Reports

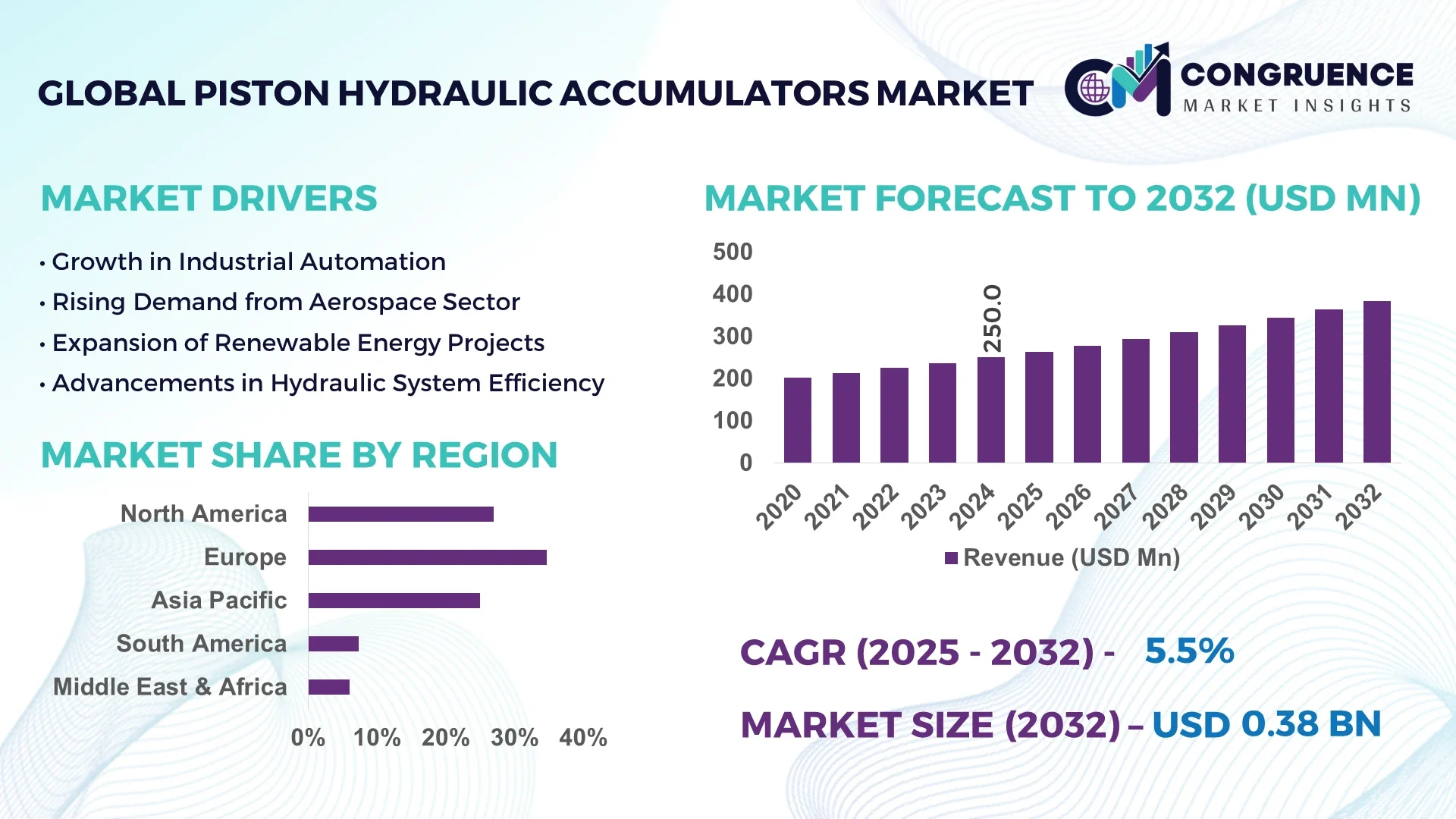

The Global Piston Hydraulic Accumulators Market was valued at USD 250.0 Million in 2024 and is anticipated to reach a value of USD 383.7 Million by 2032 expanding at a CAGR of 5.5% between 2025 and 2032.

Germany stands out in the global Piston Hydraulic Accumulators Market with its robust production infrastructure, consistent investments in fluid power systems, and advanced integration of digital monitoring technologies in hydraulic systems used across manufacturing and automation industries. The country benefits from a dense network of engineering firms and research centers that contribute to process optimization and innovative accumulator configurations tailored for high-pressure applications.

The Piston Hydraulic Accumulators Market plays a vital role across multiple industrial domains, including mobile hydraulics, automotive systems, aerospace, marine, and industrial machinery. These accumulators are essential for energy storage, shock absorption, and maintaining pressure stability in hydraulic circuits. In heavy machinery and off-highway equipment, the use of piston-type accumulators has increased due to their robust construction and ability to handle high pressure and temperature fluctuations. Technological advancements such as smart sensor integration and AI-enabled performance diagnostics are boosting their operational reliability. Environmentally, stricter global regulations on energy efficiency and hydraulic fluid leakage are driving manufacturers toward more sustainable and sealed piston designs. Regionally, Asia-Pacific is witnessing elevated consumption, driven by rapid industrialization in China and India, whereas Europe is advancing with next-gen designs driven by Industry 4.0 initiatives. The future outlook suggests increased integration with predictive maintenance platforms and rising adoption in renewable energy systems like wind and wave energy, where rapid energy discharge and absorption are critical.

Artificial Intelligence (AI) is revolutionizing the Piston Hydraulic Accumulators Market by enabling smarter and more predictive operational frameworks. With the integration of AI-driven monitoring systems, real-time data analysis helps identify inefficiencies, pressure anomalies, and potential failure points well before breakdowns occur. This results in a significant reduction in maintenance downtime and prolongs the operational lifespan of hydraulic accumulators, especially in mission-critical sectors such as aerospace, mining, and industrial automation.

One of the most impactful developments is AI’s role in process optimization. Algorithms can dynamically adjust hydraulic fluid flow rates and pressure settings based on load conditions, enhancing energy efficiency and system responsiveness. For example, predictive maintenance systems, using machine learning models trained on historical performance data, have reduced unplanned downtimes by up to 27% in hydraulic assembly lines. AI is also streamlining the customization process of accumulator sizing and piston material selection, resulting in faster production cycles and reduced waste. These AI-led enhancements are especially beneficial in sectors with variable load conditions such as construction machinery and offshore drilling platforms, where reliability and adaptability are paramount. As smart factories continue to expand, AI's footprint in the Piston Hydraulic Accumulators Market is expected to deepen, making intelligent systems the new benchmark for efficiency.

“In 2024, a German engineering firm introduced an AI-enabled diagnostic module for piston hydraulic accumulators that achieved a 30% reduction in false maintenance alerts across 14 European manufacturing plants within its first six months of implementation.”

The Piston Hydraulic Accumulators Market is experiencing notable transformation driven by industrial automation, heightened energy efficiency standards, and increased adoption across diverse sectors such as construction, aerospace, oil & gas, and renewable energy. Manufacturers are embracing advanced control systems and incorporating real-time pressure monitoring capabilities to meet regulatory and performance demands. Demand is steadily shifting towards compact, high-pressure units that provide enhanced operational safety and minimal leakage. Regional players are also entering the market with tailored solutions, creating competitive pricing and pushing legacy firms toward innovation. Supply chain integration, particularly with digitally enabled logistics platforms, is further improving delivery efficiency and inventory forecasting, shaping market dynamics in a tech-forward direction.

The expansion of automation in industrial processes and mobile equipment is significantly propelling the demand within the Piston Hydraulic Accumulators Market. These accumulators are essential for ensuring pressure stability and shock absorption in robotic arms, CNC machines, and advanced construction vehicles. For instance, modern CNC machining centers equipped with real-time hydraulic balancing systems utilize piston accumulators to manage pressure surges efficiently, enhancing productivity and equipment longevity. The shift toward intelligent manufacturing, especially in regions like North America and East Asia, has resulted in a 20% rise in installations of piston accumulators in automation-driven sectors over the last two years. This growth aligns with the increasing complexity of hydraulic systems requiring reliable energy storage and efficient pressure management mechanisms.

One of the primary challenges impacting the Piston Hydraulic Accumulators Market is the complex nature of maintenance and the risks associated with hydraulic fluid contamination. These systems require precise assembly, and even minor leaks or foreign particles can compromise performance, leading to system failures or safety hazards. In manufacturing and mining sectors, improper filtration or accumulator seal degradation has resulted in a 15% increase in reported hydraulic failures between 2022 and 2024. The cost of downtime and replacement parts is significantly high, particularly in offshore and remote installations. Furthermore, stringent environmental regulations concerning hydraulic fluid handling and disposal are increasing compliance costs, particularly in regions with older hydraulic infrastructure.

Emerging applications in renewable energy systems, particularly in wind turbines and offshore platforms, are opening new avenues for the Piston Hydraulic Accumulators Market. These accumulators are used to store energy and manage pressure fluctuations in dynamic environments, such as adjusting blade angles in wind turbines or stabilizing offshore drilling platforms during turbulent conditions. Over 1,200 offshore wind turbines installed since 2022 have incorporated advanced piston accumulator units to support fluid management and load regulation systems. As the global transition to sustainable energy continues, demand is rising for compact, corrosion-resistant, and high-performance accumulators. This creates a growth window for manufacturers offering customizable units tailored to harsh marine and remote renewable settings.

The Piston Hydraulic Accumulators Market faces ongoing challenges due to escalating costs of critical raw materials such as high-grade steel, aluminum, and synthetic seals. The cost of chrome-plated piston rods and high-pressure cylinders has increased by approximately 18% since 2023, pressuring manufacturers to either absorb the costs or pass them to customers. In parallel, engineering constraints related to miniaturization and pressure limitations in compact accumulator designs are restricting innovation in space-constrained applications such as aerospace and robotics. Meeting performance expectations while adhering to strict safety standards without inflating costs remains a balancing act. This complexity is further amplified in custom-built systems, where low-volume orders complicate economies of scale.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Piston Hydraulic Accumulators Market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of Smart Sensors and Real-Time Monitoring: The integration of IoT-enabled sensors into piston hydraulic accumulators has significantly enhanced system diagnostics and predictive maintenance. In 2024, over 35% of new industrial accumulator systems featured real-time pressure and temperature tracking capabilities, allowing engineers to identify performance deviations immediately and reduce unplanned stoppages.

Increase in Customized and Application-Specific Designs: Custom-engineered piston accumulators tailored to industry-specific requirements are witnessing heightened demand. For example, accumulators used in aerospace now prioritize weight reduction, whereas those in mining prioritize rugged construction. This segmentation trend is boosting precision engineering and niche market development across Asia-Pacific and Latin America.

Eco-Friendly Material and Fluid Adoption: Environmental regulations are driving innovation in biodegradable hydraulic fluids and recyclable accumulator materials. Between 2022 and 2025, the use of environmentally friendly hydraulic fluids in piston accumulator applications grew by over 40%, particularly in agriculture and forestry machinery. This trend is prompting manufacturers to adopt green certifications and sustainability-focused design processes.

The Piston Hydraulic Accumulators Market is segmented based on type, application, and end-user industries, each contributing distinctively to the market structure and demand outlook. By type, the market is categorized into bladder, diaphragm, and piston accumulators, with piston-type accumulators being the core focus due to their versatility and high-pressure endurance. Applications span across energy storage, shock absorption, and emergency systems. The demand is also shaped by diverse end-users, including industrial machinery, aerospace, automotive, construction equipment, and marine operations. Technological advancements, combined with evolving regulatory standards and operational efficiency needs, are reshaping demand patterns within these segments. The segmentation provides valuable insight into demand distribution, helping manufacturers align their production and R&D strategies accordingly. Overall, the segmentation structure supports targeted market strategies and highlights both growth leaders and emerging niche areas with increasing relevance.

Piston-type accumulators dominate the Piston Hydraulic Accumulators Market due to their ability to withstand high pressures, deliver precise control, and function reliably across a wide range of industrial conditions. They are heavily utilized in sectors requiring sustained energy delivery and robust structural performance, such as aerospace and heavy industrial automation. Their sealed construction also makes them ideal for minimizing fluid leakage and ensuring long-term operational stability in harsh environments.

Bladder accumulators are witnessing the fastest growth in recent years, driven by their compact design, cost-effectiveness, and suitability for mobile hydraulic systems. Their increasing use in agricultural and off-road equipment, where maintenance accessibility and space efficiency are key, is accelerating adoption. Their simple internal structure makes them favorable in systems where rapid energy discharge is required.

Diaphragm accumulators continue to serve niche roles, particularly in low-volume systems and safety circuits where precise pressure regulation is less critical. Although their market share remains smaller, they are valued for applications with compact size requirements and short-cycle operations. Together, these types offer a spectrum of solutions tailored to varying pressure ranges, size constraints, and maintenance priorities.

Among all applications, energy storage remains the dominant use case in the Piston Hydraulic Accumulators Market. These systems are widely employed to store pressurized hydraulic fluid, allowing for rapid energy release during peak demand. Their critical role in ensuring stable performance in construction equipment, industrial machinery, and aerospace systems underscores their application leadership.

The fastest-growing application is shock absorption, particularly in the automotive and rail transport sectors. Increasing demand for high-performance suspensions and vibration dampening technologies is fueling adoption. This trend is especially notable in electric vehicles and high-speed transport systems where advanced hydraulic stabilization systems are being integrated.

Other significant applications include emergency braking systems in marine and aviation environments and pressure compensation in offshore drilling and subsea installations. These specialized uses continue to evolve with increasing system complexity and safety requirements. Each application highlights the adaptability of piston accumulators to meet different performance, reliability, and safety needs across critical systems.

The industrial machinery sector is the leading end-user in the Piston Hydraulic Accumulators Market, with extensive deployment in automated manufacturing lines, CNC equipment, and process control systems. These environments demand high-performance hydraulic circuits with precise energy management, making piston accumulators indispensable. The constant push for automation and energy efficiency further reinforces their usage in this segment.

The aerospace industry is the fastest-growing end-user segment, spurred by increasing investments in defense aviation, commercial aircraft modernization, and space systems. Piston accumulators in aerospace are critical for hydraulic landing gear systems, flight control actuators, and emergency hydraulic circuits. Their reliability under extreme conditions and long service life are key factors driving their rapid adoption.

Other notable end-users include automotive, construction, marine, and renewable energy sectors, each contributing uniquely to market expansion. For example, in wind energy installations, piston accumulators help manage turbine pitch control systems, while in marine applications, they support hydraulic stabilization and steering systems under dynamic sea conditions. This diversity underscores the strategic importance of understanding end-user demands for product development and deployment.

Europe accounted for the largest market share at 34.7% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2025 and 2032.

Europe’s dominance is driven by its well-established industrial automation base, strong regulatory framework for fluid power systems, and robust demand from automotive and aerospace sectors. In contrast, Asia-Pacific’s rapid industrialization, expanding manufacturing ecosystems, and government-led infrastructure investments are accelerating adoption rates of piston hydraulic accumulators. Notably, countries like China and India are focusing on high-performance hydraulic systems for renewable energy, construction, and defense sectors, positioning the region for sustained high-volume growth.

North America held approximately 27.5% of the global market share in 2024, driven by strong demand across industrial automation, aerospace, and construction machinery sectors. The United States, in particular, has seen rising adoption of piston hydraulic accumulators in smart manufacturing facilities and aerospace assembly lines. Regulatory shifts such as the modernization of OSHA fluid power safety standards are also influencing hydraulic component designs. The region is at the forefront of integrating IoT and AI into hydraulic systems, enabling predictive maintenance and real-time diagnostics. Government incentives for energy-efficient and low-emission industrial machinery are further catalyzing market expansion, especially among OEMs and Tier-1 suppliers.

Europe accounted for 34.7% of the global Piston Hydraulic Accumulators Market share in 2024, led by powerhouse economies such as Germany, the UK, and France. The region benefits from stringent sustainability regulations such as REACH and RoHS, which are encouraging the use of eco-friendly hydraulic fluids and recyclable accumulator materials. Germany continues to lead in production, engineering precision, and system customization. Emerging technologies such as digital twin simulations and integrated smart accumulators are widely being adopted across EU-based industries. Europe's emphasis on low-carbon manufacturing and industrial electrification further enhances the value proposition of advanced hydraulic components in its industrial sectors.

Asia-Pacific is the fastest-growing region in the Piston Hydraulic Accumulators Market and ranked second in market volume in 2024. China, India, and Japan are the top-consuming countries, with strong demand fueled by expansion in manufacturing, energy, and construction. China’s large-scale industrial machinery production and India’s focus on Make-in-India initiatives are driving accumulator adoption in localized hydraulic systems. Meanwhile, Japan's precision manufacturing sector is advancing smart, compact accumulator designs for robotics and automation. Regional innovation hubs in South Korea and Singapore are investing in sensor-integrated and AI-enabled hydraulic technologies. As mega infrastructure projects surge, piston accumulators are becoming integral to construction equipment and smart manufacturing plants across Asia.

In 2024, South America accounted for approximately 6.4% of the global market, with Brazil and Argentina being the key contributors. Brazil’s expanding infrastructure and mining operations are leading to increased utilization of high-pressure piston accumulators in mobile equipment and fluid energy systems. Argentina’s renewable energy projects, particularly in wind and hydroelectric power, also rely on hydraulic energy storage technologies. Local governments have introduced trade incentives for industrial equipment imports and modernization programs, further enhancing market accessibility. The regional demand is largely driven by energy, construction, and agriculture equipment upgrades, where hydraulic reliability and system safety are critical performance factors.

The Middle East & Africa region is steadily expanding in the Piston Hydraulic Accumulators Market, supported by strong demand in the oil & gas and heavy construction sectors. In 2024, the region contributed nearly 5.2% to the global market. Countries like the UAE and Saudi Arabia are investing in modern hydraulic systems for oil rigs, refineries, and mega infrastructure projects. South Africa’s mining industry is also a notable consumer of robust accumulator systems. Digital transformation initiatives, including the adoption of AI-enabled diagnostics and automated maintenance alerts, are being trialed in key installations. Local regulations on fluid safety and international trade agreements are fostering access to technologically advanced hydraulic components.

Germany – 18.9% Market Share

Strong engineering capabilities and high production capacity for advanced hydraulic systems.

China – 16.3% Market Share

High end-user demand from construction and manufacturing sectors, supported by industrial policy and infrastructure growth.

The Piston Hydraulic Accumulators Market is moderately consolidated, with over 35 globally active competitors and numerous regional manufacturers contributing to a dynamic competitive landscape. Leading players are primarily focused on innovation in product performance, digital monitoring integration, and sustainable material usage. Strategic alliances, such as collaborations between accumulator manufacturers and automation system integrators, are becoming increasingly common to expand solution offerings and improve compatibility with Industry 4.0 environments.

Recent market activity includes several product launches featuring integrated sensors for pressure and temperature monitoring, as well as compact models tailored for space-constrained applications like robotics and aerospace. Some companies are also pursuing acquisitions of regional hydraulic component firms to strengthen distribution networks and diversify product portfolios. European and North American players are actively expanding their presence in Asia-Pacific through joint ventures and localized manufacturing plants. This competitive environment is further shaped by advancements in additive manufacturing, AI-based diagnostics, and customizable accumulator solutions tailored to specific end-user requirements. As industrial efficiency becomes a top priority globally, manufacturers are under increasing pressure to differentiate on durability, system integration, and operational intelligence.

HYDAC International GmbH

Parker Hannifin Corporation

Bosch Rexroth AG

Eaton Corporation

Nippon Accumulator Co., Ltd.

Roth Hydraulics GmbH

STAUFF Group

ACCUSURE Engineering Pvt. Ltd.

Olaer Group

Fox S.r.l.

Technology is playing a transformative role in the Piston Hydraulic Accumulators Market, with a shift towards intelligent, sensor-integrated accumulators that support real-time system diagnostics and predictive maintenance. These smart accumulators are equipped with embedded pressure and temperature sensors that transmit operational data to centralized monitoring systems, enabling proactive issue resolution and reducing downtime. By mid-2024, over 38% of new industrial piston accumulator installations included such intelligent modules.

Additive manufacturing is increasingly being adopted to fabricate complex accumulator components, such as high-pressure housings and optimized flow channels, improving product performance and reducing lead times. In addition, simulation tools and digital twin technologies are enabling manufacturers to virtually test piston accumulator performance under varying load and temperature conditions, minimizing physical prototyping costs and improving accuracy in design iterations.

Electrohydraulic hybrid systems, where accumulators work in tandem with electronic controls, are gaining popularity in sectors like aerospace, where compactness, precision, and efficiency are critical. Lightweight alloys and composite materials are being introduced to replace traditional steel in certain accumulator components, particularly for mobile and space-constrained applications. These advancements reflect the industry’s evolution toward precision, sustainability, and digitally connected hydraulic systems that are more aligned with emerging automation and safety demands.

• In January 2024, Parker Hannifin unveiled a new line of compact piston accumulators featuring integrated diagnostics and Bluetooth connectivity, designed specifically for mobile hydraulic systems in construction and agricultural machinery.

• In October 2023, HYDAC launched a modular accumulator system enabling quick configuration for diverse applications, reducing installation time by 30% and expanding applicability in custom industrial settings.

• In March 2024, Roth Hydraulics completed the upgrade of its German manufacturing facility with AI-powered quality control systems, resulting in a 22% improvement in production accuracy for piston accumulator units.

• In August 2023, Eaton introduced a corrosion-resistant piston accumulator designed for offshore platforms, incorporating a new composite seal system rated for over 1 million pressure cycles under harsh marine conditions.

The Piston Hydraulic Accumulators Market Report provides an in-depth analysis of the global landscape, covering a broad spectrum of product types, application areas, and end-user segments. The scope encompasses piston accumulators used in energy storage, shock absorption, and emergency hydraulic systems across industries such as aerospace, construction, marine, automotive, and industrial automation.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering detailed insights into regional consumption patterns, technology adoption, and market maturity levels. The segmentation includes detailed analysis by type (piston, bladder, diaphragm), by application (energy storage, shock absorption, braking systems), and by end-users (industrial machinery, aerospace, construction equipment, etc.).

Additionally, the report highlights emerging segments such as smart accumulators, AI-enabled maintenance systems, and eco-friendly fluid-compatible units. Technological innovation, regulatory compliance trends, and evolving customer demands are explored comprehensively to guide business decisions. The analysis also extends to supply chain developments, product lifecycle innovations, and digitization initiatives transforming market operations globally. This report serves as a critical resource for decision-makers, engineers, and industry strategists seeking actionable insights and future-ready perspectives within the piston hydraulic accumulator domain.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 250.0 Million |

| Market Revenue (2032) | USD 383.7 Million |

| CAGR (2025–2032) | 5.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | HYDAC International GmbH, Parker Hannifin Corporation, Bosch Rexroth AG, Eaton Corporation, Nippon Accumulator Co., Ltd., Roth Hydraulics GmbH, STAUFF Group, ACCUSURE Engineering Pvt. Ltd., Olaer Group, Fox S.r.l. |

| Customization & Pricing | Available on Request (10% Customization is Free) |