Reports

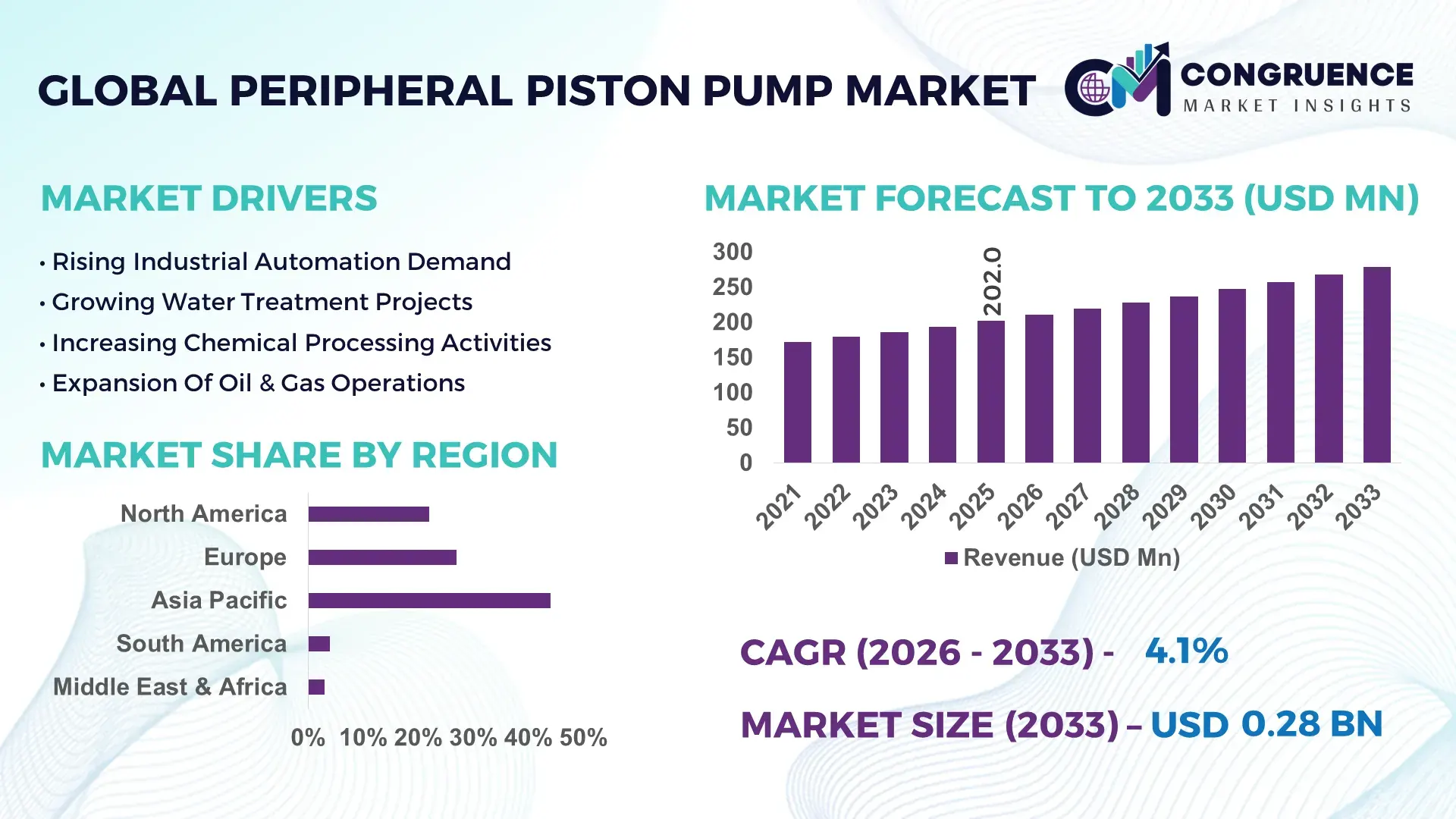

The Global Peripheral Piston Pump Market was valued at USD 202 Million in 2025 and is anticipated to reach a value of USD 278.6 Million by 2033 expanding at a CAGR of 4.1% between 2026 and 2033. Rising deployment of compact high-pressure fluid handling systems across industrial automation, chemical dosing, and water treatment applications is accelerating demand for precision-engineered peripheral piston pumps with 18% higher operational efficiency than conventional rotary alternatives. The market is also benefiting from post-2024 manufacturing relocation trends, particularly as European and North American OEMs diversify component sourcing away from single-country supply chains following Red Sea shipping disruptions and industrial energy cost volatility.

China continues to dominate the global Peripheral Piston Pump Market with nearly 31% manufacturing share, supported by over 4,000 medium-scale industrial fluid equipment suppliers and aggressive automation investments across petrochemical, wastewater, and industrial machinery sectors. The country expanded industrial pump exports by 14% in 2025, while localized smart pump integration in factory systems crossed 28% adoption among large manufacturing facilities. Compared to legacy diaphragm systems, advanced peripheral piston pump units deliver nearly 22% lower maintenance downtime in continuous-duty industrial environments, strengthening their role in process optimization and operational reliability.

As industrial operators prioritize compactness, pressure stability, and lifecycle cost optimization, manufacturers are strategically accelerating high-efficiency product development and regional production expansion to secure long-term competitive positioning in high-growth industrial infrastructure markets.

Market Size & Growth: USD 202 Million in 2025 reaching USD 278.6 Million by 2033 at 4.1% CAGR, driven by industrial automation and precision fluid control demand.

Top Growth Drivers: Industrial automation adoption rose 24%, wastewater infrastructure spending increased 19%, and compact high-pressure systems deployment expanded 17%.

Short-Term Forecast: By 2028, smart pump monitoring integration is projected to improve operational efficiency by 21% while reducing maintenance costs by 16%.

Emerging Technologies: AI-enabled diagnostics, corrosion-resistant composite materials, and sensor-based pressure optimization are reshaping advanced peripheral piston pump systems.

Regional Leaders: Asia-Pacific leads with USD 92 Million demand, Europe exceeds USD 58 Million through energy-efficient adoption, while North America advances smart industrial deployment.

Consumer/End-User Trends: Nearly 34% of industrial operators now prioritize low-maintenance precision pumps for continuous-duty processing environments.

Pilot/Case Example: In 2025, a German chemical processing upgrade reduced fluid pressure fluctuation by 27% after deploying digitally monitored peripheral piston pumps.

Competitive Landscape: Top five manufacturers control nearly 42% market share, led by Verder Group, Cat Pumps, LEWA, Wanner Engineering, and SEKO.

Regulatory & ESG Impact: Industrial energy-efficiency mandates improved adoption of optimized pump systems by 23%, especially across European processing facilities.

Investment & Funding: More than USD 310 Million in industrial fluid management investments supported regional manufacturing expansion and smart equipment partnerships during 2024–2026.

Innovation & Future Outlook: Next-generation modular pump platforms with predictive analytics and compact low-noise designs are transforming high-growth industrial infrastructure markets.

Industrial manufacturing accounts for nearly 38% of total Peripheral Piston Pump Market demand, followed by water treatment and chemical processing applications contributing over 29% combined. Manufacturers are increasingly integrating AI-enabled pressure monitoring and ceramic-coated piston systems, improving operational life by nearly 20% while reducing leakage rates. Asia-Pacific continues dominating volume deployment with over 44% demand concentration as regional production localization accelerates amid global supply chain restructuring. Simultaneously, stricter industrial energy-efficiency regulations across Europe are reshaping procurement strategies toward precision-engineered pump technologies. These execution-level shifts are setting the foundation for deeper strategic competition and long-term operational differentiation.

The Peripheral Piston Pump Market is rapidly transforming into a strategically critical segment within industrial fluid management as manufacturers, infrastructure operators, and process industries intensify their focus on pressure precision, compact system integration, and energy-efficient operations. Competition is accelerating because industrial facilities are no longer evaluating pumps solely on throughput capacity; procurement decisions are increasingly driven by lifecycle efficiency, predictive maintenance capability, and operational stability under continuous-duty environments. This shift is redefining supplier positioning across chemical processing, industrial automation, water treatment, and precision dosing applications.

Global industrial supply chain restructuring and component localization pressures are forcing manufacturers to diversify production networks and reduce dependency on single-region sourcing hubs. Smart peripheral piston pump systems integrated with IoT-enabled diagnostics now improve operational efficiency by 26% while reducing maintenance expenditure by 18% compared to legacy mechanical pumping systems. Asia-Pacific leads global production volume with nearly 44% market concentration due to manufacturing scale advantages, while Europe leads in high-efficiency adoption with over 36% of industrial operators prioritizing low-energy fluid systems to meet tightening emissions and energy compliance standards.

Over the next two to three years, deployment of digitally monitored peripheral piston pumps is projected to increase predictive maintenance accuracy by 31%, significantly improving uptime in process-intensive industries. ESG positioning is also becoming a direct competitive advantage, as energy-efficient pump optimization reduces industrial electricity consumption by nearly 14%, strengthening compliance readiness and lowering operating costs simultaneously.

A notable example emerged in 2025 when a large-scale wastewater treatment facility in Japan upgraded to sensor-integrated piston pump systems and reduced pressure instability incidents by 24% while lowering service intervention frequency by 19%. In response, manufacturers are accelerating investments in modular product platforms, localized assembly plants, and smart fluid-control partnerships to secure long-term industrial contracts. The companies gaining market leadership are those optimizing efficiency, digitization, and regional manufacturing resilience simultaneously, positioning the Peripheral Piston Pump Market as a decisive battleground for industrial performance leadership and future infrastructure competitiveness.

The Peripheral Piston Pump Market is undergoing a structural transformation driven by industrial automation, energy-efficiency mandates, and precision fluid handling requirements across manufacturing-intensive sectors. Demand patterns are shifting from conventional pumping systems toward compact, digitally monitored peripheral piston pumps capable of delivering stable pressure control with reduced maintenance cycles. Industrial processing facilities are increasingly prioritizing high-efficiency pumping technologies as energy costs remain volatile and operational downtime becomes more expensive. More than 32% of industrial fluid management upgrades during 2024–2025 focused on compact pressure-optimized systems, reinforcing the market’s transition toward advanced engineering solutions. Simultaneously, global supply chain diversification and regional manufacturing localization are reshaping production strategies across pump manufacturers. Asia-Pacific continues leading production scale due to cost-efficient manufacturing ecosystems, while Europe and North America are accelerating smart pump deployment through automation-focused industrial modernization initiatives. Regulatory pressure surrounding industrial energy efficiency and water management is also influencing procurement decisions, forcing companies to redesign product portfolios around durability, lower leakage rates, and predictive monitoring capability. As industrial operators seek operational resilience and lifecycle cost optimization, the Peripheral Piston Pump Market is increasingly defined by technology integration, supply chain adaptability, and performance differentiation.

Industrial automation expansion is becoming the strongest growth engine for the Peripheral Piston Pump Market as manufacturers intensify investments in precision-controlled fluid systems capable of supporting continuous production environments. Automated industrial facilities now require nearly 21% higher pressure consistency compared to traditional manufacturing setups, directly increasing demand for compact piston-based pumping technologies. The rapid expansion of chemical processing, wastewater treatment, and industrial dosing systems is accelerating deployment across both developed and emerging economies. The global shift toward smart factories following supply chain disruptions and labor shortages has intensified operational digitization across production infrastructure. In 2025, over 34% of newly commissioned industrial automation projects integrated digitally monitored fluid control systems, forcing pump manufacturers to redesign products around sensor compatibility and predictive diagnostics. Compared to conventional centrifugal systems, advanced peripheral piston pumps reduce maintenance interruptions by nearly 18%, significantly improving operational continuity. This demand surge is driving aggressive business responses. Leading manufacturers are expanding regional assembly operations, increasing automation-focused R&D spending, and forming strategic industrial partnerships to accelerate deployment capability. Several Asian manufacturers increased production capacity by more than 16% during 2024–2025 to address rising export demand from European industrial modernization projects. The market is increasingly rewarding suppliers capable of combining precision engineering, digital integration, and operational durability at scale.

The Peripheral Piston Pump Market continues facing structural pressure from rising raw material costs, component supply concentration, and manufacturing complexity associated with high-precision pumping systems. Stainless steel, specialty alloys, and ceramic-coated piston components experienced price fluctuations exceeding 13% during 2024–2025, directly impacting production economics and equipment pricing. These cost pressures are particularly severe for small and mid-sized manufacturers operating with limited procurement leverage. Supply chain dependency remains another major limitation. Nearly 48% of precision pump sealing and high-pressure valve components are sourced from a concentrated supplier base in East Asia and Europe, creating vulnerability to geopolitical disruptions and logistics instability. Red Sea shipping disruptions and elevated freight costs extended industrial equipment lead times by approximately 11% in several export-heavy regions during 2025. These delays constrained large industrial procurement cycles and postponed infrastructure upgrade timelines. The direct business impact includes higher inventory carrying costs, delayed deployment schedules, and reduced pricing flexibility in competitive contracts. In response, manufacturers are increasingly diversifying supplier networks, negotiating long-term material agreements, and investing in localized component manufacturing. Several companies are also accelerating adoption of composite material alternatives and modular pump architectures to reduce dependency on high-cost imported components. The ability to stabilize supply resilience while controlling engineering costs is becoming a decisive competitive requirement.

The strongest opportunity within the Peripheral Piston Pump Market is emerging from the convergence of digital monitoring technologies, industrial infrastructure expansion, and energy-efficiency optimization initiatives. Industrial operators are rapidly adopting sensor-integrated pumping systems capable of real-time diagnostics, predictive maintenance, and pressure optimization. Facilities deploying smart fluid management platforms reported nearly 27% lower unplanned downtime and 19% higher operational efficiency during continuous-duty industrial operations. Emerging economies are also creating substantial untapped demand pockets. Infrastructure investment across Southeast Asia, the Middle East, and Latin America increased by over 22% during 2024–2025, accelerating deployment of compact high-pressure fluid systems across water treatment, industrial processing, and construction applications. Unlike mature industrial markets focused primarily on replacement demand, these regions are building entirely new industrial ecosystems requiring scalable fluid-control infrastructure.A particularly important shift involves modular peripheral piston pump systems designed for remote diagnostics and rapid deployment. Companies integrating AI-based monitoring into pump systems reduced maintenance response time by nearly 31%, creating a measurable operational advantage for industrial operators managing distributed facilities. Manufacturers are responding aggressively through R&D expansion, localized production partnerships, and ecosystem-building strategies centered around digital industrial automation. The next wave of market leadership will be captured by companies capable of combining smart analytics, operational durability, and scalable manufacturing execution across high-growth industrial regions.

The Peripheral Piston Pump Market faces escalating execution challenges linked to system integration complexity, operational reliability demands, and skilled workforce limitations. Advanced peripheral piston pumps require highly calibrated installation and pressure-balancing processes, yet nearly 29% of industrial facilities report shortages of technically trained maintenance personnel capable of managing digitally integrated fluid systems. This operational skills gap is constraining deployment efficiency across multiple industrial sectors. Infrastructure inconsistency is creating additional scalability barriers. In several emerging manufacturing regions, unstable industrial power supply and limited predictive maintenance infrastructure increase equipment failure risk and shorten operational life cycles by nearly 14%. At the same time, industrial buyers are demanding higher pressure precision, lower noise emissions, and reduced leakage thresholds, forcing manufacturers to accelerate engineering upgrades while maintaining competitive pricing. Regulatory tightening surrounding industrial energy consumption and wastewater efficiency is also increasing compliance pressure on manufacturers. Companies unable to improve pump efficiency metrics risk losing procurement eligibility in highly regulated industrial environments. In response, leading suppliers are increasing investment in digital service platforms, advanced materials engineering, and regional technical support partnerships. Long-term competitiveness will depend on solving execution reliability, workforce capability, and compliance scalability simultaneously while maintaining operational affordability in increasingly competitive industrial markets.

32% Rise in Smart Pump Integration Reshaping Industrial Operations: Industrial facilities are rapidly integrating IoT-enabled peripheral piston pumps with predictive monitoring systems, increasing smart deployment rates by 32% during 2024–2025. Manufacturers are embedding sensor-driven diagnostics to reduce unplanned downtime by 21% and improve pressure stability across continuous-duty applications. This transition is forcing suppliers to restructure product portfolios around digital compatibility and remote servicing capabilities. Industrial operators are prioritizing lifecycle optimization over upfront equipment cost, accelerating partnerships between automation firms and pump manufacturers.

27% Increase in Localized Manufacturing Redefining Supply Chains: Regional production expansion accelerated by 27% as manufacturers responded to shipping disruptions, tariff uncertainty, and industrial procurement delays linked to Red Sea trade instability. Asia-Pacific producers expanded localized assembly operations while European OEMs increased dual-sourcing strategies to reduce component dependency risks. This operational shift shortened lead times by nearly 16% and improved inventory responsiveness for industrial customers. Companies are increasingly optimizing regional supply ecosystems instead of relying on centralized export-heavy manufacturing structures.

24% Shift Toward Energy-Efficient Systems Optimizing Industrial Compliance: Industrial buyers are replacing legacy pumping technologies with energy-efficient peripheral piston systems capable of reducing electricity consumption by approximately 14%. Nearly 24% of new industrial fluid-control installations now prioritize low-noise, low-leakage pump configurations due to tightening environmental and efficiency regulations. Manufacturers are responding through advanced ceramic-coated piston technologies and compact modular designs that improve operational durability. Compliance-driven procurement is redefining competitive positioning across chemical processing and wastewater treatment sectors.

19% Growth in Service-Based Business Models Reshaping Vendor Competition: Equipment suppliers are increasingly shifting toward maintenance contracts, remote monitoring subscriptions, and performance-based servicing models, with adoption rising 19% during 2025. Industrial operators prefer bundled service agreements that improve uptime visibility and reduce maintenance planning complexity. This transition is creating recurring revenue ecosystems while forcing smaller manufacturers to expand digital support infrastructure. A non-obvious shift is emerging where aftersales analytics capability is becoming as strategically important as pump hardware performance itself.

The Peripheral Piston Pump Market is segmented by type, application, and end-user, with demand increasingly concentrating around high-efficiency industrial fluid handling environments. Industrial-grade configurations continue dominating volume deployment due to their ability to support continuous-duty operations with stable pressure output and lower maintenance frequency. More than 41% of total demand originates from manufacturing and industrial processing applications where operational precision and energy efficiency directly influence production performance. Demand distribution is also shifting toward digitally integrated and compact pump configurations as automation adoption accelerates across wastewater treatment, chemical processing, and infrastructure systems. Application diversification is strengthening market resilience, particularly as emerging industrial economies expand localized production capabilities and infrastructure investments. End-user procurement behavior increasingly prioritizes lifecycle cost optimization, predictive maintenance compatibility, and regulatory compliance, forcing manufacturers to redesign products around operational durability and smart monitoring integration. Companies focusing on scalable production, modular design flexibility, and regional customization strategies are capturing stronger positioning across both mature industrial markets and high-growth infrastructure-driven economies.

Industrial Peripheral Piston Pumps dominate the Peripheral Piston Pump Market with approximately 46% share due to their superior durability, continuous-duty capability, and compatibility with automated fluid handling systems across manufacturing-intensive industries. Their structural advantage lies in stable pressure delivery, lower operational downtime, and easier integration into industrial process infrastructure. Large-scale chemical processing and water treatment facilities increasingly prioritize industrial-grade pumps because they improve operational consistency by nearly 19% compared to traditional fluid-transfer systems. Smart Peripheral Piston Pumps represent the fastest-growing segment, expanding adoption by nearly 24% as industrial operators accelerate deployment of sensor-enabled monitoring and predictive maintenance systems. Compared to conventional industrial pumps, smart variants significantly reduce maintenance interruptions and improve energy optimization through real-time pressure diagnostics. The market is clearly shifting from purely mechanical systems toward digitally integrated fluid-control architectures. Meanwhile, compact utility-grade and specialized corrosion-resistant variants collectively account for nearly 54% of total deployment, maintaining strong strategic relevance in precision dosing, laboratory processing, and smaller-scale industrial environments. Manufacturers are responding by expanding modular product portfolios, increasing automation-focused engineering investments, and scaling localized production capabilities. Investment activity is increasingly concentrated around digitally optimized and energy-efficient pump categories, while conventional low-feature systems are gradually losing procurement priority in technologically advanced industrial sectors.

Industrial Processing remains the leading application segment within the Peripheral Piston Pump Market, accounting for nearly 38% of total demand due to high-volume fluid handling requirements across chemical manufacturing, precision dosing, and automated production environments. Demand concentration exists because industrial facilities require consistent pressure stability, low leakage rates, and continuous operational reliability to support large-scale processing systems. Peripheral piston pumps have become increasingly critical in automated industrial workflows where process consistency directly influences production efficiency. Water Treatment is emerging as the fastest-growing application segment, with deployment activity increasing by approximately 22% due to tightening wastewater regulations, infrastructure modernization programs, and rising industrial water recycling requirements. Compared to mature industrial processing applications, water treatment systems are rapidly adopting compact high-efficiency pump technologies capable of reducing energy consumption and improving fluid pressure precision. The remaining demand is distributed across oil & gas transfer systems, pharmaceutical dosing operations, and precision chemical handling applications, collectively representing nearly 40% of market utilization. Companies are responding by scaling application-specific product customization, strengthening corrosion-resistant engineering capabilities, and expanding digitally monitored pump deployment. Procurement trends increasingly favor application-focused performance optimization rather than generalized fluid-transfer solutions, creating strategic opportunities for manufacturers capable of delivering specialized operational reliability.

Manufacturing Industries lead the Peripheral Piston Pump Market with nearly 42% demand concentration because of their heavy dependence on precision-controlled fluid systems for continuous industrial operations. High-volume processing facilities prioritize peripheral piston pumps for operational stability, compact integration capability, and reduced maintenance cycles. Large manufacturing operators are increasingly replacing legacy fluid systems with digitally monitored pump platforms to improve production uptime and energy optimization. Water & Wastewater Utilities represent the fastest-growing end-user segment, with adoption increasing by nearly 23% as governments and infrastructure operators accelerate investment in industrial water recycling, pressure-controlled distribution systems, and energy-efficient wastewater management. Compared to established manufacturing buyers focused on productivity, utility operators prioritize regulatory compliance, operational durability, and lifecycle cost reduction. The remaining demand is distributed across oil & gas, pharmaceutical, food processing, and specialty chemical sectors, collectively accounting for nearly 35% of market usage. End-user purchasing behavior is increasingly shifting toward customized pump configurations, long-term service contracts, and predictive maintenance integration. Manufacturers are responding through flexible pricing strategies, regional technical partnerships, and application-specific engineering development. Future demand is expected to concentrate around sectors requiring operational resilience, digital monitoring capability, and compliance-focused fluid management infrastructure.

Asia-Pacific accounted for the largest market share at 44% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 4.8% between 2026 and 2033.

Asia-Pacific dominates the Peripheral Piston Pump Market due to large-scale industrial manufacturing expansion, cost-efficient production ecosystems, and strong infrastructure investment across China, India, Japan, and Southeast Asia. Europe holds approximately 27% market share, driven by energy-efficiency regulations and accelerated adoption of precision-controlled industrial fluid systems. North America contributes nearly 22% of global demand and leads in smart pump integration, predictive maintenance deployment, and automation-focused industrial modernization. Meanwhile, South America and the Middle East & Africa collectively account for 7%, supported by industrial infrastructure upgrades and resource-sector investments. Supply chain diversification and regional manufacturing localization strategies are increasingly reshaping competitive positioning, prompting major companies to prioritize Asia-Pacific for scale, North America for digital innovation, and Europe for compliance-driven product advancement.

North America accounts for nearly 22% of the global Peripheral Piston Pump Market, supported by strong demand across industrial automation, chemical processing, and advanced wastewater infrastructure sectors. The United States dominates regional deployment due to aggressive modernization of manufacturing facilities and increasing integration of predictive maintenance technologies. More than 36% of industrial fluid management upgrades during 2025 involved digitally monitored pumping systems designed to improve uptime and operational precision. Rising energy-efficiency standards and industrial operating cost pressures are accelerating the replacement of legacy pump infrastructure with compact high-pressure systems. Manufacturers expanded smart pump production capacity by approximately 18% across the region to address rising demand from automation-intensive industries. Enterprise buyers increasingly prioritize lifecycle cost optimization, remote diagnostics, and service-based procurement models. Companies are aggressively investing in regional production expansion and industrial automation partnerships because North America remains a critical profitability and innovation-driven market.

Europe represents approximately 27% of the global Peripheral Piston Pump Market, led by Germany, France, and Italy due to advanced manufacturing ecosystems and strict industrial energy-efficiency regulations. ESG-driven industrial modernization is strongly influencing procurement behavior, particularly as European Union sustainability targets intensify pressure on industrial fluid management systems. Nearly 41% of industrial operators now prioritize low-energy, low-leakage pump technologies to strengthen compliance readiness and reduce operational waste. Manufacturers are increasingly integrating sensor-enabled monitoring systems and ceramic-coated piston technologies to improve efficiency and reduce maintenance cycles by nearly 17%. Regulatory pressure surrounding industrial emissions and wastewater management is accelerating adoption of digitally optimized fluid systems across chemical and processing industries. Enterprise purchasing patterns remain quality-focused and compliance-driven, favoring technologically advanced pump configurations over low-cost alternatives. Europe continues forcing product innovation and engineering adaptation, making the region strategically important for premium industrial pump manufacturers.

Asia-Pacific leads the Peripheral Piston Pump Market with approximately 44% global demand concentration, driven by rapid industrialization, manufacturing scale advantages, and expanding infrastructure investment across China, India, Japan, and Southeast Asia. China alone contributes nearly 31% of regional manufacturing output due to its extensive industrial equipment ecosystem and export-oriented production base. Localized manufacturing expansion and lower production costs continue strengthening the region’s supply chain dominance. More than 29% of industrial automation upgrades across Asia-Pacific integrated advanced fluid-control systems during 2025, accelerating adoption of compact high-efficiency peripheral piston pumps. Regional manufacturers expanded export-oriented production capacity by approximately 16% to meet rising demand from Europe and North America. Enterprise buyers across the region prioritize scalability, speed, and operational affordability, encouraging suppliers to optimize modular product designs and localized assembly operations. Asia-Pacific remains strategically critical because it combines manufacturing scale, infrastructure expansion, and accelerating industrial modernization simultaneously.

South America accounts for nearly 4% of the global Peripheral Piston Pump Market, with Brazil and Argentina leading regional demand through industrial processing, mining, and water infrastructure projects. Demand growth is increasingly linked to modernization of wastewater treatment systems and expansion of industrial manufacturing operations requiring compact high-pressure fluid technologies. However, infrastructure limitations, currency volatility, and higher import dependency continue constraining broader market scalability. Industrial equipment procurement costs increased by approximately 12% during 2025 due to logistics inefficiencies and imported component exposure. Despite these limitations, localized industrial demand grew nearly 15% across selected manufacturing corridors where automation adoption accelerated. Enterprise buyers remain highly price-sensitive and prioritize operational durability over premium digital functionality. Manufacturers are responding through regional distributor partnerships, localized servicing capability, and lower-cost modular system offerings. South America presents a strategic balance between emerging industrial opportunity and execution-level operational risk.

The Middle East & Africa region contributes approximately 3% of the global Peripheral Piston Pump Market, supported by growing investments in oil & gas processing, desalination infrastructure, and industrial construction projects across Saudi Arabia, the UAE, and South Africa. Industrial diversification initiatives and infrastructure modernization programs are increasing deployment of advanced fluid management systems across high-pressure operational environments. Government-backed industrial expansion projects accelerated regional industrial equipment investment by nearly 14% during 2025. Companies are increasingly adopting digitally monitored peripheral piston pump systems to improve pressure reliability and reduce maintenance intervention in remote operational sites. Large infrastructure contractors and energy operators prioritize durable, low-maintenance systems capable of operating under demanding environmental conditions. Regional enterprises are increasingly partnering with international manufacturers to improve technology transfer and operational efficiency. The Middle East & Africa market is becoming strategically important for infrastructure-focused suppliers targeting long-term industrial transformation and resource-sector modernization opportunities.

China – 31% Market share: Dominates through large-scale industrial manufacturing capacity, export-oriented production ecosystems, and aggressive automation deployment across fluid management industries.

United States – 19% Market share: Leads in advanced adoption due to strong industrial automation investment, smart manufacturing integration, and high demand for predictive maintenance-enabled pumping systems.

The Peripheral Piston Pump Market is characterized by intense competition between global precision pump manufacturers, automation-focused engineering firms, and cost-competitive regional suppliers. Companies such as Verder Group, LEWA GmbH, Wanner Engineering, SEKO, Cat Pumps, and ProMinent are competing aggressively across industrial automation, chemical processing, and high-pressure fluid management applications. Global leaders dominate premium industrial contracts through advanced engineering and digital integration, while regional manufacturers compete primarily on pricing flexibility and localized delivery speed.

The top five players collectively control nearly 42% of global market activity, with competition increasingly centered on efficiency optimization, predictive maintenance capability, and modular customization. Smart pump integration improved industrial uptime by nearly 26%, forcing manufacturers to accelerate digital product development. Simultaneously, localized manufacturing expansion reduced delivery lead times by approximately 18%, intensifying competition around supply chain responsiveness and regional servicing capability.

Companies are actively pursuing production expansion, technology partnerships, and vertical integration strategies to strengthen component control and aftermarket service positioning. The market is also witnessing a competitive shift toward AI-enabled diagnostics and energy-efficient pump systems as industrial operators prioritize lifecycle optimization over initial equipment cost. High engineering complexity, certification requirements, and precision component dependency remain major entry barriers. Winning in this market increasingly requires technological differentiation, regional supply resilience, advanced service infrastructure, and the ability to deliver high-efficiency customized solutions at industrial scale.

LEWA GmbH

Wanner Engineering, Inc.

Cat Pumps

SEKO S.p.A.

ProMinent GmbH

Milton Roy

SPX FLOW

Dover Corporation

IDEX Corporation

Grundfos Holding A/S

Graco Inc.

Watson-Marlow Fluid Technology Solutions

Seepex GmbH

The Peripheral Piston Pump Market is rapidly transitioning toward digitally integrated, high-efficiency fluid handling technologies designed to improve precision, durability, and operational intelligence. Smart monitoring systems with IoT-enabled diagnostics are now deployed across nearly 34% of newly installed industrial pump systems, enabling predictive maintenance and reducing unplanned downtime by approximately 21%. Manufacturers are increasingly integrating AI-based pressure optimization algorithms and remote performance analytics to strengthen industrial process stability and lower servicing costs.

Advanced materials engineering is also reshaping pump performance standards. Ceramic-coated pistons, corrosion-resistant alloys, and modular diaphragm technologies are improving operational life by nearly 18% while reducing leakage-related maintenance interruptions. Compared to conventional mechanical pump systems, next-generation digitally optimized peripheral piston pumps improve energy efficiency by approximately 24% and reduce maintenance expenditure by 17%. This technology shift is creating a strong competitive advantage for manufacturers capable of delivering high-pressure precision with lower lifecycle costs.

Emerging mechatronic drive systems and intelligent flow-control technologies are accelerating adoption across chemical processing, water treatment, and pharmaceutical dosing applications. Companies investing in digitally controlled modular pump architectures are securing stronger positioning in high-value industrial contracts where automation compatibility and operational reliability are becoming mandatory procurement criteria.

Between 2026 and 2028, adoption of sensor-integrated and predictive-maintenance-enabled pump systems is expected to exceed 40% across advanced industrial facilities. Suppliers capable of combining digital diagnostics, energy optimization, and localized technical support will benefit most as industrial operators increasingly prioritize uptime assurance, remote servicing capability, and long-term operational resilience.

March 2025 – LEWA GmbH upgraded its ecoflow® LDG process pump platform, increasing hydraulic power by 15% within the same footprint while improving discharge pressure performance from 659 bar to 713 bar. The upgrade strengthened high-pressure industrial processing efficiency and reduced space requirements by nearly 40%. [Power Density Shift] Source: www.lewa.com

April 2025 – Verder Group consolidated Ponndorf peristaltic pump manufacturing into a new high-efficiency facility in Poland to improve production speed, sustainability, and global supply responsiveness. The move expanded operational capacity and streamlined regional manufacturing efficiency amid increasing industrial demand volatility. [Localized Production Push]

October 2025 – LEWA expanded its micro-metering pump portfolio with two new models designed for gas odorization applications, improving dosing flexibility across broader flow and pressure combinations. The innovation enhanced precision injection performance while reducing oversizing-related operating costs in industrial gas distribution systems. [Precision Dosing Expansion]

May 2026 – LEWA enhanced its ecoflow® LDH Boxer pump series with a 20% hydraulic power increase, enabling higher flow rates and pressure performance without requiring larger equipment footprints. The advancement strengthened modular high-pressure processing capability across aggressive industrial fluid applications. [High-Pressure Upgrade]

The Peripheral Piston Pump Market Report provides comprehensive coverage of industrial fluid handling technologies across multiple product categories, applications, end-user industries, and global regions. The report analyzes segmentation by pump type, industrial application, and end-user demand behavior while evaluating operational trends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It further examines emerging technologies including smart monitoring systems, AI-enabled diagnostics, modular pump architectures, and advanced corrosion-resistant materials increasingly adopted across high-pressure industrial environments.

The study delivers detailed analytical depth through evaluation of more than 15 strategic market indicators, including regional adoption concentration, industrial deployment patterns, operational efficiency improvements, and competitive positioning metrics. Over 44% of global demand concentration within Asia-Pacific manufacturing ecosystems and nearly 34% adoption of digitally integrated pump systems are assessed to identify shifting procurement priorities and technology transformation trends. The report also profiles major global manufacturers, regional suppliers, and automation-focused engineering firms shaping industrial competition.

From a strategic perspective, the report supports investment planning, manufacturing expansion, supplier diversification, and competitive benchmarking decisions. It additionally evaluates future-facing developments between 2026 and 2033, including predictive maintenance integration, smart industrial automation adoption, localized production expansion, and next-generation energy-efficient fluid management systems transforming industrial infrastructure modernization globally.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 202 Million |

| Market Revenue (2033) | USD 278.6 Million |

| CAGR (2026–2033) | 4.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Verder Group; LEWA GmbH; Wanner Engineering, Inc.; Cat Pumps; SEKO S.p.A.; ProMinent GmbH; Milton Roy; SPX FLOW; Dover Corporation; IDEX Corporation; Grundfos Holding A/S; Graco Inc.; Watson-Marlow Fluid Technology Solutions; Seepex GmbH |

| Customization & Pricing | Available on Request (10% Customization Free) |