Reports

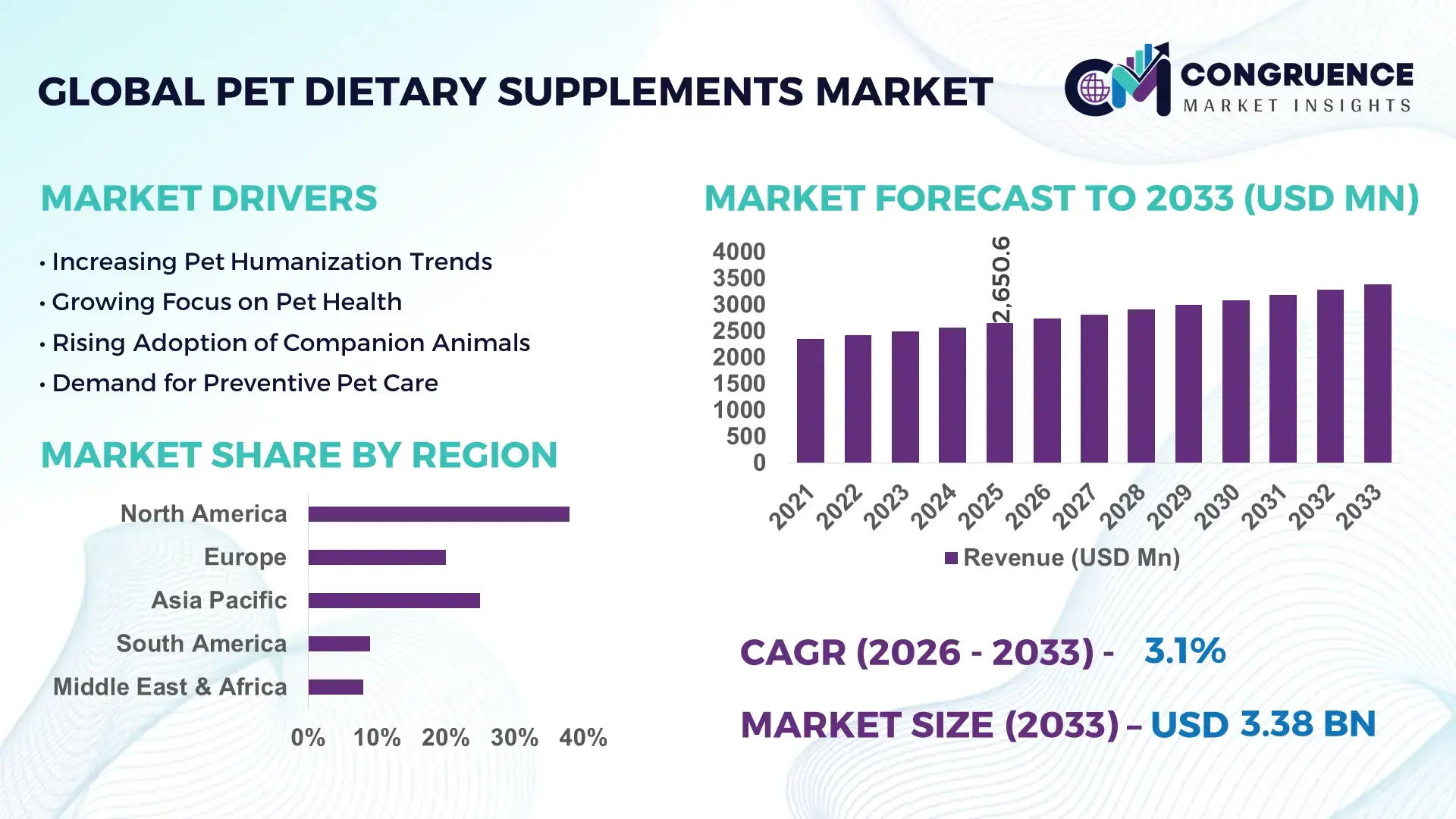

The Global Pet Dietary Supplements Market was valued at USD 2650.59 Million in 2025 and is anticipated to reach a value of USD 3383.86 Million by 2033 expanding at a CAGR of 3.1% between 2026 and 2033. Rising companion animal obesity rates, preventive veterinary care spending, and accelerated adoption of probiotic, joint-health, and omega-based formulations across premium pet food distribution channels are driving sustained expansion in the global pet dietary supplements industry.

The United States dominates the global pet dietary supplements market with approximately 34% share, supported by advanced pet healthcare infrastructure, over USD 2.4 billion annual pet wellness product spending, and strong penetration of functional nutrition products across retail and e-commerce channels. China is rapidly narrowing the gap through domestic manufacturing expansion and over 18% increase in pet ownership among urban households since post-pandemic lifestyle shifts. Europe maintains stable demand through regulated clean-label supplement adoption and sustainability-focused ingredient sourcing amid tightened cross-border supply chain controls linked to Red Sea shipping disruptions in 2026.

Companies prioritizing premium formulations, veterinary partnerships, and region-specific manufacturing capacity are positioned to secure stronger margin control and long-term competitive advantage.

Market Size & Growth: USD 2650.59 Million in 2025 reaching USD 3383.86 Million by 2033 at 3.1% growth, driven by premium probiotic and immunity-support product expansion.

Top Growth Drivers: Pet humanization contributes 31% demand growth, preventive veterinary spending 27%, and e-commerce subscription sales 22%.

Short-Term Forecast: By 2028, automated supplement packaging reduces operational costs by 14% while fulfillment efficiency improves 19%.

Emerging Technologies: AI-based pet nutrition analytics, microencapsulation, and precision probiotic delivery improve nutrient absorption rates by nearly 21%.

Regional Leaders: North America exceeds USD 1.1 billion supported by veterinary wellness adoption, Europe surpasses USD 820 million through clean-label demand, and Asia-Pacific approaches USD 900 million with urban pet ownership expansion.

Consumer/End-User Trends: More than 46% of premium pet owners purchase joint-health and digestive supplements through recurring digital subscriptions.

Pilot/Case Example: In 2026, a Japanese pet wellness manufacturer improved production efficiency by 17% using automated ingredient traceability systems.

Competitive Landscape: Leading multinational brands collectively control nearly 38% market share alongside Nestlé Purina, Mars Petcare, Virbac, Zoetis, and ADM.

Regulatory & ESG Impact: Sustainable marine-sourced omega ingredients reduced packaging and sourcing emissions by 12% across advanced pet wellness supply chains.

Investment & Funding: Global investments exceeded USD 780 million in 2026 through manufacturing expansion, strategic acquisitions, and veterinary nutrition partnerships.

Innovation & Future Outlook: Functional longevity supplements, CBD-alternative calming formulas, and personalized nutrition platforms are accelerating premium product differentiation strategies.

Pet dietary supplements are experiencing strong demand across digestive health, mobility support, skin wellness, and stress-management applications as advanced functional ingredients gain wider veterinary acceptance. Freeze-dried probiotics, algae-based omega blends, and personalized nutrition formulations improved repeat purchase rates by nearly 24% in premium retail channels during 2026. Regional ingredient localization and stricter labeling compliance standards are also reshaping procurement strategies, creating a more competitive environment for strategic product innovation and market positioning.

Pet dietary supplements are becoming strategically critical as pet healthcare shifts from reactive treatment toward preventive nutrition and condition-specific wellness management. Veterinary clinics, premium pet food manufacturers, and digital pet-care platforms are integrating supplements into recurring care ecosystems to improve customer retention and lifetime spending. The market is also benefiting from ingredient supply-chain restructuring, particularly in omega oils, probiotics, and plant-derived actives, as manufacturers reduce dependence on single-country sourcing after logistics disruptions across Red Sea trade corridors in 2026.

Advanced microencapsulation and precision blending technologies are improving nutrient stability by nearly 28% compared to conventional powder formulations while reducing ingredient waste by 16% during manufacturing. The United States leads in veterinary-backed supplement deployment and subscription-based wellness programs, whereas Japan and South Korea are advancing compact functional formulations for aging pets in urban households. Over 41% of premium pet supplement launches in 2026 included customized formulations linked to breed size, age, or digestive sensitivity.

Manufacturers are expanding localized production partnerships and cold-chain ingredient capabilities to secure faster retail replenishment and regulatory compliance. In Germany, automated traceability platforms reduced batch verification time by 22% across functional pet nutrition facilities. Over the next two to three years, companies prioritizing formulation science, digital pet-health integration, and diversified sourcing networks will strengthen operational resilience and premium market positioning.

Rising integration of preventive nutrition into veterinary care models is accelerating demand for functional pet dietary supplements across mobility, digestive, and immunity categories. More than 52% of urban pet owners in the United States now purchase at least one condition-specific supplement annually, while veterinary recommendation rates for joint-health formulations increased by 19% during 2026. Expanding companion animal obesity levels and aging pet populations are strengthening long-term consumption patterns. China and Brazil are also experiencing rapid premiumization of pet wellness portfolios through e-commerce-driven distribution. In response, manufacturers are investing in clinically validated probiotic blends, veterinary partnerships, and personalized nutrition platforms. A notable operational shift involves direct-to-consumer subscription models, which improved repeat purchase retention by nearly 24%, enabling companies to stabilize inventory planning and strengthen recurring revenue channels.

Volatility in marine-derived omega ingredients, probiotics, and specialty proteins is creating sustained cost pressure across pet dietary supplement manufacturing. Fish oil input prices fluctuated by nearly 18% in 2026 due to tightening export controls and climate-linked supply constraints affecting Peru and Nordic fisheries. Simultaneously, stricter labeling and formulation verification requirements in the European Union increased compliance testing costs by approximately 14% for mid-sized manufacturers. These pressures are compressing margins, particularly for companies dependent on imported active ingredients and fragmented contract manufacturing networks. To reduce operational exposure, producers in the United States and Thailand are expanding localized ingredient sourcing and long-term procurement agreements. Several firms are also shifting toward algae-based omega alternatives and automated formulation tracking systems to improve traceability and reduce dependency on volatile marine supply chains.

Breed-specific supplementation, AI-enabled nutrition tracking, and microbiome-based formulations are creating high-value expansion opportunities across advanced pet wellness ecosystems. More than 37% of premium pet owners in Japan and South Korea actively use digital pet-health applications linked to nutrition monitoring and supplement recommendations. Personalized supplement packs generated approximately 21% higher repeat order frequency compared to standard formulations during 2026. Companies are increasingly investing in precision probiotic technologies, smart dispensing systems, and veterinary telehealth partnerships to strengthen customer retention and data-driven product development. India is emerging as a strategic manufacturing and formulation hub due to lower production costs and expanding nutraceutical capabilities. A key non-obvious opportunity lies in integrating wearable pet health data with supplement subscription models, enabling manufacturers to improve dosage personalization while reducing inventory forecasting inefficiencies across direct-to-consumer channels.

Scaling clinically validated pet dietary supplements across multiple markets remains a major operational challenge due to fragmented regulatory standards, formulation inconsistencies, and manufacturing complexity. Nearly 29% of new supplement formulations launched in 2026 required reformulation adjustments to meet country-specific ingredient thresholds and labeling protocols. Stability issues linked to probiotics and bioactive compounds also increase cold-chain dependency and raise logistics costs by approximately 12% in long-distance distribution networks. In the United States, veterinary scrutiny around efficacy claims is intensifying pressure for documented clinical outcomes and standardized testing protocols. Companies must also address shortages of formulation specialists and pet nutraceutical researchers to maintain product differentiation. To sustain competitiveness, manufacturers are investing in automated quality-control systems, regional testing laboratories, and strategic research collaborations focused on bioavailability optimization and long-term formulation stability.

• Precision Nutrition Product Scaling Personalized pet supplement deployment accelerated during 2026 as over 39% of premium pet owners in the United States adopted breed-specific or age-targeted formulations. Companies are integrating AI-driven nutrition profiling and microbiome testing into subscription wellness platforms, reducing customer churn by nearly 18%. Manufacturers in Japan expanded small-batch automated production systems to improve formulation flexibility and shorten customized product lead times by 21%, strengthening premium product differentiation and inventory responsiveness.

• Localized Ingredient Supply Expansion Supply-chain restructuring is shifting sourcing strategies toward localized nutraceutical inputs and alternative omega ingredients. European manufacturers reduced marine-oil dependency by approximately 16% through algae-based formulations after continued logistics pressure across Red Sea shipping routes. Thailand and India expanded probiotic fermentation capacity to stabilize raw material access and reduce import exposure. Companies are also increasing multi-supplier procurement agreements and automated traceability systems to improve compliance efficiency and ingredient verification speed.

• Veterinary Channel Integration Growth Veterinary clinics are becoming operational distribution hubs for condition-specific supplements, particularly in digestive and mobility categories. More than 44% of veterinary practices in Germany integrated digital supplement recommendation systems into preventive care workflows during 2026. This transition improved repeat treatment adherence by nearly 23% while strengthening clinic-margin performance. Companies are responding through veterinary partnerships, clinician education programs, and co-branded wellness formulations aligned with long-term pet care plans.

• Functional Format Innovation Surge Advanced delivery formats including soft chews, liquid sachets, and encapsulated powders are reshaping consumption behavior and manufacturing priorities. Soft chew adoption increased by 27% among aging pet households due to higher compliance rates and easier administration. South Korean manufacturers deployed moisture-resistant packaging technologies that extended probiotic shelf stability by 19% during cross-border distribution. Firms are scaling automated packaging lines and investing in palatability-focused R&D to improve retention rates and operational efficiency across premium retail channels.

Joint Supplements remain the leading segment within the pet dietary supplements market due to rising aging pet populations, increased mobility disorders, and strong veterinary endorsement across preventive care programs. Nearly 48% of senior dog supplement purchases in the United States during 2026 were linked to glucosamine and chondroitin-based mobility products. Their dominance is reinforced by high repeat-purchase frequency, broad retail availability, and integration into veterinary wellness subscriptions. Companies are expanding clinical validation programs and premium chewable formats to strengthen customer retention and pricing power.

Probiotics represent the fastest-growing type as digestive health management becomes operationally linked to immunity and nutrient absorption efficiency. Premium probiotic formulations recorded approximately 26% higher online conversion rates than conventional vitamin blends in Japan and South Korea. Omega Fatty Acids continue gaining traction through skin-health positioning and sustainable algae-based sourcing strategies, while Vitamins maintain stable demand through multinutrient daily wellness products. Protein Supplements are increasingly used in recovery and weight-support applications for active pets. Manufacturers are prioritizing microbiome science partnerships, functional ingredient acquisitions, and automated formulation technologies to secure long-term differentiation across specialized nutrition portfolios.

Digestive Health dominates the application landscape as veterinarians increasingly connect gut microbiome balance with immunity, nutrient utilization, and chronic condition management. More than 43% of pet supplement buyers in Germany and the United States prioritized digestive-support products during 2026, particularly probiotic and prebiotic combinations targeting recurring gastrointestinal sensitivity. Companies are scaling automated probiotic production systems and subscription-based replenishment models to stabilize recurring demand and improve customer retention. Strong integration with preventive veterinary care programs continues strengthening deployment consistency across premium retail and clinic channels.

Weight Management is emerging as the fastest-growing application due to rising pet obesity levels and increased monitoring through connected pet-health ecosystems. Smart feeding integrations and AI-enabled activity tracking improved supplement adherence rates by approximately 22% in digitally connected pet households across Japan. Joint Health remains strategically important among aging companion animals, while Skin and Coat Care continues expanding through omega-based formulations and clean-label ingredient positioning. Immunity Support products are also benefiting from heightened preventive health awareness and stress-management supplementation trends. Companies are expanding personalized wellness bundles and cross-category formulations to strengthen operational scale and premium product positioning.

Pet Owners represent the dominant end-user group due to rising direct-to-consumer purchasing behavior, expanding premium pet wellness awareness, and higher adoption of recurring supplement routines. Approximately 57% of supplement transactions in the United States during 2026 originated through independent consumer purchasing rather than clinical recommendation channels. Growing digital engagement and personalized nutrition marketing are enabling manufacturers to strengthen retention through subscription delivery models and customized wellness packs. Companies are increasingly targeting urban multi-pet households with tailored formulations and loyalty-driven pricing strategies to improve repeat purchasing frequency.

Online Retailers are the fastest-growing end-user segment as digital pet-care ecosystems accelerate convenience-driven purchasing and automated replenishment. Online supplement sales in China increased by nearly 29% during 2026 following expansion of veterinary e-commerce integration and same-day fulfillment infrastructure. Veterinary Clinics and Animal Hospitals continue influencing premium product credibility through preventive care recommendations, while Pet Specialty Stores maintain relevance through experiential merchandising and high-margin wellness portfolios. Pet Care Companies are also strengthening ecosystem partnerships with nutrition brands to integrate supplements into broader pet wellness services. Competitive positioning is increasingly shifting toward omnichannel distribution efficiency and data-driven customer retention systems.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.6% between 2026 and 2033.

Veterinary Wellness Ecosystems Strengthen Premium Supplement Demand

North America maintains leadership in the pet dietary supplements market through advanced veterinary infrastructure, premium pet nutrition spending, and strong penetration of subscription-based wellness products. The region contributes nearly 38% of global deployment volume, supported by widespread adoption of condition-specific supplements for digestive health and mobility care. More than 46% of premium pet households in the United States integrated at least one daily supplement regimen during 2026. Companies are expanding automated manufacturing and traceability systems to improve formulation consistency and regulatory compliance. Strategic partnerships between veterinary clinics and digital pet-health platforms are also accelerating personalized supplement recommendations, while localized ingredient sourcing investments are helping manufacturers reduce logistics exposure and maintain supply continuity.

United States Market Outlook: The United States remains the operational center of the regional market due to large-scale veterinary networks, advanced nutraceutical manufacturing capacity, and strong direct-to-consumer distribution infrastructure. More than 52% of online pet wellness purchases in 2026 included recurring supplement subscriptions linked to personalized nutrition plans. Domestic manufacturers are increasing investment in microbiome research, functional chew technologies, and AI-driven pet wellness analytics to strengthen retention rates and premium pricing strategies across competitive retail and clinical channels.

Clean-Label Compliance Reshapes Product Development

Europe is advancing through regulatory-driven product modernization, sustainable ingredient sourcing, and strong demand for clean-label pet nutrition formulations. Germany, France, and the United Kingdom collectively represent over 61% of regional supplement deployment activity due to mature veterinary wellness adoption and stricter product verification frameworks. European manufacturers increased algae-based omega integration by approximately 17% during 2026 to reduce dependence on volatile marine sourcing channels. Companies are investing in automated traceability systems, low-emission packaging formats, and regional ingredient partnerships to align with tightening sustainability and labeling standards. Functional digestive supplements and hypoallergenic formulations are gaining operational importance as premium pet ownership rises across urban households.

Germany Market Outlook: Germany leads the European market through strong veterinary infrastructure, advanced formulation research, and highly regulated pet nutrition standards. More than 44% of premium supplement launches in 2026 featured clinically positioned digestive or mobility formulations targeting aging pets. Domestic manufacturers are prioritizing recyclable packaging systems, precision probiotic technologies, and localized ingredient procurement to improve compliance efficiency and reduce long-term sourcing risk across high-value pet wellness portfolios.

Manufacturing Expansion Accelerates Regional Scale

Asia-Pacific is emerging as the fastest-scaling market due to rising urban pet ownership, expanding nutraceutical manufacturing infrastructure, and rapid digital retail adoption. China, Japan, and South Korea account for nearly 68% of regional premium supplement consumption, supported by growing demand for functional digestive and immunity-support products. Automated formulation facilities in Southeast Asia improved production throughput by approximately 23% during 2026 as manufacturers responded to increasing export demand. Companies are also expanding cross-border e-commerce partnerships and localized packaging operations to improve delivery speed and product accessibility. Breed-specific supplementation and compact dosage formats are becoming key operational priorities across densely populated urban markets.

China Market Outlook: China is strengthening its position through expanding domestic pet-care manufacturing, aggressive e-commerce integration, and rising premiumization of companion animal wellness products. Online supplement transactions increased by nearly 31% during 2026 following same-day fulfillment expansion across major metropolitan centers. Local companies are investing in smart manufacturing systems, personalized nutrition technologies, and veterinary retail partnerships to strengthen product differentiation and reduce dependency on imported pet wellness formulations.

Premium Pet Nutrition Adoption Expands

South America is experiencing rising adoption of pet dietary supplements through premium pet food expansion, urbanization, and increasing preventive veterinary care awareness. Brazil accounts for the largest share of regional demand due to strong companion animal ownership and growing penetration of functional pet wellness products across specialty retail channels. During 2026, regional distributors expanded localized warehousing capacity by approximately 14% to reduce import-related delays and stabilize inventory availability. Companies are increasingly targeting mobility-support and skin-health categories through cost-optimized formulations and veterinary partnerships. However, currency volatility and uneven cold-chain logistics continue limiting scalability for premium probiotic and omega-based products in several secondary markets.

Brazil Market Outlook: Brazil dominates the regional landscape through large-scale pet ownership, expanding veterinary service networks, and growing domestic nutraceutical production capabilities. More than 37% of premium pet supplement purchases in 2026 originated from urban households seeking preventive digestive and mobility care solutions. Manufacturers are investing in regional blending facilities, localized ingredient sourcing, and flexible pricing strategies to improve accessibility while maintaining product consistency across fragmented retail distribution networks.

Urban Pet Care Modernization Drives Demand

The Middle East & Africa market is evolving through rising premium pet ownership, expanding veterinary infrastructure, and increasing investment in modern pet-care retail ecosystems. Gulf countries account for a significant share of regional premium supplement consumption due to higher disposable income levels and growing demand for imported functional nutrition products. In 2026, veterinary wellness chains across the United Arab Emirates expanded digital consultation and supplement delivery integration by nearly 18%, improving customer retention and recurring product purchases. Companies are strengthening regional distribution partnerships and climate-controlled storage infrastructure to support stable deployment of probiotic and omega-based formulations in high-temperature operating environments.

United Arab Emirates Market Outlook: The United Arab Emirates is emerging as the region’s strategic premium pet wellness hub due to advanced retail infrastructure, rising veterinary investment, and strong demand for imported high-value supplements. More than 41% of urban pet owners purchasing premium nutrition products in 2026 preferred personalized wellness bundles linked to digital pet-care applications. Companies are expanding localized warehousing, veterinary partnerships, and omnichannel delivery systems to improve product accessibility and support high-margin wellness positioning across affluent consumer segments.

The pet dietary supplements market is led by global nutrition specialists competing directly with veterinary healthcare companies, premium pet wellness brands, and fast-scaling digital-first supplement providers. Nestlé Purina, Mars Petcare, ADM, Virbac, Zoetis, and Nutramax Laboratories collectively control nearly 42% of premium product distribution through veterinary networks and branded retail ecosystems. Competition centers on formulation science, supply-chain reliability, ingredient traceability, and personalized nutrition deployment rather than price alone. Advanced probiotic formulations improved premium product retention by approximately 21%, while automated fulfillment systems reduced subscription delivery costs by nearly 15% across direct-to-consumer channels. Companies are expanding through veterinary partnerships, regional manufacturing localization, and microbiome-focused acquisitions to secure ingredient access and accelerate product differentiation. Consolidation is increasing as clinically validated supplement portfolios gain stronger regulatory preference. Entry barriers remain high due to formulation compliance requirements, clinical testing expectations, and premium ingredient sourcing complexity. Companies succeeding in this market combine scalable manufacturing, scientific credibility, omnichannel distribution, and operational agility.

Nestlé Purina PetCare

Mars Petcare

ADM

Virbac

Zoetis

Nutramax Laboratories

Zesty Paws

Vetoquinol

NOW Foods

PetHonesty

Nordic Naturals

Swedencare

NaturVet

Animal Essentials

Microencapsulation, precision probiotic stabilization, and AI-enabled formulation analytics are becoming core technologies across the pet dietary supplements market between 2026 and 2028. More than 43% of premium supplement manufacturers now use controlled-release encapsulation systems to improve probiotic survivability and nutrient absorption. Automated blending and moisture-control systems reduced formulation variability by nearly 18% compared to conventional batch processing. Companies deploying integrated manufacturing execution platforms are also lowering production downtime by approximately 14%, strengthening inventory consistency and accelerating premium product launches across veterinary and retail channels.

Emerging technologies are reshaping formulation customization and deployment efficiency. AI-driven pet nutrition platforms improved personalized supplement recommendation accuracy by nearly 26% compared to rule-based legacy wellness systems. Digital microbiome analysis tools are gaining traction in Japan and the United States, where over 31% of advanced pet wellness brands integrated microbiome-based product development during 2026. Smart packaging with QR-linked dosage tracking is also improving customer adherence and subscription retention rates, creating operational advantages for digitally integrated supplement providers.

Disruptive technologies including strain-specific canine probiotics, algae-derived omega alternatives, and automated precision dosing are redefining competitive positioning. New-generation probiotic stabilization systems extended shelf-life performance by nearly 22% over traditional powder formats. Companies investing early in formulation science, digital wellness ecosystems, and localized smart manufacturing infrastructure are expected to secure stronger premium positioning and faster product scalability through 2028.

February 2026 – Vitaquest International opened a new probiotics manufacturing suite in New Jersey featuring two blending rooms and four encapsulation rooms, increasing probiotics production capacity by 100% while strengthening formulation flexibility and regulatory-grade quality control for premium pet supplement brands. Source: https://vitaquest.com

January 2026 – Zesty Paws expanded into veterinary-exclusive distribution with its Professional supplement line, introducing canine-native probiotic formulations shown to support digestive balance within 7 days. The move strengthened clinical channel penetration and expanded partnerships with veterinary wellness networks nationwide.

May 2026 – Bimini Pet Health expanded its Topeka manufacturing facility through a 2,300-square-foot operational addition designed to improve workflow efficiency and increase production scalability. The expansion supports higher supplement throughput, additional hiring, and stronger private-label manufacturing responsiveness for wellness brands. Source: https://www.petfoodprocessing.net

April 2026 – IFF launched PureStrong™, a canine-specific probiotic platform designed around targeted microbiome strains instead of generic multi-strain formulations. The technology enabled lower-dose precision formulations and improved digestive performance consistency, strengthening science-backed differentiation within advanced functional pet nutrition portfolios.

The Pet Dietary Supplements Market Report delivers detailed analysis across functional nutrition categories including Vitamins, Probiotics, Omega Fatty Acids, Joint Supplements, and Protein Supplements, with strategic assessment of applications such as Digestive Health, Immunity Support, Joint Health, Skin and Coat Care, and Weight Management. The study evaluates demand concentration across Veterinary Clinics, Pet Owners, Online Retailers, Animal Hospitals, and Pet Specialty Stores while covering operational trends across North America, Europe, Asia-Pacific, South America, and Middle East & Africa. More than 40% of premium product launches analyzed within the report are linked to microbiome-focused or personalized nutrition technologies.

The report also examines manufacturing modernization, precision formulation systems, smart packaging integration, and supply-chain localization strategies shaping industry competition between 2026 and 2033. It highlights deployment shifts including automated production, subscription-based wellness models, and veterinary digital integration, while evaluating strategic positioning of leading manufacturers, ingredient suppliers, and functional nutrition innovators supporting long-term investment planning and competitive expansion decisions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 2650.59 Million |

|

Market Revenue in 2033 |

USD 3383.86 Million |

|

CAGR (2026 - 2033) |

3.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Nestlé Purina PetCare, Mars Petcare, ADM, Virbac, Zoetis, Nutramax Laboratories, Zesty Paws, Vetoquinol, NOW Foods, PetHonesty, Nordic Naturals, Swedencare, NaturVet, Animal Essentials |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |