Reports

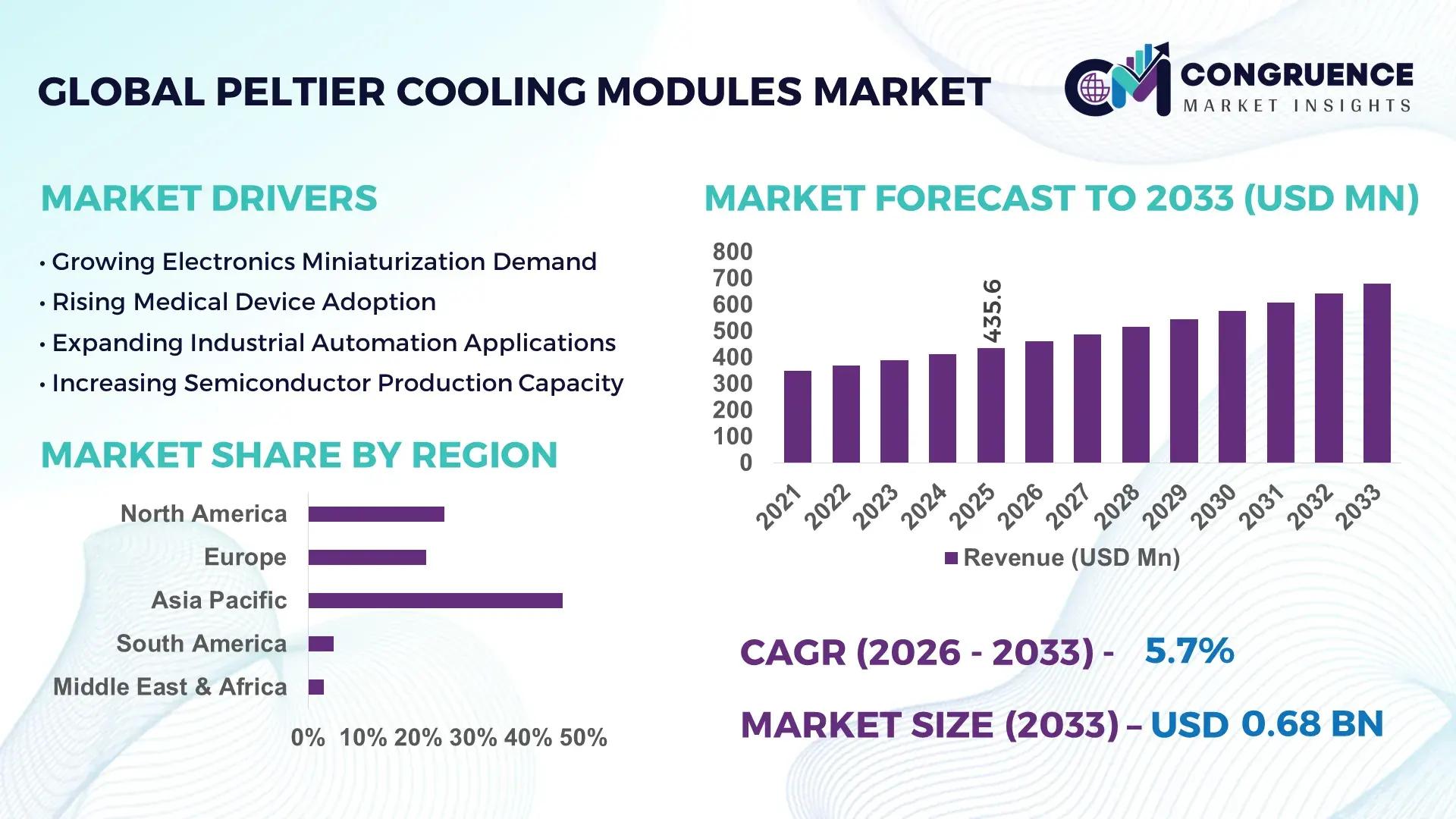

The Global Peltier Cooling Modules Market was valued at USD 435.6 Million in 2025 and is anticipated to reach a value of USD 680.8 Million by 2033 expanding at a CAGR of 5.74% between 2026 and 2033. Growth is being accelerated by rising deployment of thermoelectric cooling in semiconductor fabrication equipment, medical diagnostics systems, laser technologies, and electric vehicle battery thermal management applications requiring precise temperature control.

China remains the dominant country in the market, accounting for approximately 38% of global thermoelectric module manufacturing capacity, supported by investments exceeding USD 1.5 billion in semiconductor and advanced electronics production ecosystems. Japan follows with nearly 18% market participation driven by precision medical devices and optical equipment, while China's module output volume is estimated to be more than 2.1 times that of Japan. Ongoing supply-chain diversification following U.S.-China technology restrictions is further reshaping sourcing strategies across electronics and industrial cooling segments.

Strategically, manufacturers that secure localized supply networks and invest in high-efficiency thermoelectric materials are positioned to strengthen competitive advantage across high-value electronics and industrial applications.

Market Size & Growth: USD 435.6 million in 2025 reaching USD 680.8 million by 2033 at 5.74% CAGR, supported by expanding semiconductor fabrication and precision thermal management requirements.

Top Growth Drivers: Semiconductor equipment demand (+22%), medical diagnostics adoption (+18%), and EV battery thermal management integration (+16%) are driving market expansion.

Short-Term Forecast: By 2028, module energy efficiency is expected to improve by 12% while system integration costs decline by approximately 9%.

Emerging Technologies: AI-enabled thermal monitoring, advanced bismuth telluride materials, and automated manufacturing are improving cooling precision by up to 15%.

Regional Leaders: Asia Pacific surpasses USD 300 million, North America exceeds USD 145 million, and Europe approaches USD 120 million, driven by electronics, healthcare, and industrial automation investments.

Consumer/End-User Trends: More than 35% of new compact medical diagnostic devices now incorporate solid-state thermoelectric cooling technologies.

Pilot/Case Example: In 2024, advanced laser cooling deployments improved temperature stability by 20% and reduced maintenance interventions by 14%.

Competitive Landscape: The top five suppliers collectively control nearly 45% share, led by Ferrotec, Laird Thermal Systems, KELK, TEC Microsystems, and Crystal Ltd.

Regulatory & ESG Impact: Solid-state cooling solutions reduce refrigerant dependency by nearly 100% while supporting stricter environmental compliance initiatives.

Investment & Funding: More than USD 800 million has been directed toward electronics manufacturing expansion and thermal technology upgrades amid global supply-chain realignment.

Innovation & Future Outlook: Next-generation nanostructured thermoelectric materials demonstrate efficiency gains exceeding 10%, supporting higher-performance cooling architectures.

Peltier Cooling Modules are becoming increasingly important across semiconductor manufacturing, photonics, laboratory instrumentation, and compact healthcare equipment where temperature precision directly influences operational performance. Recent innovations in high-density thermoelectric materials and intelligent thermal control systems have improved cooling efficiency by nearly 15%. As manufacturers diversify production footprints beyond traditional electronics hubs, demand for reliable solid-state cooling solutions continues to strengthen, setting the stage for broader strategic market developments.

Peltier cooling modules are becoming strategically important as industries prioritize compact, vibration-free, and highly precise thermal management systems. Semiconductor fabrication, medical diagnostics, aerospace electronics, and photonics manufacturers increasingly rely on thermoelectric cooling to maintain product performance and reliability. The market is also benefiting from supply-chain restructuring efforts as manufacturers diversify sourcing and production footprints following global technology trade restrictions and electronics sector realignments.

Compared with conventional compressor-based cooling systems, advanced thermoelectric modules can reduce system footprint by nearly 40% while delivering temperature control accuracy within ±0.1°C in critical applications. China leads large-scale manufacturing capacity, while Japan and South Korea maintain advantages in precision engineering and high-performance module integration. Across industrial automation applications, adoption of smart thermal monitoring systems has increased by more than 20%, improving equipment uptime and operational consistency.

Recent deployments in laser systems and diagnostic imaging platforms demonstrate measurable improvements in thermal stability and maintenance efficiency. Companies are expanding partnerships with semiconductor equipment suppliers, investing in advanced materials research, and localizing manufacturing capabilities to strengthen resilience. Over the next two to three years, growing integration into EV electronics, optical communication systems, and AI hardware infrastructure will further elevate the strategic value of thermoelectric cooling technologies, creating durable competitive differentiation for early adopters.

The accelerating expansion of semiconductor fabrication and precision electronics manufacturing remains the strongest market driver. Semiconductor capital expenditures increased by over 15% globally in recent years, while advanced packaging adoption expanded by approximately 20%, creating greater demand for localized temperature management solutions. Peltier modules provide temperature stability within fractions of a degree, making them essential for photonics, lasers, sensors, and testing equipment. U.S.-China technology restrictions have also encouraged investment diversification across countries such as Vietnam, India, and Malaysia, increasing deployment opportunities for thermoelectric cooling systems. In response, manufacturers are expanding production capacity, strengthening semiconductor partnerships, and investing in next-generation materials that improve thermal transfer efficiency. The strategic outcome is deeper integration of thermoelectric technologies into mission-critical industrial and electronics infrastructure.

Material cost volatility continues to constrain market scalability. Bismuth, tellurium, and other critical thermoelectric materials have experienced price fluctuations exceeding 25% during recent supply disruptions, creating procurement challenges for module manufacturers. China controls a significant share of global tellurium processing capacity, increasing exposure to trade-related risks and sourcing concentration. Additionally, high-performance thermoelectric systems often carry 20–30% higher upfront costs compared with conventional cooling alternatives in standard industrial applications. These factors directly affect profitability and purchasing decisions among cost-sensitive end users. To mitigate risk, manufacturers are diversifying supplier networks, pursuing regional sourcing strategies, and investing in material efficiency improvements. A key operational insight is that supply resilience increasingly influences customer contracts as much as product performance.

Emerging applications in electric vehicles, AI computing hardware, and optical communication networks present significant opportunities. Global AI server deployments are increasing by more than 25% annually, while EV electronic content per vehicle continues to expand. These trends create demand for compact thermal management systems capable of operating in space-constrained environments. Advanced thermoelectric materials have demonstrated efficiency improvements exceeding 10%, enabling broader deployment across next-generation electronics. Government-backed semiconductor initiatives in India, South Korea, and the United States are also accelerating localized demand for precision cooling technologies. Companies are responding through collaborative R&D programs, strategic acquisitions, and specialized product development targeting high-density electronics. A notable opportunity lies in integrating intelligent thermal analytics with cooling modules to create value-added performance optimization solutions.

A major long-term challenge involves maintaining efficiency in increasingly power-dense environments. AI processors, advanced semiconductor tools, and high-performance optical systems generate thermal loads that have increased by approximately 30% over the last five years. While Peltier modules excel in precision cooling, integration complexity rises significantly as heat flux levels increase. Engineering teams must balance energy consumption, thermal dissipation, and system architecture constraints to achieve consistent performance. Workforce shortages in thermal engineering disciplines and growing design complexity further pressure deployment timelines. Companies are addressing these issues through advanced simulation tools, hybrid cooling architectures, and strategic engineering partnerships. Organizations that successfully improve scalability while maintaining thermal precision will secure stronger competitive positioning in next-generation electronics ecosystems.

Semiconductor Thermal Precision Expansion Semiconductor equipment manufacturers are increasing thermoelectric cooling integration as process nodes become more temperature sensitive. Advanced packaging deployments have grown by nearly 20%, while precision thermal control requirements have improved by over 15% in leading fabrication facilities. Taiwan and South Korea continue expanding high-performance chip production, pushing suppliers to scale module output and strengthen long-term manufacturing partnerships. The result is improved process stability, reduced defect rates, and greater equipment utilization across critical semiconductor workflows.

Localized Supply Chain Restructuring Supply-chain diversification has become a major operational trend following technology trade restrictions and material sourcing pressures. More than 25% of electronics manufacturers have expanded supplier qualification programs, while localized procurement initiatives increased by approximately 18% across industrial cooling ecosystems. Companies are restructuring production networks, establishing secondary sourcing channels, and increasing regional assembly capabilities. This shift improves delivery reliability, reduces procurement risks, and strengthens operational resilience for high-value electronics applications.

Smart Thermal Monitoring Integration Intelligent temperature management platforms are being integrated directly with cooling modules to enhance operational performance. AI-enabled thermal diagnostics have reduced unplanned maintenance events by nearly 12%, while predictive monitoring adoption increased by over 20% among advanced electronics manufacturers. Companies are combining sensors, analytics software, and thermoelectric modules into unified thermal management architectures. This transition improves asset reliability, extends equipment life cycles, and lowers maintenance-related operating costs.

Miniaturization Across Medical Devices Demand for compact healthcare and diagnostic equipment is accelerating the adoption of smaller thermoelectric cooling systems. Portable diagnostic device deployments increased by approximately 17%, while compact optical imaging platforms improved thermal efficiency by nearly 10%. Regulatory emphasis on precision diagnostics and decentralized healthcare delivery is encouraging manufacturers to redesign products around smaller cooling footprints. Suppliers are responding through automation investments, high-density module development, and specialized healthcare partnerships that improve integration flexibility.

Single-stage Peltier modules remain the leading segment, accounting for an estimated 58% of total market demand due to their cost efficiency, compact design, and suitability for mainstream temperature-control applications. Their widespread deployment across consumer electronics, medical devices, laboratory equipment, and optical systems supports consistent demand. Manufacturers continue improving thermal conductivity and reducing power consumption, helping increase adoption across space-constrained equipment. Investment priorities remain focused on optimizing performance while maintaining affordability, particularly in China, Japan, and South Korea. Multi-stage modules represent the fastest-growing segment as demand rises for ultra-low temperature applications requiring higher cooling differentials. Adoption within photonics, semiconductor testing, and advanced scientific instrumentation has increased by nearly 14% over the past two years. Meanwhile, micro Peltier modules are gaining traction in wearable diagnostics and compact sensing platforms, while high-capacity industrial modules maintain strategic relevance in automation systems and specialized manufacturing environments. Companies are expanding product portfolios, strengthening engineering partnerships, and developing application-specific module architectures to capture emerging high-performance opportunities.

Electronics remains the leading application segment, representing approximately 42% of overall deployment activity due to extensive use in semiconductor manufacturing, laser systems, sensors, and optical communication equipment. Increasing miniaturization trends and higher processing densities are driving demand for precise thermal management. More than 30% of advanced electronics systems now utilize localized cooling solutions to improve performance stability and component longevity. Manufacturers continue expanding integration capabilities to support increasingly compact device architectures. Medical equipment is emerging as the fastest-growing application segment as diagnostic accuracy and portable healthcare technologies become operational priorities. Adoption within molecular diagnostics, imaging systems, and laboratory instrumentation has expanded by nearly 16% in recent years. Industrial automation applications continue generating stable demand through process monitoring and precision control requirements, while aerospace and defense applications prioritize reliability under extreme operating conditions. Companies are investing in customized module configurations, automated assembly capabilities, and industry-specific thermal management platforms to address evolving application requirements and strengthen competitive differentiation.

Electronics and semiconductor manufacturers constitute the dominant end-user group, accounting for nearly 40% of market consumption due to extensive thermal management requirements across fabrication equipment, testing platforms, and precision electronic devices. The segment benefits from continuous infrastructure investments and increasing demand for temperature-sensitive manufacturing processes. More than 25% of newly deployed semiconductor support systems incorporate advanced thermoelectric cooling solutions to improve process consistency and operational reliability. Suppliers are prioritizing long-term contracts and customized engineering support for these customers. Healthcare organizations and medical device manufacturers represent the fastest-growing end-user category, driven by rising deployment of portable diagnostics, imaging technologies, and laboratory automation systems. Adoption across healthcare-related applications has increased by approximately 15%, supported by growing requirements for stable thermal regulation in sensitive diagnostic environments. Industrial enterprises continue investing in process-control applications, while aerospace and defense organizations prioritize mission-critical reliability. Companies are responding through application-focused product development, strategic healthcare partnerships, and flexible pricing models designed to strengthen customer retention and support long-term deployment expansion.

Asia-Pacific accounted for the largest market share at 46.2% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2026 and 2033.

North America represents approximately 24.8% of global market activity, supported by strong semiconductor manufacturing investments, advanced medical technology deployment, and expanding aerospace electronics applications. The region maintains high adoption of thermoelectric cooling within laboratory instrumentation, optical communication systems, and precision testing equipment. Increased domestic semiconductor capacity development has accelerated demand for localized thermal management technologies. More than 30% of newly commissioned advanced semiconductor support systems in the United States now integrate precision cooling architectures. Companies are strengthening supply-chain resilience through local sourcing partnerships, automation investments, and engineering collaborations focused on improving thermal efficiency across high-performance electronic environments.

United States Market Outlook: The United States remains the region's largest market due to extensive semiconductor fabrication investments, defense electronics production, and medical technology innovation. Federal manufacturing initiatives continue encouraging localized electronics supply chains, creating sustained demand for precision thermal management systems. More than 40 major semiconductor expansion projects announced since 2023 have increased deployment opportunities for advanced cooling technologies. U.S.-based enterprises are prioritizing strategic partnerships, materials innovation, and vertically integrated manufacturing approaches to strengthen operational control and reduce supply dependency.

Europe accounts for nearly 21.5% of global demand, driven by industrial automation, medical diagnostics, photonics, and advanced manufacturing modernization initiatives. The region benefits from strong engineering expertise and increasing adoption of environmentally sustainable cooling alternatives that reduce reliance on conventional refrigerant-based systems. Precision manufacturing facilities across Germany, France, and the Netherlands are integrating thermoelectric cooling technologies into advanced production workflows. More than 18% of newly deployed high-precision industrial monitoring systems now incorporate thermoelectric temperature stabilization components. Market participants are investing in automation, digital manufacturing platforms, and next-generation thermal materials to enhance operational performance and equipment reliability.

Germany Market Outlook: Germany leads the European market through its strong industrial manufacturing base, advanced automotive engineering ecosystem, and globally competitive automation sector. The country's leadership in industrial electronics and optical technologies continues generating significant demand for high-performance thermal control systems. More than 25% of Europe’s industrial automation equipment production is concentrated in Germany, supporting sustained integration of thermoelectric technologies. Companies are emphasizing energy-efficient manufacturing processes, precision engineering capabilities, and technology partnerships to maintain industrial competitiveness.

Asia-Pacific dominates the global market with approximately 46.2% share, supported by large-scale electronics manufacturing, semiconductor production, medical device development, and optical communication infrastructure. The region serves as the primary production hub for thermoelectric modules, benefiting from integrated supply chains and extensive component manufacturing networks. Electronics production clusters across China, Japan, South Korea, and Taiwan continue driving deployment volumes. More than 55% of global semiconductor packaging and testing activities are concentrated within Asia-Pacific, reinforcing demand for advanced thermal management solutions. Manufacturers are expanding capacity, strengthening export capabilities, and investing in automation to support increasing performance requirements.

China Market Outlook: China remains the most influential country market due to its dominant electronics manufacturing ecosystem and extensive thermoelectric module production capacity. The country accounts for roughly 38% of global thermoelectric manufacturing capacity and maintains a significant advantage in supply-chain integration. Strong investments in semiconductor self-sufficiency, industrial automation, and advanced electronics continue supporting deployment growth. Chinese manufacturers are expanding production efficiency, developing higher-performance materials, and increasing localization across critical component supply chains to strengthen global competitiveness.

South America contributes approximately 4.6% of global market activity, with demand centered around industrial electronics, laboratory equipment, healthcare technologies, and telecommunications infrastructure. Growing modernization of manufacturing operations is increasing interest in compact thermal management systems that support operational reliability. While infrastructure limitations and import dependency remain constraints, industrial digitalization programs are encouraging adoption of precision cooling technologies. Investment activity in industrial automation projects increased by nearly 12% across key economies during the past two years. Companies are pursuing distribution partnerships and localized support networks to improve equipment accessibility and reduce deployment lead times.

Brazil Market Outlook: Brazil represents the largest market in South America due to its diversified industrial base, expanding healthcare infrastructure, and growing electronics assembly sector. Industrial modernization programs continue supporting demand for temperature-sensitive equipment used in manufacturing and diagnostics. Nearly 45% of the region’s industrial electronics activity is concentrated in Brazil, creating favorable deployment conditions for thermoelectric cooling solutions. Local enterprises are strengthening technical service capabilities and collaborating with international suppliers to improve product availability and application expertise.

Middle East & Africa accounts for approximately 2.9% of global market demand but is emerging as the fastest-evolving regional opportunity. Expanding digital infrastructure, healthcare modernization programs, telecommunications investments, and industrial diversification initiatives are increasing adoption of precision cooling technologies. Data center development and advanced diagnostic equipment deployments are creating new operational requirements for compact thermal management solutions. More than 15% growth in regional data center capacity expansion projects has strengthened demand for supporting thermal control systems. Market participants are leveraging strategic partnerships and infrastructure-focused investments to improve deployment capabilities and technical expertise.

Saudi Arabia Market Outlook: Saudi Arabia leads regional market development through large-scale economic diversification initiatives, digital infrastructure expansion, and healthcare modernization programs. Government-backed industrial development strategies continue attracting technology investments that require advanced thermal management capabilities. More than 20 major smart infrastructure and technology projects are currently supporting demand for precision electronic systems across the country. Companies are increasing local partnerships, establishing regional service networks, and aligning with national industrial development priorities to capture long-term market opportunities.

The competitive landscape is led by global thermoelectric specialists including Ferrotec Holdings Corporation, Laird Thermal Systems, KELK Ltd., TEC Microsystems GmbH, and Crystal Ltd.. Global technology leaders compete directly with cost-focused Asian manufacturers, while OEM-integrated suppliers compete against specialized module innovators for high-value semiconductor, medical, and photonics contracts. The top five players collectively control approximately 45% of global market activity. Competition is increasingly determined by thermal efficiency, miniaturization capability, supply-chain control, and application-specific customization rather than pricing alone. Advanced module performance has improved by nearly 10–15% in recent product generations, while automated manufacturing has reduced production cycle times by approximately 20%. Companies are expanding regional manufacturing footprints, securing material supply agreements, and investing in advanced thermoelectric materials. The competitive shift is moving toward vertically integrated supply chains and high-performance cooling architectures. Material sourcing remains a critical barrier. Winning requires superior thermal performance, resilient supply networks, and deep application engineering expertise.

Laird Thermal Systems

TEC Microsystems GmbH

Crystal Ltd.

Komatsu Ltd.

RMT Ltd.

TE Technology Inc.

Thermonamic Electronics (Jiangxi) Corp., Ltd.

Same Sky

Guangdong Fuxin Technology Co., Ltd.

Merit Technology Group

Phononic Inc.

Kryotherm

Current technology development is centered on advanced bismuth telluride materials, automated module manufacturing, and precision thermal control electronics. New-generation thermoelectric materials deliver 10–15% higher cooling efficiency than earlier designs while reducing power consumption in compact electronics applications. More than 35% of newly deployed high-performance optical communication systems now utilize precision thermoelectric temperature stabilization. This enables improved device reliability, lower maintenance requirements, and tighter operational tolerances in semiconductor and photonics environments.

Emerging technologies include AI-enabled thermal management, nanostructured thermoelectric materials, and high-density micro-Peltier architectures. Compared with conventional thermoelectric designs, next-generation micro-cooling platforms provide up to 20% greater heat-pumping density while occupying significantly smaller footprints. Adoption is accelerating across laser systems, LiDAR platforms, advanced diagnostics, and edge computing hardware. Companies with strong semiconductor and photonics exposure benefit most because thermal precision increasingly influences product performance and operational stability.

Disruptive innovation is emerging through advanced thermoelectric materials, transverse thermoelectric architectures, and integrated smart-cooling platforms. Between 2026 and 2028, deployment of intelligent thermal monitoring systems is expected to expand by more than 25% across precision electronics environments. Businesses investing early in automated manufacturing, advanced materials engineering, and AI-driven thermal optimization will gain stronger operational efficiency, improved product differentiation, and enhanced competitiveness in increasingly temperature-sensitive applications.

April 2025 – KELK Ltd. launched the KELGEN G-Unit KSGU400 thermoelectric power-generation unit for industrial waste-heat recovery applications. The system converts unused process heat into reusable electricity, strengthening industrial energy-efficiency initiatives and expanding thermoelectric deployment beyond cooling applications. Source: www.kelk.komatsu

November 2024 – Laird Thermal Systems introduced the OptoTEC MBX Series micro thermoelectric coolers featuring heat-pumping densities up to 43 W/cm² and temperature differentials reaching 82°C. The launch strengthened the company's position in optical communications, LiDAR, and AI-driven photonics infrastructure.

June 2024 – Laird Thermal Systems launched the SuperCool X Series thermoelectric assemblies with cooling performance improvements of approximately 10% over previous models. The development enhanced compact thermal management capabilities for analytical instrumentation and medical diagnostic systems requiring refrigerant-free operation.

March 2025 – National Institute for Materials Science (NIMS) announced a thermoelectric permanent magnet technology achieving a record power density of 56.7 mW/cm². The breakthrough advances next-generation thermoelectric module performance and supports future high-efficiency cooling and energy-harvesting applications.

This report provides comprehensive analysis of the global Peltier Cooling Modules market across major module types, application categories, end-user industries, and regional markets. The assessment covers single-stage, multi-stage, micro, and industrial-grade thermoelectric modules alongside key applications including electronics, healthcare, industrial automation, aerospace, photonics, and advanced communication systems. Regional evaluation spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with detailed country-level competitive and operational insights.

The study examines technology adoption trends, manufacturing concentration, supply-chain dynamics, deployment patterns, and innovation strategies influencing market evolution between 2026 and 2033. Analysis includes competitive positioning of leading manufacturers, emerging material technologies, thermal management advancements, and investment priorities shaping future demand. More than 40% of market activity remains concentrated within electronics and semiconductor applications, while healthcare and precision diagnostics continue expanding adoption. The report supports strategic decision-making related to market entry, capacity expansion, partnership development, product innovation, competitive benchmarking, and long-term growth planning.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 435.6 Million |

| Market Revenue (2033) | USD 680.8 Million |

| CAGR (2026–2033) | 5.74% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Ferrotec Holdings Corporation; Laird Thermal Systems; KELK Ltd.; TEC Microsystems GmbH; Crystal Ltd.; Komatsu Ltd.; RMT Ltd.; TE Technology Inc.; Thermonamic Electronics (Jiangxi) Corp., Ltd.; Same Sky; Guangdong Fuxin Technology Co., Ltd.; Merit Technology Group; Phononic Inc.; Kryotherm |

| Customization & Pricing | Available on Request (10% Customization Free) |