Reports

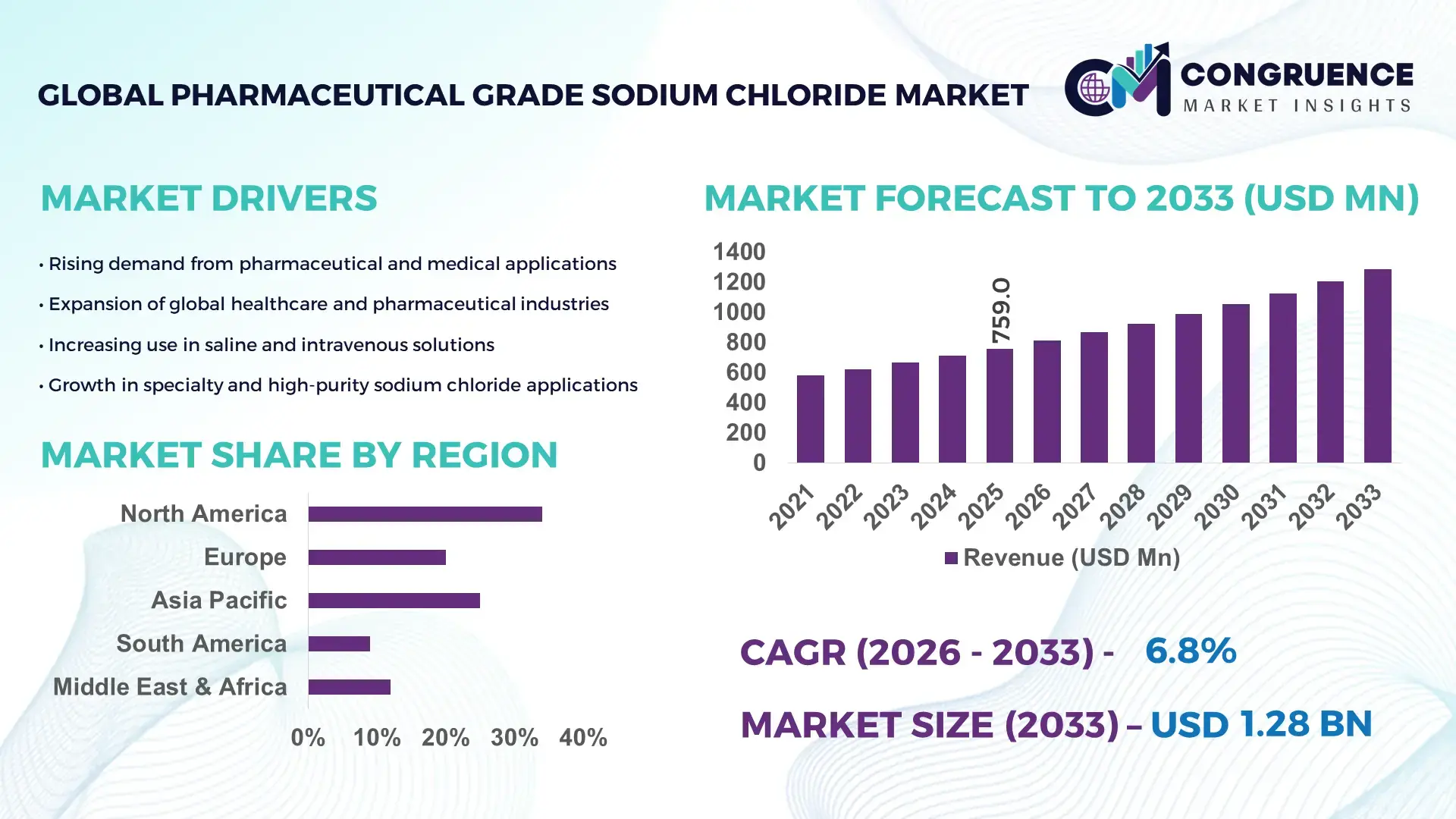

The Global Pharmaceutical Grade Sodium Chloride Market was valued at USD 759 Million in 2025 and is anticipated to reach a value of USD 1284.72 Million by 2033 expanding at a CAGR of 6.8% between 2026 and 2033. This growth is driven by rising demand for high‑purity sodium chloride in intravenous solutions, dialysis fluids, and advanced biopharmaceutical applications that require stringent quality standards.

Asia‑Pacific leads the global landscape with robust production capacity, particularly in China and India, where over 3.4 million metric tons of pharmaceutical grade sodium chloride were produced in 2023, supporting regional and international pharmaceutical supply chains. Investment in state‑of‑the‑art purification technologies and expansion of injection solution facilities has accelerated technological advancements, while pharmaceutical adoption in hospitals and clinics continues to expand with high‑volume injectable and dialysis use cases. Asia‑Pacific markets benefit from integrated salt‑to‑pharma manufacturing clusters, strong industrial backing, and increasing consumer adoption of advanced sterile solutions.

Market Size & Growth: Global market valued at ~USD 759M in 2025; projected to reach ~USD 1284.72M by 2033 at ~6.8% CAGR driven by expanding healthcare infrastructure and biopharmaceutical production.

Top Growth Drivers: Rising sterile injectable demand (45%), dialysis solution expansion (38%), and biologics manufacturing growth (29%).

Short‑Term Forecast: By 2028, production efficiency improvements expected to reduce operational cost by ~12% through enhanced crystallization and purification processes.

Emerging Technologies: Advanced vacuum crystallization systems; multi‑compendial compliance analytics; low endotoxin purification frameworks.

Regional Leaders: Asia‑Pacific ~USD 310M by 2033 with rapid pharmaceutical adoption, North America ~USD 235M with mature healthcare demands, Europe ~USD 285M with quality‑focused production.

Consumer/End‑User Trends: Hospital infusion centers and dialysis clinics increasingly adopt ultra‑pure sodium chloride; pharmaceutical CDMOs integrate high‑purity inputs for complex formulations.

Pilot or Case Example: In 2025, a scalable purification pilot yielded a 15% uptick in low‑endotoxin sodium chloride output, reducing batch defects.

Competitive Landscape: Leading supplier controls ~13% share; major competitors include AkzoNobel, Tata Chemicals, Nouryon, and Dominion Salt.

Regulatory & ESG Impact: Adoption of stringent USP/EP/JP specifications and environmental mandates on energy‑efficient production influence manufacturing compliance.

Investment & Funding Patterns: Recent investments exceeded USD 120M in plant upgrades, capacity expansion, and GMP compliance projects.

Innovation & Future Outlook: Forward‑looking projects emphasize smart manufacturing integration, trace‑metal control technologies, and supply chain localization.

The Pharmaceutical Grade Sodium Chloride Market encompasses major industry sectors including sterile injectable production, dialysis treatment solutions, oral rehydration therapies, and specialized excipients for biopharmaceutical manufacturing, collectively contributing significant utilization. Recent technological innovations, such as ultra‑low endotoxin purification processes and automated GMP‑certified production lines, have enhanced product quality and reduced contamination risk. Regulatory drivers including USP/EP/JP compliance frameworks and quality mandates continue to shape market adoption, while economic factors such as healthcare investment and infrastructure expansion support regional consumption growth. Asia‑Pacific demonstrates strong growth dynamics with increasing processing capacity and downstream pharmaceutical integration, Europe emphasizes quality‑driven adoption, and North American demand remains anchored in advanced hospital and clinical utilization patterns, with future trends pointing toward tailored sodium chloride grades for emerging therapies and personalized medicine applications.

The Pharmaceutical Grade Sodium Chloride Market holds strategic relevance as a foundational raw material for critical healthcare applications such as intravenous (IV) saline solutions, dialysis fluids, injectable medications, and biologics manufacturing, anchoring pharmaceutical production and clinical care standards. Advanced purification technologies such as membrane filtration and recrystallization deliver up to 30% improvement in impurity removal compared to older standard crystallization methods, significantly enhancing product quality and regulatory compliance performance. North America dominates in volume due to well‑established healthcare infrastructure and rigorous compendial adherence, while Asia‑Pacific leads in adoption with over 40% of global production capacity and fast‑growing pharmaceutical manufacturing enterprises. By 2028, integration of artificial intelligence (AI)‑based quality monitoring systems is expected to improve batch consistency and reduce quality deviations by roughly 18%, supporting scalability and traceability across distributed production networks. Firms are committing to ESG metrics such as energy efficiency improvements and a 22% reduction in water usage intensity by 2029 through closed‑loop water recycling systems that align with sustainability mandates and cost controls. In 2025, a leading Indian pharmaceutical chemical producer achieved a 14% reduction in endotoxin variability through automated purification analytics, highlighting measurable operational gains. Looking ahead, the Pharmaceutical Grade Sodium Chloride Market is poised as a pillar of resilience, compliance, and sustainable growth in global healthcare supply chains, driving innovation and quality assurance across critical therapeutic sectors.

The increasing prevalence of chronic diseases such as chronic kidney disease (CKD), cardiovascular disorders, and dehydration directly escalates demand for pharmaceutical grade sodium chloride due to its critical use in dialysis and intravenous solutions. A significant proportion of dialysis treatments rely on high‑purity sodium chloride to maintain electrolyte balance and support hemodialysis efficacy, with a growing chronic kidney disease patient population requiring frequent treatment. Expansion of minimally invasive surgical procedures and emergency care interventions also drives the necessity for sterile saline solutions, heightening the adoption of pharmaceutical grade specifications. Concurrently, expanding global healthcare infrastructure and rising healthcare expenditures in emerging economies increase the volume of hospital admissions and injectable drug use, reinforcing demand. Additionally, biopharmaceutical and biologics manufacturing, which depends on high‑purity excipients for formulation stability and compatibility, further amplifies market growth. Together, these healthcare demand drivers underscore the indispensable nature of pharmaceutical grade sodium chloride across multiple critical care and treatment pathways, underpinning sustained market expansion.

Stringent regulatory requirements and quality standards impose significant restraints on the Pharmaceutical Grade Sodium Chloride Market by increasing the complexity and cost of production, limiting entry, and slowing time‑to‑market for new players. Producers must adhere to rigorous compendial specifications such as USP, EP, JP, and other pharmacopeial guidelines that govern purity, endotoxin levels, microbial control, and documentation, requiring substantial investment in quality control systems and clean manufacturing environments. These compliance demands elevate operational costs and create barriers for smaller manufacturers that may lack the capital to implement advanced analytical testing and cleanroom facilities, effectively narrowing the competitive landscape. Regulatory approval processes involve extensive validation, audits, and documentation, which lengthen product development cycles and delay commercialization, particularly across regions with divergent regulatory frameworks. Furthermore, maintaining consistent production quality and robust supply chain coordination is challenging due to strict oversight and quality assurance expectations. These factors collectively restrain market expansion by concentrating production among established manufacturers that can absorb regulatory costs and navigate complex compliance landscapes.

The expansion of biopharmaceutical manufacturing and growing healthcare access in emerging markets present compelling opportunities for the Pharmaceutical Grade Sodium Chloride Market. Increasing investments in biologics, vaccine production, and cell therapy development require high‑purity excipients like pharmaceutical grade sodium chloride for formulation stability, buffer preparation, and injectable solutions, driving new demand avenues. Emerging economies such as India, China, and Southeast Asian markets are rapidly scaling healthcare infrastructure and pharmaceutical manufacturing capacities, creating substantial uptake potential as domestic producers seek compliant raw materials to support regional supply chains. Public and private sector spending on healthcare expansion enhances access to hospitals, dialysis centers, and specialized clinics, broadening consumption patterns. Technological innovations in purification, traceability, and automated quality monitoring also enable cost efficiencies and scalability for manufacturers targeting these growth regions. Strategic partnerships between global salt producers and local pharmaceutical entities further facilitate market penetration and knowledge transfer, unlocking new customer segments and expanding geographic reach. These opportunities position the market for accelerated adoption in specialized pharmaceutical applications and emerging healthcare systems.

Rising production costs and supply chain complexities present significant challenges to the Pharmaceutical Grade Sodium Chloride Market, affecting profitability, scalability, and supply reliability. The highly purified nature of pharmaceutical grade sodium chloride necessitates energy‑intensive purification processes, specialized filtration systems, and strict quality control measures, which increase operational expenditures for manufacturers. Fluctuations in raw material prices, particularly high‑purity brine or rock salt inputs, contribute to cost volatility and complicate pricing strategies. Additionally, maintaining contaminant‑free supply chains requires robust logistics coordination, traceability mechanisms, and cold‑chain management for sensitive formulations, adding layers of complexity and risk. Environmental sustainability concerns, such as water usage and waste management associated with crystallization processes, may lead to stricter regulations and higher compliance expenses, particularly in regions with resource constraints. These production and supply chain challenges strain manufacturing capacity, particularly for smaller producers, and can result in supply disruptions or cost pressures that constrain market growth despite steady demand for pharmaceutical applications.

Expansion of High-Purity Injectable Applications: The demand for ultra-pure pharmaceutical grade sodium chloride in injectable formulations continues to grow, with over 60% of hospitals in North America and Europe now using advanced low-endotoxin saline solutions. Automation in filtration and crystallization has improved product consistency by 18%, supporting safer intravenous therapy and dialysis treatments.

Integration of AI and Real-Time Quality Monitoring: Pharmaceutical producers are increasingly deploying AI-driven monitoring systems, with adoption rates exceeding 40% in Asia-Pacific manufacturing facilities. These systems deliver up to 20% faster detection of impurities compared to traditional laboratory inspections, enabling real-time process adjustments and reducing batch discard rates by 12%.

Sustainability and ESG Compliance Measures: Firms are actively implementing ESG initiatives, including closed-loop water recycling and energy-efficient purification processes. Approximately 35% of manufacturers have reduced water consumption intensity by 22% over the last two years, while energy-efficient crystallization equipment has cut electricity usage by 15%, meeting stricter environmental compliance standards.

Regional Diversification and Localized Production: Asia-Pacific now accounts for 42% of global production volume, with localized manufacturing hubs reducing dependency on imports. In Europe, 48% of pharmaceutical companies are investing in regional production lines to ensure uninterrupted supply, while North America is optimizing warehouse and logistics networks to lower downtime by 10% and improve inventory turnover.

The Pharmaceutical Grade Sodium Chloride Market is segmented into types, applications, and end-users, providing a comprehensive view of supply and demand dynamics. By type, the market is categorized into injectable grade, oral rehydration grade, and excipient grade, each serving distinct pharmaceutical and healthcare requirements. Injectable-grade sodium chloride dominates adoption due to its critical role in IV solutions and dialysis applications, accounting for approximately 58% of total consumption. Applications span dialysis solutions, intravenous therapy, biologics manufacturing, and oral rehydration formulations, with dialysis and IV solutions collectively representing over 65% of usage, reflecting high-volume healthcare demand. End-users include hospitals, clinical laboratories, pharmaceutical manufacturers, and dialysis centers, with hospitals leading in volume at around 50% due to large-scale infusion and surgical treatment requirements. Other end-users, including research institutions and specialty pharma manufacturers, contribute to the remaining 35%, focusing on high-precision and niche applications. This segmentation highlights both current adoption trends and areas for strategic investment, supporting decision-makers in resource allocation and production planning.

Injectable-grade sodium chloride is the leading type, accounting for 58% of the market, primarily due to its indispensable role in IV therapy and hemodialysis solutions. Automated purification and low-endotoxin processes have strengthened its adoption in hospitals and dialysis centers globally. Oral rehydration grade accounts for 22%, used in solutions for dehydration management, particularly in pediatric and emergency care, while excipient-grade products make up the remaining 20%, serving niche applications in biopharmaceutical and laboratory formulations. The fastest-growing type is excipient grade, driven by rising biologics and personalized medicine formulations, expected to surpass 25% adoption by 2033.

Dialysis and intravenous therapy applications lead the market, together accounting for 65% of adoption, due to consistent patient demand and healthcare infrastructure expansion. Dialysis solutions dominate slightly at 35%, as chronic kidney disease prevalence continues to grow globally. The fastest-growing application is biologics manufacturing, supported by trends in vaccine production, cell therapy, and injectable biologics requiring high-purity sodium chloride; adoption in this segment is projected to rise significantly, reaching nearly 20% by 2033. Other applications, including oral rehydration therapies and buffer preparation, account for the remaining 15%, addressing emerging and regional-specific healthcare needs.

Hospitals are the leading end-user segment, representing roughly 50% of market consumption, driven by high-volume infusion, dialysis, and surgical applications. Dialysis centers are the fastest-growing end-user segment, with adoption expected to increase by over 18% by 2033, fueled by rising chronic kidney disease cases and expansion of renal care facilities in Asia-Pacific. Pharmaceutical manufacturers account for 30% of use, employing sodium chloride in injectable drug formulations and biologics production, while research institutions and specialty labs comprise the remaining 20%, focusing on precision applications and quality compliance.

North America accounted for the largest market share at 34% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

North America consumed over 260,000 metric tons of pharmaceutical grade sodium chloride in 2025, driven by high-volume hospitals, dialysis centers, and biologics manufacturing facilities. Asia-Pacific production exceeded 340,000 metric tons, with China and India leading adoption through local manufacturing clusters. Europe held 28% of the market in 2025, with Germany, France, and the UK as primary consumers. South America contributed 12%, concentrated in Brazil and Argentina, while the Middle East & Africa accounted for 6% with notable growth in UAE and South Africa. Advanced purification technology adoption rates are highest in North America (over 40%), while Asia-Pacific leads in production capacity expansion. Regional variations in consumer behavior include higher institutional adoption in North America, regulatory-driven demand in Europe, and rapid manufacturing integration in Asia-Pacific.

How are technological advancements and healthcare adoption shaping high-purity sodium chloride use?

North America holds a 34% market share, driven by hospitals, dialysis centers, and pharmaceutical manufacturers. Government support for healthcare infrastructure upgrades and stricter compendial compliance is accelerating adoption. Technological advancements, including AI-based quality monitoring and automated crystallization systems, enhance product consistency by 18%. Local players, such as Morton Salt, have introduced advanced low-endotoxin injectable solutions, catering to large hospital networks. Consumer behavior reflects high enterprise adoption, with over 65% of hospital chains using ultra-pure sodium chloride in infusion and dialysis applications. Digital transformation in supply chain and traceability further supports rapid distribution and inventory optimization.

How do regulatory mandates and sustainability initiatives drive premium sodium chloride adoption?

Europe accounts for approximately 28% of the global market, with Germany, the UK, and France as key contributors. Regulatory pressure from USP, EP, and national quality standards ensures high-quality production and consistent supply. Emerging technologies, including automated filtration and low-endotoxin analytics, are being implemented across European facilities to meet stringent compliance. Local manufacturers, such as AkzoNobel, have upgraded purification plants, improving efficiency and traceability. Regulatory emphasis on environmental sustainability has led to 20% reductions in water consumption across production lines. European consumer behavior favors explainable and traceable products, supporting demand for pharmaceutical grade sodium chloride that meets both safety and ESG criteria.

What infrastructure and production expansions are driving regional sodium chloride consumption?

Asia-Pacific is the fastest-growing region, with production volumes surpassing 340,000 metric tons in 2025. China, India, and Japan are the top-consuming countries, with hospitals, dialysis centers, and pharmaceutical manufacturers driving demand. Expansion of integrated salt-to-pharma manufacturing hubs and adoption of automated crystallization technology have improved product consistency by 15%. Local players, such as Tata Chemicals, are investing in new purification facilities and high-purity injectable lines. Regional trends include rapid adoption of digital monitoring tools and process automation. Consumer behavior reflects high demand for locally produced high-quality sodium chloride to support large-scale healthcare and pharmaceutical production.

How are industrial and government initiatives influencing sodium chloride demand?

South America accounted for roughly 12% of the market in 2025, with Brazil and Argentina as leading consumers. Hospitals and dialysis centers drive adoption, supported by government incentives for pharmaceutical production and trade facilitation. Infrastructure improvements, including modernized crystallization facilities, have increased supply reliability by 10%. Local players are upgrading production capabilities to meet regulatory standards and regional demand fluctuations. Consumer behavior shows preference for locally manufactured products that reduce import dependency. Energy-efficient purification processes and digital monitoring are being gradually introduced to enhance production efficiency and product consistency.

What regional trends and modernization initiatives shape market growth?

The Middle East & Africa held 6% of the market in 2025, with UAE and South Africa as major growth countries. Demand is driven by hospitals, dialysis centers, and pharmaceutical manufacturers, supported by oil & gas sector investment in infrastructure. Technological modernization, including automated filtration systems and low-endotoxin analytics, is increasing efficiency and quality control. Local regulations and trade partnerships encourage compliance and regional production. Consumer behavior varies, with institutions prioritizing high-purity locally sourced sodium chloride to ensure continuous supply. Regional producers are implementing energy-efficient crystallization and water recycling measures, supporting sustainability goals while meeting growing healthcare needs.

China: 22% market share; dominance due to large-scale production capacity and extensive pharmaceutical manufacturing infrastructure.

United States: 20% market share; strong hospital and dialysis center demand, coupled with regulatory compliance and advanced technology adoption, supports leadership.

The Pharmaceutical Grade Sodium Chloride market exhibits a moderately fragmented competitive environment, with over 75 active global manufacturers operating across North America, Europe, and Asia-Pacific. The top five companies collectively hold approximately 48% of total market share, indicating a mix of established leaders and emerging regional players. Market leaders are focusing on strategic initiatives such as capacity expansion, advanced purification technology adoption, product differentiation, and cross-border partnerships to strengthen their market positioning. In 2025, several companies launched low-endotoxin injectable-grade sodium chloride lines, while others invested in automated crystallization and digital quality monitoring systems to improve consistency and regulatory compliance. Innovation trends such as AI-driven process control, multi-compendial compliance analytics, and energy-efficient production methods are shaping competitive advantage, enabling firms to reduce production variability by up to 15% and accelerate time-to-market. Regional competition is intensifying, particularly in Asia-Pacific, where local players are expanding manufacturing hubs, while North American and European firms focus on premium high-purity products. The market’s competitive nature encourages continuous technological advancement and strategic partnerships, reinforcing resilience and differentiation in a growing global landscape.

Dominion Salt

Nouryon

Cargill Salt

K+S Group

Tata Chemicals Europe

Compass Minerals International

Ercros S.A.

The Pharmaceutical Grade Sodium Chloride Market is increasingly driven by advancements in purification, automation, and quality assurance technologies. Current production relies heavily on vacuum crystallization, membrane filtration, and multi-stage recrystallization systems, which collectively remove up to 99.9% of impurities and ensure compliance with USP, EP, and JP compendial standards. Approximately 42% of manufacturing facilities in North America and Europe now employ automated quality monitoring systems, enabling real-time detection of endotoxins and particulates, which reduces batch rejection rates by nearly 12%.

Emerging technologies are further transforming production efficiency and product consistency. AI-enabled process control is being integrated into filtration and crystallization lines, improving process stability by 15% and reducing manual inspection requirements. Digital twin modeling is being applied in select facilities, allowing simulation of production cycles and predictive maintenance, which decreases unplanned downtime by 10%. Additionally, low-energy crystallization equipment and closed-loop water recycling systems are being implemented, resulting in a 20% reduction in energy consumption and a 22% decrease in water usage intensity.

Trace-metal control technologies are gaining traction, particularly in biologics and injectable-grade production, ensuring ultrahigh purity for critical pharmaceutical applications. Some regional innovation hubs in Asia-Pacific have deployed smart manufacturing systems that combine IoT sensors, AI analytics, and automated reporting, enhancing traceability and ensuring regulatory compliance. These technological advancements are enabling manufacturers to produce higher-quality sodium chloride more efficiently, while supporting sustainability goals, regulatory adherence, and operational resilience, positioning the market for continued innovation and competitive differentiation.

• In early 2024, Tata Chemicals completed an upgrade at its Gujarat facility to add a dedicated pharmaceutical‑grade sodium chloride production line compliant with USP, EP, and JP standards, enhancing injectable use readiness and operational capacity improvements noted throughout the year.

• In 2024, US Salt implemented automated batch traceability and contamination detection systems at its Rochester plant, improving regulatory audit outcomes and reducing product recalls through advanced digital quality controls that strengthened operational consistency.

• In 2024, Cargill launched pre‑filled sterile sodium chloride ampoules tailored for hospital automation systems, addressing growing demand for barcoded, ready‑to‑use excipients and supporting hospital supply chain efficiency.

• In 2025, K+S Group entered a strategic partnership with a dialysis fluid packaging firm in Austria, enabling co‑packaged delivery of sodium chloride concentrate with bicarbonate cartridges for streamlined end‑use in renal therapy centers.

The Pharmaceutical Grade Sodium Chloride Market Report provides a comprehensive analysis of global market segments, geographic distributions, application areas, technology trends, competitive landscapes, and emerging focus areas relevant to decision‑makers across pharmaceutical and healthcare sectors. The report examines key product types used—including injectable, dialysis, oral rehydration, and excipient grades—highlighting differences in purity levels, end‑use environments, and manufacturing process complexities. Regional analysis covers North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, detailing production capacities, consumption patterns, regulatory influences, and infrastructure readiness across these markets. The report also explores application segments such as intravenous therapy, dialysis solutions, biologics production, and specialty formulations, outlining usage volumes and adoption trends among healthcare institutions, dialysis centers, and pharmaceutical manufacturers. Technology trends such as advanced purification systems, automated quality monitoring, digital traceability, and low‑endotoxin production techniques are examined for their impact on product integrity and operational scalability. Industry drivers like chronic disease prevalence, healthcare infrastructure development, and compendial compliance pressures are coupled with insights on sustainability measures, supply chain resilience, and digital transformation adoption. Niche market segments such as ultra‑pure salts for biopharmaceuticals and ready‑to‑use sterile formats are also discussed, providing a full scope of current and future market opportunities. The report is structured to support strategic planning, competitive benchmarking, and investment prioritization for corporate leaders, analysts, and stakeholders engaged in pharmaceutical grade sodium chloride production, distribution, or utilization.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

6.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Morton Salt, Tata Chemicals, AkzoNobel, Dominion Salt, Nouryon, Cargill Salt, K+S Group, Tata Chemicals Europe, Compass Minerals International, Ercros S.A. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |