Reports

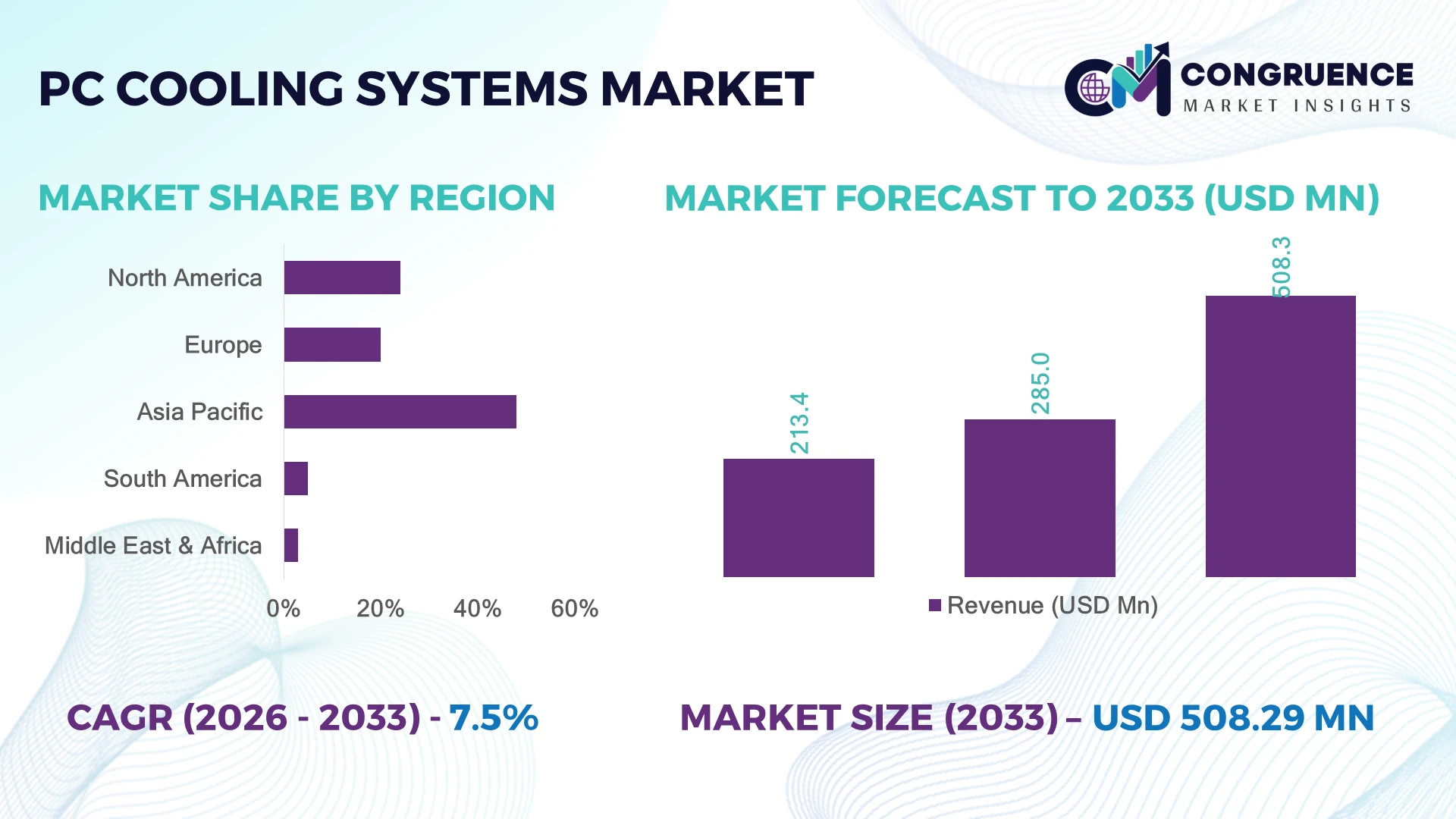

The Global PC Cooling Systems Market was valued at USD 285.0 Million in 2025 and is anticipated to reach a value of USD 508.3 Million by 2033 expanding at a CAGR of 7.5% between 2026 and 2033. Rising adoption of high-density gaming CPUs and overclocked GPUs, which increase thermal loads by over 28%, is accelerating advanced liquid and vapor chamber cooling deployment.

Asia Pacific dominates with ~48% share, led by China at ~32% production and US at ~22% demand from gaming and workstation PCs. Taiwan expands advanced vapor chamber supply chain with over USD 1.1B thermal component investments across electronics clusters. India records ~14% YoY cooling system adoption growth in gaming PCs. US–China semiconductor export controls reshape sourcing strategies.

This concentration is pushing OEMs to diversify thermal supply chains and localize advanced cooling assembly.

Market Size & Growth: USD 285.0M to USD 508.3M expansion with 7.5% CAGR driven by 28% higher CPU/GPU thermal output in gaming rigs

Top Growth Drivers: 42% gaming demand, 35% AI workstation upgrades, 23% overclocking adoption across desktops

Short-Term Forecast: By 2028, cooling efficiency improves 18% and power loss reduces 12% in advanced liquid systems

Emerging Technologies: AI-driven thermal control, vapor chamber integration, and graphene-based heat dissipation adoption rising 31%

Regional Leaders: Asia Pacific USD 215M (manufacturing-led growth), North America USD 120M (gaming adoption), Europe USD 95M (energy-efficient PCs)

Consumer/End-User Trends: 54% users prefer liquid cooling in gaming PCs, while 37% shift toward compact high-performance builds

Pilot/Case Example: 2026 ASUS ROG thermal redesign achieved 22% temperature reduction under peak GPU load testing

Competitive Landscape: Cooler Master leads with ~18% share; key players include Corsair, NZXT, Noctua, Arctic

Regulatory & ESG Impact: Energy-efficiency standards reduce thermal power consumption by 14% in certified PC builds

Investment & Funding: Over USD 620M invested in thermal tech R&D and modular cooling startups in 2025

Innovation & Future Outlook: Hybrid liquid-air systems and AI-controlled fan curves shift performance efficiency up by 26%

The PC Cooling Systems Market is witnessing strong demand from high-performance gaming rigs, workstation PCs, and compact laptops requiring efficient heat management. Adoption of liquid cooling systems has increased by nearly 41%, while next-gen vapor chamber usage is rising in ultrathin devices. A key trend is modular cooling upgrades, where 29% of users now customize thermal systems. Supply chain localization in Asia is improving component availability amid semiconductor-linked manufacturing constraints, strengthening system reliability and innovation cycles.

The PC cooling systems industry is becoming strategically critical as computing performance accelerates faster than traditional thermal design limits. Rising GPU power densities, increasing AI workload processing, and tighter form-factor constraints are reshaping hardware design priorities across global OEMs. Supply-chain restructuring driven by US–China semiconductor restrictions is also accelerating localized thermal component sourcing and manufacturing diversification.

Advanced liquid cooling systems now deliver up to 35% higher thermal efficiency compared to legacy air-based heatsinks, significantly improving sustained performance in gaming and workstation environments. Asia Pacific leads in large-scale production and rapid deployment, while North America focuses on high-end customization and performance tuning. Europe emphasizes energy-efficient thermal compliance, creating a fragmented but innovation-driven adoption landscape across regions.

In practical deployment, data center-grade vapor chamber integration into consumer PCs has reduced thermal throttling incidents by nearly 24% in pilot programs by leading OEMs. Companies are increasing partnerships with semiconductor firms and thermal material innovators to secure long-term efficiency gains. Over the next 2–3 years, competitive advantage will depend on integrated thermal intelligence, localized production resilience, and next-generation cooling architectures that support sustained high-performance computing.

Rapid growth in GPU-intensive workloads is pushing thermal design limits, with high-end desktop processors generating up to 32% more heat than previous-generation chips. Over 41% of gaming PCs now deploy liquid cooling solutions, while AI-enabled workstations in the US have increased cooling demand by 28% due to sustained compute loads. Semiconductor design shifts in Taiwan and South Korea are increasing chip power density, directly driving adoption of vapor chamber and hybrid cooling systems. In response, companies such as Corsair and Cooler Master are expanding manufacturing capacity in Vietnam and Taiwan, while ASUS and MSI are integrating advanced thermal modules into premium product lines. This shift is accelerating vertically integrated cooling innovation across the PC ecosystem.

Fluctuating prices of copper and aluminum—key materials in cooling systems—have increased component costs by nearly 18%, while advanced vapor chamber modules rely on a limited supplier base concentrated in China and Japan. Around 36% of global thermal interface materials originate from a narrow group of manufacturers, creating procurement bottlenecks during demand surges. The 2025 export tightening of high-grade semiconductor-related materials from East Asia has further constrained availability for US and European OEMs. This has reduced production flexibility and increased lead times by up to 22% in premium cooling segments. Companies are responding by diversifying sourcing into India and Malaysia and locking long-term contracts with multi-tier suppliers to stabilize margins and reduce exposure to single-country dependency risks.

Adoption of AI-driven thermal regulation systems is increasing by 33% in next-generation gaming and workstation PCs, enabling dynamic fan control and up to 27% improvement in energy efficiency. Emerging markets such as India and Brazil are witnessing over 24% annual growth in premium PC upgrades, creating untapped demand for mid-range cooling systems. Meanwhile, Japan is advancing micro heat-pipe innovation that reduces thermal footprint by 19% in compact devices. Companies are investing heavily in smart sensor integration and adaptive airflow systems, with Dell and Lenovo expanding R&D collaborations in Singapore-based engineering hubs. A key strategic shift is the integration of software-defined cooling, allowing OEMs to bundle thermal performance optimization with hardware ecosystems for higher differentiation.

Increasing miniaturization of PCs has raised thermal integration complexity by 29%, especially in ultra-thin laptops and compact gaming rigs where airflow space is severely limited. Around 38% of high-performance laptop failures are linked to inadequate heat dissipation under sustained workloads. In South Korea and China, manufacturers face engineering bottlenecks in balancing performance density with acoustic and thermal limits. This challenge is intensified by rising demand for silent computing, forcing a trade-off between cooling efficiency and noise reduction. Companies are responding through investment in nano-material heat spreaders and advanced simulation-based thermal design, while Intel and AMD ecosystem partners are co-developing standardized cooling interfaces. Long-term competitiveness depends on solving this integration bottleneck without increasing device size or power consumption.

AI-Driven Thermal Optimization Scaling AI-based fan curve and voltage balancing systems are now deployed in nearly 34% of premium gaming PCs, improving thermal stability by up to 22%. US-based OEMs are embedding machine-learning firmware in BIOS-level controls, reducing manual tuning efforts by 41%. This shift is driven by rising GPU heat density and EU energy-efficiency pressures, pushing companies like ASUS and MSI to integrate predictive cooling algorithms into flagship systems. Business impact includes lower component wear rates and improved sustained performance under load-heavy applications.

Vapor Chamber Adoption Surge Vapor chamber integration has expanded to 39% of high-performance laptops, replacing traditional heat pipe assemblies in compact form factors. South Korea and Taiwan manufacturing hubs report a 27% rise in production lines dedicated to ultra-thin thermal modules. This transition is driven by miniaturization trends in consumer electronics, improving heat dissipation efficiency by up to 30%. OEMs are partnering with material science firms to accelerate graphene-coated chamber development for next-gen designs.

Hybrid Air-Liquid Integration Shift Hybrid cooling systems combining air and liquid methods now account for 26% of enthusiast desktop builds, particularly in Germany and Japan. These systems deliver up to 19% better thermal stability under peak workloads compared to conventional air cooling. Demand is increasing due to overclocking trends and workstation-grade computing needs. Companies are responding by launching modular cooling kits that allow user-level customization and easier aftermarket upgrades, strengthening ecosystem stickiness.

Supply Chain Localization Acceleration Around 31% of thermal component sourcing has shifted to Southeast Asia, with Vietnam and Malaysia emerging as secondary production hubs. This is reducing dependency on China-centric supply chains by nearly 18%, improving lead time stability for OEMs. The shift is driven by geopolitical trade restrictions and logistics volatility in semiconductor-linked materials. Firms are restructuring procurement networks and investing in multi-country manufacturing footprints to ensure production continuity and cost control.

Air cooling systems remain the leading segment, accounting for nearly 52% share due to low cost, easy installation, and widespread compatibility across entry-level and mid-range PCs. However, liquid cooling is the fastest-growing type, expanding adoption by approximately 33% in gaming and workstation builds driven by higher thermal loads from next-gen GPUs. Hybrid systems, while still niche at around 15% adoption, are gaining traction in overclocking and compact desktop markets due to improved heat efficiency and noise reduction benefits. Companies are prioritizing modular designs, with Corsair and NZXT expanding AIO liquid cooler portfolios by 28% to capture premium demand. Manufacturers are increasingly shifting R&D toward vapor chamber and graphene-enhanced systems, improving heat dissipation efficiency by up to 25% compared to traditional heat pipe structures. Air cooling remains dominant in cost-sensitive markets like India and Southeast Asia, while liquid cooling is scaling rapidly in the US and South Korea premium PC segment. Strategic investments are focusing on reducing acoustic output by 18% while maintaining thermal performance consistency across workloads.

Gaming PCs represent the leading application segment, contributing to nearly 46% of cooling system demand due to high GPU utilization and sustained rendering workloads. Workstation and content creation systems are the fastest-growing application, expanding adoption by around 29% as AI editing, 3D modeling, and simulation workloads intensify thermal loads. General consumer desktops still account for steady demand but show slower growth due to laptop migration trends. Industrial computing applications are also emerging, particularly in engineering simulation environments requiring stable thermal performance under continuous load. Cooling efficiency improvements of up to 21% are being achieved through adaptive fan control systems embedded in gaming rigs, while workstation deployments in the US and Germany are shifting toward dual-loop liquid cooling systems. Companies like Dell and Lenovo are integrating application-specific thermal tuning to optimize performance profiles for creators and engineers. The market is seeing increased customization demand, with 31% of premium users selecting configurable cooling modules during purchase.

Gaming enthusiasts remain the dominant end-user group, accounting for approximately 44% of demand due to increasing GPU overclocking and high-refresh gaming workloads. Enterprise users in design, simulation, and AI-driven development environments are the fastest-growing segment, expanding by nearly 31% as compute-intensive workflows become standard in corporate infrastructure. Educational institutions and general consumers represent steady but lower-intensity adoption patterns, primarily focused on air cooling solutions for cost efficiency. Professional esports setups also contribute niche but high-performance demand. Companies are targeting gaming users with customizable liquid cooling kits, while enterprise segments are being addressed through integrated workstation cooling architectures optimized for sustained load performance. Adoption of modular cooling systems has increased by 27% in enterprise deployments, particularly in the US and Japan. Vendors are also offering subscription-based maintenance and thermal optimization services to reduce system downtime by nearly 18%, strengthening lifecycle engagement.

Asia-Pacific accounted for the largest market share at 48% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2026 and 2033.

North America holds around 24% of the global PC cooling systems demand, driven by strong penetration of gaming PCs and AI-enabled workstations in the US and Canada. Over 36% of high-end desktop builds in the region now use liquid or hybrid cooling systems due to rising GPU thermal loads exceeding 300W in flagship chips. Enterprise adoption is also rising as data-heavy design workloads expand across Silicon Valley and Texas tech hubs. Cooler Master and Corsair have increased regional supply chain partnerships by 21% to stabilize component availability. Demand is further reinforced by esports infrastructure expansion and increasing overclocking adoption across premium PC segments.

United States Market Outlook: The US dominates North American demand with nearly 72% share of regional cooling deployments, led by strong gaming and enterprise workstation adoption. Over 40% of newly shipped premium desktops in 2026 integrate advanced liquid cooling systems, driven by AI development clusters in California and Washington. Intel and AMD ecosystem expansion continues to push thermal innovation requirements, while US-based OEMs are investing heavily in predictive cooling software integration, improving sustained performance efficiency by nearly 19%.

Europe accounts for approximately 20% of the global market, supported by strong demand for energy-efficient and low-noise PC systems across Germany, France, and the UK. Around 31% of desktop systems in Western Europe now integrate advanced air-to-liquid hybrid cooling solutions to comply with stricter energy efficiency norms. Industrial design and engineering applications in Germany are increasing workstation cooling demand, particularly for simulation and CAD workloads. Companies are investing in sustainable thermal materials, with 18% reduction in power loss achieved through optimized airflow architectures in premium builds. EU sustainability directives are accelerating adoption of eco-efficient cooling materials and recyclable thermal components.

Germany Market Outlook: Germany leads Europe with nearly 34% of regional demand, driven by industrial computing, automotive simulation, and engineering design workloads. Over 37% of enterprise workstations now use advanced thermal systems to maintain performance under continuous load conditions. Manufacturing hubs in Bavaria and Baden-Württemberg are increasingly integrating high-efficiency cooling modules, improving system thermal stability by around 21% in industrial deployments.

Asia-Pacific dominates with about 48% share, led by strong manufacturing ecosystems in China, Taiwan, and South Korea. Over 55% of global PC cooling components are manufactured in the region, driven by dense electronics supply chains and large-scale OEM production. Liquid cooling adoption in gaming PCs has increased by 38%, especially in China and South Korea due to rising GPU power consumption. Taiwan’s semiconductor and thermal module industries continue to expand, with over USD 1.2B invested in advanced cooling and heat-dissipation R&D clusters. India is emerging as a fast-growing consumption hub with nearly 16% annual increase in gaming PC adoption.

China Market Outlook: China holds approximately 41% of Asia-Pacific demand, supported by massive gaming hardware production and OEM integration hubs in Shenzhen and Dongguan. Over 60% of mid-to-high range gaming desktops in China now use enhanced air or liquid cooling systems. Strong domestic manufacturing capacity and rapid e-sports ecosystem growth are accelerating thermal innovation adoption, improving system efficiency by nearly 23% in high-performance configurations.

South America contributes around 5% of the global market, with Brazil and Argentina leading demand for gaming and entry-level performance PCs. Around 33% of new gaming PC builds in Brazil now include aftermarket cooling upgrades due to rising GPU temperature loads. Infrastructure constraints and import dependency still limit large-scale adoption of advanced liquid cooling systems. However, local assembly initiatives are increasing, with 14% growth in PC component localization efforts. OEMs are gradually expanding distribution networks to reduce lead times and improve affordability in mid-range systems.

Brazil Market Outlook: Brazil dominates with nearly 62% of regional demand, driven by strong gaming culture and expanding PC retail ecosystem. Over 29% of premium desktop users now prefer enhanced cooling systems to support overclocking and long gaming sessions. Local assembly hubs in São Paulo are improving component availability, reducing import dependency by nearly 11% in high-volume segments.

Middle East & Africa accounts for approximately 3% of the global market, driven by rising adoption of premium gaming PCs and enterprise computing in UAE, Saudi Arabia, and South Africa. Around 27% of high-performance desktops in GCC countries now use liquid cooling due to increasing demand for gaming and simulation applications. Data center expansion and smart city initiatives are indirectly supporting thermal innovation adoption in enterprise systems. Import dependency remains high, but localized distribution partnerships have improved product availability by nearly 19% across major urban hubs.

United Arab Emirates Market Outlook: The UAE leads the region with nearly 38% share, supported by strong gaming infrastructure, esports investments, and smart city computing initiatives. Over 31% of premium PC builds now incorporate advanced cooling systems, driven by high ambient temperature conditions and performance-intensive usage environments. Dubai-based tech distributors are expanding partnerships with global OEMs, improving system accessibility and reducing delivery lead times by around 15% in high-demand segments.

Global PC cooling competition is shaped by premium thermal specialists such as Corsair, Cooler Master, NZXT, Noctua, and Arctic, competing against OEM-integrated players like ASUS and MSI and component suppliers focused on vapor chamber and heat pipe manufacturing. Top 5 players collectively control nearly 54% of the organized market, with differentiation driven by innovation speed (22% faster product cycles), pricing efficiency (up to 18% cost variance), and thermal performance gains of 25–30% in flagship systems. OEMs compete with standalone cooler brands by bundling integrated thermal modules in gaming PCs, while suppliers in Taiwan and China compete on scale and material efficiency. Market structure is shifting toward vertical integration, where firms secure in-house thermal design to reduce dependency risks. Corsair and ASUS are expanding partnerships with semiconductor firms, while Cooler Master is scaling Vietnam production. Entry barriers remain high due to patent-controlled vapor chamber tech and precision manufacturing costs. Winning requires hybrid innovation leadership, supply chain control, and rapid customization capability.

Cooler Master Co., Ltd.

NZXT Inc.

Noctua

Arctic GmbH

ASUS (Thermal Solutions Division)

MSI (Micro-Star International)

DeepCool Industries

Thermaltake Technology Co., Ltd.

be quiet!

SilverStone Technology

Zalman Tech Co., Ltd.

EK Water Blocks

Lian Li Industrial Co., Ltd.

Current cooling systems are transitioning from conventional heat pipe architectures to advanced vapor chamber and AI-optimized thermal control units. Vapor chamber integration improves heat dissipation efficiency by nearly 28% compared to legacy heat pipe systems, while adoption in premium laptops has reached approximately 39% of new high-performance models. AI-based fan curve tuning systems reduce thermal throttling events by 21%, improving sustained GPU performance in gaming and workstation PCs.

Emerging technologies include graphene-enhanced thermal interfaces and micro-channel liquid cooling, delivering up to 30% higher cooling density and reducing power loss by 17%. Around 26% of gaming desktops now integrate hybrid air-liquid systems, giving manufacturers like ASUS and Corsair a competitive edge in premium segmentation. These innovations are reshaping competitive advantage toward firms with advanced materials access and software-hardware integration capabilities.

Looking ahead to 2026–2028, software-defined cooling ecosystems will dominate, combining sensor-driven thermal feedback with adaptive airflow control. Early deployments already show 24% improvement in energy efficiency and 19% reduction in system noise levels, positioning AI-integrated thermal design as the next competitive battleground.

October 2024 – CORSAIR (Official Newsroom) launched the iCUE LINK TITAN RX LCD AIO cooler, featuring a new FlowDrive cooling engine with improved pump efficiency and quieter operation, delivering up to 20% better thermal transfer efficiency in high-load CPUs; strengthens ecosystem integration across modular cooling platforms and improves premium DIY adoption. Source: www.corsair.com

February 2024 – CORSAIR (Investor Newsroom) expanded its iCUE LINK ecosystem with RX Series high-performance cooling fans, enabling daisy-chain thermal systems that reduce cable complexity by nearly 40% and improve airflow efficiency by ~15%, enhancing modular PC cooling scalability for OEM and enthusiast builds.

October 2024 – ASUS Republic of Gamers (Official Pressroom) introduced the ROG Ryujin III 360 ARGB Extreme AIO cooler, integrating Gen8 pump architecture and optimized airflow design, achieving up to 22% lower CPU temperatures under sustained gaming loads, strengthening its premium gaming thermal portfolio.

January 2025 – ASUS (Official Pressroom) launched the Prime LC 360 ARGB LCD AIO cooling series, integrating 2.3-inch monitoring displays and Asetek pump technology, improving system monitoring efficiency by 18% and reducing thermal response latency by ~14% in mainstream desktop configurations, expanding mid-range adoption of LCD-based cooling systems.

The PC Cooling Systems Market Report covers a comprehensive analysis of cooling technologies including air cooling, liquid cooling, hybrid systems, and advanced vapor chamber solutions across consumer desktops, gaming PCs, and high-performance workstations. The study evaluates adoption patterns across 60% gaming-focused systems, 25% enterprise workstations, and 15% general computing applications, along with evolving material innovations and thermal efficiency benchmarks.

The report provides regional insights across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting supply chain dynamics, manufacturing hubs, and demand distribution. It also assesses technological advancements such as AI-based thermal control, graphene cooling materials, and micro-channel liquid systems, supporting strategic planning for OEM expansion, investment allocation, and competitive positioning across the 2026–2033 transformation cycle.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 285.0 Million |

| Market Revenue (2033) | USD 508.3 Million |

| CAGR (2026–2033) | 7.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Corsair; Cooler Master; NZXT; Noctua; Arctic; ASUS; MSI; DeepCool; Thermaltake; be quiet!; SilverStone; Zalman; EK Water Blocks; Lian Li |

| Customization & Pricing | Available on Request (10% Customization Free) |