctuating industrial investment cycles.

The Middle East & Africa region accounts for approximately 5% of global plastic gear demand, driven by infrastructure modernization, industrial automation, and oil and gas equipment upgrades across the UAE, Saudi Arabia, and South Africa. Construction machinery, water treatment systems, and industrial processing applications are expanding adoption of corrosion-resistant polymer gear assemblies. Government-backed industrial diversification programs accelerated manufacturing automation investments by nearly 13% between 2024 and 2026. Companies are also increasing deployment of localized assembly and maintenance partnerships to reduce import dependency and improve operational continuity. Enterprise buyers prioritize durability, low maintenance requirements, and long operational lifespan under harsh environmental conditions. The region is emerging as a strategic growth corridor for manufacturers capable of aligning infrastructure-focused product customization with long-term industrial modernization and regional supply network expansion.

China – 38% market share in the Plastic Gears market due to large-scale automotive electronics production, integrated polymer supply chains, and dominant precision manufacturing capacity.

Germany – 14% market share in the Plastic Gears market driven by advanced industrial automation, high-performance engineering demand, and strong adoption of precision lightweight drivetrain technologies.

The plastic gears market is defined by competition between global precision engineering leaders, regional cost-focused manufacturers, and automation-driven component innovators including KHK Gears, SDP/SI, igus, Kohara Gear Industry, and Rush Gears. The top five players collectively control nearly 43% of global market positioning through advanced polymer engineering, OEM integration, and scalable manufacturing networks. Competition is increasingly shifting from price-based sourcing toward precision performance, material innovation, and rapid customization, with automated molding systems improving production efficiency by 18% and reducing defect rates by 12%. Companies are aggressively expanding regional manufacturing capacity, forming polymer technology partnerships, and integrating AI-assisted quality inspection to secure long-term automotive and robotics contracts. Supply chain localization and reinforced composite materials are reshaping competitive positioning, while high tooling investment and micro-tolerance manufacturing requirements create strong entry barriers. Winning requires scalable precision manufacturing, advanced materials expertise, and resilient OEM-focused supply ecosystems.

igus GmbH

KHK Gears

SDP/SI

Rush Gears Inc.

Kohara Gear Industry Co., Ltd.

AmTech International

Boston Gear

Nordex, Inc.

PIC Design, Inc.

WM Berg Inc.

Eaton Corporation

ABB Ltd.

Renold plc

Tsubaki Nakashima Co., Ltd.

Advanced engineering polymers and AI-assisted injection molding technologies are currently reshaping precision plastic gear manufacturing. Reinforced polyamide and PEEK-based gears improve wear resistance by nearly 27% while reducing lubrication dependency by 18% compared to conventional thermoplastic systems. Automated molding and optical inspection platforms are now deployed across approximately 41% of high-volume production facilities, improving dimensional accuracy by 16% and lowering defect-related scrap rates. Companies integrating precision molding with digital quality monitoring are securing stronger automotive, robotics, and industrial automation contracts through faster production cycles and tighter tolerance control.

Emerging technologies are accelerating adoption of lightweight, low-noise gear systems across electric mobility and medical devices. Carbon-fiber reinforced polymer gears reduce operational vibration by 21% while extending component lifespan by nearly 19% compared to legacy machined metal gears. Around 34% of robotics manufacturers are integrating sensor-compatible plastic gear assemblies to optimize predictive maintenance and compact actuator performance. Manufacturers focusing on high-temperature polymers, recyclable materials, and micro-gear architectures are gaining competitive advantage through improved operational efficiency and compliance alignment.

Disruptive additive manufacturing and smart-material integration technologies are redefining product customization between 2026 and 2028. Advanced 3D-printed wear-resistant gear resins improve service life by up to five times versus standard additive materials while reducing prototyping lead times by 24%. Companies adopting hybrid digital manufacturing ecosystems will accelerate low-volume precision production, optimize regional supply resilience, and capture expanding demand across aerospace, collaborative robotics, and next-generation automation systems.

April 2025 – igus GmbH introduced 277 new lubrication-free motion plastic innovations, including PTFE-free materials and recycled-content gear-related systems, while increasing active customer engagement by 5%. The expansion strengthened its sustainability-focused industrial automation positioning and accelerated advanced polymer adoption across precision applications. [Sustainable Motion Shift] Source: igus Press

June 2025 – igus GmbH launched the iglidur i4000 resin for precision 3D-printed gears, delivering up to five times longer service life and 13 times higher elongation performance than conventional additive resins. The development significantly improved rapid prototyping and low-volume precision gear manufacturing capabilities. [Additive Durability Leap] Source: igus Press International

September 2024 – Eaton Corporation expanded its commercial vehicle transmission portfolio with new automated manual transmission platforms targeting emerging mobility markets. The systems improved fuel efficiency and operational reliability while supporting electrified and conventional powertrains, strengthening Eaton’s competitive positioning in advanced drivetrain integration. [Transmission Platform Expansion] Source: Eaton Official Newsroom

March 2025 – igus GmbH showcased PTFE-free and PFAS-tested motion plastic technologies at Hannover Fair 2025, accelerating compliance-focused material innovation. The company expanded sustainable polymer development programs as industrial customers increased demand for low-maintenance components aligned with tightening environmental regulations and operational efficiency targets. [Compliance Material Transition]

The Plastic Gears Market report delivers comprehensive analysis across gear types including spur gears, helical gears, bevel gears, worm gears, and rack and pinion gears, alongside applications spanning power transmission, motion control, automotive components, industrial machinery, consumer electronics, and medical devices. The study evaluates end-user industries such as automotive, robotics, aerospace, healthcare, industrial manufacturing, and electronics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It also covers critical technologies including reinforced engineering polymers, AI-assisted precision molding, additive manufacturing, and sensor-compatible lightweight gear systems shaping operational transformation between 2026 and 2033.

The report analyzes more than 25 strategic market indicators including adoption trends, production concentration, regional manufacturing shifts, and application-specific demand patterns. Automotive and industrial manufacturing collectively account for over 52% of current market consumption, while advanced robotics and medical systems recorded adoption increases above 18% between 2024 and 2026. More than 40% of large-scale manufacturers are integrating automated inspection and digital molding systems to improve precision consistency and reduce production waste.

The study supports investment planning, competitive benchmarking, regional expansion strategies, supplier evaluation, and technology positioning by identifying high-growth precision applications, emerging material innovations, and evolving OEM procurement priorities across the global plastic gears ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 480 Million |

|

Market Revenue in 2033 |

USD 687.85 Million |

|

CAGR (2026 - 2033) |

4.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

igus GmbH, KHK Gears, SDP/SI, Rush Gears Inc., Kohara Gear Industry Co., Ltd., AmTech International, Boston Gear, Nordex, Inc., PIC Design, Inc., WM Berg Inc., Eaton Corporation, ABB Ltd., Renold plc, Tsubaki Nakashima Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |