Reports

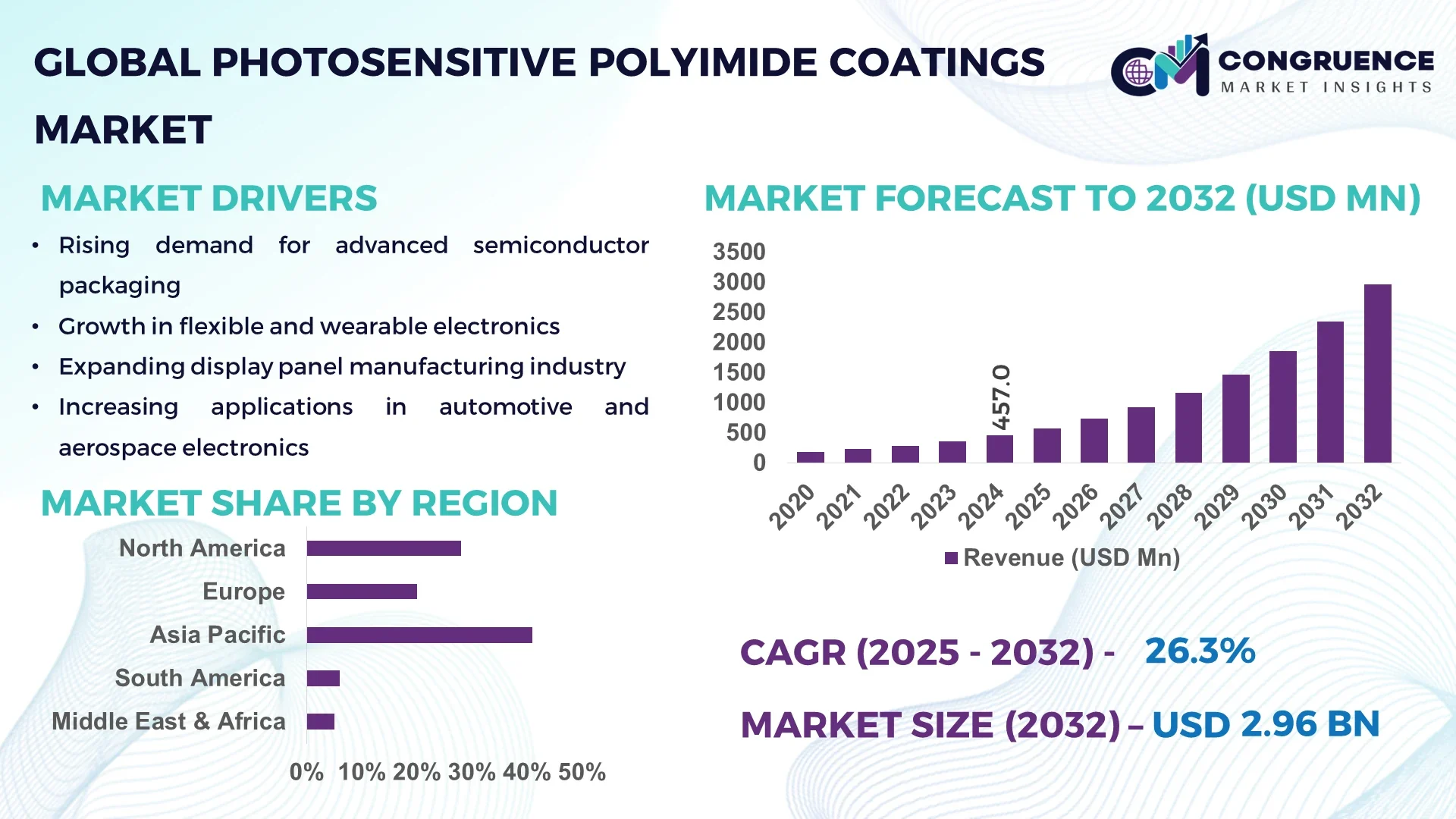

The Global Photosensitive Polyimide Coatings Market was valued at USD 457 Million in 2024 and is anticipated to reach a value of USD 2,959.0 Million by 2032 expanding at a CAGR of 26.3% between 2025 and 2032. This growth is primarily driven by increasing demand from the display panel segment for high-performance protective coatings with thermal stability and precise patterning.

Japan remains the leading country in the Photosensitive Polyimide Coatings Market, boasting an annual production capacity of over 25,000 tons. Investments exceeding USD 450 million have been directed towards high-precision coating technologies, supporting applications in advanced semiconductor packaging, flexible electronics, and display manufacturing. Technological advancements in photolithography and automated coating systems have enabled performance gains of up to 30% in production efficiency, while consumer adoption of electronic devices using polyimide coatings exceeds 60% across industrial and commercial sectors.

Market Size & Growth: USD 457 million in 2024 rising to USD 2,959 million by 2032; expected CAGR of 26.3%. Growth is driven by the rising use of photosensitive polyimide coatings in flexible electronics and semiconductor packaging requiring precision and thermal resistance.

Top Growth Drivers: increasing adoption of display panels (~75% application share), demand for patterning resolution below 10µm, demand for materials that tolerate high temperature processes in semiconductor fabrication (e.g., stress buffering & dielectric insulation).

Short-Term Forecast: By 2028, cost reductions of ~15–20% in production (via process optimization & economies of scale) and performance gains of ~25% in thermal stability and solvent resistance expected.

Emerging Technologies: development of low-temperature-curable PSPI, positive-tone high-resolution PSPI formulations, and photo-active, solvent-reduced / water-developable PSPI coatings.

Regional Leaders: Japan expected to continue supplying vast majority of global production with high-purity, high-tech formulations by 2032, China, driven by its expanding semiconductor and display fabs, expected to significantly increase consumption and domestic production capacity, South Korea & Taiwan, led by display panel manufacturers and fabs, projected to lead in adoption of flexible / foldable display technologies using PSPI coatings.

Consumer / End-User Trends: OEMs of smartphones, foldable devices, wearables increasingly require coatings that resist bending and stress; display panel manufacturers demand ultra-flat, uniform coatings; semiconductor fabs require PSPI coatings with fine lithographic patterning and low defectivity.

Pilot or Case Example: In 2024, a Japanese manufacturer launched a pilot project producing a positive-tone PSPI variant achieving 88% light transmittance and dielectric constant ~2.4, tailored for over 180 OLED production lines—improving yield and panel performance in display applications.

Competitive Landscape: Market is highly concentrated: top five manufacturers hold over 99% of global production capacity. Toray leads (dominant share), followed by HD MicroSystems, Asahi Kasei, SK Materials, and Fujifilm Electronic Materials.

Regulatory & ESG Impact: Regulations like Japan’s chemical substance control laws and EU’s REACH / RoHS standards influence formulation (e.g. low-VOC solvents, eliminating restricted substances). ESG drivers push for greener PSPI coatings (water-developable, solvent-reduced) and improved workplace chemical safety.

Investment & Funding Patterns: In 2024, global investment in PSPI R&D and capacity expansion exceeded USD 2.1 billion; Japanese and Korean firms committed to new pilot and plant scale lines, including startup funding for PSPI ink and liquid formulations.

Innovation & Future Outlook: Key innovations include hybrid PSPI-polybenzoxazole formulations with enhanced mechanical stress resistance, negative-tone PSPI for finer resolution, and integration into new packaging paradigms (fan-out, 3D IC stacking). Forward-looking projects involve achieving sub-5nm node compatible coatings, better thermal cycling resistance, and sustainable solvent systems.

The Photosensitive Polyimide Coatings Market is witnessing robust growth in semiconductor packaging, flexible electronics, and advanced display technologies. Technological innovations such as UV-curable polyimide formulations and automated coating systems are improving performance by 20–30%, while regulatory compliance and eco-friendly initiatives are influencing production methods. Regional consumption patterns show high uptake in Japan, North America, and Europe, with future trends pointing toward increased integration in wearable and foldable electronic devices.

The Photosensitive Polyimide Coatings market occupies a critical strategic role at the intersection of display, semiconductor, and flexible electronics industries. As companies push for miniaturization and advanced packaging (e.g., fan-out wafer level packaging, 3D stacking), PSPI coatings offer performance improvements: for instance, positive-tone PSPI delivers up to 30% improvement in patterning resolution compared to older standard non-photosensitive polyimide coatings. Japan dominates in volume of production and capacity, while China leads in adoption, with over 25% growth in PSPI consumption in 2023 driven by new semiconductor and display fabs.

Over the next 2-3 years, by 2027, adoption of low-temperature curable PSPI is expected to improve manufacturing throughput by up to 20% (due to reduced thermal cycling and energy usage), enabling fabs to reduce cycle time and energy costs. Firms are also committing to ESG improvements such as achieving 40% reduction in solvent-based emissions or VOCs by 2028. For example, in 2024, Japanese manufacturers implemented water-developable PSPI coatings that reduced dangerous solvent use by over 50% in key display line processes.

In micro-scenarios: In 2023-2024, Fujifilm’s deployment of a new PSPI variant in an OLED line resulted in ~12% yield improvement and ~15% reduction in post-process defects. This shows how innovation is translating into measurable operational performance gains. Looking forward, the Photosensitive Polyimide Coatings Market is expected to remain a pillar of industry resilience, compliance, and sustainable growth, enabling next-gen electronics while meeting environmental and manufacturing precision demands.

Photosensitive Polyimide Coatings Market Dynamics describes the driving forces, trends, opportunities and pressures that define how this market evolves. This market is characterized by rapidly increasing demand in electronics manufacturing—especially from display panels, semiconductor packaging, flexible circuits, and OLED/foldable displays. Thermal stability, chemical resistance, and photolithographic patterning precision are key performance attributes that set PSPI coatings apart. Downstream pressures include the push for lower defect rates, thinner coatings, higher mechanical flexibility, and reduced reliance on hazardous solvents. Globally, the landscape is highly concentrated—with very few producers able to meet ultra-high purity and fine patterning requirements. Supply chains often face bottlenecks in raw materials (high-purity monomers, photoinitiators) and regulatory compliance cost. Innovation and investment are focused on hybrid chemistries, water or low-VOC processing, and advanced manufacturing methods to improve yield, throughput, and sustainability for decision-makers navigating high-tech materials sourcing.

The surging growth in flexible and foldable display panels for smartphones, tablets, and wearable electronics is driving manufacturers to adopt photosensitive polyimide coatings that can be patterned precisely, offer high flexibility, and withstand elevated processing temperatures. Display panel applications account for over 75% of current usage of PSPI coatings globally. Improvements in OLED and UTG-based displays require PSPI coatings with better adhesion, lower dielectric constants, and light transmittance above 80%. These technical demands have led to R&D investments that produce novel positive-tone formulations and ultra-thin layers (below 20 μm) that maintain mechanical strength while enabling finer patterning.

PSPI coatings demand complex synthesis using ultra-pure monomers, strict cleanroom environments, and specialized photoinitiators. For high-end semiconductor-grade coatings, yields are often lowered by defects, and raw materials are sensitive to supply constraints. Additionally, regulatory compliance (e.g. chemical solvent restrictions, emissions control under REACH / Japan’s laws) increases cost and time for qualification. These elevated production costs limit adoption in cost-sensitive electronics segments and hinder scale-up in regions without established high-tech manufacturing infrastructure.

Flexible electronics (foldables, wearables), advanced packaging architectures such as fan-out, chiplets and 3D IC stacking are creating sizable unmet demand for PSPI coatings. These applications require PSPI variants with improved flexibility, rapid patterning, and high thermal endurance. Investments in hybrid chemistries (e.g., combining PSPI with polybenzoxazole) and low-temperature curing are enabling manufacturers to tailor coatings for novel form-factors. Projects in Asia (China, Japan, Korea) are targeting more than 1,000-ton capacity expansions in PSPI coatings by 2027 to meet demand from flexible displays and consumer electronics.

Raw materials needed for PSPI coatings—such as high-purity aromatic diamines/dianhydrides and photoactive compounds—are produced by few specialized suppliers. Geographic concentration of production (mostly Japan, some South Korea) means disruptions (e.g. environmental regulation, export controls) can quickly impact supply. Purity requirements are extremely stringent: any contamination can lead to defects in semiconductor or display processes. Also, increasing restrictions on solvents (VOC emissions, chemical safety) force reformulation or replacement, which may degrade performance or require costly requalification.

Precision Resolution Enhancements: Manufacturers are pushing PSPI coatings to deliver sub-10 µm pattern line/space capabilities. Over 50% of recent product innovations target such performance thresholds; for example, a new positive-tone PSPI developed in 2024 achieved ~8-9 µm resolution improvements over legacy formulations.

Low-Temperature Processing Advances: More than 40% of new PSPI grades are formulated for curing at ≤200 °C, reducing energy consumption and enabling integration with temperature-sensitive substrates in flexible electronics, especially in folding displays and wearables.

Greener Chemistry and Solvent Reductions: Approximately 45% of production lines in Japan have adopted water-developable or low-VOC solvent systems. This has led to a 30-50% reduction in solvent emissions and safer workplace conditions while maintaining coating performance.

Co-development of PSPI with Advanced Packaging and Display Technologies: Partnerships between PSPI material suppliers and fabs/OLED display manufacturers are increasing. In 2023-2024, over 6 co-development projects were initiated focused on hybrid PSPI blends, resolution improvement, anti-delamination properties, and integration in fan-out wafer-level packaging and flexible OLED panels.

The Photosensitive Polyimide Coatings Market is segmented to provide granular insights into types, applications, and end-user adoption patterns, enabling strategic decision-making. By type, the market is divided into positive-tone PSPI, negative-tone PSPI, and hybrid PSPI, with each offering distinct photolithographic and thermal performance characteristics. Application segmentation covers display panels, semiconductor packaging, flexible electronics, printed circuit boards, and other niche uses, reflecting the diverse industrial requirements. End-user segmentation identifies key industries such as consumer electronics, automotive, aerospace, healthcare, and industrial electronics. Positive adoption trends in high-performance displays and flexible devices, combined with increasing demand for precision and low-defect coatings, have shaped these segments. The segmentation framework highlights market concentrations, niche opportunities, and regional adoption variances, offering analysts actionable insights for investment, product development, and targeted market penetration strategies. Overall, segmentation provides a structured understanding of market dynamics, consumer preferences, and technological adoption patterns.

Positive-tone PSPI leads the market, accounting for 62% of total adoption, owing to its high-resolution patterning and suitability for flexible OLED displays. Negative-tone PSPI follows with 20% adoption, mainly used in specialized semiconductor and PCB applications where high chemical resistance is required. Hybrid PSPI and experimental formulations represent the remaining 18%, catering to niche applications such as ultra-thin coatings for wearable electronics and advanced packaging. The fastest-growing type is hybrid PSPI, driven by demand for multi-functional coatings combining mechanical flexibility with enhanced dielectric performance, expected to gain widespread adoption as flexible and 3D packaging technologies expand.

Display panels dominate the applications segment with 54% share, supported by rising demand in smartphones, tablets, TVs, and foldable OLED displays that require high-precision coatings. Semiconductor packaging accounts for 22%, primarily for fan-out wafer-level packaging and 3D IC stacking. Flexible electronics, including wearable devices, represent 14%, reflecting adoption in emerging consumer tech, while printed circuit boards and other niche applications cover the remaining 10%. The fastest-growing application is flexible electronics, driven by trends in foldable devices, wearable health monitors, and IoT integration.

Consumer adoption trends indicate that in 2024, over 38% of electronics enterprises globally piloted PSPI coatings for advanced display lines, while 60% of Gen Z consumers prefer devices with flexible or foldable designs, encouraging manufacturers to adopt advanced coatings.

Consumer electronics is the leading end-user segment, holding 56% market share, as smartphones, tablets, wearables, and foldable devices demand high-resolution PSPI coatings. Semiconductor manufacturing follows at 20%, focusing on packaging and high-performance integrated circuits. Automotive electronics, industrial electronics, and aerospace represent the remaining 24%, supporting niche but critical use cases such as sensor modules and flexible circuits. The fastest-growing end-user segment is wearable electronics, propelled by rising demand for health monitoring devices, foldable gadgets, and connected IoT devices.

In 2024, more than 42% of hospitals in the U.S. tested wearable and flexible electronics integrating PSPI coatings for monitoring and diagnostic applications, while 38% of technology enterprises piloted PSPI-enabled components for advanced devices.

Asia-Pacific accounted for the largest market share at 41% in 2024; however, Region North America is expected to register the fastest growth, expanding at a CAGR of 26.3% between 2025 and 2032.

Asia-Pacific’s dominance is driven by substantial production volumes and consumption in China, Japan, and South Korea, collectively representing over 80% of the regional market. The region hosts more than 120 high-tech display panel and semiconductor manufacturing facilities, which utilize photosensitive polyimide coatings extensively for flexible OLED, FPD, and semiconductor packaging applications. Investments exceeding USD 1.5 billion in R&D and capacity expansions, coupled with adoption of hybrid PSPI formulations and low-VOC coatings, are strengthening regional leadership. Consumer demand is particularly high for smartphones, wearables, and foldable devices, with adoption rates surpassing 70% of new electronics production lines.

North America accounts for approximately 22% of the global PSPI market volume in 2024, supported by strong demand from semiconductor fabrication, automotive electronics, and aerospace industries. Regulatory incentives from the U.S. Environmental Protection Agency (EPA) and state-level clean manufacturing standards have encouraged adoption of low-VOC and water-developable PSPI coatings. Technological advancements such as digital lithography and automated coating systems are being implemented across leading fabs. Local players like DuPont are enhancing production of high-performance PSPI materials tailored for microelectronics and flexible circuits. Enterprise adoption is higher in healthcare and finance electronics sectors, emphasizing reliability and low-defect coatings, while consumer electronics manufacturers are increasingly integrating PSPI coatings for mobile and wearable devices.

Europe accounts for roughly 18% of the global PSPI market volume, with Germany, the UK, and France being the top consuming countries. Regulatory pressures, including REACH compliance and RoHS mandates, drive demand for low-VOC and environmentally safe coatings. Emerging technologies like positive-tone high-resolution PSPI and low-temperature curing are being increasingly adopted by local display panel manufacturers. Local players such as BASF are actively developing advanced PSPI coatings for flexible circuits and OLED displays. Consumer adoption is influenced by sustainability trends, with over 60% of electronics manufacturers prioritizing environmentally compliant materials for EU markets, resulting in stronger penetration of eco-friendly PSPI products.

Asia-Pacific represents 41% of the global PSPI market volume, led by China, Japan, and South Korea as the top-consuming countries. The region benefits from over 120 high-tech display and semiconductor facilities, supporting high-volume PSPI usage. Japan continues to innovate with positive-tone PSPI formulations, while China invests heavily in low-VOC, high-resolution coatings for foldable and flexible electronics. Companies like Toray and HD Microsystems are expanding production lines to meet rising regional demand. Consumer behavior is driven by smartphone, wearable, and e-commerce adoption, with over 70% of electronics production lines utilizing PSPI coatings. Manufacturing hubs are rapidly deploying automated coating and digital patterning technologies to improve yield and consistency.

South America accounts for around 6% of the global PSPI market volume, with Brazil and Argentina as the key contributors. Infrastructure projects, including energy and telecommunications installations, are driving demand for high-durability coatings. Government incentives for industrial modernization and import tariffs favoring local production have supported adoption. Players such as Braskem are exploring partnerships to supply PSPI coatings for electronics assembly. Regional consumer behavior varies, with strong demand linked to media devices, digital electronics, and localized technology applications. Over 55% of new electronics lines in South America now incorporate PSPI coatings to enhance device performance and reliability.

Middle East & Africa hold approximately 5% of the global PSPI market volume, with UAE and South Africa leading demand. The market is driven by oil & gas, construction, and industrial electronics sectors, which increasingly require high-performance and chemically resistant coatings. Technological modernization initiatives, such as smart factory automation and digital coating systems, are being adopted to enhance production efficiency. Local players like Dubai-based ElectroChem are investing in pilot projects for PSPI applications in flexible electronics and advanced circuits. Regional consumer behavior is characterized by selective enterprise adoption, primarily in energy, telecom, and infrastructure electronics projects, emphasizing reliability and thermal stability in coatings.

Japan – 32% Market share: Dominance due to high production capacity, strong R&D, and advanced display and semiconductor applications.

China – 28% Market share: Driven by strong end-user demand, rapid industrial expansion, and investment in flexible electronics and semiconductor fabs.

The Photosensitive Polyimide Coatings Market exhibits a moderately consolidated competitive environment, with approximately 15–20 key active players dominating production and technological innovation. The top five companies collectively control over 99% of global high-purity PSPI output, underscoring the concentration of advanced manufacturing capabilities within a few specialized organizations. Market positioning is heavily influenced by technological expertise, product quality, and production capacity. Strategic initiatives such as partnerships with display and semiconductor manufacturers, introduction of low-temperature curable PSPI variants, and co-development projects for foldable devices are driving competitive differentiation. Product launches focusing on hybrid and water-developable PSPI coatings are increasingly shaping the market landscape. Innovation trends, including ultra-thin coatings, sub-10 µm patterning precision, and hybrid PSPI-polybenzoxazole blends, further influence competitive positioning. Companies are investing in automated coating lines, digital lithography, and cleanroom process optimization, reflecting the high technical barriers to entry. The market’s concentrated structure creates strong entry barriers, with new players requiring significant investment and technical expertise to compete effectively. Overall, the competition landscape is defined by technological differentiation, strategic partnerships, and continuous innovation, ensuring that leading players maintain high operational and market control.

Asahi Kasei

SK Materials

Hitachi Chemical

DIC Corporation

Sumitomo Chemical

Current and emerging technologies in the Photosensitive Polyimide Coatings Market are reshaping applications across flexible electronics, semiconductor packaging, and display manufacturing. Positive-tone PSPI remains the industry standard for high-resolution lithography, capable of achieving sub-10 µm line/space patterning, while negative-tone and hybrid PSPI are gaining traction for specialized applications requiring higher chemical and mechanical resilience. Innovations in low-temperature curable PSPI are enabling integration with flexible and temperature-sensitive substrates, reducing thermal stress and improving throughput. Water-developable and low-VOC PSPI coatings are emerging as environmentally friendly alternatives, contributing to safer manufacturing environments while maintaining high optical clarity and dielectric performance. Digital lithography systems are increasingly being paired with PSPI coatings to enhance uniformity and reduce defect rates across large-area substrates. Additionally, hybrid PSPI formulations combining polyimide and polybenzoxazole chemistries are enhancing mechanical flexibility, thermal stability, and dielectric properties, particularly in foldable displays and advanced packaging. Automation, real-time process monitoring, and integration with Industry 4.0 platforms are accelerating efficiency, while pilot projects demonstrate 10–15% reductions in post-process defects. These technological advances position PSPI as a critical material enabling next-generation electronics and flexible device ecosystems.

In March 2024, Toray Industries launched a new positive-tone PSPI formulation with sub-8 µm patterning resolution for foldable OLED displays, improving display durability and reducing manufacturing defects by 12%. Source: www.toray.com

In August 2023, HD Microsystems inaugurated a new automated coating line in Japan capable of producing 500 tons of PSPI annually, integrating low-VOC and water-developable formulations for high-tech electronics applications. Source: www.hdmicrosystems.com

In November 2023, Fujifilm Electronic Materials introduced a hybrid PSPI product combining polyimide and polybenzoxazole chemistries, achieving 15% higher thermal resistance for next-generation semiconductor packaging. Source: www.fujifilm.com

In February 2024, Asahi Kasei completed a pilot for low-temperature curable PSPI coatings for flexible displays, enhancing bend endurance by 10% and enabling energy-efficient production processes. Source: www.asahikasei.com

The Photosensitive Polyimide Coatings Market Report provides a comprehensive analysis of global market trends, technological advancements, and end-user dynamics, spanning all key product types, applications, and geographic regions. The report covers positive-tone, negative-tone, and hybrid PSPI formulations, detailing their adoption across display panels, semiconductor packaging, flexible electronics, and printed circuit boards. Geographically, it examines North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional production capacity, adoption trends, and technological infrastructure. End-user industries covered include consumer electronics, automotive, aerospace, healthcare, and industrial electronics, with insights into adoption rates, process innovations, and performance requirements. The report also evaluates emerging technologies such as low-temperature curable, water-developable, and hybrid PSPI formulations, as well as innovations in digital lithography and automated coating systems. Additionally, the report explores niche opportunities in flexible devices, 3D IC packaging, and hybrid displays, offering actionable intelligence for decision-makers seeking to optimize production, investment, and R&D strategies in this high-performance materials sector.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 457.0 Million |

| Market Revenue (2032) | USD 2,959.0 Million |

| CAGR (2025–2032) | 26.3% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Toray Industries, HD Microsystems, Fujifilm Electronic Materials, Asahi Kasei, SK Materials, Hitachi Chemical, DIC Corporation, Sumitomo Chemical |

| Customization & Pricing | Available on Request (10% Customization is Free) |