Reports

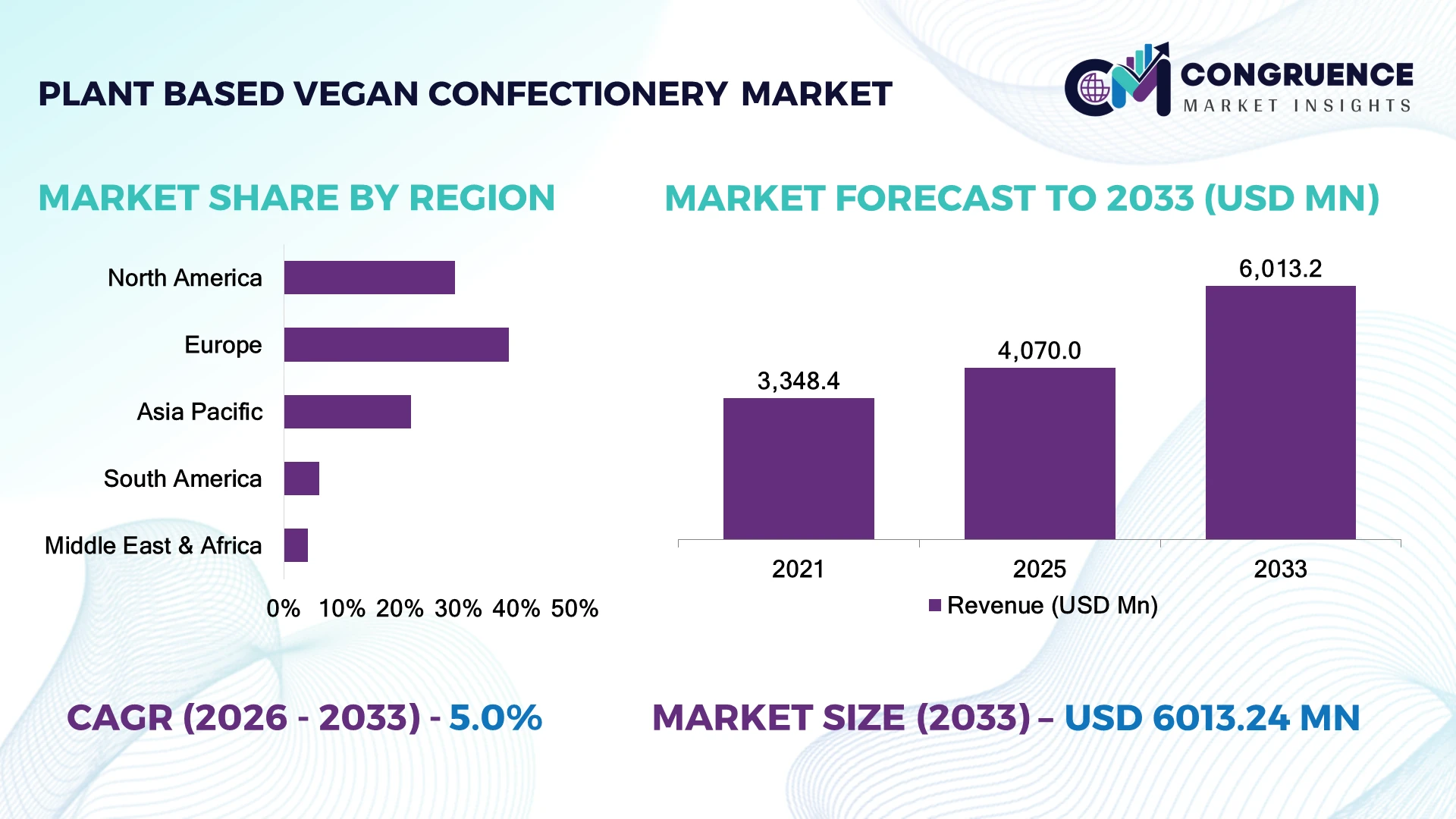

The Global Plant-Based Vegan Confectionery Market was valued at USD 4,070.0 Million in 2025 and is anticipated to reach a value of USD 6,013.2 Million by 2033 expanding at a CAGR of 5.0% between 2026 and 2033. Growth is primarily driven by rapid reformulation using dairy-free ingredients, rising clean-label product launches, and expanding retail distribution supported by sustainable cocoa and plant-based ingredient sourcing.

Germany leads the global market with approximately 24% of Europe's plant-based confectionery production, supported by more than 350 specialized food manufacturers and strong investments in sustainable food processing. Compared with France, Germany records higher vegan confectionery retail penetration, while nationwide labeling standards under the European Green Deal accelerate product adoption across premium and mainstream retail channels.

This leadership reinforces Europe as the preferred destination for capacity expansion, product innovation, and long-term supply-chain investments.

Market Size & Growth: USD 4,070.0 Million in 2025, reaching USD 6,013.2 Million by 2033 at 5.0% CAGR, supported by clean-label innovation and dairy-free ingredient commercialization.

Top Growth Drivers: Plant-based food adoption exceeds 18%, premium vegan confectionery launches increased 22%, and sustainable cocoa sourcing initiatives expanded by 16%.

Short-Term Forecast: By 2028, manufacturing efficiency is projected to improve by 14% through automated processing and optimized ingredient sourcing.

Emerging Technologies: AI-powered formulation, precision fermentation, and advanced plant-protein processing improve product consistency and accelerate innovation cycles.

Regional Leaders: Europe approaches USD 2.4 Billion, North America exceeds USD 1.6 Billion, and Asia-Pacific surpasses USD 1.2 Billion, driven by premium retail expansion and localized product development.

Consumer/End-User Trends: More than 35% of urban consumers actively seek vegan confectionery with natural ingredients and reduced sugar formulations.

Pilot/Case Example: In 2024, automated chocolate processing trials reduced ingredient waste by approximately 12% while improving production consistency.

Competitive Landscape: Leading manufacturers collectively account for nearly 38% market share, with Mondelēz International, Lindt & Sprüngli, Nestlé, Katjes Group, and Plamil Foods among major participants.

Regulatory & ESG Impact: Sustainable sourcing programs reduced certified cocoa supply-chain emissions by approximately 15% while supporting stricter environmental compliance.

Investment & Funding: More than USD 600 Million has been directed toward production expansion, strategic partnerships, and next-generation ingredient manufacturing.

Innovation & Future Outlook: Functional ingredients, sugar-reduction technologies, and alternative dairy formulations are strengthening premium product positioning across global markets.

Plant-Based Vegan Confectionery Market demand continues expanding across premium chocolate, sugar confectionery, and functional snack categories as manufacturers introduce cleaner formulations with improved texture and taste. More than 30% of new vegan confectionery launches now emphasize natural ingredients and reduced sugar content. Stable plant-protein supply chains, evolving sustainability standards, and advanced ingredient processing are strengthening product differentiation, setting the foundation for broader strategic market developments.

Plant-based vegan confectionery has become a strategic category as food manufacturers compete through premium positioning, ingredient transparency, and sustainable production. Supply-chain restructuring around certified cocoa, oat-based ingredients, and alternative sweeteners is strengthening resilience while enabling brands to respond faster to changing consumer preferences. Retailers are also expanding shelf space dedicated to plant-based confectionery portfolios.

Modern ingredient processing technologies deliver measurable operational gains compared with conventional production methods. Precision formulation and automated mixing systems improve batch consistency by approximately 18% while reducing raw material waste by nearly 12%. Europe remains the innovation leader through established manufacturing ecosystems and regulatory support, whereas Asia-Pacific is expanding production capacity rapidly through localized product development and modern food-processing investments.

Companies are strengthening competitive positions by investing in dedicated production facilities, expanding co-manufacturing partnerships, and introducing region-specific product portfolios. A practical example includes automated dairy-free chocolate production lines that improve manufacturing flexibility while shortening production cycles. Over the next two to three years, continued investment in advanced ingredient technologies, sustainable sourcing, and premium product innovation will strengthen operational efficiency and establish long-term competitive differentiation across the global confectionery industry.

Consumer preference for healthier confectionery is accelerating reformulation across chocolate, gummies, and sugar confectionery categories. More than 35% of newly introduced vegan confectionery products now feature clean-label positioning, while demand for dairy-free chocolate has increased by over 20% across organized retail. Germany continues strengthening certified cocoa sourcing through sustainable procurement initiatives under evolving European food standards, encouraging ingredient transparency across supply chains. This shift improves brand credibility and supports premium pricing. In response, manufacturers are expanding dedicated plant-based production lines, investing in alternative protein and fat technologies, and partnering with ingredient suppliers to improve taste, texture, and shelf stability. A notable strategic advantage lies in vertically integrating ingredient sourcing, enabling companies to strengthen supply resilience while reducing formulation variability.

Price fluctuations in cocoa, nuts, and specialty plant-based ingredients continue to pressure manufacturing economics. Certified sustainable cocoa prices have experienced periodic increases exceeding 18%, while premium plant-derived ingredients can cost 25–40% more than conventional alternatives. Weather-related disruptions affecting cocoa-producing countries such as Ghana and Côte d'Ivoire have tightened ingredient availability, increasing procurement uncertainty for manufacturers. These structural constraints directly affect production planning, inventory management, and profit margins, particularly for mid-sized brands. Companies are responding by diversifying supplier networks, increasing localized ingredient sourcing where feasible, negotiating long-term procurement agreements, and developing alternative formulations using oat, rice, and sunflower-based ingredients. Strong procurement diversification has become an operational differentiator rather than simply a cost-control measure.

Growing consumer interest in nutrition-enhanced confectionery is creating opportunities beyond traditional vegan products. Nearly 30% of premium launches now incorporate functional ingredients such as plant proteins, probiotics, or natural botanical extracts, while automated formulation technologies reduce product development cycles by approximately 15%. The United Kingdom is supporting food innovation through alternative protein research and sustainable manufacturing initiatives, encouraging rapid commercialization of next-generation confectionery. Manufacturers are expanding R&D partnerships with ingredient technology firms to improve sensory performance without artificial additives. An emerging opportunity lies in personalized nutrition and low-sugar premium confectionery, where digital formulation tools enable faster product customization while improving manufacturing efficiency and reducing ingredient waste across production facilities.

Maintaining consistent product quality while scaling production remains a significant operational challenge. Plant-based chocolate formulations often require 10–15% tighter processing controls than conventional recipes due to ingredient sensitivity, while more than 20% of manufacturers continue facing texture and stability inconsistencies during high-volume production. Japan's advanced confectionery sector demonstrates the importance of precision processing technologies and strict manufacturing controls to ensure repeatable product quality. Companies must invest in advanced automation, quality analytics, workforce training, and digital process monitoring to maintain consistency across expanding production networks. Long-term competitiveness will increasingly depend on manufacturing precision and process standardization rather than product variety alone, making operational excellence a critical strategic capability.

Premium Chocolate Reformulation Plant-based chocolate manufacturers are replacing dairy fats with oat, almond, and cocoa butter blends, improving product texture while reducing formulation complexity. More than 34% of new premium confectionery launches now feature clean-label positioning, and automated recipe optimization has shortened product development cycles by nearly 18%. Stricter sustainability requirements for cocoa sourcing are accelerating supplier qualification, prompting companies to expand long-term procurement partnerships and modernize ingredient processing for greater production consistency.

Sugar Reduction Accelerates Innovation Reduced-sugar vegan confectionery has become a core product development priority as natural sweetener adoption has increased by approximately 27% and consumer preference for functional snacks exceeds 30% across major retail channels. Manufacturers in the United Kingdom are integrating precision blending systems that reduce ingredient waste by around 12% while improving batch uniformity. Companies are restructuring product portfolios and expanding collaborations with specialty ingredient developers to strengthen premium positioning and manufacturing efficiency.

Localized Manufacturing Expansion Supply-chain resilience is driving manufacturers to establish regional production and packaging facilities closer to major consumer markets. More than 22% of producers have expanded localized sourcing programs, while transportation lead times have declined by nearly 15% through supplier diversification. Germany continues strengthening domestic processing capabilities for plant-based ingredients, encouraging companies to scale dedicated manufacturing lines and optimize inventory management against global logistics disruptions.

Functional Confectionery Diversification Functional vegan confectionery incorporating plant proteins, fiber, probiotics, and botanical ingredients now represents over 28% of premium product launches. Digital quality monitoring has improved production consistency by approximately 16%, reducing product rejection rates during commercial manufacturing. Companies are investing in advanced processing technologies, co-developing formulations with ingredient specialists, and expanding premium retail portfolios to capture health-focused consumers while differentiating products beyond traditional dairy-free positioning.

Dairy-Free Chocolate dominates the Plant-Based Vegan Confectionery Market with an estimated 46% market share, supported by broad consumer acceptance, premium retail positioning, and continuous advances in cocoa and plant-based fat formulations. The segment benefits from established manufacturing infrastructure and extensive supermarket distribution, making it the preferred category for multinational brands. Vegan Gummies represent the fastest-growing segment as fruit-based formulations and natural color technologies gain traction among younger consumers. Vegan Hard Candies and Vegan Toffees maintain stable demand through affordable pricing and longer shelf life, while Vegan Marshmallows continue expanding within seasonal and specialty confectionery categories. Manufacturers are increasing investments in texture optimization, clean-label ingredients, and sugar-reduction technologies. Nearly 36% of new vegan confectionery launches now focus on chocolate-based products, while over 24% incorporate functional ingredients for premium positioning. Strategic product diversification enables brands to strengthen retailer relationships and improve category penetration across convenience stores, supermarkets, and online channels.

Retail Consumption accounts for approximately 63% of overall market demand, driven by supermarket expansion, specialty vegan retailers, and growing e-commerce penetration. Strong merchandising strategies and wider product availability continue strengthening purchase frequency among health-conscious consumers. Online Retail represents the fastest-growing application as direct-to-consumer channels improve product accessibility and personalized marketing. Foodservice, including cafés, bakeries, and restaurants, continues expanding vegan dessert offerings, while Corporate Gifting and Seasonal Sales maintain strategic importance through premium product assortments and limited-edition launches. Manufacturers are strengthening omnichannel distribution while integrating automated inventory planning and demand forecasting. More than 31% of premium launches now debut through digital retail platforms before wider physical distribution, and approximately 26% of foodservice operators have expanded plant-based confectionery menus. These evolving application patterns are encouraging brands to optimize packaging, logistics, and promotional strategies for multiple consumption channels.

Individual Consumers remain the dominant end-user segment with an estimated 71% share, supported by increasing preference for plant-based lifestyles, healthier snacking habits, and premium confectionery purchases. Consistent demand across supermarkets, convenience stores, and online platforms reinforces large-scale production and product diversification. Commercial Foodservice is the fastest-growing end-user category as cafés, hotels, and restaurants broaden vegan dessert offerings to address evolving menu preferences. Institutional Buyers, including corporate cafeterias and hospitality providers, continue adopting plant-based confectionery within wellness-oriented food programs, while Specialty Retailers strengthen premium brand visibility through curated product selections. Companies are introducing differentiated packaging, premium formulations, and targeted pricing strategies to address diverse purchasing behavior. Around 33% of consumers actively seek confectionery with clean-label claims, while nearly 21% of hospitality operators have expanded vegan confectionery selections during the past two years. Competitive positioning increasingly depends on tailored product portfolios and integrated retail partnerships.

Europe accounted for the largest market share at 38.6% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.3% between 2026 and 2033.

North America accounted for approximately 29.4% of the global Plant-Based Vegan Confectionery Market in 2025, supported by strong premium food retail networks, advanced food manufacturing infrastructure, and continuous investment in dairy-free product innovation. Large-scale confectionery manufacturers are integrating automated ingredient handling and digital quality monitoring systems, improving production consistency while reducing processing waste. Private-label vegan confectionery portfolios continue expanding across major retail chains, increasing category accessibility. Manufacturing partnerships between ingredient suppliers and confectionery producers are strengthening localized procurement, helping reduce supply disruptions and improve operational flexibility. Growing investments in sustainable packaging and certified ingredient sourcing further reinforce long-term competitiveness across the regional value chain.

United States Market Outlook: The United States leads regional demand through its highly developed food manufacturing ecosystem, extensive organized retail presence, and strong product innovation capabilities. More than 40% of premium confectionery launches now include plant-based or dairy-free variants across major supermarket chains. Companies continue expanding dedicated production facilities, investing in alternative ingredient technologies, and strengthening partnerships with specialty ingredient suppliers to improve manufacturing efficiency and accelerate commercialization of premium vegan confectionery products.

Europe represents the largest regional market with approximately 38.6% share, supported by mature vegan food consumption, strict ingredient transparency requirements, and advanced confectionery manufacturing capabilities. Continuous modernization of processing facilities and increased adoption of certified sustainable cocoa strengthen operational efficiency throughout the production chain. Manufacturers are expanding clean-label product portfolios while investing in automated processing technologies that improve batch consistency and production flexibility. Cross-border distribution networks and premium retail channels continue supporting rapid commercialization of innovative dairy-free confectionery products across multiple consumer segments.

Germany Market Outlook: Germany remains the regional manufacturing leader due to its advanced food processing industry, strong confectionery production capacity, and well-established sustainable sourcing ecosystem. Approximately one-quarter of Europe's plant-based confectionery production is concentrated in Germany, supported by hundreds of specialized food manufacturers. Companies continue investing in dedicated vegan production lines, advanced ingredient processing, and product reformulation to strengthen premium positioning and export competitiveness across international markets.

Asia-Pacific accounted for nearly 21.8% of the global market in 2025 and continues strengthening its position through expanding food manufacturing capacity, urban consumer demand, and growing premium retail infrastructure. Local manufacturers are increasing investments in automated confectionery production, localized ingredient sourcing, and modern packaging technologies to improve operational efficiency. International brands are expanding manufacturing partnerships and regional production hubs to shorten supply chains and respond faster to changing consumer preferences. Rising availability of plant-based ingredients supports broader product diversification across established and emerging consumer markets.

Japan Market Outlook: Japan leads regional premium confectionery innovation through advanced food manufacturing technologies, precision processing capabilities, and strong quality control standards. More than 30% of premium confectionery innovation projects incorporate healthier or plant-based formulations. Companies continue enhancing automated production systems, investing in functional ingredient development, and expanding premium product portfolios that combine traditional confectionery expertise with evolving consumer wellness preferences.

South America accounted for approximately 6.1% of the global market in 2025, supported by expanding organized retail, rising premium food consumption, and gradual adoption of plant-based dietary preferences. Manufacturers are improving regional distribution capabilities while increasing localized packaging and processing operations to reduce logistics costs. Investment in domestic ingredient sourcing is improving supply-chain resilience despite periodic agricultural and transportation challenges. Premium supermarket chains continue expanding shelf space dedicated to dairy-free confectionery, creating stronger commercial opportunities for regional and international brands.

Brazil Market Outlook: Brazil represents the largest market in South America due to its extensive food manufacturing industry, expanding supermarket infrastructure, and growing consumer interest in plant-based foods. Nearly 35% of premium vegan confectionery sales within the region originate from Brazil. Companies are strengthening domestic production, expanding retail partnerships, and increasing investments in localized ingredient processing to improve product availability and operational efficiency.

The Middle East & Africa accounted for approximately 4.1% of the global market in 2025 as food manufacturing modernization, premium retail expansion, and investment in diversified food production continue strengthening market fundamentals. International confectionery producers are increasing partnerships with regional distributors while modern manufacturing facilities improve production capabilities for premium food categories. Retail expansion across major metropolitan areas is enhancing consumer access to specialized vegan confectionery products. Investment in cold-chain logistics and advanced packaging solutions is improving product quality throughout regional distribution networks.

United Arab Emirates Market Outlook: The United Arab Emirates serves as the region's primary commercial hub due to its advanced retail infrastructure, strong food import network, and premium consumer market. More than 45% of regional premium vegan confectionery imports are distributed through the country's established retail ecosystem. Companies continue expanding regional distribution centers, premium retail partnerships, and specialized food product portfolios to strengthen long-term market penetration and supply-chain efficiency.

The Plant-Based Vegan Confectionery Market is led by global confectionery manufacturers including Lindt & Sprüngli, Nestlé, Mondelēz International, Katjes Group, and Plamil Foods, competing directly with specialist vegan brands and agile regional producers. The top five participants collectively control approximately 42% of the market, while independent manufacturers compete through niche formulations and localized product portfolios. Competition centers on premium product quality, ingredient innovation, sustainable sourcing, manufacturing efficiency, and retail distribution rather than price alone. Automated production has improved manufacturing efficiency by nearly 16%, while clean-label formulations account for over 35% of new product launches and certified cocoa sourcing exceeds 40% among premium portfolios. Companies are expanding dedicated vegan production, securing long-term ingredient partnerships, investing in alternative protein technologies, and vertically integrating cocoa procurement to strengthen supply resilience. Competitive momentum is shifting toward premium innovation and supply-chain control as cocoa availability tightens. New entrants face significant barriers from formulation expertise, retailer relationships, certification requirements, and ingredient sourcing. Winning requires differentiated innovation, resilient procurement, scalable manufacturing, and trusted premium branding.

Nestlé S.A.

Mondelēz International, Inc.

Katjes Group

Plamil Foods Ltd.

Moo Free Chocolates

Vego Good Food GmbH

No Whey Foods

LoveRaw Ltd.

iChoc (EcoFinia GmbH)

Nomo (Kinnerton Confectionery)

Ritter Sport

Alter Eco Foods

Endangered Species Chocolate

Advanced formulation technologies are transforming plant-based vegan confectionery through precision fat replacement, plant protein optimization, and AI-assisted recipe development. Digital formulation platforms reduce product development time by approximately 20%, while automated ingredient dosing improves batch consistency by nearly 15%. Around 38% of premium manufacturers now deploy intelligent process monitoring to enhance quality control and reduce production variability. These technologies strengthen product texture, flavor stability, and manufacturing repeatability, creating a competitive advantage for premium brands.

Emerging technologies include precision fermentation, enzyme-assisted flavor enhancement, and digital twin manufacturing systems. Compared with conventional recipe development, AI-supported formulation delivers approximately 25% faster optimization and reduces experimental ingredient waste by nearly 18%. Manufacturers with integrated automation and advanced quality analytics benefit from shorter commercialization cycles, stronger retailer confidence, and improved operational efficiency across multiple production facilities.

Between 2026 and 2028, smart manufacturing platforms, predictive quality analytics, and sustainable ingredient processing are expected to become standard competitive capabilities. Adoption of connected production systems is projected to exceed 50% among leading premium confectionery manufacturers. Companies investing early in intelligent processing, alternative ingredient technologies, and automated manufacturing will strengthen product differentiation, accelerate innovation, improve supply-chain resilience, and secure long-term leadership in the evolving global plant-based confectionery industry.

April 2024 Lindt & Sprüngli introduced LINDOR Non-Dairy OatMilk Truffles across the United States, expanding its plant-based confectionery portfolio with two oat-based varieties. The launch strengthened premium vegan offerings and broadened retail reach for dairy-free consumers. Source: www.prnewswire.com

March 2025 Nestlé India launched KITKAT Professional Spread for hotels, restaurants, and catering businesses, extending the KITKAT brand into professional dessert applications. The product supports multiple hot and cold culinary uses, strengthening the company's foodservice portfolio. Source: www.nestle.in

September 2025 Plamil Foods launched a new range of 40 g vegan chocolate bars featuring updated branding and new flavors while maintaining value-focused pricing. The initiative strengthened product differentiation and reinforced the company's position within premium vegan confectionery. Source: www.plamilfoods.pressat.co.uk

June 2026 Lindt & Sprüngli achieved 100% Rainforest Alliance Certified cocoa sourcing through its Farming Program, strengthening sustainable raw material procurement and reinforcing supply-chain resilience across its global chocolate manufacturing operations.

This report provides comprehensive analysis of the Plant-Based Vegan Confectionery Market across major product types, applications, end-user categories, and key regional markets. It evaluates competitive positioning, manufacturing trends, sustainable ingredient adoption, retail expansion, and technology integration influencing industry development. The assessment covers premium chocolate, gummies, hard candies, marshmallows, and other vegan confectionery categories while examining evolving consumer purchasing patterns, distribution strategies, and enterprise investments across developed and emerging markets.

The report analyzes market dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, covering more than 40% premium product concentration among leading manufacturers and increasing automation across confectionery production. It provides strategic insights into formulation technologies, sustainable sourcing, digital manufacturing, and supply-chain optimization while supporting investment planning, product portfolio expansion, competitive benchmarking, partnership evaluation, and long-term business positioning throughout the 2026–2033 forecast period.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 4,070.0 Million |

| Market Revenue (2033) | USD 6,013.2 Million |

| CAGR (2026–2033) | 5.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Lindt & Sprüngli; Nestlé S.A.; Mondelēz International, Inc.; Katjes Group; Plamil Foods Ltd.; Moo Free Chocolates; Vego Good Food GmbH; No Whey Foods; LoveRaw Ltd.; iChoc (EcoFinia GmbH); Nomo (Kinnerton Confectionery); Ritter Sport; Alter Eco Foods; Endangered Species Chocolate |

| Customization & Pricing | Available on Request (10% Customization Free) |