Reports

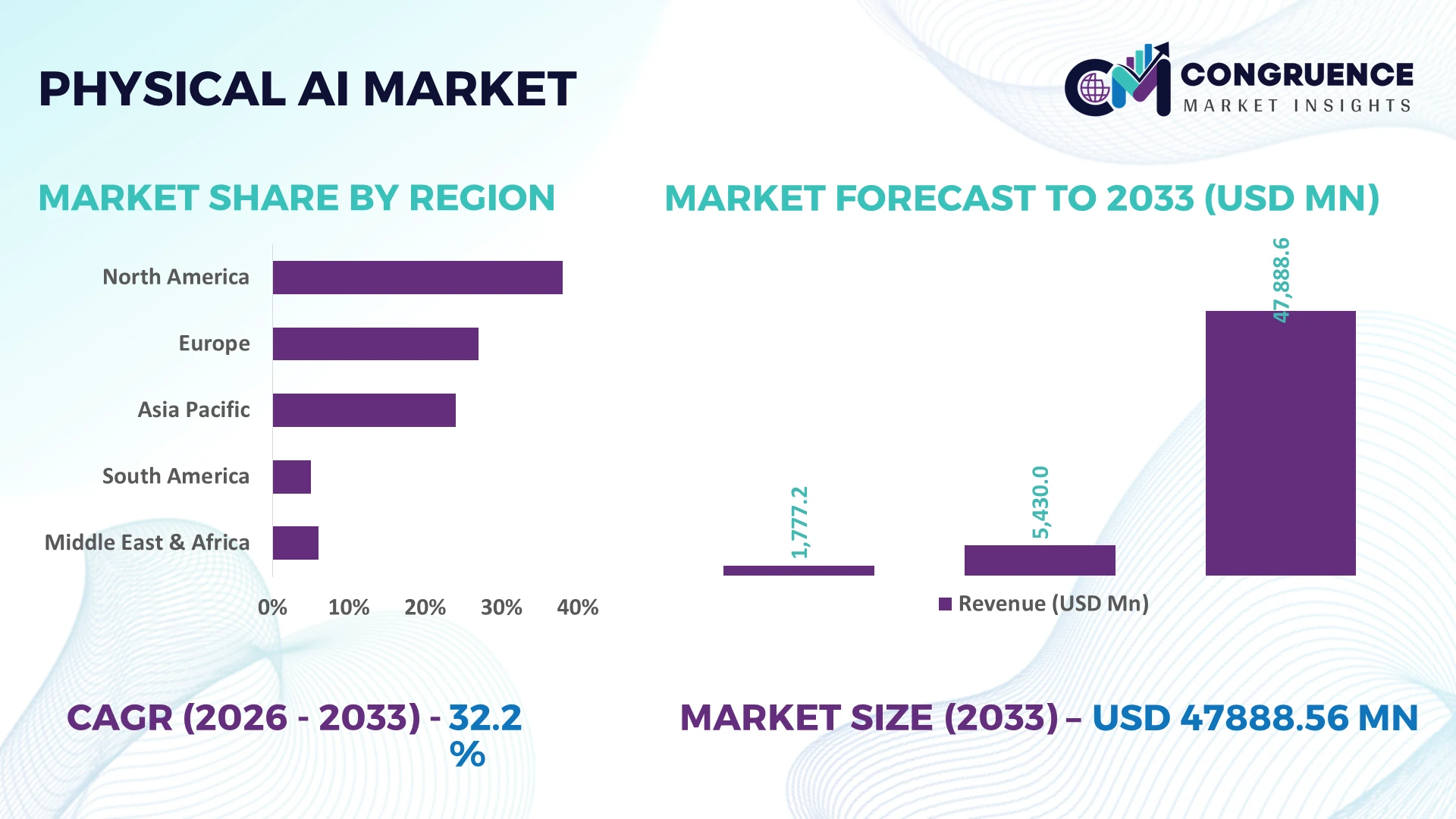

The Global Physical AI Market was valued at USD 5430 Million in 2025 and is anticipated to reach a value of USD 47888.56 Million by 2033 expanding at a CAGR of 32.21% between 2026 and 2033. Growth is primarily driven by accelerated deployment of AI-enabled robotics, edge computing platforms, autonomous industrial systems, and multimodal foundation models across manufacturing, logistics, healthcare, and defense operations.

The United States leads the global Physical AI Market with approximately 39% of advanced deployment activity, supported by multi-billion-dollar semiconductor and robotics investments, while China accounts for nearly 30% through rapid smart manufacturing expansion and large-scale automation programs. Following the 2026 global semiconductor supply-chain diversification initiatives, Japan and South Korea strengthened industrial AI hardware production, with industrial robot density exceeding 400 units per 10,000 manufacturing employees in leading facilities, reinforcing regional competitiveness.

Organizations prioritizing scalable AI hardware ecosystems, edge intelligence, and robotics integration are positioned to secure long-term operational advantages across high-value industrial sectors.

Market Size & Growth: USD 5430 Million (2025) to USD 47888.56 Million (2033) at 32.21% CAGR, driven by industrial robotics, edge AI processors, and autonomous system deployment.

Top Growth Drivers: AI-enabled robotics adoption exceeds 28%; factory automation investments rise 24%; edge computing integration expands 31% globally.

Short-Term Forecast: By 2028, production efficiency improves 22%, predictive maintenance costs decline 18%, and inspection accuracy exceeds 95%.

Emerging Technologies: Multimodal AI, edge intelligence, digital twins, and autonomous mobile robots accelerate high-growth industrial transformation.

Regional Leaders: North America approaches USD 17 Billion, Asia-Pacific USD 19 Billion, Europe USD 9 Billion, supported by manufacturing modernization and regional supply-chain expansion.

Consumer/End-User Trends: Over 63% of large manufacturers prioritize Physical AI for autonomous operations and intelligent asset management.

Pilot/Case Example: 2026 smart factory deployments achieved 27% lower downtime through AI-powered robotic inspection and predictive analytics.

Competitive Landscape: Top suppliers collectively control nearly 46% of advanced deployments, led by NVIDIA, ABB, Siemens, Boston Dynamics, and FANUC.

Regulatory & ESG Impact: AI governance and energy-efficiency initiatives reduce operational energy consumption by approximately 15% across automated facilities.

Investment & Funding: More than USD 20 Billion supports robotics, AI infrastructure, semiconductor partnerships, and industrial automation expansion worldwide.

Innovation & Future Outlook: Next-generation embodied AI, humanoid robotics, and edge-native intelligence strengthen autonomous decision-making across complex industrial environments.

Physical AI Market demand is expanding across autonomous manufacturing, warehouse automation, healthcare robotics, and intelligent mobility, where real-time perception and adaptive decision-making deliver measurable operational gains. Nearly 35% of new industrial automation projects now incorporate AI-enabled robotic systems. Ongoing hardware localization and evolving AI governance frameworks are accelerating resilient deployment strategies, setting the stage for broader strategic market expansion.

Physical AI is becoming a strategic priority because competitive advantage increasingly depends on autonomous decision-making at the edge rather than centralized software intelligence. Manufacturers, logistics operators, and defense organizations are integrating AI directly into robots, industrial equipment, and autonomous vehicles to improve operational resilience. The ongoing restructuring of semiconductor supply chains and accelerated industrial digitalization since 2026 have strengthened investment in localized AI hardware, robotics platforms, and intelligent sensing infrastructure across advanced manufacturing ecosystems.

Compared with conventional rule-based automation, Physical AI systems improve real-time object recognition accuracy by nearly 30% while reducing inspection and response times by approximately 40% through multimodal perception and adaptive learning. The United States leads in AI chip innovation and commercial deployment, whereas China scales industrial robotics through large manufacturing clusters and government-backed automation initiatives. Over the next two to three years, enterprise adoption of AI-enabled robotic platforms is expected to exceed 45% among large manufacturers, with warehouse automation and predictive maintenance remaining the fastest operational priorities.

A practical example is the deployment of AI-powered autonomous mobile robots in distribution centers, where dynamic navigation and real-time inventory recognition have reduced order processing delays by nearly 25%. Companies are expanding partnerships between robotics developers, semiconductor suppliers, and industrial software providers to accelerate commercialization while strengthening localized production capacity. Organizations that integrate Physical AI with scalable edge infrastructure and cross-industry ecosystems will secure stronger operational flexibility, higher productivity, and sustainable competitive positioning.

The rapid convergence of industrial robotics, edge AI computing, and intelligent vision systems is transforming Physical AI deployment across manufacturing and logistics. More than 60% of large industrial facilities now prioritize autonomous operations, while AI-enabled predictive maintenance reduces unplanned equipment downtime by approximately 30% and improves asset utilization by over 20%. Japan continues expanding advanced robotics density, while the United States increases domestic AI hardware manufacturing following strategic semiconductor initiatives. In response, technology companies are investing in AI accelerators, robotics software, and integrated automation platforms through acquisitions, partnerships, and production expansion. This structural shift enables faster operational decisions, lower labor dependency, and more resilient industrial ecosystems.

Physical AI deployment remains constrained by complex integration requirements across legacy machinery, sensors, and industrial software environments. Initial implementation costs for enterprise-scale autonomous systems remain 25–35% higher than conventional automation projects, while integration activities account for nearly 30% of deployment timelines. Dependence on advanced AI processors and specialized components continues to pressure supply availability despite manufacturing diversification efforts in the United States and Japan. Companies are mitigating these constraints through modular architectures, localized component sourcing, and long-term semiconductor procurement agreements. Businesses achieving standardized interoperability reduce deployment complexity while improving scalability and protecting long-term operational investments.

Embodied AI is creating new commercial opportunities by enabling robots to interpret environments, learn continuously, and execute complex physical tasks with minimal human intervention. Autonomous warehouse operations improve fulfillment productivity by nearly 35%, while AI-driven inspection systems reduce quality-control defects by approximately 28%. South Korea and Singapore continue accelerating smart manufacturing initiatives through industrial AI infrastructure and advanced robotics programs. Companies are increasing investment in multimodal foundation models, collaborative robotics, and digital twin ecosystems to deliver adaptive automation across diverse industries. Organizations developing interoperable Physical AI platforms gain access to recurring software services, intelligent maintenance solutions, and high-value industrial applications beyond traditional automation.

Long-term commercialization depends on consistent deployment across complex industrial environments where cybersecurity, workforce readiness, and infrastructure maturity remain critical. Around 45% of industrial organizations identify AI system integration skills as a significant operational gap, while connected autonomous assets increase cyber risk exposure by more than 30% compared with isolated automation networks. Germany and the United States are strengthening industrial cybersecurity standards alongside expanding AI governance requirements. Companies must invest in secure edge computing, workforce reskilling, simulation-based validation, and resilient communications infrastructure to maintain dependable autonomous performance. Organizations that successfully combine trusted AI governance with scalable operational deployment will establish stronger long-term competitiveness and customer confidence.

Edge AI Becomes Standard Enterprise deployments increasingly process intelligence at the edge, reducing cloud dependency and improving response times by nearly 45%. Around 58% of new industrial AI projects now integrate edge inference hardware, driven by latency requirements and cybersecurity priorities. Companies are redesigning automation architectures, expanding semiconductor partnerships, and deploying distributed AI infrastructure to improve production continuity and operational resilience.

Multimodal Robotics Expansion Physical AI platforms now combine vision, language, and sensor fusion, enabling robots to perform complex tasks with approximately 32% higher object-recognition accuracy and 25% faster workflow execution than earlier systems. Labor shortages across Japan and Germany are accelerating enterprise adoption. Robotics developers are scaling collaborative platforms, integrating foundation models, and strengthening partnerships with industrial equipment manufacturers to improve deployment flexibility.

AI-Native Factory Modernization Manufacturers are replacing isolated automation with connected Physical AI ecosystems where autonomous robots, AI sensors, and predictive control systems operate simultaneously. More than 50% of newly upgraded production facilities now integrate intelligent robotics, while maintenance interventions decline by nearly 28%. Companies are restructuring digital manufacturing strategies and standardizing interoperable platforms to simplify plant-wide deployment and improve asset utilization.

Localized Hardware Ecosystems Strengthen Semiconductor diversification and supply-chain resilience initiatives are shifting production closer to end markets, reducing component lead times by approximately 20% and improving procurement stability by nearly 18%. The United States and South Korea continue expanding advanced AI hardware capacity. Companies are increasing domestic manufacturing, securing long-term supplier agreements, and co-developing specialized AI processors to support large-scale Physical AI commercialization.

Autonomous Robots represent the leading segment because they deliver scalable automation across manufacturing, logistics, and infrastructure operations while reducing dependence on manual intervention. Their ability to navigate dynamic environments, perform continuous operations, and integrate with industrial AI platforms has made them the preferred deployment choice, accounting for nearly 41% of enterprise Physical AI implementations. AI Sensors remain essential for environmental perception and real-time decision-making, while Edge AI Systems strengthen local processing by reducing latency by approximately 40%. Companies continue expanding robotics software ecosystems and embedded AI capabilities to improve deployment efficiency.

Humanoid Robots are emerging as the fastest-growing type as enterprises evaluate them for complex human-centric workflows including warehouse support, inspection, and service operations. AI Drones continue expanding across infrastructure monitoring and precision agriculture, improving inspection productivity by almost 35%. Technology providers are increasing investment in modular hardware platforms, multimodal AI integration, and strategic robotics partnerships, reflecting shifting enterprise priorities toward adaptive, interoperable Physical AI systems capable of operating across multiple industrial environments.

Manufacturing remains the dominant application because Physical AI directly improves production efficiency, predictive maintenance, and automated quality inspection across high-volume industrial facilities. Nearly 46% of enterprise deployments are concentrated in manufacturing, where intelligent robotics and AI sensors reduce equipment downtime by approximately 30% while improving inspection consistency. Logistics follows as a mature application through warehouse automation and autonomous material handling, prompting technology suppliers to expand integrated robotics and software platforms for industrial customers.

Autonomous Vehicles represent the fastest-growing application as AI perception, sensor fusion, and edge computing accelerate intelligent mobility systems. Healthcare is rapidly adopting Physical AI for robotic assistance and precision procedures, while Agriculture benefits from AI-enabled drones and autonomous equipment that improve field productivity by nearly 25%. Companies are expanding deployment partnerships, strengthening software integration, and developing application-specific AI platforms to address operational requirements across increasingly diverse industries.

Manufacturing is the largest end-user segment due to extensive automation requirements, continuous production environments, and significant dependence on intelligent robotics. Approximately 48% of enterprise Physical AI investments originate from manufacturers seeking higher throughput, improved quality control, and predictive maintenance capabilities. Automotive companies remain major adopters through AI-powered assembly and inspection systems, while Retail increasingly deploys autonomous inventory management and warehouse robotics. Vendors continue customizing integrated AI platforms and expanding industrial partnerships to strengthen long-term enterprise adoption.

Defense is the fastest-growing end-user segment as autonomous systems, intelligent surveillance platforms, and AI-enabled mission support become strategic priorities. Healthcare organizations are increasing investment in robotic assistance and intelligent diagnostics, while Automotive manufacturers continue modernizing production through collaborative robotics. Companies are developing industry-specific solutions, flexible deployment models, and ecosystem partnerships, enabling customers to accelerate implementation while improving operational efficiency, safety, and long-term infrastructure scalability.

North America accounted for the largest market share at 37.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 34.9% CAGR between 2026 and 2033.

Industrial AI Infrastructure Accelerates Enterprise Automation

North America maintains the leading position through advanced AI semiconductor production, mature robotics deployment, and extensive enterprise digital transformation. The region represents approximately 37.8% of global Physical AI adoption, supported by strong investments in autonomous manufacturing, logistics automation, and defense technologies. AI-enabled robotic systems are increasingly integrated with edge computing platforms, reducing operational latency by nearly 40% in large industrial environments. Strategic partnerships between semiconductor manufacturers, robotics developers, and cloud infrastructure providers continue strengthening commercialization. The expansion of domestic AI hardware production and intelligent factory modernization further improves supply resilience while enabling enterprises to scale autonomous operations across manufacturing, warehousing, healthcare, and transportation sectors.

United States Market Outlook: The United States leads regional deployment through its advanced semiconductor ecosystem, AI software leadership, and strong industrial automation capabilities. More than 60% of large manufacturing enterprises are actively integrating AI-enabled robotics into production and warehouse operations. Federal support for semiconductor manufacturing, combined with growing private investment in embodied AI and autonomous systems, is strengthening domestic production capacity while accelerating commercialization across industrial, healthcare, defense, and logistics applications.

Smart Manufacturing and Industrial Modernization Drive Adoption

Europe continues expanding Physical AI deployment through advanced manufacturing modernization, industrial automation, and AI governance frameworks that encourage secure enterprise adoption. The region contributes nearly 26% of global implementation activity, supported by automotive, precision engineering, and industrial equipment sectors. Intelligent robotics deployments improve production efficiency by approximately 24% while reducing maintenance interventions across digitally connected factories. Companies increasingly integrate collaborative robotics, AI sensors, and edge intelligence into existing manufacturing systems. Sustainability objectives also encourage energy-efficient automation, prompting enterprises to modernize production infrastructure while strengthening cross-border industrial technology partnerships.

Germany Market Outlook: Germany remains the region's strongest market due to its globally competitive automotive manufacturing base, industrial robotics leadership, and advanced engineering capabilities. Factory automation continues expanding through AI-powered production systems, with industrial robot density among the world's highest. Manufacturers increasingly invest in intelligent inspection, predictive maintenance, and autonomous material handling to strengthen production flexibility and improve export competitiveness across high-value manufacturing sectors.

Manufacturing Scale Fuels AI Deployment

Asia-Pacific is emerging as the fastest-expanding market because of its large manufacturing ecosystem, accelerating industrial automation, and expanding AI hardware production capacity. The region accounts for approximately 33% of global Physical AI deployment and continues increasing investments in robotics manufacturing, semiconductor fabrication, and smart industrial infrastructure. Industrial automation projects have increased by nearly 30% across key manufacturing hubs, while AI-enabled robotics improve production throughput and operational consistency. Governments and enterprises continue prioritizing intelligent factories, localized semiconductor ecosystems, and autonomous logistics networks to strengthen global manufacturing competitiveness.

China Market Outlook: China dominates regional deployment through its extensive manufacturing capacity, large robotics installation base, and continuous investment in intelligent production. Domestic manufacturers are rapidly integrating AI-enabled autonomous robots and machine vision systems into electronics, automotive, and logistics facilities. Smart manufacturing initiatives continue expanding nationwide, while localized AI chip production and industrial software development strengthen supply-chain resilience and accelerate enterprise-scale Physical AI adoption.

Industrial Automation Expands Beyond Traditional Sectors

South America is steadily adopting Physical AI across manufacturing, mining, agriculture, and logistics as enterprises pursue higher operational efficiency despite infrastructure constraints. The region contributes nearly 6% of global market activity, with automation deployments increasing by approximately 18% in major industrial facilities. Mining companies increasingly utilize autonomous inspection systems and AI-enabled monitoring technologies to improve equipment utilization and worker safety. Businesses are strengthening partnerships with global automation providers while modernizing production assets to improve productivity and reduce operational disruptions across resource-intensive industries.

Brazil Market Outlook: Brazil leads regional demand through its diversified industrial economy, expanding logistics infrastructure, and strong agricultural technology adoption. Manufacturing companies increasingly deploy intelligent robotics and AI-powered warehouse automation to improve operational performance. Precision agriculture also supports wider adoption of AI drones and autonomous equipment, enabling producers to optimize field operations while strengthening productivity across large-scale commercial farming and food processing industries.

Infrastructure Investment Supports Intelligent Automation

The Middle East & Africa market is advancing through large-scale infrastructure modernization, industrial diversification, and government-supported digital transformation programs. The region represents approximately 5% of global Physical AI deployment, with intelligent automation increasingly adopted across logistics, energy, manufacturing, and smart city projects. Industrial AI deployments improve asset monitoring efficiency by nearly 22%, while investments in digital infrastructure strengthen autonomous operations across critical industries. Enterprises continue expanding technology collaborations and automation partnerships to support long-term modernization while improving operational resilience in strategic industrial sectors.

Saudi Arabia Market Outlook: Saudi Arabia leads regional development through extensive investment in smart manufacturing, industrial digitalization, and advanced infrastructure projects aligned with national economic diversification objectives. Industrial facilities are integrating AI-enabled robotics, intelligent inspection systems, and autonomous logistics technologies to improve operational efficiency. Continued expansion of technology partnerships and advanced manufacturing initiatives is strengthening enterprise adoption while positioning the country as a regional hub for intelligent industrial transformation.

The Physical AI market is led by NVIDIA, ABB, Siemens, FANUC, and Boston Dynamics, competing directly against specialized robotics developers, industrial automation OEMs, AI chip designers, and regional system integrators. The top five players collectively control approximately 47% of advanced enterprise deployments through integrated hardware, AI software, and robotics ecosystems. Competition centers on computing performance, deployment speed, supply-chain resilience, and platform interoperability rather than price alone. AI-enabled automation platforms deliver nearly 35% faster deployment cycles, while optimized edge computing reduces inference latency by about 40%, creating measurable operational advantages. Global technology leaders emphasize proprietary AI models and semiconductor integration, whereas regional automation firms compete through customized industrial solutions and localized implementation services. Strategic partnerships between robotics manufacturers, semiconductor suppliers, and industrial software providers are accelerating commercialization, while selective acquisitions strengthen vertical integration. Tight AI chip availability and high engineering expertise remain major entry barriers. Winning requires scalable AI ecosystems, dependable hardware supply, rapid deployment capability, and continuous innovation aligned with enterprise operational requirements.

NVIDIA Corporation

ABB Ltd.

Siemens AG

FANUC Corporation

Boston Dynamics

Rockwell Automation, Inc.

Teradyne, Inc.

Zebra Technologies Corporation

Qualcomm Incorporated

Tesla, Inc.

Agility Robotics

Sanctuary AI

Figure AI

Universal Robots A/S

Current Physical AI innovation is centered on multimodal AI models, edge AI processors, intelligent vision systems, and high-performance robotics controllers. More than 55% of new industrial deployments integrate edge inference to enable real-time decision-making without continuous cloud connectivity. AI-powered perception improves object recognition accuracy by approximately 30%, while advanced sensor fusion reduces navigation errors by nearly 25%. Manufacturers and logistics operators benefit most because these technologies improve productivity while reducing operational interruptions and response latency.

Emerging technologies include embodied AI, digital twins, collaborative robotics, and event-driven AI sensors that continuously adapt to changing environments. Compared with conventional rule-based automation, embodied AI platforms complete dynamic industrial tasks nearly 35% faster while lowering manual intervention by approximately 28%. Around 40% of enterprise automation projects now evaluate digital twin integration before large-scale deployment, allowing companies to optimize workflows virtually before implementation. Technology providers increasingly combine robotics, AI software, and semiconductor expertise through integrated development partnerships.

Between 2026 and 2028, autonomous learning systems, specialized AI accelerators, and edge-native robotics platforms will redefine industrial automation. Early adopters gain faster deployment cycles, improved asset utilization, and stronger operational resilience as localized AI hardware becomes more widely available. Organizations investing now in interoperable Physical AI architectures, secure edge computing, and scalable robotics ecosystems will establish stronger competitive differentiation while reducing long-term integration complexity across manufacturing, logistics, healthcare, and intelligent mobility applications.

March 2024 NVIDIA introduced Project GR00T alongside the Jetson Thor robot computer and expanded the Isaac robotics platform to accelerate humanoid robot development. The new platform targets next-generation Physical AI with accelerated simulation and robot learning capabilities.

March 2025 NVIDIA released the open-weight Isaac GR00T N1 foundation model for humanoid robots, demonstrating higher benchmark performance than previous imitation-learning approaches across multiple robot embodiments. The launch accelerated ecosystem collaboration and lowered barriers for Physical AI application development.

March 2026 ABB Robotics and NVIDIA announced a strategic partnership integrating NVIDIA Omniverse with RobotStudio HyperReality, achieving up to 99% simulation-to-real deployment accuracy. The collaboration significantly shortens industrial robot commissioning cycles and expands enterprise-scale Physical AI deployment.

March 2026 NVIDIA unveiled its Physical AI Data Factory Blueprint at GTC 2026, introducing an open architecture for generating and validating large-scale robot training datasets using synthetic and real-world data. The initiative improves AI model robustness while accelerating robotics development workflows.

This report delivers comprehensive analysis of the Physical AI market across Humanoid Robots, Autonomous Robots, AI Drones, AI Sensors, and Edge AI Systems, while evaluating applications spanning manufacturing, logistics, healthcare, agriculture, and autonomous vehicles. It assesses demand patterns across manufacturing, healthcare, automotive, retail, and defense, covering North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 45% of enterprise deployments analyzed focus on intelligent industrial automation and edge-based autonomous operations.

The study examines competitive positioning, technology adoption, deployment strategies, robotics ecosystems, AI hardware integration, and emerging embodied AI platforms between 2026 and 2033. It evaluates enterprise expansion priorities, innovation pipelines, partnership strategies, supply-chain developments, and regional investment momentum to support strategic planning. The report also identifies high-potential niche opportunities, evolving deployment trends, and operational benchmarks that help organizations strengthen market positioning, optimize technology investments, and improve long-term competitive decision-making.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 5430 Million |

Market Revenue in 2033 | USD 47888.56 Million |

CAGR (2026 - 2033) | 32.21% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | NVIDIA Corporation, ABB Ltd., Siemens AG, FANUC Corporation, Boston Dynamics, Rockwell Automation, Inc., Teradyne, Inc., Zebra Technologies Corporation, Qualcomm Incorporated, Tesla, Inc., Agility Robotics, Sanctuary AI, Figure AI, Universal Robots A/S |

Customization & Pricing | Available on Request (10% Customization is Free) |