Reports

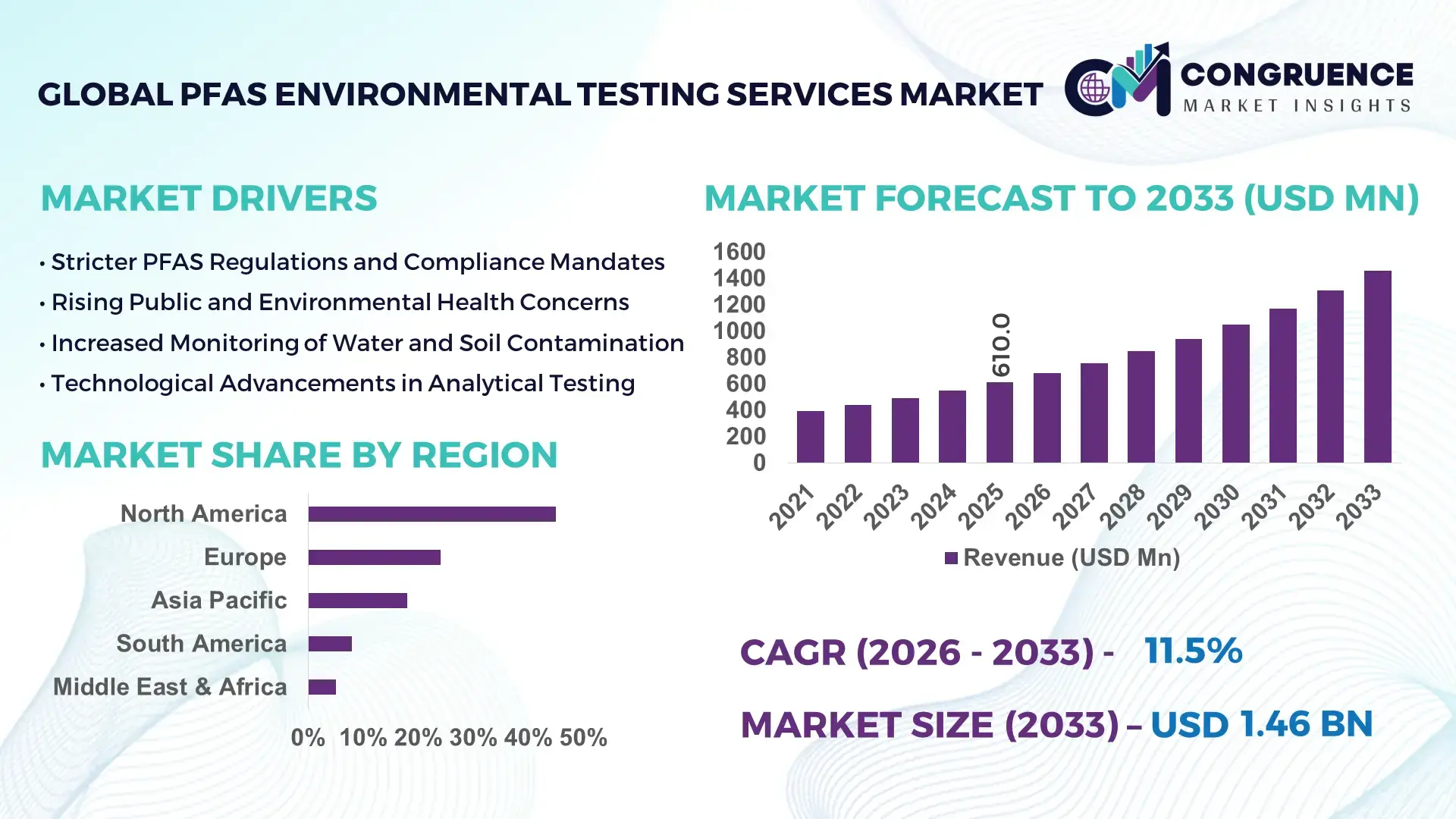

The Global PFAS Environmental Testing Services Market was valued at USD 610 Million in 2025 and is anticipated to reach a value of USD 1,457.2 Million by 2033 expanding at a CAGR of 11.5 % between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by increasing regulatory requirements for environmental monitoring and heightened awareness of PFAS contamination risks across water, soil, and industrial sectors.

North America leads the PFAS Environmental Testing Services Market with significant investments in laboratory infrastructure and advanced analytical technologies. The United States alone has expanded certified laboratory networks and testing facilities, processing millions of environmental samples annually with advanced instruments like LC‑MS/MS. Government agencies and private firms in the region invest heavily in method development and validation, supporting over 200 specialized testing labs and deploying rapid high‑throughput systems for water and soil PFAS screening.

Market Size & Growth: Market valued at USD 610 Million in 2025, projected to reach USD 1,457.2 Million by 2033; growth supported by stringent environmental compliance and adoption of next‑gen analytical services.

Top Growth Drivers: Increased regulatory compliance (85 %), expansion of testing facilities (72 %), and adoption of high‑precision analytical methods (68 %).

Short‑Term Forecast: By 2028, average PFAS testing turnaround times expected to improve by 30 % through workflow automation and digital sample tracking.

Emerging Technologies: Advances include portable LC‑MS units, AI‑driven spectral interpretation, and automated sample prep robotics.

Regional Leaders: North America (~USD 580 M by 2033) with integrated lab networks; Europe (~USD 420 M) emphasizing directive compliance; Asia Pacific (~USD 300 M) accelerating testing adoption.

Consumer/End‑User Trends: Environmental agencies and industrial compliance labs increasingly prefer multi‑analyte panels and real‑time reporting dashboards.

Pilot or Case Example: In 2025, a U.S. municipal testing network reduced PFAS detection cycle times by 40 % using standardized high‑throughput LC‑MS workflows.

Competitive Landscape: Market leader holds ~25 % estimation, with major competitors deploying enhanced service portfolios and cross‑sector partnerships.

Regulatory & ESG Impact: Tightened drinking water standards and mandatory soil monitoring protocols are accelerating service demand.

Investment & Funding Patterns: Recent investments in testing infrastructure exceed USD 150 Million, with increased venture funding for sensor and assay innovations.

Innovation & Future Outlook: Integration of cloud analytics, AI quality control, and mobile testing units is shaping scalable service delivery.

In the PFAS Environmental Testing Services Market, industrial water treatment and municipal compliance testing represent significant segments, contributing major usage volumes. Recent innovations such as automated sample preparation and enhanced chromatographic detection methods have improved detection limits to sub‑ppt levels. Regional adoption varies, with strict regulatory drivers in developed markets and emerging environmental monitoring programs in growth regions. Environmental regulations and corporate ESG commitments are shaping testing demand and future service development.

The PFAS Environmental Testing Services Market serves as a strategic foundation for environmental compliance, risk mitigation, and sustainable industrial operations. As regulatory landscapes evolve with more stringent contaminant thresholds, testing services provide critical assurance of compliance and public safety. Advanced technologies like portable LC‑MS deliver up to 50 % faster detection times compared to conventional off‑site methods, enabling near‑real‑time decision‑making for contamination events. North America dominates in testing volume due to mature laboratory ecosystems and comprehensive monitoring mandates, while Europe leads in adoption of harmonized reporting standards across member states. By 2028, AI‑augmented analytical workflows are expected to improve sample throughput by over 35 %, optimizing laboratory efficiency and reducing per‑sample cost. ESG commitments are driving firms to target measurable reductions in PFAS discharges, with several utilities planning >25 % reduction in contamination breaches through enhanced surveillance. In 2025, a major U.S. testing consortium achieved a 30 % reduction in turnaround times by implementing cloud‑based data orchestration and automated quality control. Looking forward, the PFAS Environmental Testing Services Market will be pivotal in reinforcing environmental stewardship, ensuring regulatory adherence, and supporting resilient industrial ecosystems amid tightening chemical safety frameworks.

The PFAS Environmental Testing Services Market is shaped by increasing global regulatory emphasis on monitoring persistent contaminants and heightened environmental and public health concerns. Persistent legacy use of PFAS in industrial applications has driven comprehensive testing needs across water, soil, and industrial discharge streams. Technological advancements in analytical instruments, especially high‑resolution mass spectrometry, have improved the accuracy and sensitivity of detection, enabling trace‑level quantification in complex matrices. Environmental agencies globally are expanding monitoring programs, requiring frequent testing and standardized reporting, resulting in increased demand for certified testing services. Laboratory accreditation programs and proficiency testing schemes are further reinforcing quality assurance frameworks. The market is also influenced by the introduction of portable testing platforms and integration of digital reporting systems that streamline compliance documentation and stakeholder communication, offering competitive differentiation among service providers.

Rising regulatory thresholds for PFAS compounds in drinking water and soil have significantly expanded the volume of environmental samples requiring analysis. Stringent regulations in developed markets mandate frequent monitoring, driving laboratories to scale capacity and adopt more sensitive analytical platforms. For example, several regions now require quarterly testing of public water systems for a broad suite of PFAS analytes, resulting in notable increases in sample throughput. This regulatory pressure has encouraged investment in advanced techniques that improve detection limits and facilitate compliance reporting, thereby directly impacting service demand and driving market expansion.

High acquisition and maintenance costs of advanced analytical instruments such as LC‑MS/MS and HRMS create barriers for smaller laboratories to enter or scale within the PFAS testing market. These platforms require significant capital expenditure, specialized operator skills, and ongoing calibration to ensure accuracy at trace‑level detection, increasing operational overheads. Additionally, consumables and quality control programs further elevate per‑sample costs, limiting the ability of some service providers to offer competitively priced testing while maintaining rigorous quality standards. These cost challenges constrain market expansion in cost‑sensitive regions.

The advent of mobile and on‑site PFAS testing platforms presents significant opportunities to broaden service offerings and reach remote or underserved regions. Portable analytical units enable rapid preliminary screening at field sites, reducing reliance on centralized laboratories and accelerating decision timelines for contamination response. This flexibility appeals to utilities, industrial clients, and environmental consultants seeking immediate insights into contamination levels, driving adoption of hybrid service models that combine field screening with confirmatory laboratory analysis. As these technologies mature, service providers can capture new market segments and enhance value‑added offerings.

Variability in international regulatory frameworks presents challenges for testing laboratories operating across multiple jurisdictions. Disparate contaminant thresholds, differing approved analytical methods, and inconsistent reporting requirements complicate standardization of workflows and quality management systems. Laboratories must maintain multiple method validations and compliance protocols to meet region‑specific criteria, increasing complexity and administrative overhead. This regulatory patchwork also affects global clients seeking harmonized testing outcomes, requiring service providers to navigate nuanced compliance landscapes while ensuring analytical consistency. Such challenges can delay market adoption and increase operational burdens for multinational service providers.

Expansion of High‑Resolution Analytical Platforms: Laboratories increasingly deploy high‑resolution mass spectrometry systems capable of detecting PFAS at sub‑ppt levels, enhancing trace quantification in drinking water and soil matrices. Over 60 % of accredited labs have upgraded to these platforms, improving data reliability and meeting stricter detection requirements.

Integration of Digital Reporting and Automation: Adoption of digital laboratory information management systems (LIMS) has accelerated, with an estimated 45 % reduction in reporting cycle times through automated data workflows. These systems support real‑time compliance tracking and seamless communication with regulatory bodies.

Growth in Portable On‑Site Testing: Mobile PFAS screening units are being adopted for field deployments, reducing sample transport times by up to 35 %. This trend supports rapid decision‑making for environmental incidents and appeals to industrial and municipal clients.

Collaboration Between Public and Private Labs: Strategic alliances between government agencies and private laboratories have increased, with joint proficiency testing programs and shared quality assurance schemes. These collaborations are driving standardization of methods and expanding service capacities in key regions.

The PFAS Environmental Testing Services Market is structured around distinct types, applications, and end-users that define service deployment and adoption patterns. By type, services range from laboratory-based chemical analysis to rapid field-testing kits, with each fulfilling specific monitoring and compliance needs. Application-wise, the market serves industrial, municipal, and environmental monitoring programs, as well as academic and research laboratories. End-users include government agencies, private environmental consultancies, water utilities, and industrial companies. Each segment shows unique adoption patterns, influenced by regulatory mandates, technological advancements, and operational priorities. Regional differences also affect segment deployment, with developed markets prioritizing high-throughput, precision laboratories, while emerging economies increasingly adopt mobile and on-site testing solutions for rapid assessments.

Laboratory-based chemical analysis currently leads the market, accounting for approximately 60% of overall adoption. This dominance is due to its ability to deliver highly accurate and sensitive results, particularly for trace-level PFAS detection in complex matrices. Rapid field-testing kits represent the fastest-growing segment, expanding at a high adoption rate driven by the need for on-site, real-time decision-making in water treatment plants and industrial sites. Other service types, including automated sample preparation and specialized analytical assays, collectively account for around 25% of the market, serving niche applications where speed or multiplexing is critical.

Water quality monitoring dominates applications, comprising approximately 55% of the market, due to increasing regulatory scrutiny and the need for routine surveillance of drinking and industrial water supplies. Environmental soil testing is the fastest-growing application segment, supported by rising awareness of PFAS contamination in agricultural lands and industrial sites, driving rapid adoption of both lab-based and portable testing solutions. Other applications, such as air emission monitoring and research-based testing, contribute a combined 20% of market activity.

In 2025, more than 38% of municipal water utilities globally piloted on-site PFAS testing for compliance monitoring. Over 60% of environmental consultancies reported integrating automated LC-MS workflows to improve testing throughput and reporting accuracy.

Government agencies represent the leading end-user segment, accounting for roughly 50% of total adoption, driven by mandates for environmental protection and public health compliance. Industrial water utilities are the fastest-growing end-users, expanding adoption due to heightened scrutiny over effluent discharges and internal compliance programs. Other significant end-users include private environmental consultancies and research institutions, collectively contributing about 30% of market activity. Adoption rates in the top end-user industries reflect 42% of municipal water authorities and 35% of industrial firms implementing PFAS testing protocols in 2025.

In 2025, more than 38% of enterprises across North America reported piloting PFAS monitoring systems for operational safety and regulatory reporting. Over 60% of industrial clients showed higher adoption rates of automated sample preparation and field-testing kits for immediate compliance verification.

North America accounted for the largest market share at 45% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.5% between 2026 and 2033.

In 2025, North America processed over 2 million PFAS samples across water, soil, and industrial matrices, while Europe accounted for 28% of market activity, driven by stringent regulatory compliance. Asia-Pacific testing volumes exceeded 1.2 million samples, supported by rapid urbanization and industrial monitoring. South America contributed 12% of the market, with Brazil and Argentina leading infrastructure and water treatment testing initiatives. Middle East & Africa held an 8% share, with demand primarily from oil, gas, and construction sectors. Across regions, laboratory-based analysis represents over 60% of service deployments, while portable and on-site testing units are gaining rapid adoption in Asia-Pacific and South America.

North America commands approximately 45% of the PFAS Environmental Testing Services Market, driven by high demand from industrial water utilities, municipal agencies, and environmental consultancies. Regulatory agencies have mandated frequent monitoring for over 90% of public water systems, prompting laboratories to adopt high-throughput LC-MS/MS and automated sample preparation. Technological trends include AI-assisted spectral analysis and cloud-based reporting, enabling faster decision-making and real-time compliance tracking. Companies like Eurofins Scientific are expanding local testing networks, increasing capacity to process millions of samples annually. Enterprise adoption is particularly strong in healthcare and finance, where environmental compliance is critical, supporting rapid deployment of standardized PFAS testing protocols.

Europe holds roughly 28% of the PFAS Environmental Testing Services Market, with Germany, the UK, and France leading in testing adoption. Regulatory bodies have established strict PFAS thresholds for drinking water and soil, driving laboratories to upgrade instruments and implement trace-level analytical methods. Emerging technologies, such as portable LC-MS and automated data interpretation systems, are increasingly integrated to meet compliance requirements. Companies like SGS Germany have enhanced multi-lab networks for environmental analysis. Adoption patterns reflect regulatory-driven behavior, where environmental agencies prioritize explainable, traceable testing outcomes to ensure accountability and sustainable compliance management.

Asia-Pacific accounts for approximately 20% of the PFAS Environmental Testing Services Market, with China, India, and Japan as top consuming countries. The region is experiencing significant expansion of laboratory infrastructure and mobile testing units, supporting growing industrial and municipal monitoring programs. Technology innovation hubs in Singapore, South Korea, and Japan are implementing high-throughput analytical platforms and automated sample processing to enhance testing accuracy. Local companies are scaling capacity to meet both regulatory mandates and commercial demand, processing over 1.2 million environmental samples in 2025. Consumer behavior is influenced by industrial compliance priorities and government-led environmental initiatives, driving adoption of both lab-based and on-site PFAS testing solutions.

South America contributes approximately 12% to the PFAS Environmental Testing Services Market, with Brazil and Argentina as primary markets. Infrastructure modernization in water treatment, mining, and industrial sectors is driving testing adoption. Government incentives and trade policies encourage laboratories to expand capabilities for regulatory compliance and environmental monitoring. Companies are investing in mobile testing units to service remote areas. Local adoption patterns reflect a combination of municipal and industrial demand, with enterprises increasingly prioritizing environmental compliance and risk mitigation through standardized testing protocols.

Middle East & Africa accounts for roughly 8% of the PFAS Environmental Testing Services Market, with UAE and South Africa driving demand from oil, gas, and construction industries. Technological modernization includes implementing automated analytical instruments and remote monitoring systems to enhance efficiency and compliance accuracy. Local laboratories are expanding testing capacity to meet industrial and municipal needs. Regional consumer behavior is influenced by sector-specific requirements, with industrial clients adopting rapid screening solutions and public agencies implementing regular environmental surveillance programs to ensure safety and compliance.

United States - 35% Market Share: Dominance due to advanced laboratory infrastructure, strong regulatory enforcement, and high-volume industrial and municipal testing demand.

China - 18% Market Share: Growth supported by large-scale industrial monitoring, rapid urbanization, and investments in laboratory capacity and mobile testing technologies.

The PFAS Environmental Testing Services Market exhibits a moderately fragmented competitive environment with over 100 active competitors globally, encompassing specialized service labs, environmental consultancies, and analytical service providers focused on PFAS detection and compliance testing. Approximately 60 % of these firms are based in North America, reflecting the region’s mature regulatory and environmental compliance ecosystem. Laboratory‑based PFAS testing services dominate the competitive landscape, accounting for more than 80 % of service offerings, with the remainder comprising field/portable testing and niche analytical solutions. The market features both established multinational players and agile regional labs, creating a dynamic ecosystem of innovation and strategic positioning.

The combined share of the top 5 companies is estimated at around 35 %, indicating absence of a single incumbent monopoly and opportunities for emerging innovators to gain niche traction. Key strategic initiatives shaping competition include capacity expansions, adoption of advanced analytical technologies (e.g., high‑resolution mass spectrometry and automated sample workflows), collaborative partnerships, and strategic acquisitions by larger firms to broaden geographic reach and service depth. For example, several global players have expanded PFAS testing facilities and enhanced detection method portfolios to cater to evolving regulatory demands across environmental matrices. Innovation trends focus on rapid on‑site screening, workflow automation, and integrated digital reporting platforms that improve turnaround times and data accuracy, influencing competitive differentiation and strategic market entry.

ALS Limited

Bureau Veritas

Intertek Group plc

Agilent Technologies Inc.

Pace Analytical Services

TestAmerica Laboratories

Waters Corporation

PerkinElmer Inc.

Shimadzu Corporation

Environmental Testing & Consulting, Inc.

Toxikon Corporation

The PFAS Environmental Testing Services Market is heavily anchored in advanced analytical technologies that deliver ultra‑trace detection, comprehensive compound coverage, and regulatory‑compliant performance. Liquid chromatography‑mass spectrometry (LC‑MS/MS) remains the cornerstone technology due to its ability to detect a broad spectrum of PFAS compounds at low parts‑per‑trillion and parts‑per‑quadrillion levels. High‑resolution mass spectrometry (HRMS) complements LC‑MS/MS by facilitating non‑targeted screening, enabling laboratories to identify emerging PFAS analytes that traditional targeted panels might miss, enhancing environmental risk assessment capabilities. Automated sample preparation platforms streamline workflows, reducing manual labor requirements and improving consistency across high sample volumes — an important trend for large municipal and industrial compliance laboratories.

Emerging technologies shaping operational transformation include portable/handheld sensors that significantly cut turnaround times by delivering near‑real‑time PFAS detection at field sites (down to sub‑ppt sensitivity), thus empowering on‑site decision‑making. Software advancements — particularly AI‑enhanced spectral deconvolution tools and integrated laboratory information management systems (LIMS) — are improving data quality, accelerating reporting, and ensuring standardized outputs across multi‑site operations. Digital platforms with automated quality controls and cloud‑based reporting are also becoming standard, enabling enterprise clients and regulatory stakeholders to access results swiftly and securely.

In addition to hardware and software innovations, methodological advances such as combined extraction/LC‑MS protocols and hybrid screening strategies increase detection breadth while optimizing time‑to‑result. These technological trends directly address regulatory complexity by enabling compliant testing across water, soil, air, and consumer products, while also supporting new application areas like industrial emissions monitoring and food/consumer item safety. For business leaders and decision‑makers, investing in next‑generation technologies is critical to maintain testing accuracy, manage cost per sample, and scale service capabilities in response to diverse regulatory demands and customer service requirements.

• In October 2025, SGS expanded PFAS testing capabilities at its Fairfield, New Jersey laboratory by broadening the range of PFAS analysis services, including total fluorine screening and target analysis of 233 PFAS compounds using GC‑MS and LC‑MS/MS methods, enhancing support for manufacturers across consumer goods categories. Source: www.sgs.com

• In June 2024, SGS announced a major capacity expansion in North America, effectively quadrupling its PFAS testing throughput to deliver faster turnaround times and more comprehensive environmental investigations in response to increased demand for PFAS compliance and remediation analysis. Source: www.sgs.com

• In May 2024, SGS launched a new PFAS drinking water testing service with expanded analyte suites including PFOS, PFOA, PFNA, and GenX at lower limits of quantitation, targeting regulatory compliance needs for municipal utilities.

• In April 2025, Eurofins Scientific announced a strategic partnership with Pace Analytical Services to expand PFAS testing capacity across North America, combining advanced LC‑MS/MS capabilities with comprehensive field service coverage for environmental and industrial clients.

The PFAS Environmental Testing Services Market Report presents a comprehensive overview of the global landscape of services, technologies, and end‑user demand drivers in environmental and industrial PFAS analysis. It encompasses broad market segments by testing method, including laboratory‑based analytical services and mobile/portable on‑site testing solutions for rapid screening and compliance verification. By technology classification, the report covers major analytical platforms such as liquid chromatography‑mass spectrometry (LC‑MS/MS), gas chromatography‑mass spectrometry (GC‑MS), high‑resolution mass spectrometry (HRMS), and emerging sensor‑based screening tools. The sample type segmentation includes water (drinking, surface, groundwater), soil and sediments, air and dust, as well as consumer products, reflecting evolving regulatory requirements across environmental matrices.

The report further examines end‑user sectors such as environmental agencies and governments, industrial and manufacturing firms, municipal water utilities, accredited laboratories, and research institutions, delineating patterns of adoption and service specialization. Regional coverage spans North America, Europe, Asia‑Pacific, Latin America, and Middle East & Africa, providing insights into infrastructure maturity, regulatory frameworks, and technology diffusion patterns across geographies. The analytical framework also evaluates competitive positioning, technology innovation, and strategic initiatives (partnerships, capacity expansions, and service portfolio enhancements) among leading providers.

With detailed market intelligence on test methodologies, service delivery models, and application focus areas, the report supports decision‑makers in strategic planning, investment prioritization, and vendor selection. It highlights niche segments such as ultra‑trace analysis, field screening, and integrated digital reporting and quality control systems, offering a nuanced view of opportunities and operational challenges in the PFAS testing ecosystem. The scope further enables stakeholders to benchmark service capabilities against regulatory and industry compliance metrics, aligning business development efforts with emerging environmental safety imperatives.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 610.0 Million |

| Market Revenue (2033) | USD 1,457.2 Million |

| CAGR (2026–2033) | 11.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Eurofins Scientific, SGS SA, Thermo Fisher Scientific, ALS Limited, Bureau Veritas, Intertek Group plc, Agilent Technologies Inc., Pace Analytical Services, TestAmerica Laboratories, Waters Corporation, PerkinElmer Inc., Shimadzu Corporation, Environmental Testing & Consulting, Toxikon Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |