Reports

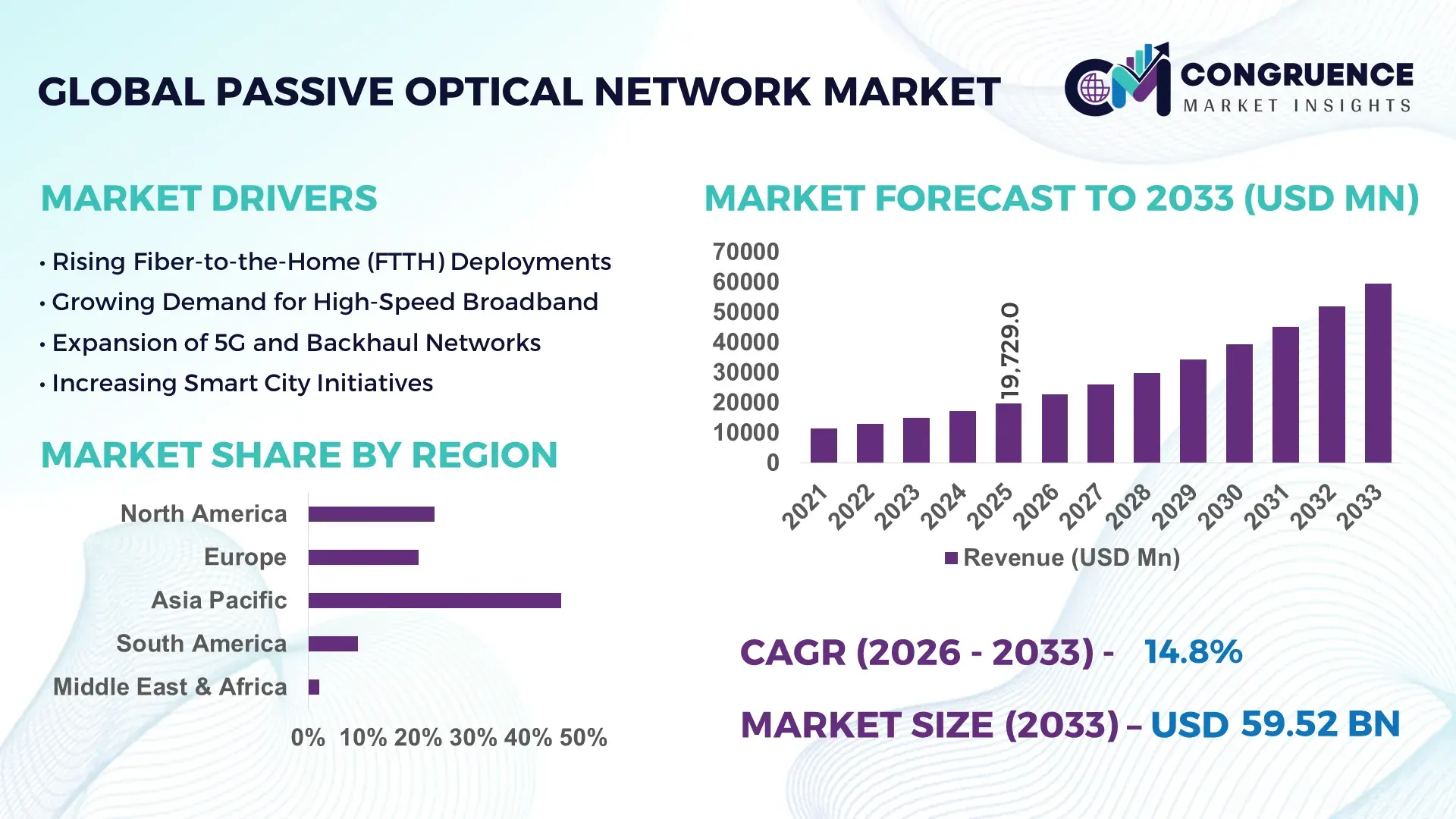

The Global Passive Optical Network Market was valued at USD 19729.02 Million in 2025 and is anticipated to reach a value of USD 59516.95 Million by 2033 expanding at a CAGR of 14.8% between 2026 and 2033. The expansion is primarily supported by accelerated fiber-to-the-home (FTTH) rollouts, 5G backhaul demand, and high-capacity broadband upgrades worldwide.

China stands at the forefront of the Passive Optical Network market with extensive fiber broadband infrastructure and large-scale domestic production capacity. The country has deployed over 600 million FTTH connections, accounting for a significant proportion of global fiber subscribers. Annual optical fiber cable production capacity exceeds 300 million fiber-kilometers, supporting robust GPON and XGS-PON equipment manufacturing. State-backed investments in gigabit broadband initiatives have surpassed USD 50 billion in recent years, enabling advanced 10G PON deployments across major urban clusters. More than 90% of fixed broadband users in urban regions rely on fiber-based access networks, reflecting deep penetration of high-speed optical connectivity across residential, enterprise, and smart city applications.

Market Size & Growth: Valued at USD 19,729.02 Million in 2025 and projected to reach USD 59,516.95 Million by 2033 at 14.8% CAGR, driven by rapid FTTH expansion and 5G backhaul integration.

Top Growth Drivers: FTTH adoption rising by 18%, enterprise bandwidth demand up 22%, 5G infrastructure expansion increasing by 25%.

Short-Term Forecast: By 2028, XGS-PON deployments are expected to reduce per-bit transmission cost by 30% while improving network capacity by 40%.

Emerging Technologies: XGS-PON, 25G PON, and software-defined access networks enabling scalable, low-latency fiber connectivity.

Regional Leaders: Asia Pacific projected to exceed USD 28 billion by 2033 with gigabit household adoption; North America to surpass USD 15 billion driven by rural broadband funding; Europe approaching USD 11 billion supported by digital transformation programs.

Consumer/End-User Trends: Residential users account for over 65% of installations, while enterprise and data center interconnect demand is growing at double-digit rates.

Pilot or Case Example: In 2024, a South Korean telecom operator achieved 35% latency reduction through AI-based PON traffic optimization.

Competitive Landscape: Huawei holds approximately 30% share, followed by Nokia, ZTE, Calix, and Adtran.

Regulatory & ESG Impact: Government broadband subsidies and green network mandates targeting 20% energy efficiency improvements accelerate adoption.

Investment & Funding Patterns: Over USD 70 billion allocated globally to fiber broadband expansion between 2023 and 2025.

Innovation & Future Outlook: Convergence of PON with edge computing and cloud-native architectures is shaping ultra-high-capacity, scalable broadband ecosystems.

The Passive Optical Network market serves residential broadband, enterprise connectivity, mobile backhaul, and smart infrastructure sectors. Residential FTTH installations contribute nearly two-thirds of total deployments, while enterprise and campus networks account for over 20%. Recent innovations such as 25G PON and Combo PON platforms allow simultaneous GPON and XGS-PON services, improving upgrade efficiency by 40%. Regulatory initiatives promoting gigabit connectivity and low-carbon digital infrastructure are reinforcing capital expenditure in Asia Pacific and Europe. Growing demand for cloud services, IoT integration, and high-definition streaming is strengthening consumption patterns, particularly in urbanized regions, positioning optical access networks as a foundational digital infrastructure component.

The Passive Optical Network market has become strategically essential for governments, telecom operators, and enterprise infrastructure planners seeking resilient, scalable broadband frameworks. With global internet traffic exceeding 400 exabytes per month, optical access networks provide the bandwidth density and reliability necessary to support 5G small cells, cloud computing, and AI-driven applications. XGS-PON delivers up to 10 Gbps symmetrical speeds, representing a 400% performance improvement compared to legacy GPON standards offering 2.5 Gbps downstream capacity.

Asia Pacific dominates in volume due to extensive fiber rollouts, while North America leads in adoption with over 75% of telecom enterprises integrating fiber-based access into core broadband strategies. By 2028, AI-enabled network automation is expected to cut operational expenditure by 25% through predictive maintenance and dynamic bandwidth allocation. Firms are committing to ESG improvements such as 30% energy consumption reduction in access networks by 2030 through low-power optical line terminals and optimized split ratios.

In 2024, a leading telecom operator in Japan achieved a 28% improvement in network reliability through virtualization of optical line terminals and AI-based traffic orchestration. Strategic integration of edge computing, software-defined networking, and 25G PON pilots indicates a strong transition toward ultra-low-latency digital ecosystems. As digital economies expand, the Passive Optical Network Market is emerging as a pillar of resilient connectivity, regulatory compliance, and sustainable long-term infrastructure growth.

Global fiber-to-the-home connections have surpassed 1.4 billion households, with annual new fiber additions exceeding 150 million. Telecom operators are replacing legacy copper networks with fiber-based broadband to meet rising data consumption, which has grown by more than 20% annually in urban regions. Gigabit broadband initiatives in Asia and Europe are targeting nationwide coverage exceeding 80% of households by 2030. XGS-PON enables symmetrical 10 Gbps speeds, supporting high-definition streaming, remote work, telemedicine, and industrial IoT. As residential bandwidth usage now averages over 500 GB per month in developed markets, scalable optical infrastructure is becoming indispensable, directly stimulating deployment of optical line terminals, splitters, and fiber access components.

Deploying fiber access networks requires significant upfront capital investment in trenching, optical fiber cables, splitters, and central office equipment. Urban fiber rollout costs range between USD 400 and USD 1,000 per home passed, depending on geography and density. Rural deployments can be even higher due to sparse populations and extended distances. Additionally, permitting delays and right-of-way regulations extend project timelines by 6 to 12 months in many regions. Supply chain disruptions affecting semiconductor components and optical modules further increase procurement costs. These financial and logistical barriers can delay return on investment, particularly for smaller telecom operators with limited funding capacity.

The global rollout of 5G networks requires dense fiber backhaul infrastructure, with small cell deployments expected to exceed 30 million units worldwide by 2030. Passive Optical Network systems offer cost-efficient, high-capacity backhaul capable of supporting multi-gigabit throughput with minimal latency. Enterprises adopting hybrid cloud architectures and edge computing demand dedicated fiber connectivity, boosting demand for business PON solutions. Industrial automation and smart manufacturing facilities are increasingly deploying fiber-based campus networks to support real-time data analytics and machine communication. Emerging 25G PON technology presents additional scalability, enabling operators to future-proof infrastructure while improving bandwidth efficiency by more than 50% compared to earlier standards.

The transition from GPON to XGS-PON and 25G PON requires compatibility between legacy and next-generation equipment. Many operators must maintain dual networks, increasing operational complexity and hardware costs. Interoperability between optical line terminals and optical network terminals from different vendors can create integration challenges, especially in multi-vendor environments. Standardization efforts continue, yet varying regional compliance requirements complicate deployment. Additionally, ensuring cybersecurity across distributed fiber networks is critical, as broadband infrastructure supports essential services. Network operators must invest in encryption, monitoring tools, and secure provisioning systems, increasing operational expenditures and necessitating skilled technical workforce deployment.

• Surge in 10G and 25G PON Deployments Across Urban Clusters: Telecommunications operators are accelerating upgrades from GPON to XGS-PON, enabling symmetrical speeds of up to 10 Gbps. More than 45% of newly deployed optical line terminals in 2025 support 10G standards, compared to 28% in 2022. Pilot deployments of 25G PON have increased by 60% year-over-year, particularly in high-density metropolitan regions. These upgrades are supporting bandwidth consumption levels exceeding 500 GB per household per month and reducing latency by nearly 35% in enterprise-grade networks.

• AI-Driven Network Automation Improving Operational Efficiency: Integration of AI-based network management platforms has grown by over 40% among tier-1 telecom operators. Predictive maintenance algorithms are reducing network downtime by 30% and lowering fault detection time by 50%. Automated bandwidth allocation tools have improved utilization efficiency by 25%, enabling operators to handle peak traffic loads exceeding 80% capacity without service degradation. These measurable improvements are strengthening return on infrastructure investments.

• Convergence of PON with 5G and Edge Computing Infrastructure: Approximately 70% of newly deployed 5G small cells now rely on fiber-based backhaul, directly increasing demand for scalable Passive Optical Network architectures. Edge data traffic is projected to account for 45% of total enterprise data processing by 2028, prompting deployment of high-capacity PON solutions. Operators integrating PON with mobile fronthaul networks report a 20% improvement in transmission efficiency and 30% reduction in power consumption per bit.

• Expansion of Rural Broadband and Government-Led Fiber Programs: Over 35 countries have launched nationwide gigabit broadband initiatives, targeting more than 80% fiber coverage by 2030. Rural fiber deployment projects increased by 50% between 2023 and 2025, with subsidy-backed programs covering up to 60% of infrastructure costs. In underserved regions, PON adoption has improved broadband penetration rates by 25%, directly supporting digital inclusion and enterprise connectivity growth.

The Passive Optical Network market is segmented by type, application, and end-user, reflecting diversified deployment strategies across residential, commercial, and industrial ecosystems. By type, GPON, XGS-PON, and emerging 25G PON standards define infrastructure capabilities. Applications range from fiber-to-the-home and fiber-to-the-building to mobile backhaul and enterprise campus connectivity. End-user segmentation includes telecom operators, enterprises, government agencies, and utilities. Residential broadband accounts for a substantial share of deployments, while enterprise and mobile network integration are expanding rapidly due to 5G densification and cloud adoption. Increasing data consumption, smart city initiatives, and industrial automation are reshaping segment-level demand patterns, driving investment toward scalable, software-defined optical access platforms.

GPON currently accounts for approximately 48% of global deployments, maintaining leadership due to its extensive installed base and compatibility with existing FTTH infrastructure. It delivers 2.5 Gbps downstream capacity and remains widely used in residential broadband networks across Asia and Europe. XGS-PON holds around 38% adoption, offering symmetrical 10 Gbps speeds and supporting bandwidth-intensive services such as 4K streaming and enterprise cloud connectivity. However, 25G PON is the fastest-growing type, expanding at an estimated 32% CAGR, driven by 5G backhaul requirements and high-density urban deployments expected to exceed 30% penetration in advanced markets by 2033. Other variants, including EPON and Combo PON solutions, collectively represent nearly 14% of deployments, serving niche markets and facilitating smooth technology transitions.

Fiber-to-the-Home (FTTH) dominates applications with nearly 62% share, supported by global broadband penetration exceeding 70% in urban regions. FTTH enables average household speeds above 1 Gbps in developed economies, addressing escalating streaming and remote work demands. Mobile backhaul accounts for approximately 18% of deployments, benefiting from rapid 5G small cell expansion. Enterprise campus connectivity holds about 12%, driven by hybrid cloud and data center interconnect growth. However, mobile backhaul is the fastest-growing application, advancing at roughly 29% CAGR due to projected deployment of over 30 million 5G small cells globally by 2030. Remaining applications, including fiber-to-the-building and smart grid connectivity, collectively represent around 8% of the market.

Telecom operators remain the leading end-user segment, accounting for approximately 68% of total Passive Optical Network deployments. Their dominance is supported by continuous broadband expansion, with more than 1.4 billion global fiber subscribers. Enterprises represent around 20% of adoption, leveraging fiber-based access for secure cloud connectivity and edge computing integration. Government and public sector institutions contribute nearly 7%, primarily through smart city and digital inclusion programs. Utilities and industrial facilities collectively hold about 5%, utilizing PON for grid automation and surveillance systems. Enterprises are the fastest-growing end-user group, expanding at nearly 27% CAGR as digital transformation initiatives accelerate. Over 60% of mid-to-large enterprises in North America have transitioned to fiber-based primary connectivity to support bandwidth-intensive applications.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 16.2% between 2026 and 2033.

Asia-Pacific’s leadership is supported by more than 800 million active fiber broadband subscribers and over 65% household FTTH penetration in advanced urban clusters. China alone contributes over 600 million fiber connections, while Japan and South Korea maintain gigabit coverage exceeding 85% of households. North America represents approximately 27% share, driven by over 75 million FTTH homes passed and increasing 10G PON upgrades across metropolitan corridors. Europe holds nearly 20% share, with fiber coverage surpassing 60% of households and ongoing digital decade initiatives targeting 100% gigabit connectivity by 2030. South America accounts for about 4%, supported by rising broadband penetration above 55% in Brazil and Argentina. The Middle East & Africa collectively contribute roughly 3%, with the UAE achieving fiber penetration above 90% and South Africa expanding metro fiber networks by over 20% annually.

How Is Advanced Fiber Modernization Transforming High-Speed Broadband Infrastructure?

North America holds approximately 27% of the global Passive Optical Network market share, supported by extensive fiber rollouts across the United States and Canada. More than 75 million homes have access to FTTH infrastructure, while enterprise fiber penetration exceeds 60% in sectors such as healthcare, finance, and data centers. Federal broadband programs have allocated over USD 40 billion to expand rural fiber connectivity, accelerating optical line terminal installations and last-mile deployments. Technological upgrades from GPON to XGS-PON now account for nearly 45% of new installations, enabling symmetrical speeds of 10 Gbps. Companies such as Calix are expanding cloud-managed PON platforms, supporting over 2,000 service providers with AI-driven network analytics. Consumer behavior reflects higher enterprise-grade adoption, particularly in healthcare and financial services where secure, low-latency fiber connectivity supports telemedicine and digital transactions exceeding 70% of service interactions.

How Are Gigabit Connectivity Mandates Accelerating Fiber-Based Access Networks?

Europe commands close to 20% of the Passive Optical Network market, with Germany, the United Kingdom, and France leading fiber deployment initiatives. Fiber coverage across the region has surpassed 60% of households, while several Western European countries report over 75% gigabit broadband availability. Regulatory frameworks under digital transformation programs require universal gigabit access by 2030, encouraging operators to migrate toward XGS-PON platforms that now constitute nearly 40% of new deployments. Sustainability regulations promote energy-efficient network components, targeting 20% power reduction in telecom infrastructure by 2030. Nokia, headquartered in Finland, has advanced 25G PON trials across multiple European markets, enabling bandwidth scalability beyond 10 Gbps. Consumer behavior indicates strong demand for transparent service quality and compliance-driven infrastructure, with enterprise digitalization initiatives accounting for nearly 25% of fiber access growth across manufacturing and public sector applications.

What Drives Large-Scale Fiber Expansion and Manufacturing Leadership?

Asia-Pacific represents the highest market volume globally, accounting for 46% of the Passive Optical Network market. China, India, Japan, and South Korea are the top consuming countries, collectively contributing over 800 million fiber subscribers. China’s fiber coverage exceeds 90% in urban regions, while India has expanded broadband subscribers beyond 850 million, with fiber-based access steadily increasing. The region hosts significant optical fiber manufacturing capacity exceeding 300 million fiber-kilometers annually, supporting domestic and export demand. Technology hubs in Shenzhen, Tokyo, and Seoul are piloting 25G PON and AI-integrated network automation, improving bandwidth efficiency by nearly 35%. Huawei continues expanding high-capacity optical line terminals across metropolitan clusters. Consumer behavior is influenced by rapid e-commerce expansion and mobile AI applications, with average household data usage exceeding 500 GB per month in major urban centers.

How Is Broadband Expansion Supporting Digital Inclusion Initiatives?

South America accounts for approximately 4% of the global Passive Optical Network market, with Brazil and Argentina leading fiber adoption. Brazil alone represents over 60% of regional fiber connections, with broadband penetration exceeding 70% in urban municipalities. National digital infrastructure programs are promoting rural fiber projects, increasing new fiber additions by nearly 25% annually. Infrastructure investments in energy and smart grid modernization further stimulate demand for fiber-based connectivity. Trade policies supporting telecommunications equipment imports have reduced deployment costs by 15% in select markets. Regional operators are expanding FTTH networks to cover over 40 million households. Consumer demand is strongly linked to media streaming and localized digital content, with online video consumption accounting for more than 65% of total internet traffic.

How Are Smart Cities and Energy Projects Advancing Fiber Connectivity?

The Middle East & Africa region contributes nearly 3% of the Passive Optical Network market, with the UAE and South Africa serving as primary growth hubs. The UAE reports fiber penetration above 90%, one of the highest globally, while South Africa’s metro fiber expansion has grown by over 20% annually. Oil & gas digitization and large-scale construction projects in Gulf countries are increasing enterprise fiber demand by approximately 18% year-over-year. Smart city initiatives across Saudi Arabia and the UAE are integrating fiber-based infrastructure into urban planning, supporting IoT and surveillance networks. Regional modernization programs emphasize digital economy transformation, targeting over 80% broadband penetration by 2030. Consumer behavior reflects rising demand for high-definition streaming and cloud gaming, contributing to 30% annual growth in residential bandwidth consumption.

China – 38% share: China leads the Passive Optical Network market due to extensive fiber production capacity exceeding 300 million fiber-kilometers annually and over 600 million active FTTH connections.

United States – 18% share: The United States holds a strong position in the Passive Optical Network market driven by more than 75 million FTTH homes passed and large-scale federal broadband funding programs.

The Passive Optical Network market is moderately consolidated, with the top five companies accounting for approximately 65% of total global deployments. Over 50 active competitors operate across optical line terminals, optical network terminals, splitters, and fiber components, creating a competitive yet innovation-driven environment. Huawei leads with nearly 30% share, followed by Nokia, ZTE, Calix, and Adtran, each investing heavily in 10G and 25G PON advancements.

Strategic initiatives include partnerships between telecom operators and equipment vendors to accelerate XGS-PON upgrades, with over 40 major 10G deployment agreements signed globally between 2023 and 2025. Product launches focusing on energy-efficient OLT platforms have reduced power consumption by up to 20% per port. Mergers and collaborations targeting software-defined access integration have increased by 25%, reflecting the shift toward cloud-managed broadband systems. Competition increasingly centers on scalability, interoperability, and AI-driven network automation capabilities, positioning technology differentiation as the primary driver of market leadership.

Huawei

Nokia

ZTE

Calix

Adtran

FiberHome

DASAN Zhone Solutions

Iskratel

TP-Link Technologies

Allied Telesis

The Passive Optical Network market is undergoing rapid technological transformation driven by next-generation fiber access standards, software-defined networking, and AI-enabled automation. XGS-PON technology, delivering symmetrical 10 Gbps speeds, has become mainstream, with over 45% of newly deployed optical line terminals globally supporting 10G capability. This represents a significant upgrade from GPON’s 2.5 Gbps downstream capacity, enabling operators to support 4K/8K streaming, cloud gaming, telemedicine, and enterprise-grade VPN services without network congestion.

Emerging 25G PON solutions are gaining commercial traction, particularly in dense urban corridors and enterprise campuses where bandwidth demand exceeds 5 Gbps per user during peak hours. Field trials demonstrate up to 2.5x throughput improvement over XGS-PON, while maintaining backward compatibility with existing fiber infrastructure. Combo PON platforms, which integrate GPON and XGS-PON ports within a single optical line terminal, have reduced upgrade costs by nearly 30% by eliminating parallel network builds.

Virtualized optical line terminals (vOLTs) are transforming network architecture by decoupling hardware from software. Cloud-native OLT deployments have reduced provisioning time by 40% and improved scalability across distributed networks. AI-driven traffic management systems now detect anomalies within milliseconds, lowering mean time to repair by up to 50%. Energy-efficient chipsets and low-power optics have improved port-level energy consumption by nearly 20%, aligning with telecom ESG mandates targeting 30% carbon intensity reduction by 2030.

Integration with 5G fronthaul and edge computing is another pivotal trend. Approximately 70% of new 5G small cells rely on fiber-based backhaul, increasing demand for low-latency PON architectures with sub-10 millisecond performance. Software-defined access networking further enhances bandwidth orchestration, enabling real-time traffic slicing and optimized network utilization exceeding 80% capacity thresholds. These innovations collectively position Passive Optical Network infrastructure as a foundational digital platform supporting scalable broadband ecosystems.

• In October 2024, Nokia announced the expansion of its 25G PON solution portfolio, enabling operators to deliver 20 Gbps and higher broadband services over existing fiber infrastructure. The solution supports coexistence with GPON and XGS-PON, simplifying migration while increasing network capacity density for enterprise and mobile backhaul applications. Source: www.nokia.com

• In February 2025, ZTE Corporation completed a 50G PON live network trial with a major Asian telecom operator, achieving peak downstream speeds above 45 Gbps and demonstrating compatibility with existing optical distribution networks. The milestone supports ultra-high-capacity access for smart city and industrial digitalization projects. Source: www.zte.com.cn

• In May 2024, Calix introduced an enhanced cloud-managed XGS-PON platform designed to support symmetrical 10 Gbps services for residential and small business subscribers. The platform integrates AI-driven analytics, enabling service providers to improve customer experience metrics and reduce operational complexity.

• In March 2025, Huawei unveiled its next-generation intelligent 10G PON solution featuring energy-efficient optical modules that reduce power consumption per port by up to 20%. The solution incorporates AI-based network optimization to enhance bandwidth allocation efficiency in high-density urban deployments.

The Passive Optical Network Market Report provides a comprehensive evaluation of fiber-based broadband infrastructure spanning core technology standards, deployment models, and end-user verticals. The report covers GPON, XGS-PON, 25G PON, and emerging 50G PON technologies, analyzing their deployment across residential, enterprise, mobile backhaul, and smart infrastructure applications. Over 1.4 billion global fiber subscribers and more than 800 million FTTH connections form the basis of the market’s installed ecosystem, creating substantial upgrade and expansion opportunities.

Geographically, the report examines five primary regions: Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, incorporating analysis of more than 25 key countries with fiber penetration rates ranging from 40% to over 90%. It evaluates infrastructure readiness, government broadband initiatives targeting 80–100% gigabit coverage, and enterprise fiber adoption levels exceeding 60% in developed markets.

Application coverage includes fiber-to-the-home, fiber-to-the-building, enterprise campus networks, 5G mobile backhaul, and industrial IoT connectivity. The report also assesses integration with edge computing and cloud-native architectures, highlighting scenarios where bandwidth consumption surpasses 500 GB per household monthly.

In addition, the scope encompasses vendor landscape analysis of over 50 active competitors, supply chain dynamics in optical fiber manufacturing exceeding 300 million fiber-kilometers annually, and ESG-driven efficiency benchmarks targeting 20–30% power reduction in access networks. Emerging niches such as smart grid connectivity, rural broadband expansion programs, and AI-enabled virtualized OLT deployments are examined to provide a forward-looking perspective for strategic investment and infrastructure planning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

14.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Huawei, Nokia, ZTE, Calix, Adtran, FiberHome, DASAN Zhone Solutions, Iskratel, TP-Link Technologies, Allied Telesis |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |