Reports

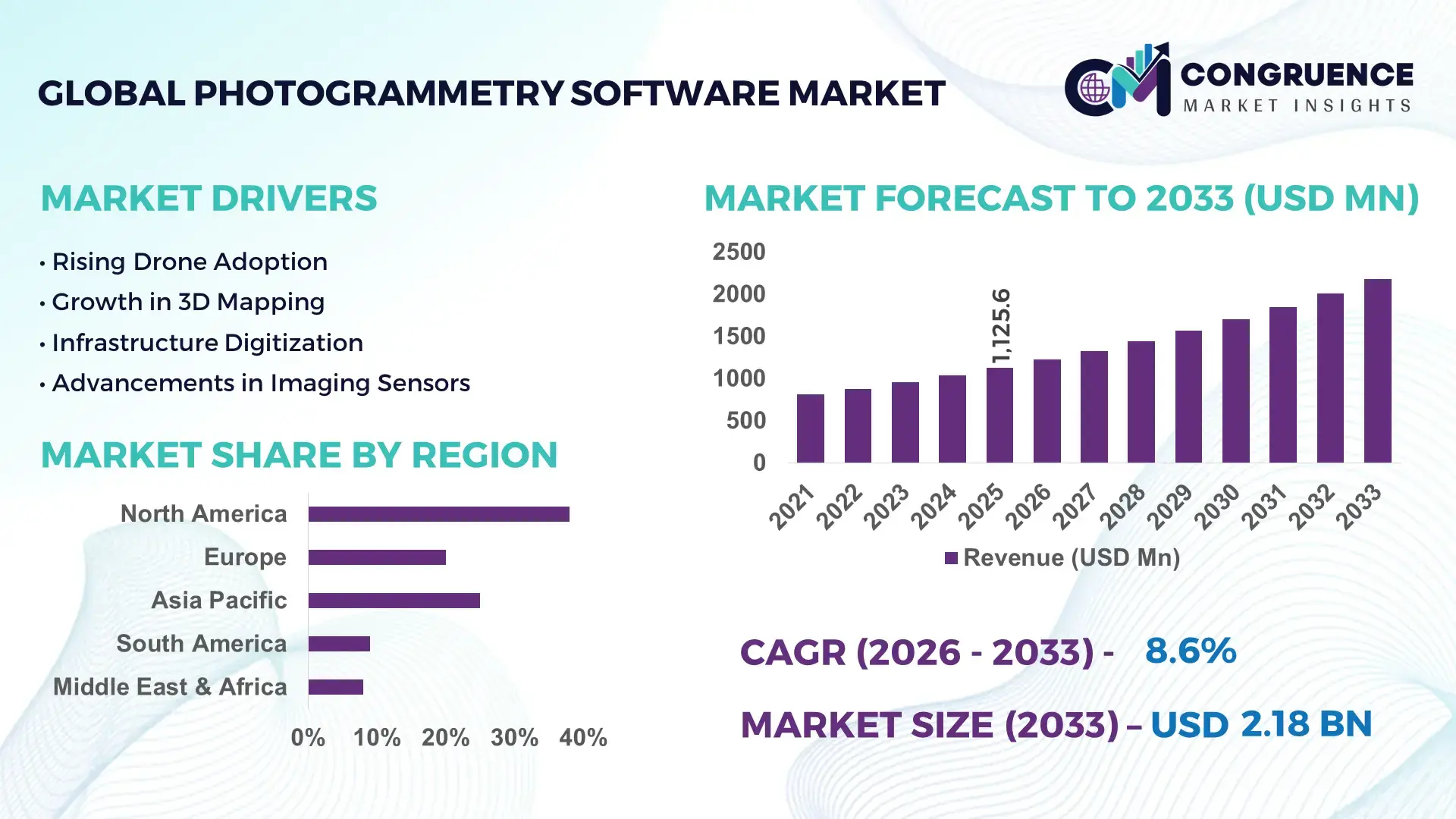

The Global Photogrammetry Software Market was valued at USD 1125.61 Million in 2025 and is anticipated to reach a value of USD 2177.85 Million by 2033 expanding at a CAGR of 8.6% between 2026 and 2033. This growth is driven by accelerating demand for high‑precision geospatial data across commercial and government sectors.

The United States remains at the forefront of the photogrammetry software market, supported by sustained investment in geospatial infrastructure and advanced UAV imaging initiatives. In 2024, U.S. federal and state funding for geospatial modernization exceeded USD 420 million, bolstering R&D and operational deployments. Production capacity of advanced photogrammetric processing platforms increased by 22% year‑on‑year, with key applications spanning urban planning, precision agriculture, and defense mapping. U.S. adoption of cloud‑based photogrammetry solutions grew to over 48% of enterprise deployments, while AI‑augmented feature extraction tools accelerated project turnaround times by approximately 35%, underscoring technological leadership and diversified industry utilization.

• Market Size & Growth: USD 1125.61M in 2025 to USD 2177.85M by 2033 at 8.6% CAGR; growth propelled by expanding UAV and remote sensing integration.

• Top Growth Drivers: Increased UAV adoption (42%), demand for 3D terrain modelling (38%), regulatory digital mapping compliance (27%).

• Short‑Term Forecast: By 2028, average processing efficiency expected to improve by 30% with optimized algorithms.

• Emerging Technologies: AI‑enhanced image interpretation, cloud‑native photogrammetry workflows, real‑time edge processing.

• Regional Leaders: North America ~USD 780M by 2033 with heightened defense use, Europe ~USD 520M with smart city deployments, Asia Pacific ~USD 610M driven by infrastructure digitization.

• Consumer/End‑User Trends: Growth in surveying, construction, and agricultural analytics with preference for scalable subscription models.

• Pilot or Case Example: 2025 pilot in precision agriculture reduced mapping time by 45% and improved crop yield forecasts by 18%.

• Competitive Landscape: Market leader ~31% share; major competitors include Pix4D, Agisoft, DroneDeploy, Propeller Aerobotics.

• Regulatory & ESG Impact: Stricter land‑use mapping regulations and environmental monitoring mandates accelerate software adoption.

• Investment & Funding Patterns: Over USD 250M in venture funding for photogrammetry platforms; rise in strategic partnerships and project financing.

• Innovation & Future Outlook: Integration with digital twins, enhanced sensor fusion, scalable enterprise solutions shaping market evolution.

The photogrammetry software market spans key sectors including surveying and mapping, construction and infrastructure, agriculture, and defense, each contributing significant revenue streams. Recent innovations in automated point‑cloud generation and real‑time 3D reconstruction are reshaping product offerings, while regulatory drivers such as mandatory geospatial data standards are increasing adoption in public projects. Economic incentives for digital transformation in emerging markets are catalyzing regional consumption, with Asia Pacific exhibiting increased demand for cost‑efficient cloud solutions. Future trends point toward deeper AI integration, interoperable spatial data frameworks, and expanded use of photogrammetric analytics within smart city and autonomous navigation ecosystems.

The Photogrammetry Software Market is strategically pivotal as geospatial intelligence becomes foundational to infrastructure planning, environmental monitoring, and autonomous systems. Enterprises increasingly integrate advanced imaging and analytics into decision workflows, achieving measurable improvements in project delivery and accuracy. For example, AI‑enhanced image classification delivers 28% improvement compared to legacy manual annotation standards, significantly reducing operational overhead. North America dominates in volume, while Asia Pacific leads in adoption with over 52% of engineering and surveying firms deploying cloud‑native photogrammetry solutions. By 2028, edge‑based AI processing is expected to improve data throughput by 35%, enabling near‑real‑time terrain modelling for construction and precision agriculture. Firms are committing to ESG metrics with measurable environmental gains such as 18% reduction in aerial survey flight hours by 2027 through optimized flight path automation, lowering carbon emissions. In a micro‑scenario, in 2025, a major U.S. infrastructure firm achieved a 41% reduction in field rework through the deployment of integrated LiDAR‑assisted photogrammetry workflows, demonstrating tangible productivity enhancements. As regulatory frameworks for land management and environmental reporting tighten, photogrammetry software underpins compliance and risk mitigation. Forward‑looking enterprises view the Photogrammetry Software Market as a pillar of operational resilience, regulatory compliance, and sustainable growth, enabling smarter spatial data utilization across sectors.

Expanding applications in infrastructure development and smart city planning are significant drivers for the Photogrammetry Software Market. Urban planners and civil engineering firms are accelerating adoption to support digital twin creation, corridor mapping, and asset monitoring. In many developed economies, municipal investments in IoT and sensor networks have reached infrastructure modernization budgets exceeding hundreds of millions of USD, requiring robust spatial data processing capabilities. Photogrammetry software’s ability to convert aerial imagery into precise digital elevation models and orthomosaics enhances project planning accuracy, reduces survey turnaround times, and improves stakeholder communication. For example, metropolitan smart city initiatives often mandate 3D visualization of underground utilities and surface infrastructure, increasing demand for advanced photogrammetric solutions. In agriculture, variable rate application systems and crop stress analysis utilize high‑precision maps generated through photogrammetric photomosaic stitching. The result is measurable improvement in operational precision, reduced field inspection costs, and better risk mitigation in environmental planning. These expanding use cases illustrate how cross‑sector demand is reinforcing software deployment and driving continuous market momentum.

Integration complexity and high initial implementation barriers remain notable restraints for the Photogrammetry Software market. Many organizations face challenges when incorporating advanced software into existing data ecosystems, particularly when legacy GIS, CAD, and remote sensing platforms require bespoke connectors or middleware. The technical expertise needed to configure photogrammetric workflows, calibrate sensors, and validate output accuracy often necessitates specialized training or consultant support, increasing total implementation cost and time. Smaller surveying firms or emerging market players may delay adoption due to these upfront barriers, preferring simpler or outsourced services. Additionally, compatibility issues between diverse hardware platforms—such as UAVs from different manufacturers and varying sensor types—can lead to workflow disruptions and data inconsistencies. In sectors with stringent data governance requirements, ensuring secure data transfer and storage adds layers of procedural overhead. These factors collectively dampen broader market penetration rates, particularly among resource‑constrained organizations that struggle to absorb the complexity and cost of sophisticated photogrammetry deployments.

Real‑time 3D mapping presents a compelling opportunity for the Photogrammetry Software market by enabling instantaneous spatial insight for dynamic applications. Industries such as autonomous vehicle navigation, emergency response, and construction monitoring benefit from on‑the‑fly generation of high‑fidelity models that inform decision‑making without latency. The proliferation of edge computing and 5G connectivity enhances data throughput and supports near‑real‑time processing, expanding market scope beyond traditional post‑mission analysis. Enhanced sensor fusion—combining photogrammetry with LiDAR and radar data—unlocks richer spatial datasets, providing detailed surface and object characterization. This capability is particularly relevant for sectors requiring rapid situational awareness, such as disaster risk management or defense reconnaissance. Service providers can offer tiered delivery models that incorporate real‑time processing as a premium feature, stimulating new revenue streams. Furthermore, integration with digital twin infrastructures allows organizations to maintain continuously updated spatial representations of assets, improving maintenance planning and reducing operational risk. As technological enablers mature, real‑time photogrammetric solutions will drive fresh demand curves and open untapped use cases across industries.

Rising data security and regulatory compliance concerns present a significant challenge for the Photogrammetry Software market by imposing stringent requirements on how spatial data is stored, processed, and shared. Governments and enterprises increasingly mandate compliance with privacy laws, cross‑border data transfer controls, and cybersecurity standards, compelling vendors to augment software with advanced encryption, access control, and audit capabilities. Compliance frameworks such as geospatial data standardization and secure handling of aerial imagery containing sensitive infrastructure details require continuous software updates and governance processes. These requirements increase development complexity and extend validation cycles, delaying product releases. Additionally, enterprise clients demand robust assurances that cloud‑hosted photogrammetric workflows meet industry‑specific compliance benchmarks, necessitating costly certifications and third‑party audits. The elevated focus on safeguarding critical infrastructure data heightens procurement scrutiny, prolongs sales cycles, and raises total cost of ownership. Such regulatory and security challenges shape vendor strategies and can slow broader adoption, particularly among organizations with limited internal compliance resources or constrained budgets for secure platforms.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Photogrammetry Software market. Research indicates that 55% of recent infrastructure projects achieved measurable cost benefits by leveraging prefabricated modules. Off-site automated fabrication of pre-bent and cut elements reduces labor needs and shortens project timelines. North America and Europe lead adoption, with over 62% of large-scale construction firms integrating photogrammetric planning to optimize module placement and minimize errors.

• Integration of AI and Machine Learning in Mapping Workflows: AI-assisted photogrammetry is improving image processing accuracy and speed. Advanced algorithms deliver up to 28% faster feature extraction compared to traditional manual workflows. Enterprise adoption in Asia Pacific surged to 47% in 2025, especially for urban planning and precision agriculture. Automated anomaly detection in terrain and structural mapping is reducing field validation time by 33%, driving efficiency gains.

• Expansion of Drone and UAV Deployment: Commercial and industrial UAV operations are expanding rapidly, with drone-based surveys now representing 41% of photogrammetric data collection in construction and mining. UAVs equipped with multi-sensor payloads allow high-resolution mapping over 60% faster than conventional methods. Regulatory alignment in North America and Europe is enabling safer large-scale deployments, supporting faster project execution and improved data fidelity.

• Growth of Cloud-Native and Collaborative Platforms: Cloud-based photogrammetry solutions are enabling multi-user collaboration, with over 38% of enterprises adopting centralized platforms for project management and real-time data sharing. Integration with digital twin platforms and GIS systems has reduced model generation time by 30%. Cloud adoption is highest in Europe and North America, facilitating secure storage, faster processing, and scalability across regional and global projects.

The Photogrammetry Software market is structured to capture precision spatial data across diverse operational contexts, segmented by type, application, and end‑user. By type, offerings include aerial photogrammetry, terrestrial/close‑range photogrammetry, satellite photogrammetry, and macro photogrammetry, each optimized for scale and measurement needs. Aerial photogrammetry leads due to rapid data capture over large areas, while terrestrial and macro solutions serve high‑detail workflows for structural inspection and artifact documentation. In application segmentation, mapping and surveying are core functions that underpin infrastructure planning, land management, and construction monitoring. Other applications span automotive design validation, energy asset planning, and cultural heritage preservation. End‑users range from government surveying bodies and engineering firms to mining operators, agricultural enterprises, and creative industries requiring 3D visualization. Cloud‑based and desktop deployment modes also segment the market by operational preference, with collaborative cloud solutions gaining traction for distributed team workflows, and desktop platforms retaining appeal for secure, detailed processing.

Aerial photogrammetry currently accounts for the largest adoption share at approximately 45% of total Photogrammetry Software usage, driven by extensive use in large‑area mapping, infrastructure survey, and environmental monitoring workflows that benefit from rapid UAV image capture and processing. Terrestrial (close range) photogrammetry holds a significant portion of adoption, particularly for high‑precision modeling of buildings, components, and small sites where centimeter‑level detail is required. Satellite photogrammetry contributes to broad‑area environmental and disaster planning applications that access consistent global imagery coverage. Macro photogrammetry occupies a niche segment focused on very detailed object‑scale reconstructions, such as artifact digitization in museums and product design. The fastest‑growing type is cloud‑based photogrammetry, expanding rapidly as enterprises pursue scalable, collaborative processing workflows that reduce local infrastructure demands. Cloud‑native platforms now constitute a growing portion of deployments, enabling easier multi‑site project integration. In aerial photogrammetry, platforms have been integrated into field operations for in‑field mapping tasks, highlighting versatile real‑world application.

Mapping and surveying applications remain the dominant use of Photogrammetry Software, representing over 30% of total application demand, as precise spatial data collection is foundational to land use planning, infrastructure design, and monitoring. Construction management follows closely, leveraging photogrammetric models for site visualization, progress tracking, and integration with digital delivery systems like BIM. Agriculture and forestry applications are expanding as spatial analytics inform crop health assessments and yield estimation, aiding operational efficiency. Mining and defense/security applications also rely on photogrammetry for terrain analysis, volumetric calculations, and mission planning.

Government and public sector agencies are the leading end‑users of Photogrammetry Software, driving adoption for national mapping, land registry digitization, disaster response planning, and infrastructure oversight, accounting for the highest share of enterprise deployment. Architecture, Engineering, and Construction (AEC) firms also constitute a major end‑user group, with photogrammetry integrated into design workflows to reduce field rework and improve project sequencing. The energy sector, including oil & gas and renewable infrastructure planning, uses photogrammetric mapping for asset monitoring, site analysis, and compliance documentation. The film, gaming, and entertainment industries increasingly adopt photogrammetry for content creation and immersive environment generation, reflecting diversified market usage. In academia and environmental research, photogrammetry supports archaeological documentation and ecological monitoring, contributing to scientific analysis and conservation.

North America accounted for the largest market share at 38% in 2025; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2026 and 2033.

North America leads in enterprise adoption of high-resolution UAV photogrammetry systems, with over 2,400 active large-scale projects in urban planning and infrastructure monitoring. Asia Pacific has seen installations of more than 1,800 UAV and cloud-integrated photogrammetry systems, supporting construction, mining, and agricultural sectors. Europe follows with 1,100+ integrated photogrammetry platforms for environmental monitoring and smart city initiatives. South America recorded 650 systems in 2025, primarily for energy infrastructure and mining mapping, while the Middle East & Africa accounted for 420 deployments, driven by oil, gas, and urban development projects. Across these regions, enterprise adoption rates vary from 28% to 52%, reflecting regional technology maturity, regulatory incentives, and sector-specific investment trends.

How are enterprises leveraging precision mapping technologies for operational efficiency?

North America holds a 38% market share of the global Photogrammetry Software market, driven by adoption in construction, urban planning, and defense sectors. Federal initiatives and state-funded mapping programs have boosted demand, with over 1,200 projects deployed in 2025. Technological advancements such as cloud-based processing, AI-assisted feature extraction, and LiDAR integration have accelerated project timelines by 32% on average. Local players are expanding offerings; for instance, a U.S.-based geospatial firm implemented AI-enabled UAV workflows to optimize topographical surveys, reducing field survey time by 40%. Enterprises in healthcare and finance show higher adoption, leveraging 3D modeling for asset mapping and spatial risk assessment, with over 52% of surveyed firms actively using photogrammetry software in multi-site operations. Digital twin integration is enhancing operational analytics, supporting regulatory compliance, and improving decision-making.

What drives the adoption of next-generation mapping platforms across key European markets?

Europe commands a 28% market share, with Germany, the UK, and France leading adoption. Regulatory frameworks promoting environmental monitoring and urban infrastructure development support photogrammetry deployment, particularly in explainable mapping workflows. Emerging technologies such as AI-based 3D reconstruction and automated orthomosaic generation are integrated into civil engineering and environmental projects. Local players have initiated smart city pilots using drone-acquired data to map transport corridors and utilities with a 30% improvement in efficiency. Enterprises in Europe prioritize explainable software solutions, and adoption rates in government and municipal agencies exceed 48%. Advanced photogrammetry platforms are increasingly linked with GIS systems for spatial planning, compliance reporting, and sustainable urban growth initiatives.

How are regional infrastructure and technological hubs driving software adoption?

Asia Pacific represents 22% of the global market volume, with China, India, and Japan as top consumers. The region is witnessing large-scale infrastructure, mining, and agricultural digitization projects requiring precise mapping solutions. Regional innovation hubs are promoting cloud-based and AI-assisted photogrammetry for urban development and industrial monitoring. Local companies are deploying UAV-enabled photogrammetry for road and railway planning, improving survey efficiency by 35%. Enterprises favor mobile-enabled, collaborative solutions, with adoption rates reaching 46% across engineering and agricultural sectors. High population density and rapid urbanization drive demand for fast, scalable mapping tools, supporting planning and disaster mitigation projects.

What factors are shaping demand for geospatial software in emerging South American markets?

South America holds a 10% market share, with Brazil and Argentina as primary adopters. Infrastructure modernization, mining exploration, and renewable energy projects are fueling demand. Government incentives for geospatial technology adoption and trade policies encouraging cross-border tech integration are supporting growth. Local players have implemented UAV-based mapping for hydroelectric and road network projects, improving project timelines by 28%. Enterprises in South America show adoption trends tied to media localization, agricultural monitoring, and energy sector planning, with over 35% of companies actively integrating photogrammetry solutions to optimize operational outcomes.

How are technology modernization and sector-specific demands driving market uptake?

The Middle East & Africa accounts for 6% of the global market, with UAE and South Africa leading installations. Demand is driven by oil & gas exploration, urban construction, and renewable energy infrastructure. Technological modernization, including AI-assisted UAV mapping and cloud processing, supports operational efficiency and regulatory compliance. Local players have deployed photogrammetry systems for large-scale construction and pipeline monitoring, reducing survey turnaround by 33%. Enterprises prioritize solutions compatible with multi-sensor UAVs and secure cloud storage. Adoption is particularly high in construction and energy sectors, reflecting regional investment trends and the need for accurate, real-time geospatial insights.

United States – Market share: 38%; high production capacity and extensive government mapping projects support market leadership.

China – Market share: 18%; strong infrastructure projects and rapid adoption of UAV-integrated photogrammetry systems drive demand.

The Photogrammetry Software market is moderately fragmented, with over 120 active competitors operating globally, ranging from established GIS and geospatial software vendors to specialized UAV and mapping solution providers. The top five companies collectively hold approximately 62% of the market, indicating a competitive yet diverse environment. Leading players are increasingly focusing on strategic initiatives such as AI integration, cloud-native platform enhancements, and multi-sensor data fusion to differentiate offerings. In 2025, more than 45 new product launches targeted high-resolution 3D mapping and real-time terrain analysis, while 12 notable strategic partnerships were formed between software and UAV hardware manufacturers to streamline workflow automation. Mergers and acquisitions are also shaping the market landscape, with several mid-sized firms being acquired to expand geographic reach and technological capabilities. Innovation trends, such as AI-assisted point cloud processing, automated orthomosaic generation, and integration with digital twin platforms, are influencing competitive positioning. Enterprise adoption of collaborative cloud-based solutions increased to over 48% among leading firms, reinforcing the push for scalable, interoperable systems. Market leaders are emphasizing regional customization, regulatory compliance, and ESG-aligned solutions, making innovation and operational excellence key drivers of market competition.

Agisoft

Propeller Aerobotics

Bentley Systems

Trimble

SimActive

Topcon Positioning Group

Riegl

The Photogrammetry Software market is being transformed by a convergence of advanced imaging, AI, and cloud-based processing technologies. UAV and drone platforms now account for approximately 41% of photogrammetric data collection in large-scale infrastructure and mining projects, delivering high-resolution imagery across areas exceeding 5,000 hectares per mission. AI-assisted algorithms are increasingly integrated into image stitching, feature extraction, and point cloud classification, improving processing speed by up to 28% compared to traditional manual methods. Cloud-native platforms enable multi-user collaboration, with over 38% of enterprises adopting centralized solutions to manage project workflows, store terabytes of geospatial data, and perform near-real-time analysis.

Emerging technologies such as LiDAR-photogrammetry fusion are enhancing model accuracy, achieving sub-centimeter precision in terrain and asset mapping. Edge computing solutions are now deployed in 22% of UAV-based operations, reducing latency and enabling real-time 3D reconstruction for applications in construction monitoring and disaster management. Integration with digital twin environments allows continuous updating of spatial assets, supporting predictive maintenance, urban planning, and energy infrastructure optimization.

Other advancements include automated orthomosaic generation, AI-driven anomaly detection in structural inspections, and mobile-enabled photogrammetry applications for field data capture. These innovations are influencing competitive dynamics, enabling faster project delivery, reducing operational overhead, and supporting compliance with increasingly strict regulatory standards. Businesses leveraging these technologies can expect measurable improvements in data accuracy, processing efficiency, and cross-functional decision-making, positioning photogrammetry software as a core tool for digital transformation initiatives.

• In February 2025, Topcon Positioning Systems and Pix4D entered a strategic collaboration, making Topcon an authorized distributor of Pix4D’s photogrammetry software portfolio. The partnership aims to expand access to high‑precision positioning and 3D mapping technologies across surveying, AEC, energy, and public safety sectors.

• In December 2025, Pix4Dmatic released major software enhancements, including a new orthomosaic editor, seamless LiDAR point cloud integration, up to 300× accelerated cloud export performance, and boosted data exchange formats, significantly improving large‑scale mapping workflows and professional deliverables. (Pix4D)

• In October 2025, Pix4Dcloud introduced advanced georeferenced Gaussian splatting visualization and expanded drone dataset support alongside Annotation Snapping, direct ArcGIS Online export, and Region of Interest processing, enhancing field‑to‑cloud workflows, GIS interoperability, and collaboration.

• In September 2025, Pix4D launched a unified ecosystem update introducing Organization Management for enterprise collaboration, centralizing licenses and team workflows to strengthen spatial data capture, processing, and analysis across departments.

The Photogrammetry Software Market Report outlines a comprehensive analysis of technologies, segments, and end‑use landscapes shaping the global spatial data capture and 3D modelling ecosystem. It covers core product types such as aerial, terrestrial, satellite, and macro photogrammetry software, detailing how each supports varied use cases from infrastructure mapping to precision agriculture and environmental assessment. The report also segments by deployment mode, including on‑premises and cloud‑native platforms, highlighting the operational preferences of government agencies, engineering firms, and enterprise teams. Geographic coverage spans all major regions — North America, Europe, Asia Pacific, Latin America, and Middle East & Africa — with insights into adoption patterns, local regulatory incentives, and regional infrastructure trends influencing implementation. Application analysis includes mapping, construction monitoring, topographic survey, and cultural heritage preservation, illustrating how photogrammetry tools address sector‑specific demands and operational intricacies. Technology focus areas such as AI‑assisted feature extraction, LiDAR fusion, real‑time processing capabilities, and digital twin integration are examined to show how innovation enhances accuracy, scalability, and workflow efficiency. The report also examines niche segments such as mobile‑based photogrammetry, immersive visualization, and integration with GIS/BIM environments, offering decision‑makers a robust view of both mainstream adoption and emerging opportunities within the photogrammetry software landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

8.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Pix4D, Agisoft, DroneDeploy, Propeller Aerobotics, Bentley Systems, Trimble, Esri, SimActive, Topcon Positioning Group, Riegl |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |