Reports

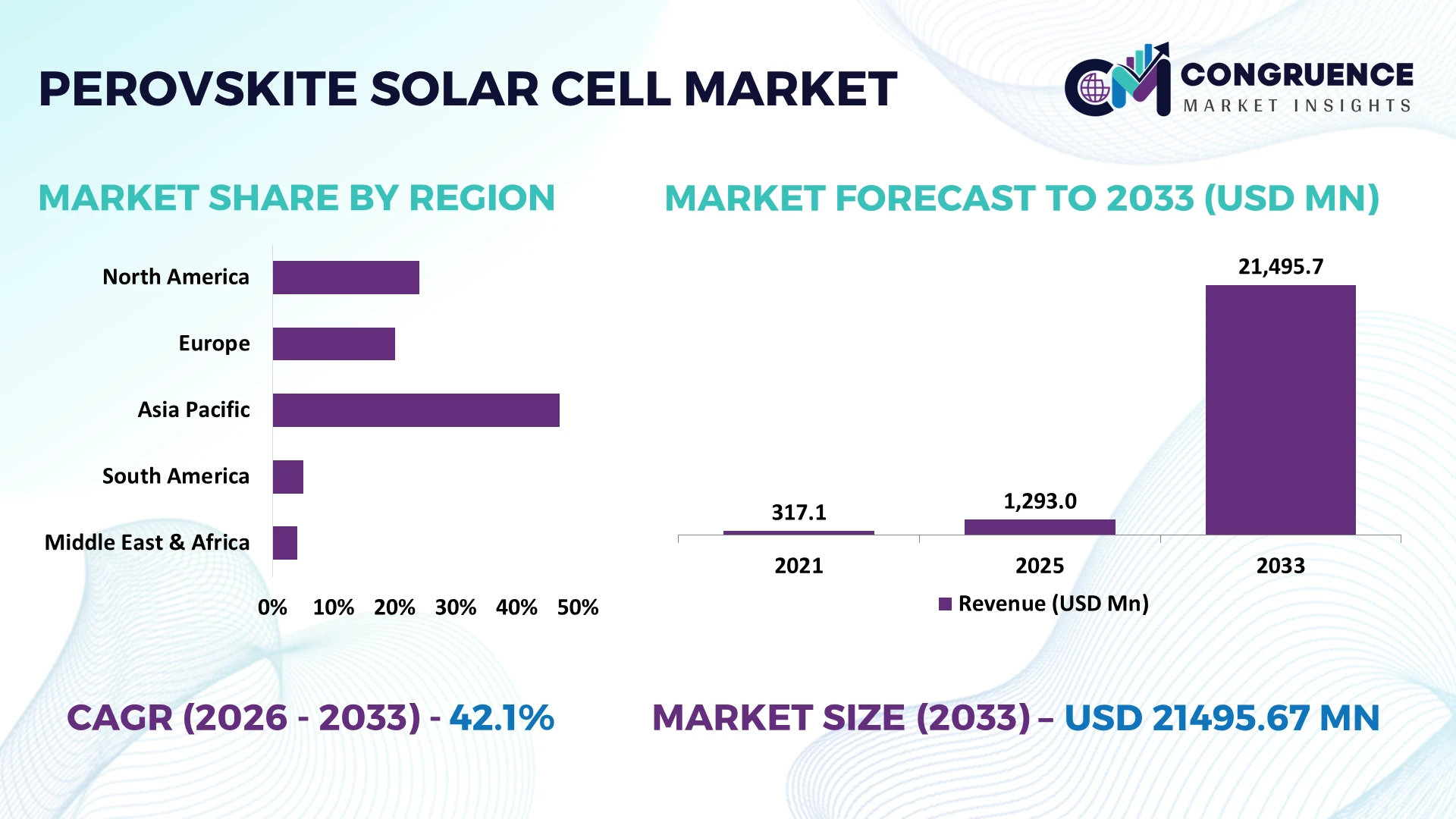

The Global Perovskite Solar Cell Market was valued at USD 1293 Million in 2025 and is anticipated to reach a value of USD 21495.67 Million by 2033 expanding at a CAGR of 42.1% between 2026 and 2033. Rapid commercialization of tandem solar modules, accelerated pilot-scale manufacturing, improved material stability, and government-backed clean energy deployment programs are strengthening large-scale adoption across utility, building-integrated photovoltaic, and next-generation energy applications.

China leads the global Perovskite Solar Cell Market with over 45% of pilot manufacturing capacity, supported by multi-billion-dollar clean energy investments and strong electronics manufacturing capabilities, while Germany remains a technology leader through advanced research commercialization. Following post-2025 global supply-chain diversification, Japan continues expanding high-efficiency photovoltaic deployment, with certified tandem cell efficiencies exceeding 33%, reinforcing competitive technology advancement across major economies.

Strategic investments in scalable manufacturing, efficiency enhancement, and resilient material supply chains will determine long-term competitive positioning.

Market Size & Growth: USD 1293 million in 2025, reaching USD 21495.67 million by 2033 at 42.1% CAGR, driven by tandem solar commercialization and advanced photovoltaic manufacturing.

Top Growth Drivers: Cell efficiency exceeds 33%, manufacturing costs decline nearly 30%, and renewable capacity additions continue expanding above 15% annually.

Short-Term Forecast: By 2028, module production costs decline about 25% while commercial conversion efficiency improves by approximately 12%.

Emerging Technologies: AI-assisted material discovery, automated roll-to-roll manufacturing, and tandem silicon-perovskite architectures accelerate industrial scalability.

Regional Leaders: Asia-Pacific exceeds USD 9800 million, Europe approaches USD 5600 million, and North America surpasses USD 4200 million, supported by localized manufacturing expansion.

Consumer/End-User Trends: More than 40% of emerging commercial projects prioritize lightweight, high-efficiency photovoltaic solutions for buildings and distributed energy systems.

Pilot/Case Example: In 2026, industrial tandem module demonstrations delivered over 20% higher energy output than conventional single-junction alternatives.

Competitive Landscape: Leading manufacturers collectively account for nearly 38% of commercialization activity, with Oxford PV, Microquanta, Saule Technologies, GCL, and UtmoLight advancing production.

Regulatory & ESG Impact: Carbon-reduction policies support renewable deployment targets above 50% across several major economies, accelerating advanced solar investments.

Investment & Funding: Industry investment exceeds USD 4 billion through strategic partnerships, pilot manufacturing expansion, and technology commercialization despite global supply-chain realignment.

Innovation & Future Outlook: Stable encapsulation materials, scalable printing processes, and tandem module integration strengthen the next phase of global high-growth photovoltaic deployment.

Perovskite Solar Cell Market demand is expanding across utility-scale solar farms, building-integrated photovoltaics, portable electronics, and industrial energy systems as manufacturers prioritize high-efficiency tandem technologies. Recent advances in material stability have extended operational performance by more than 20%, while localized manufacturing initiatives and evolving clean-energy regulations strengthen supply resilience, setting the foundation for the strategic market assessment that follows.

The Perovskite Solar Cell Market has become strategically important as governments and manufacturers seek faster deployment of high-efficiency photovoltaic technologies while reducing dependence on conventional silicon supply chains. Supply-chain restructuring since 2025 has accelerated localized manufacturing, while energy infrastructure modernization is encouraging utilities and industrial users to evaluate lightweight, high-output solar modules that shorten installation timelines and improve energy density across commercial projects.

Perovskite-silicon tandem cells now achieve certified conversion efficiencies above 33%, compared with approximately 26–27% for mainstream crystalline silicon technologies, enabling more electricity generation from the same installation footprint. China continues expanding pilot manufacturing capacity and industrial-scale commercialization, whereas Germany concentrates on research-driven innovation and premium module development. Over the next two to three years, automated coating processes are expected to reduce production waste by nearly 20%, while pilot manufacturing utilization rates are projected to exceed 70% as commercial deployment expands.

Building-integrated photovoltaic projects increasingly incorporate perovskite modules because of their lightweight characteristics and architectural flexibility, prompting manufacturers to strengthen technology partnerships, scale pilot production, and secure localized material sourcing. Companies prioritizing manufacturing consistency, durability improvements, and strategic ecosystem collaboration will establish stronger competitive positioning as advanced photovoltaic technologies transition from demonstration projects to commercial-scale deployment.

Tandem perovskite-silicon architectures are transforming photovoltaic manufacturing by increasing energy yield while reducing module weight and material consumption. Certified cell efficiencies exceeding 33% and manufacturing cost reductions approaching 30% compared with early pilot processes are accelerating commercial interest. China continues expanding dedicated pilot production facilities, while Japan is increasing investment in advanced encapsulation technologies to improve operational stability. These developments enable manufacturers to address utility-scale, building-integrated, and industrial energy applications simultaneously. In response, leading companies are expanding production partnerships, investing in automated fabrication lines, and strengthening intellectual property portfolios to secure early commercial leadership. The strategic advantage increasingly depends on scalable manufacturing quality rather than laboratory efficiency records alone.

Long-term durability remains a structural limitation because perovskite materials are highly sensitive to moisture, heat, and ultraviolet exposure under demanding operating environments. Performance degradation of more than 10% under accelerated stress conditions still affects commercialization timelines, while manufacturing yield losses of approximately 15% increase production costs during pilot-scale operations. The United States and several European manufacturers continue tightening product qualification requirements, extending certification timelines before utility deployment. To reduce operational risk, companies are localizing critical material sourcing, adopting advanced encapsulation systems, and negotiating long-term supply agreements for specialty chemicals. Success increasingly depends on manufacturing consistency and product reliability rather than achieving peak laboratory performance.

Flexible photovoltaic modules create significant opportunities beyond conventional utility installations by enabling energy generation across buildings, transportation infrastructure, and portable power systems. Lightweight module designs reduce installation loads by nearly 40%, while automated roll-to-roll manufacturing has demonstrated production throughput improvements exceeding 25%. South Korea and Singapore are actively supporting smart-building deployment through clean-energy innovation initiatives, creating favorable commercialization environments. Manufacturers are expanding research partnerships with construction firms and electronics companies to accelerate integrated product development. A strategic opportunity lies in combining digital energy management platforms with advanced perovskite modules, allowing customers to optimize distributed generation and operational efficiency across commercial assets.

Transitioning from pilot production to gigawatt-scale manufacturing remains the industry's most significant execution challenge. Process variability across coating, crystallization, and encapsulation stages can reduce production yields by 12–18%, while maintaining uniform cell performance across large substrates requires advanced process control systems. Industrial manufacturers in China and Germany continue investing in automated quality inspection and inline monitoring to improve production consistency. Without standardized manufacturing protocols, large-scale procurement by utilities and infrastructure developers remains constrained. Companies must accelerate automation, workforce specialization, equipment standardization, and cross-industry technology partnerships to establish dependable manufacturing ecosystems capable of supporting long-term commercial deployment and maintaining competitive operational performance.

Advanced Tandem Module Scaling Certified tandem cell efficiencies now exceed 33%, while pilot manufacturing yields have improved by nearly 18% through automated deposition and quality-control systems. China's industrial expansion and tighter performance qualification standards are accelerating commercialization, prompting manufacturers to increase production capacity, strengthen technology alliances, and standardize fabrication processes to improve operational consistency.

Localized Material Supply Networks Supply-chain diversification has reduced dependence on single-country specialty material sourcing, with localized procurement increasing by approximately 25% and logistics lead times declining nearly 15%. Manufacturing companies are restructuring supplier ecosystems and establishing regional processing partnerships, improving production continuity while minimizing disruptions caused by evolving trade policies and strategic material security initiatives.

Building Integration Accelerates Building-integrated photovoltaic deployment is expanding as lightweight perovskite modules reduce structural loading by almost 40% while installation productivity improves by approximately 20%. Japan and South Korea continue supporting advanced building-energy programs, encouraging module developers to collaborate with construction firms, optimize product certification, and develop customized architectural photovoltaic solutions for commercial infrastructure.

Digital Manufacturing Intelligence Artificial intelligence-enabled inspection platforms now reduce production defects by nearly 22%, while predictive maintenance improves equipment availability by roughly 16%. Rather than expanding workforce-intensive production, manufacturers increasingly automate inline process monitoring and material optimization, enabling faster commercial qualification, improved manufacturing repeatability, and stronger competitiveness in high-volume photovoltaic production.

Tandem Solar Cells represent the leading segment with an estimated market share of approximately 38%, supported by superior conversion efficiency, compatibility with existing silicon manufacturing infrastructure, and strong commercialization momentum. Their ability to exceed 33% certified efficiency has encouraged manufacturers to prioritize tandem product portfolios for utility and commercial applications. Rigid Perovskite Cells continue serving pilot manufacturing and demonstration projects because of process stability, while Single-Junction Cells remain important for research validation and cost-effective product development.

Flexible Perovskite Cells are the fastest-growing segment as lightweight designs enable deployment across portable electronics, building-integrated systems, and curved surfaces. Printable Solar Cells are gaining strategic attention through roll-to-roll manufacturing, reducing processing complexity by nearly 25% and supporting scalable production. Companies are increasing investment in tandem integration, flexible substrates, and automated manufacturing platforms while expanding collaborative development programs to strengthen commercialization readiness and diversify application portfolios.

Utility-Scale Power remains the dominant application, accounting for approximately 41% of deployment due to large project sizes, national renewable energy targets, and increasing demand for high-efficiency photovoltaic modules. Energy developers are integrating tandem technologies to improve electricity generation from constrained installation areas while reducing balance-of-system costs. Building-Integrated Photovoltaics have become operationally important as developers seek energy-producing façades and rooftops for commercial buildings.

Building-Integrated Photovoltaics represent the fastest-growing application, supported by lightweight module designs that reduce structural loading by almost 40% and improve installation flexibility. Consumer Electronics and Portable Devices continue expanding through demand for compact energy harvesting, while Automotive manufacturers evaluate perovskite integration for auxiliary power systems and vehicle surfaces. Companies are strengthening partnerships with construction firms, electronics manufacturers, and automotive suppliers to customize products and accelerate deployment across multiple operational environments.

Energy & Utilities remain the largest end-user segment with an estimated market share of around 46%, driven by utility-scale renewable deployment, grid modernization initiatives, and growing interest in high-efficiency photovoltaic technologies. Large project developers prioritize advanced module performance to maximize electricity generation from limited land resources while improving long-term operational efficiency. Construction companies increasingly participate through integrated building-energy projects, expanding demand beyond conventional solar installations.

Construction is the fastest-growing end-user segment as commercial developers adopt integrated photovoltaic materials for sustainable infrastructure. Electronics manufacturers are expanding research into lightweight energy solutions, while Automotive companies continue evaluating vehicle-integrated photovoltaic applications. Research Institutions remain essential for material innovation, durability testing, and commercialization support. Companies are responding through sector-specific product customization, strategic partnerships, and collaborative innovation ecosystems, while deployment efficiency improvements exceeding 20% are strengthening enterprise purchasing confidence across emerging applications.

Asia-Pacific accounted for the largest market share at 47% in 2025 however, North America is expected to register the fastest growth, expanding at a 43.6% between 2026 and 2033.

Commercialization Accelerates Through Domestic Manufacturing

North America is strengthening its position through localized photovoltaic manufacturing, technology commercialization, and clean-energy industrial policy. The region represents approximately 22% of global market activity, supported by expanding pilot production, university-industry collaboration, and increased private investment in advanced solar technologies. Utility developers are evaluating tandem perovskite modules to improve energy output without expanding project footprints. Automated manufacturing platforms and advanced encapsulation techniques are improving production reliability, while domestic supply-chain development reduces dependence on imported specialty materials. Recent enterprise partnerships have increased pilot manufacturing capacity by nearly 20%, enabling faster technology validation and strengthening commercial deployment readiness across energy infrastructure projects.

United States Market Outlook: The United States leads regional commercialization through strong research capabilities, advanced manufacturing infrastructure, and extensive clean-energy deployment programs. National laboratories, photovoltaic manufacturers, and utility companies are accelerating pilot-scale deployment of tandem technologies across commercial projects. More than 30 pilot and demonstration initiatives are actively supporting manufacturing optimization, while increasing domestic equipment investment strengthens long-term industrial competitiveness and encourages strategic collaboration between technology developers and energy providers.

Research Leadership Supports Industrial Transition

Europe accounts for nearly 24% of global market activity, supported by advanced photovoltaic research, sustainability regulations, and coordinated industrial innovation. The region emphasizes technology validation, high-performance module development, and integration of perovskite technologies into existing photovoltaic manufacturing ecosystems. Industrial collaboration between research institutions and manufacturers has shortened prototype-to-commercial development cycles, while advanced testing infrastructure improves product reliability. Recent manufacturing initiatives have increased pilot production capability by approximately 18%, allowing companies to validate large-area module performance before commercial expansion and strengthen Europe's position in premium photovoltaic technologies.

Germany Market Outlook: Germany remains the region's technology leader through advanced photovoltaic research, precision manufacturing, and industrial innovation. Strong cooperation between research institutes and private enterprises accelerates tandem cell commercialization while supporting durable module development. Automated manufacturing facilities continue expanding pilot production, and certified high-efficiency module programs reinforce Germany's leadership in advanced photovoltaic engineering and commercial product qualification for international markets.

Manufacturing Scale Drives Global Leadership

Asia-Pacific maintains global leadership with approximately 47% market share, supported by integrated photovoltaic supply chains, large-scale manufacturing ecosystems, and rapid commercialization of emerging solar technologies. China, Japan, and South Korea continue investing in advanced production facilities, automation, and material innovation to strengthen industrial competitiveness. Manufacturing productivity has improved by nearly 22% through digital process optimization, while localized component sourcing enhances production resilience. Strong electronics manufacturing capabilities also accelerate integration of lightweight photovoltaic technologies into new commercial applications, positioning the region at the forefront of industrial deployment.

China Market Outlook: China dominates global production through vertically integrated photovoltaic manufacturing, extensive industrial capacity, and continuous investment in tandem module commercialization. The country accounts for more than 45% of global pilot manufacturing capability and continues expanding automated production lines for advanced photovoltaic technologies. Industrial clusters, efficient supply chains, and coordinated manufacturing ecosystems enable rapid scale-up while supporting technology exports and sustained product innovation across multiple application sectors.

Renewable Infrastructure Expands Deployment Opportunities

South America is emerging as an important deployment market as governments prioritize renewable electricity generation and grid diversification. The region contributes approximately 5% of global activity, with utility-scale solar development encouraging evaluation of next-generation photovoltaic technologies. Energy developers increasingly assess lightweight modules for projects in remote locations where installation efficiency is critical. Infrastructure limitations remain, yet public-private partnerships have improved renewable project implementation, while solar capacity additions exceeding 15% in selected markets create favorable conditions for advanced photovoltaic deployment. Companies are strengthening local partnerships and evaluating regional assembly opportunities to improve project economics.

Brazil Market Outlook: Brazil leads regional adoption through extensive renewable energy development, strong solar resource availability, and expanding utility-scale infrastructure. Large electricity distributors and renewable developers continue integrating advanced photovoltaic technologies into future project planning. Industrial investment in localized assembly and engineering capabilities supports long-term deployment efficiency, while diversified renewable policies encourage broader evaluation of next-generation solar solutions across commercial and utility applications.

Strategic Energy Diversification Fuels Adoption

The Middle East & Africa region is strengthening its role through renewable energy diversification, large-scale infrastructure investment, and modernization of electricity systems. The market accounts for approximately 2% of global activity but benefits from excellent solar irradiation and ambitious clean-energy development strategies. Governments are expanding utility-scale photovoltaic projects while evaluating advanced module technologies capable of improving energy yield in challenging environmental conditions. Recent infrastructure programs have increased renewable project pipelines by more than 20%, encouraging technology providers to establish regional partnerships and engineering collaborations for future deployment.

Saudi Arabia Market Outlook: Saudi Arabia leads regional market development through significant renewable infrastructure investment and national energy diversification initiatives. Large-scale solar programs, industrial modernization strategies, and expanding engineering capabilities create favorable conditions for advanced photovoltaic technologies. Utility developers increasingly evaluate high-efficiency tandem modules for desert operating environments, while collaborative projects with technology companies strengthen future manufacturing, deployment expertise, and long-term operational performance across the Kingdom's evolving renewable energy sector.

The market is led by Oxford PV, Microquanta Semiconductor, GCL Perovskite, Saule Technologies, and UtmoLight, with global technology innovators competing against manufacturing-focused Asian producers and specialized module developers. The top five participants collectively control approximately 58% of commercialization activity through proprietary tandem architectures, pilot-scale manufacturing, and strategic intellectual property. Competition centers on conversion efficiency, production scalability, and supply-chain integration rather than price alone. Automated manufacturing has improved production yields by nearly 20%, while advanced encapsulation extends operational stability by over 15%, creating measurable competitive differentiation. Companies are expanding through joint development agreements, localized production, equipment automation, and vertically integrated material sourcing to accelerate commercial deployment. The competitive landscape is shifting from laboratory leadership toward industrial-scale manufacturing capability, favoring organizations with proven production consistency. High certification requirements, specialized deposition equipment, and durable material engineering remain significant entry barriers. Winning requires scalable manufacturing, bankable module reliability, strategic partnerships, and continuous efficiency innovation rather than isolated technology breakthroughs.

Oxford PV

Microquanta Semiconductor

Saule Technologies

GCL Perovskite

UtmoLight

Swift Solar

Solaronix

EneCoat Technologies

Hunt Perovskite Technologies

GreatCell Solar

Frontier Energy Solution

Tandem PV

Current technology development is centered on tandem perovskite-silicon architectures, automated deposition systems, and advanced encapsulation materials that improve commercial viability. Tandem modules now achieve certified efficiencies above 33%, compared with approximately 26–27% for conventional crystalline silicon modules, representing performance improvements exceeding 20%. More than 40% of commercial development programs now prioritize tandem integration because higher power density enables greater electricity generation without increasing installation footprints. Manufacturers adopting precision coating automation also reduce material waste by nearly 18%, strengthening production economics and accelerating industrial qualification.

Emerging technologies include roll-to-roll printable manufacturing, artificial intelligence-driven process optimization, and real-time inline inspection systems. Automated quality monitoring lowers production defects by approximately 22%, while predictive process control improves manufacturing consistency by around 16%. Flexible perovskite substrates are expanding deployment opportunities across building-integrated photovoltaics and portable electronics. Technology leaders with integrated manufacturing capabilities benefit most because scalable production increasingly determines competitive differentiation over laboratory efficiency achievements.

Between 2026 and 2028, industrial emphasis will shift toward durable encapsulation, standardized manufacturing protocols, and hybrid module integration. Digital manufacturing platforms are expected to support production utilization above 70%, enabling faster commercial expansion and improved product reliability. Companies investing early in automation, materials engineering, and ecosystem partnerships will secure stronger operational advantages, while organizations relying on conventional photovoltaic manufacturing without advanced tandem integration risk losing competitiveness in next-generation solar applications.

June 2024 Oxford PV achieved a certified 26.9% efficiency record for a residential-size perovskite-silicon tandem module. The innovation strengthened commercial readiness, improved performance benchmarks, and supported broader adoption of high-efficiency photovoltaic products for space-constrained applications.

March 2025 UtmoLight reached 18.1% stabilized efficiency on a 0.72 m² perovskite module produced through its 150 MW pilot line. The manufacturing expansion demonstrated scalable production capability and improved confidence in commercial deployment across Chinese photovoltaic projects.

April 2025 Oxford PV and Trinasolar formed a patent licensing partnership covering perovskite photovoltaic products in China. The strategic agreement expanded commercialization access, strengthened intellectual property positioning, and enabled faster market entry through established solar manufacturing capabilities. Source: oxfordpv.com

February 2026 First Solar entered a patent licensing agreement with Oxford PV for perovskite device development in the United States. The collaboration supported next-generation solar innovation and expanded potential utility, commercial, and industrial applications through advanced photovoltaic technologies. Source: firstsolar.com

This report provides comprehensive coverage of the Perovskite Solar Cell Market across product types, applications, end-user industries, and major regional markets. It evaluates Rigid Perovskite Cells, Flexible Perovskite Cells, Tandem Solar Cells, Single-Junction Cells, and Printable Solar Cells, while assessing adoption across building-integrated photovoltaics, utility-scale power, consumer electronics, portable devices, and automotive applications. The analysis also examines demand from energy and utilities, construction, electronics, automotive, and research institutions, representing more than 95% of commercial deployment activity.

The report delivers strategic assessment of manufacturing trends, commercialization pathways, technology evolution, competitive positioning, and regional deployment dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It incorporates operational benchmarks, deployment patterns, enterprise strategies, and emerging application areas to support investment evaluation, expansion planning, partnership development, and product portfolio optimization between 2026 and 2033 while identifying high-priority opportunities in advanced tandem technologies, localized manufacturing, and next-generation photovoltaic integration.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 1293 Million |

Market Revenue in 2033 | USD 21495.67 Million |

CAGR (2026 - 2033) | 42.1% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Oxford PV, Microquanta Semiconductor, Saule Technologies, GCL Perovskite, UtmoLight, Swift Solar, Solaronix, EneCoat Technologies, Hunt Perovskite Technologies, GreatCell Solar, Frontier Energy Solution, Tandem PV |

Customization & Pricing | Available on Request (10% Customization is Free) |