Reports

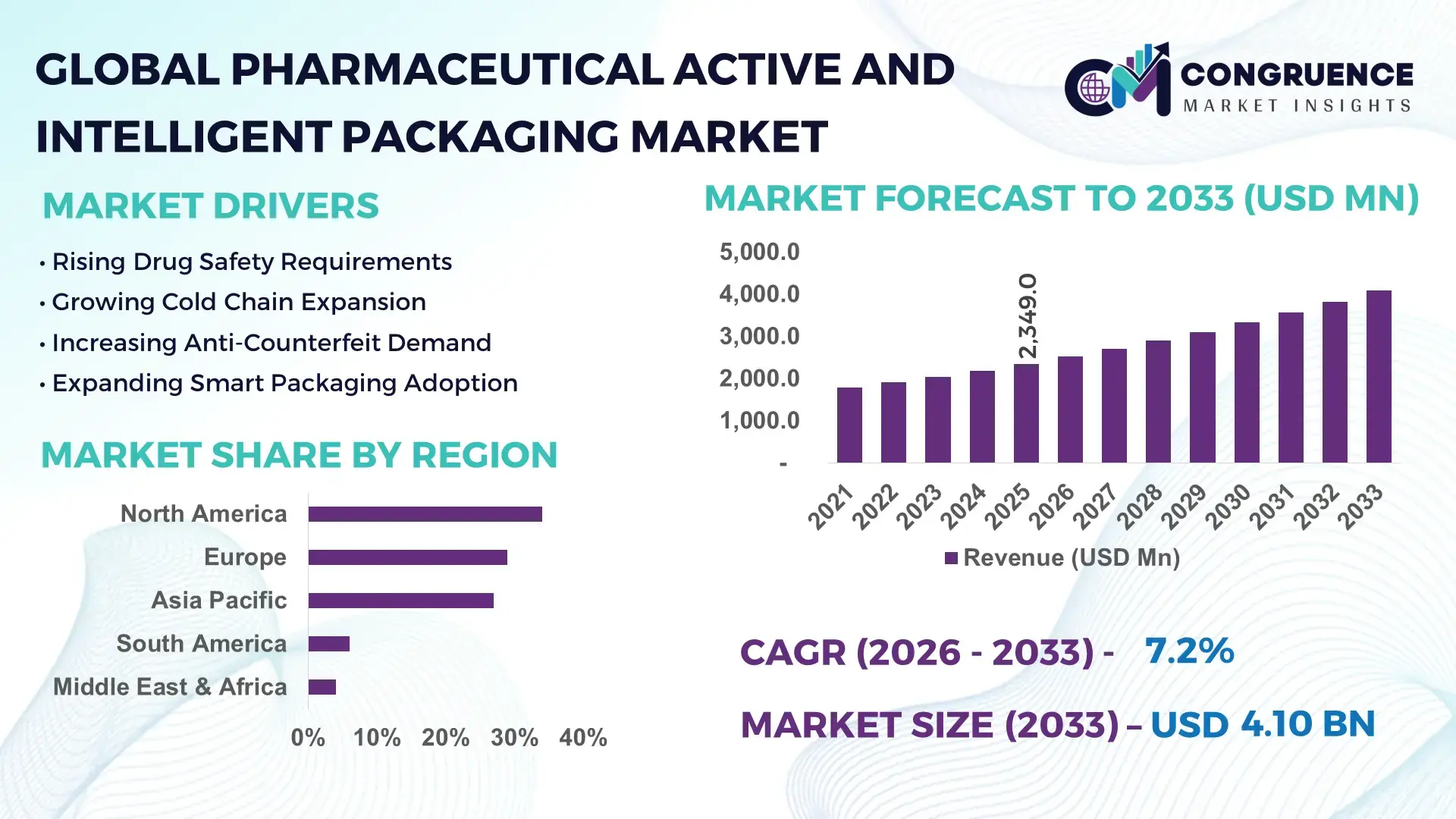

The Global Pharmaceutical Active and Intelligent Packaging Market was valued at USD 2,349.0 Million in 2025 and is anticipated to reach a value of USD 4,096.8 Million by 2033 expanding at a CAGR of 7.2% between 2026 and 2033. Rising adoption of temperature-sensitive biologics, serialization-enabled packaging systems, and oxygen/moisture scavenging technologies is accelerating deployment across pharmaceutical logistics and high-value drug distribution networks. Regulatory tightening around counterfeit drug prevention and cold-chain traceability is forcing pharmaceutical manufacturers to integrate RFID-enabled intelligent packaging and active barrier solutions at scale. Between 2024 and 2026, global pharmaceutical supply chains underwent aggressive restructuring due to Red Sea shipping disruptions, stricter EU Falsified Medicines Directive compliance, and U.S. Drug Supply Chain Security Act enforcement, pushing pharmaceutical companies toward digitally trackable and contamination-resistant packaging systems. Smart packaging integration in specialty pharmaceuticals increased by over 31%, while intelligent label deployment in biologics distribution expanded by nearly 27% during the same period.

The United States dominates the Pharmaceutical Active and Intelligent Packaging Market with approximately 34% global share, supported by over 45% of global biologics production capacity and extensive adoption of track-and-trace technologies across major pharmaceutical supply chains. More than 68% of U.S.-based pharmaceutical exporters now deploy intelligent packaging systems integrated with RFID or NFC-enabled monitoring, compared to less than 40% adoption across several developing markets. The country also benefits from over USD 4 billion in pharmaceutical cold-chain infrastructure investments since 2023, enabling faster commercialization of sensor-based and antimicrobial packaging technologies. Compared with Asia-Pacific’s scale-driven manufacturing ecosystem, the U.S. market leads in intelligent compliance packaging innovation and premium-value deployment.

As pharmaceutical distribution networks become increasingly digitized and regulation-intensive, companies prioritizing intelligent compliance packaging, traceability integration, and active preservation technologies are positioning themselves to capture long-term operational and competitive advantage.

Market Size & Growth: USD 2,349.0 Million in 2025 reaching USD 4,096.8 Million by 2033, driven by 31% higher biologics packaging demand and smart traceability adoption.

Top Growth Drivers: Cold-chain pharmaceutical expansion (+29%), anti-counterfeit regulation adoption (+34%), and smart sensor integration growth (+26%) are accelerating global deployment.

Short-Term Forecast: By 2028, intelligent packaging deployment is projected to reduce pharmaceutical spoilage losses by 18% and improve shipment visibility efficiency by 24%.

Emerging Technologies: AI-enabled tracking, NFC/RFID smart labels, and oxygen-scavenging materials are reshaping advanced pharmaceutical packaging operations globally.

Regional Leaders: North America holds 34% share, Europe 29%, and Asia-Pacific 27%, with Asia-Pacific showing the fastest smart-packaging manufacturing expansion.

Consumer/End-User Trends: Over 63% of pharmaceutical firms now prioritize real-time packaging traceability and temperature-monitoring capabilities for specialty drug logistics.

Pilot/Case Example: In 2025, a smart biologics packaging rollout reduced temperature excursion incidents by 22% across cross-border pharmaceutical shipments.

Competitive Landscape: Top players control nearly 41% market concentration, led by Amcor, WestRock, AptarGroup, Berry Global, and Sonoco Products.

Regulatory & ESG Impact: Sustainable pharmaceutical packaging adoption increased 28% following EU recycling mandates and stricter compliance on single-use material reduction.

Investment & Funding: More than USD 2.1 billion has been allocated toward smart packaging automation, cold-chain monitoring, and pharmaceutical traceability partnerships since 2024.

Innovation & Future Outlook: Blockchain-enabled authentication, printable biosensors, and connected packaging ecosystems are transforming next-generation pharmaceutical supply intelligence.

Pharmaceutical manufacturers, biologics companies, and healthcare logistics providers collectively account for over 72% of total packaging demand, with biologics and specialty therapeutics representing the fastest technology adoption segment. Intelligent RFID-enabled packaging deployments increased by 27%, while active moisture-control systems improved product stability performance by nearly 19% in temperature-sensitive applications. North America continues to dominate premium intelligent packaging adoption, whereas Asia-Pacific leads large-scale pharmaceutical packaging manufacturing expansion amid global supply chain diversification. Growing regulatory enforcement around counterfeit prevention and serialization is accelerating demand for digitally integrated pharmaceutical packaging ecosystems, setting the stage for deeper strategic transformation across healthcare logistics and compliance infrastructure.

The Pharmaceutical Active and Intelligent Packaging Market is rapidly transforming into a strategic battleground for pharmaceutical manufacturers, healthcare logistics providers, and packaging technology companies as product integrity, regulatory traceability, and biologics protection become mission-critical competitive priorities. Intelligent packaging is no longer viewed as a secondary compliance layer; it is becoming a core operational infrastructure component enabling pharmaceutical firms to optimize distribution accuracy, reduce product loss, and secure cross-border supply chain transparency.

Global pharmaceutical supply chains are facing mounting pressure from stricter serialization mandates, biologics transportation risks, and counterfeit medicine infiltration. This shift is accelerating investment into intelligent monitoring technologies, active barrier systems, and digitally integrated packaging platforms capable of real-time condition tracking. RFID-enabled intelligent packaging improves shipment visibility efficiency by 34% while reducing manual inventory verification costs by nearly 21% compared to legacy barcode-based systems. Similarly, oxygen-absorbing active packaging technologies are extending sensitive drug shelf stability by over 18%, significantly lowering waste exposure during international transit. North America leads in pharmaceutical intelligent packaging volume deployment due to its advanced biologics ecosystem and regulatory enforcement intensity, while Europe leads sustainability-focused innovation with more than 42% of pharmaceutical packaging suppliers integrating recyclable active-material platforms into production lines. Asia-Pacific, however, is rapidly transforming into the execution hub for scalable intelligent packaging manufacturing due to lower production costs and accelerated pharmaceutical exports.

Over the next three years, pharmaceutical companies are projected to increase intelligent packaging integration across specialty drug logistics by over 30%, while automated temperature-monitoring deployment is expected to reduce cold-chain product rejection rates by nearly 20%. ESG alignment is also becoming a measurable competitive advantage, as recyclable intelligent packaging formats are lowering compliance-related waste handling costs by approximately 15% across regulated European pharmaceutical markets.

A major pharmaceutical cold-chain operator recently deployed AI-connected smart labels across vaccine transportation networks, reducing shipment monitoring delays by 26% and improving real-time intervention response accuracy by 33%. In response, leading packaging companies are accelerating capital allocation toward sensor-enabled packaging lines, digital authentication platforms, and pharmaceutical-grade recyclable materials to strengthen long-term positioning. As pharmaceutical distribution ecosystems become increasingly digitized, regulated, and biologics-driven, companies capable of integrating intelligent traceability, active preservation, and sustainable packaging innovation into scalable operational models will secure decisive competitive advantage in the next phase of global pharmaceutical infrastructure transformation.

The Pharmaceutical Active and Intelligent Packaging Market is being reshaped by the convergence of pharmaceutical serialization mandates, biologics expansion, smart logistics transformation, and rising pressure to reduce drug spoilage across global healthcare supply chains. Demand is increasingly concentrated around intelligent traceability systems, temperature-monitoring labels, oxygen-scavenging materials, and contamination-resistant packaging solutions capable of protecting high-value pharmaceuticals during long-distance distribution. Over 64% of pharmaceutical manufacturers now prioritize digitally trackable packaging systems to strengthen compliance visibility and supply chain control. The market is also experiencing operational restructuring due to geopolitical shipping instability, stricter anti-counterfeit enforcement, and rapid expansion of specialty therapeutics requiring precision-controlled transport conditions. North America and Europe continue leading intelligent compliance adoption, while Asia-Pacific is emerging as the dominant pharmaceutical packaging manufacturing hub due to lower conversion costs and expanding pharmaceutical exports. Companies are aggressively investing in automation, smart labeling infrastructure, and sustainable active-material technologies to optimize operational resilience, reduce compliance risk, and strengthen pharmaceutical product integrity across increasingly complex global distribution networks.

The rapid expansion of biologics, specialty therapeutics, and temperature-sensitive pharmaceuticals is becoming the primary structural growth engine for the Pharmaceutical Active and Intelligent Packaging Market. More than 38% of newly approved pharmaceuticals now require controlled packaging environments, forcing manufacturers to adopt active moisture-control systems, oxygen absorbers, and sensor-enabled intelligent packaging solutions. Simultaneously, pharmaceutical serialization compliance adoption exceeded 71% across regulated markets in 2025, accelerating deployment of RFID-enabled labels and digitally trackable packaging systems. Global supply chain disruptions following Red Sea shipping instability and stricter U.S. Drug Supply Chain Security Act enforcement exposed major vulnerabilities in pharmaceutical logistics, increasing industry focus on real-time monitoring and anti-counterfeit protection. This shift directly increased investment in intelligent cold-chain packaging infrastructure by nearly 29% over two years. Pharmaceutical companies are responding aggressively through smart-packaging partnerships, automated packaging-line upgrades, and regional expansion strategies. Several packaging suppliers expanded intelligent label production capacity by over 20% to meet biologics distribution demand, while pharmaceutical manufacturers increasingly prioritize integrated packaging ecosystems capable of combining compliance, monitoring, and product protection within a single operational framework.

Despite strong adoption momentum, the Pharmaceutical Active and Intelligent Packaging Market faces significant structural limitations linked to high material costs, regulatory fragmentation, and integration complexity across global pharmaceutical supply chains. Smart packaging systems incorporating RFID sensors, NFC chips, and active barrier technologies increase packaging conversion costs by approximately 18–25% compared with conventional pharmaceutical packaging formats. For cost-sensitive generic drug manufacturers, this creates substantial scalability pressure. The market also remains heavily dependent on specialized electronic components and pharmaceutical-grade polymers, with nearly 62% of advanced sensor materials sourced from concentrated supplier networks in East Asia. Geopolitical trade disruptions and semiconductor supply instability between 2024 and 2025 created lead-time extensions exceeding 30% for intelligent packaging components, constraining deployment schedules across several pharmaceutical exporters. Regulatory inconsistency between the U.S., Europe, and emerging markets further complicates global scalability. Pharmaceutical companies operating across multiple regions must adapt packaging configurations to varying serialization, recycling, and traceability standards, increasing operational complexity and compliance costs. In response, companies are diversifying supplier networks, securing long-term semiconductor procurement agreements, and accelerating development of lower-cost printable sensor technologies to reduce dependency on traditional smart-chip architectures.

The integration of connected packaging ecosystems, AI-enabled monitoring, and sustainable active-material technologies is unlocking high-impact growth opportunities across the Pharmaceutical Active and Intelligent Packaging Market. More than 41% of pharmaceutical logistics providers are actively deploying intelligent packaging systems capable of real-time temperature tracking, tamper detection, and predictive shipment analytics. These technologies are improving shipment visibility by over 32% while reducing cold-chain waste exposure by nearly 19%. A major opportunity is emerging around printable electronics and battery-free intelligent labels, which reduce smart packaging deployment costs by approximately 22% compared with traditional embedded-chip systems. This cost shift is enabling broader adoption among mid-sized pharmaceutical manufacturers previously constrained by integration expenses. Asia-Pacific and Middle Eastern pharmaceutical hubs are also accelerating localized smart-packaging production investments to reduce dependence on imported packaging technologies. Pharmaceutical companies are positioning aggressively through R&D partnerships, AI logistics integration, and recyclable active-material innovation programs designed to capture future regulatory and operational advantages. Companies capable of combining sustainability, traceability, and automation within scalable packaging platforms are increasingly securing long-term pharmaceutical supply agreements and premium-value biologics contracts.

Execution complexity remains one of the most significant long-term challenges confronting the Pharmaceutical Active and Intelligent Packaging Market. Integrating intelligent monitoring systems, active barrier technologies, and pharmaceutical compliance requirements into high-speed packaging operations demands substantial infrastructure modernization and digital interoperability investment. More than 46% of pharmaceutical packaging facilities still operate on partially legacy production systems incapable of supporting large-scale intelligent packaging integration. The challenge is intensified by inconsistent global digital infrastructure and fragmented cold-chain logistics capabilities. Temperature excursion incidents continue affecting nearly 14% of cross-border biologics shipments in developing logistics corridors, undermining intelligent packaging performance consistency despite technology improvements. Additionally, smart packaging implementation increases packaging validation timelines by approximately 20%, slowing commercialization cycles for highly regulated pharmaceutical products. Labor shortages across pharmaceutical automation and semiconductor engineering sectors are also constraining deployment scalability. Companies must simultaneously balance sustainability compliance, operational efficiency, and digital transformation without disrupting production continuity. To remain competitive, leading packaging providers are accelerating automation investment, building cross-industry technology alliances, and redesigning packaging architectures around modular intelligent systems capable of faster deployment, lower maintenance complexity, and stronger compatibility across global pharmaceutical distribution environments.

34% Increase in RFID-Enabled Pharmaceutical Tracking Deployment Across Biologics Logistics: Intelligent packaging adoption is rapidly shifting toward RFID- and NFC-enabled tracking systems as pharmaceutical companies strengthen real-time shipment visibility and anti-counterfeit protection. Over 61% of specialty pharmaceutical exporters now integrate digital traceability layers into packaging operations, while automated inventory verification reduced manual reconciliation time by 28%. Companies are restructuring logistics workflows around connected packaging ecosystems to improve compliance speed and reduce biologics shipment losses amid ongoing global supply chain instability.

27% Expansion in Sustainable Active Packaging Integration Reshaping Material Procurement: Pharmaceutical packaging manufacturers are aggressively replacing conventional multilayer plastics with recyclable active-material alternatives and bio-based oxygen scavengers. Sustainable active packaging utilization increased by 27% between 2024 and 2026, while pharmaceutical firms reduced non-recyclable packaging intensity by nearly 18%. Regulatory pressure from Europe’s packaging waste directives is forcing suppliers to redesign production lines and secure low-emission raw-material sourcing partnerships, creating operational tension between sustainability goals and pharmaceutical-grade performance standards.

31% Growth in AI-Integrated Cold-Chain Monitoring Transforming Pharmaceutical Distribution: AI-connected intelligent labels and predictive monitoring systems are redefining pharmaceutical cold-chain execution. Smart monitoring deployment expanded by 31%, while automated temperature-alert systems improved intervention response speed by approximately 24%. Pharmaceutical logistics providers are scaling cloud-connected packaging analytics platforms to reduce temperature excursion risks and optimize cross-border biologics transportation efficiency. A non-obvious shift is emerging as companies increasingly centralize packaging data management alongside enterprise supply chain platforms for faster regulatory auditing.

22% Increase in Regionalized Smart Packaging Manufacturing Capacity Across Asia-Pacific: Pharmaceutical packaging production is rapidly regionalizing as companies reduce dependence on single-source supply chains. Asia-Pacific expanded intelligent packaging manufacturing capacity by 22%, supported by localized electronics integration and pharmaceutical export growth. Pharmaceutical companies are prioritizing high-volume, lower-cost intelligent packaging production ecosystems to shorten delivery cycles and improve supply resilience. In response to geopolitical shipping disruptions, packaging suppliers are accelerating regional joint ventures and automation investments to strengthen manufacturing continuity and operational flexibility.

The Pharmaceutical Active and Intelligent Packaging Market is segmented by type, application, and end-user, with demand increasingly concentrated around high-value pharmaceutical logistics, biologics preservation, and compliance-driven intelligent monitoring systems. Active packaging solutions continue dominating large-volume pharmaceutical preservation applications due to their scalability and lower integration complexity, while intelligent packaging systems are rapidly gaining traction in premium therapeutics and temperature-sensitive biologics distribution. More than 58% of demand originates from pharmaceutical manufacturing and specialty drug transportation applications, where contamination control, product stability, and traceability are operational priorities. Demand is shifting toward integrated smart-packaging ecosystems capable of combining monitoring, authentication, and active protection within a single packaging architecture. Pharmaceutical manufacturers are increasingly prioritizing intelligent packaging investments to reduce supply chain risk, strengthen regulatory compliance, and improve operational visibility across cross-border healthcare logistics networks.

Active packaging currently dominates the Pharmaceutical Active and Intelligent Packaging Market with approximately 62% share due to its broad scalability, lower deployment cost, and strong performance in moisture regulation, oxygen absorption, and contamination prevention across mass pharmaceutical distribution systems. Pharmaceutical companies continue prioritizing active packaging technologies because they integrate efficiently into existing production lines while improving drug stability and extending shelf-life performance by nearly 18%. Intelligent packaging, however, is emerging as the fastest-expanding segment, supported by over 29% growth in RFID-enabled traceability systems and connected pharmaceutical logistics platforms. Intelligent solutions are fundamentally reshaping high-value biologics transportation by enabling real-time monitoring, anti-counterfeit authentication, and automated shipment visibility. Compared with active packaging, intelligent packaging carries higher deployment costs but delivers stronger compliance integration and supply chain intelligence advantages, particularly for specialty therapeutics and cold-chain pharmaceuticals. The remaining hybrid packaging technologies account for nearly 14% of market demand, serving niche applications requiring both preservation control and digital traceability. Pharmaceutical packaging companies are increasingly investing in multifunctional systems capable of combining active protection with smart monitoring features to strengthen operational efficiency and premium-value product positioning. The market is clearly shifting toward integrated intelligent-active ecosystems, making digital traceability and smart preservation technologies strategic investment priorities for long-term competitive expansion.

Drug delivery and pharmaceutical preservation applications hold the leading share of the Pharmaceutical Active and Intelligent Packaging Market at approximately 48%, driven by high demand for moisture-control systems, oxygen scavengers, and contamination-resistant packaging in specialty therapeutics and biologics distribution. Usage concentration remains strongest in injectable drugs and temperature-sensitive formulations where packaging integrity directly impacts product stability and regulatory compliance outcomes. Track-and-trace and anti-counterfeit applications are emerging as the fastest-growing segment, supported by over 32% expansion in serialization compliance deployment and rising cross-border pharmaceutical trade complexity. Compared with traditional preservation-focused applications, intelligent authentication packaging is rapidly becoming operationally critical due to stricter pharmaceutical security regulations and increasing counterfeit medicine risks across international supply chains. The remaining applications, including condition monitoring and patient adherence systems, collectively account for nearly 30% of market demand and are gaining strategic relevance in connected healthcare ecosystems. Pharmaceutical companies are scaling deployment of NFC-enabled labels, AI-connected monitoring systems, and smart blister packaging to improve logistics visibility and patient engagement simultaneously. Demand is increasingly shifting toward integrated multifunctional packaging platforms capable of combining preservation, authentication, and digital monitoring into unified pharmaceutical distribution solutions.

Pharmaceutical manufacturers represent the dominant end-user segment in the Pharmaceutical Active and Intelligent Packaging Market with approximately 54% demand concentration due to large-scale dependency on drug stability protection, serialization compliance, and biologics transportation infrastructure. Major pharmaceutical firms are aggressively integrating intelligent packaging technologies into production and distribution operations to optimize regulatory compliance and reduce product-loss exposure across international supply chains. Healthcare logistics and cold-chain distribution providers are emerging as the fastest-growing end-user category, supported by over 26% expansion in temperature-sensitive pharmaceutical transportation volumes. Compared with traditional pharmaceutical manufacturing demand, logistics providers prioritize real-time monitoring, automated tracking, and predictive intervention systems to improve shipment integrity and operational efficiency across global biologics networks. Hospitals, specialty pharmacies, and clinical research organizations collectively account for nearly 24% of total demand, primarily focused on premium therapeutics handling, medication authentication, and patient safety optimization. Companies are increasingly targeting these segments through customized intelligent packaging systems, scalable monitoring solutions, and partnership-driven deployment models. Buying behavior is shifting toward integrated compliance-focused packaging ecosystems capable of improving operational transparency, reducing handling risk, and supporting precision pharmaceutical distribution requirements across regulated healthcare environments.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2026 and 2033.

North America maintains leadership due to advanced pharmaceutical manufacturing infrastructure, biologics concentration, and widespread deployment of intelligent traceability systems across regulated healthcare supply chains. Europe contributes nearly 29% of global demand, supported by sustainability-focused packaging regulation and aggressive adoption of recyclable active-material technologies. Asia-Pacific currently represents approximately 27% of global market activity and is rapidly accelerating through pharmaceutical export expansion, localized smart-packaging production, and lower manufacturing conversion costs. Demand remains concentrated in highly regulated pharmaceutical markets, while production capacity and operational scaling are increasingly shifting toward Asia-Pacific manufacturing ecosystems. Ongoing geopolitical shipping disruptions and serialization enforcement across major economies are accelerating regional packaging diversification strategies. Global companies are prioritizing investment across North America for premium innovation, Europe for compliance-driven sustainability transformation, and Asia-Pacific for scalable intelligent packaging manufacturing expansion.

North America holds approximately 34% of the Pharmaceutical Active and Intelligent Packaging Market, supported by strong biologics manufacturing capacity, advanced cold-chain infrastructure, and aggressive serialization compliance enforcement. Over 68% of pharmaceutical exporters in the region now deploy intelligent tracking technologies integrated with RFID or NFC-enabled systems to strengthen shipment visibility and anti-counterfeit protection. The region is being reshaped by stricter U.S. pharmaceutical traceability regulations and rapid expansion of specialty therapeutics requiring temperature-controlled distribution. Pharmaceutical companies increased investment in AI-enabled monitoring and smart-label automation by nearly 24% between 2024 and 2026. Several major packaging suppliers also expanded intelligent packaging conversion capacity by over 18% to meet biologics transportation demand. Enterprise buyers increasingly prioritize packaging ecosystems combining compliance automation, real-time monitoring, and sustainability performance, positioning North America as the primary global hub for premium intelligent pharmaceutical packaging innovation and commercialization.

Europe accounts for nearly 29% of the Pharmaceutical Active and Intelligent Packaging Market, driven by strict pharmaceutical compliance standards, sustainability-focused packaging directives, and strong adoption across Germany, France, and the United Kingdom. More than 42% of pharmaceutical packaging suppliers in the region have integrated recyclable active-material technologies into commercial production lines. The market is strongly influenced by EU packaging waste reduction mandates and expanded pharmaceutical traceability enforcement, forcing manufacturers to redesign packaging architectures around recyclable, digitally trackable solutions. Intelligent monitoring adoption across biologics packaging operations increased by approximately 25% during 2024–2026 as pharmaceutical companies optimized compliance efficiency and cross-border logistics transparency. European pharmaceutical buyers increasingly prioritize low-emission materials, traceability integration, and circular packaging performance over low-cost sourcing models. This regulatory-driven environment is forcing rapid innovation, making Europe a critical market for sustainable intelligent packaging transformation and next-generation pharmaceutical compliance infrastructure.

Asia-Pacific represents approximately 27% of the Pharmaceutical Active and Intelligent Packaging Market and is rapidly emerging as the largest pharmaceutical packaging production ecosystem globally. China, India, Japan, and South Korea are leading regional expansion through large-scale pharmaceutical exports, lower manufacturing conversion costs, and accelerated intelligent packaging localization. Regional intelligent packaging production capacity expanded by nearly 22% between 2024 and 2026, while pharmaceutical cold-chain infrastructure investment increased by approximately 19%. Companies are aggressively scaling localized RFID integration, automated packaging lines, and sensor-enabled labeling systems to strengthen export competitiveness and reduce supply chain dependency on Western manufacturing hubs. Enterprise buyers across Asia-Pacific prioritize speed, scalability, and cost efficiency, accelerating demand for mass-deployable intelligent packaging platforms. As global pharmaceutical supply chains diversify away from concentrated sourcing models, Asia-Pacific is becoming strategically critical for scalable smart-packaging production, operational flexibility, and long-term pharmaceutical logistics expansion.

South America contributes nearly 6% of the Pharmaceutical Active and Intelligent Packaging Market, led primarily by Brazil and Argentina due to expanding pharmaceutical manufacturing activity and improving healthcare logistics infrastructure. Rising demand for temperature-sensitive pharmaceuticals and imported specialty therapeutics is accelerating deployment of active preservation packaging and intelligent monitoring solutions across regional supply chains. However, the region continues facing structural constraints linked to import dependency for smart packaging components, currency volatility, and uneven cold-chain infrastructure availability. Intelligent packaging deployment costs remain approximately 17% higher than conventional alternatives across several regional markets, slowing broader adoption among smaller pharmaceutical operators. Despite these limitations, pharmaceutical distributors increased investment in localized cold-chain monitoring systems by over 14% during 2025. Enterprise buyers remain highly price-sensitive but increasingly prioritize packaging reliability and traceability, positioning South America as a strategic high-potential market requiring balanced cost optimization and infrastructure modernization strategies.

The Middle East & Africa region accounts for approximately 4% of the Pharmaceutical Active and Intelligent Packaging Market, with demand concentrated in the United Arab Emirates, Saudi Arabia, and South Africa due to healthcare infrastructure modernization and pharmaceutical import growth. Governments across the region are increasing investment in pharmaceutical logistics security and cold-chain reliability to support expanding healthcare delivery systems. Smart pharmaceutical packaging deployment increased by nearly 16% between 2024 and 2026, supported by hospital infrastructure expansion, vaccine distribution modernization, and strategic healthcare partnerships. Several regional healthcare logistics operators also implemented intelligent temperature-monitoring systems capable of reducing shipment integrity failures by approximately 20%. Enterprise buyers increasingly prioritize compliance visibility, temperature stability, and import reliability over low-cost packaging alternatives. As pharmaceutical distribution systems modernize and healthcare infrastructure investment accelerates, the region is emerging as a strategic long-term growth corridor for intelligent pharmaceutical packaging deployment and cold-chain transformation.

United States – 34% Market share: Dominates through advanced biologics manufacturing, large-scale cold-chain infrastructure, and strong pharmaceutical serialization compliance adoption.

China – 16% Market share: Leads large-scale manufacturing expansion due to high pharmaceutical export capacity, rapid smart-packaging localization, and cost-efficient production ecosystems.

The Pharmaceutical Active and Intelligent Packaging Market is dominated by global packaging leaders including Amcor, AptarGroup, Berry Global, Sonoco Products, WestRock, and CCL Industries, with competition intensifying between technology-focused intelligent packaging innovators and high-volume cost-efficient packaging manufacturers. The top five players collectively control approximately 41% of global market activity, creating a moderately consolidated structure where scale, compliance capability, and smart-packaging integration determine competitive positioning.

Competition is increasingly shifting away from traditional price-led models toward intelligent traceability, sustainable material science, and pharmaceutical-grade automation capabilities. Intelligent RFID-enabled packaging systems improve shipment visibility by nearly 34%, while recyclable active-material platforms reduce pharmaceutical waste handling costs by approximately 15%, making technology integration a primary competitive differentiator. Companies are aggressively expanding smart-packaging production capacity, securing pharmaceutical partnerships, and vertically integrating active-material supply chains to strengthen execution speed and compliance resilience.

The market is also undergoing consolidation pressure following large-scale healthcare packaging acquisitions and regional manufacturing expansion strategies. High validation requirements, regulatory complexity, and semiconductor integration costs remain major entry barriers, particularly for regional suppliers lacking pharmaceutical compliance infrastructure. Winning in this market now requires integrated smart-packaging ecosystems, scalable pharmaceutical-grade manufacturing, sustainability alignment, and the ability to deliver real-time traceability at global supply-chain scale.

AptarGroup, Inc.

Berry Global Group, Inc.

Sonoco Products Company

WestRock Company

CCL Industries Inc.

Sealed Air Corporation

Huhtamaki Oyj

Constantia Flexibles Group GmbH

Avery Dennison Corporation

Gerresheimer AG

West Pharmaceutical Services, Inc.

Schreiner Group GmbH & Co. KG

Bilcare Limited

The Pharmaceutical Active and Intelligent Packaging Market is rapidly transitioning toward digitally connected, sensor-enabled, and sustainability-focused packaging ecosystems designed to strengthen pharmaceutical integrity and logistics intelligence. RFID-enabled smart labels, NFC authentication systems, and AI-connected monitoring platforms are now deployed across more than 61% of specialty pharmaceutical distribution operations, improving shipment traceability efficiency by approximately 34%. Pharmaceutical manufacturers are increasingly integrating cloud-based monitoring platforms directly into packaging workflows to reduce cold-chain intervention delays and strengthen regulatory compliance visibility.

Active material science technologies are also advancing aggressively, particularly in oxygen-scavenging polymers, moisture-regulating films, and antimicrobial packaging systems. Dual-active barrier technologies improve pharmaceutical shelf stability by nearly 18% while reducing contamination risk during long-distance transportation. Compared with conventional passive blister systems, intelligent sensor-enabled packaging reduces manual inventory verification time by approximately 28% and significantly improves real-time shipment monitoring precision.

A major competitive shift is occurring around printable electronics and battery-free smart labels, which lower intelligent packaging deployment costs by nearly 22% compared with legacy embedded-chip architectures. Large pharmaceutical exporters and biologics manufacturers benefit most from these technologies due to their high exposure to temperature-sensitive logistics and serialization compliance requirements.

Between 2026 and 2028, packaging automation, blockchain-enabled authentication, and AI-driven predictive monitoring are expected to redefine pharmaceutical packaging execution models. Companies acting early on integrated smart-packaging infrastructure, recyclable active materials, and digitally connected compliance ecosystems are positioning themselves for stronger operational resilience, faster pharmaceutical traceability, and long-term supply-chain optimization advantage.

April 2025 – Amcor completed construction of its advanced healthcare coating facility in Malaysia, becoming the first company in Asia to produce both top and bottom substrates for medical device packaging using air knife coating technology. The facility reduces regional lead times and strengthens sterile packaging supply-chain resilience across Asia-Pacific healthcare markets. [Healthcare Coating Expansion] Source: www.amcor.com

July 2025 – Aptar Pharma commercialized its Freepod® nasal spray pump using 52% bio-based feedstock for Haleon’s Otrivin® brand, marking Aptar’s first globally deployed bio-based pharmaceutical delivery system. The innovation significantly reduces fossil-based resin dependency and accelerates sustainable pharmaceutical primary packaging adoption across respiratory healthcare applications. [Bio-Based Delivery Shift]

July 2025 – Aptar Pharma acquired Mod3 Pharma’s clinical trial materials manufacturing capabilities to strengthen Phase 1 and Phase 2 pharmaceutical support services. The acquisition expands Aptar’s integrated drug-delivery ecosystem and improves early-stage clinical packaging and fill-finish support for orally inhaled and nasal drug products. [Clinical Integration Expansion]

April 2024 – Berry Global expanded healthcare production capacity by up to 30% across three European manufacturing facilities to support rising pharmaceutical packaging and drug-delivery device demand. The investment strengthens patient-centric packaging scalability and accelerates deployment of advanced pharmaceutical packaging technologies across regulated healthcare supply chains. [European Capacity Scale-Up]

The Pharmaceutical Active and Intelligent Packaging Market Report delivers comprehensive analysis across active packaging technologies, intelligent monitoring systems, pharmaceutical applications, and end-user industries, covering both established and emerging packaging ecosystems. The report evaluates demand distribution across active barrier packaging, RFID-enabled intelligent packaging, track-and-trace systems, temperature-monitoring solutions, and connected pharmaceutical logistics technologies. Geographic analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with country-level strategic assessment focused on manufacturing concentration, pharmaceutical exports, regulatory infrastructure, and intelligent packaging deployment trends.

The report analyzes more than 12 major industry participants and evaluates over 20 operational and technology-level market indicators including adoption intensity, compliance integration, smart-packaging deployment rates, sustainability penetration, and pharmaceutical cold-chain modernization patterns. Intelligent packaging technologies now account for more than 38% of premium pharmaceutical logistics applications, while recyclable active-material integration has expanded by nearly 27% across regulated healthcare packaging operations.

From a strategic perspective, the report supports investment prioritization, expansion planning, supply-chain optimization, and competitive positioning decisions by identifying where intelligent packaging adoption is accelerating, where manufacturing capacity is regionalizing, and which technologies are redefining pharmaceutical compliance execution. Future-focused coverage from 2026–2033 highlights emerging opportunities in AI-enabled monitoring, printable electronics, blockchain traceability, and sustainable active-material innovation, enabling decision-makers to align long-term packaging strategies with evolving pharmaceutical distribution and regulatory transformation trends.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,349.0 Million |

| Market Revenue (2033) | USD 4,096.8 Million |

| CAGR (2026–2033) | 7.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Amcor Plc; AptarGroup, Inc.; Berry Global Group, Inc.; Sonoco Products Company; WestRock Company; CCL Industries Inc.; Sealed Air Corporation; Huhtamaki Oyj; Constantia Flexibles Group GmbH; Avery Dennison Corporation; Gerresheimer AG; West Pharmaceutical Services, Inc.; Schreiner Group GmbH & Co. KG; Bilcare Limited |

| Customization & Pricing | Available on Request (10% Customization Free) |