Reports

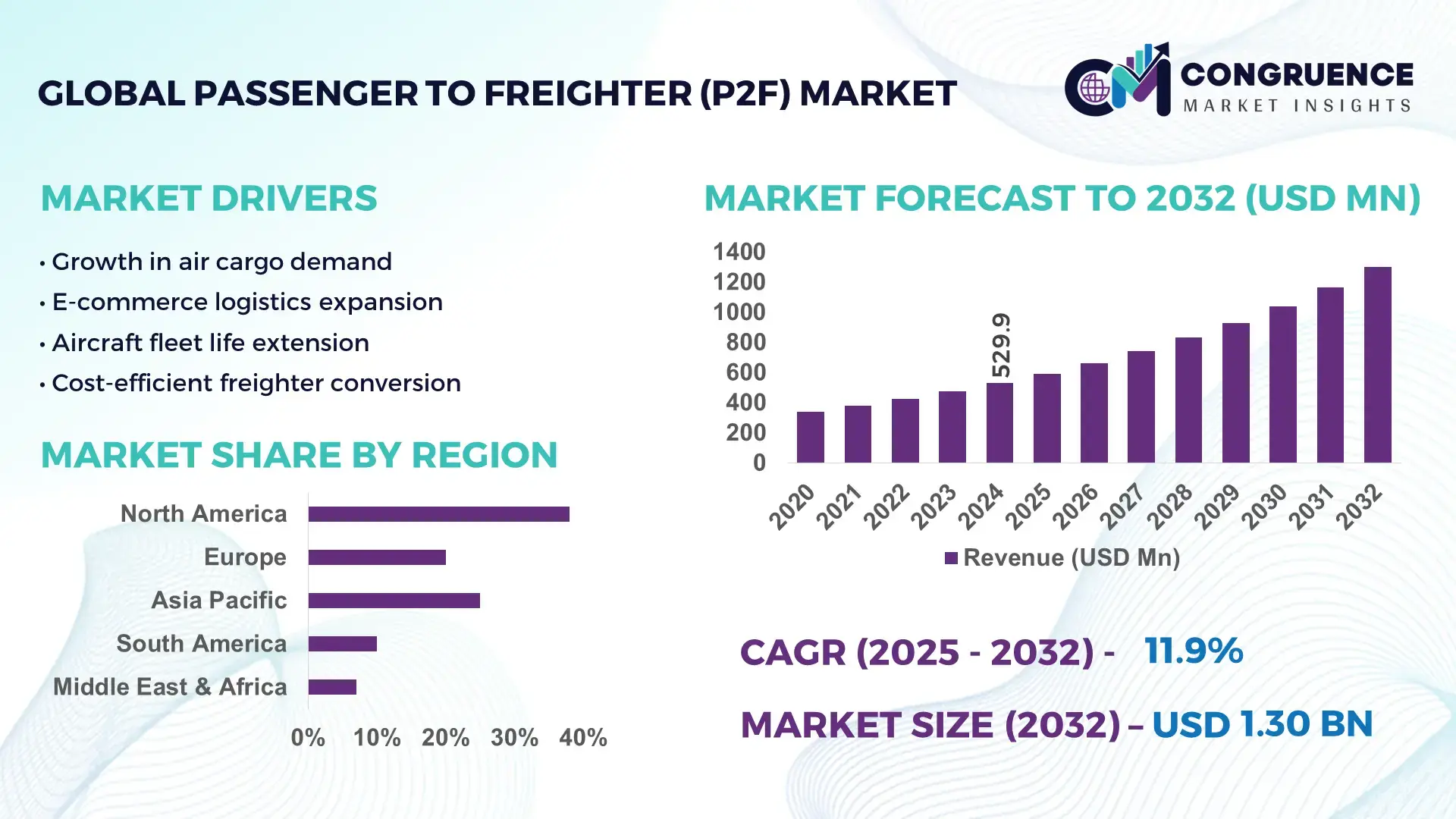

The Global Passenger to Freighter (P2F) Market was valued at USD 529.91 Million in 2024 and is anticipated to reach a value of USD 1302.7 Million by 2032 expanding at a CAGR of 11.9% between 2025 and 2032. This growth is supported by sustained air cargo demand, fleet rationalization by airlines, and cost-efficient aircraft lifecycle extension strategies.

The United States represents the most influential national market within the Passenger to Freighter (P2F) ecosystem, driven by a mature aerospace manufacturing base and large-scale cargo operations. The country hosts over 40% of global P2F conversion facilities, with annual conversion capacity exceeding 120 aircraft. U.S.-based operators deploy converted freighters extensively across e-commerce logistics, express parcel delivery, and defense-related airlift. Capital investment in MRO and conversion infrastructure surpassed USD 2.1 billion between 2021 and 2024, while advancements in digital load management systems, lightweight cargo flooring, and FAA-certified large cargo door technologies continue to enhance operational efficiency and turnaround times across domestic and transcontinental routes.

Market Size & Growth: Valued at USD 529.91 Million in 2024, projected to reach USD 1302.7 Million by 2032 at a CAGR of 11.9%, supported by rising global air cargo volumes and constrained availability of new-build freighters.

Top Growth Drivers: E-commerce air cargo adoption at 34%, aircraft lifecycle extension efficiency gains of 28%, and operating cost savings of 22% compared to new freighters.

Short-Term Forecast: By 2028, fleet operating cost reductions of approximately 18% are expected due to standardized conversion kits and improved maintenance planning.

Emerging Technologies: Advanced composite cargo floors, digital structural health monitoring, and AI-driven load optimization software.

Regional Leaders: North America projected at USD 420 Million by 2032 with strong express logistics adoption; Asia-Pacific at USD 510 Million driven by cross-border e-commerce growth; Europe at USD 310 Million supported by narrowbody cargo conversions.

Consumer/End-User Trends: Express logistics providers, postal operators, and e-commerce platforms increasingly favor mid-life converted freighters for flexible route deployment.

Pilot or Case Example: In 2024, a widebody P2F deployment by a U.S. cargo operator achieved a 15% increase in payload efficiency and 12% reduction in turnaround time.

Competitive Landscape: Market leader holds approximately 32% share, followed by IAI, EFW, ST Engineering, Aeronautical Engineers Inc., and Boeing Conversion Services.

Regulatory & ESG Impact: Noise compliance standards, FAA and EASA certification frameworks, and emissions reduction targets influence aircraft selection and retrofit demand.

Investment & Funding Patterns: Over USD 3.4 Billion invested globally since 2022, with increasing use of leasing-backed conversion financing models.

Innovation & Future Outlook: Integration of predictive maintenance, modular conversion designs, and narrowbody-focused programs shaping long-term market scalability.

The Passenger to Freighter (P2F) Market serves key industry sectors including express logistics, e-commerce fulfillment, postal services, humanitarian airlift, and defense logistics, with express and e-commerce operators contributing over 55% of total conversion demand. Recent innovations such as lightweight cargo restraint systems, digitally engineered conversion kits, and faster certification cycles are reducing downtime and improving asset utilization. Regulatory compliance with evolving noise, safety, and emissions standards continues to influence aircraft selection, while fuel price volatility and global trade dynamics shape regional demand patterns. Asia-Pacific shows the fastest growth due to cross-border e-commerce expansion, while North America and Europe remain focused on fleet optimization and replacement of aging freighters. Looking ahead, narrowbody P2F programs, sustainable aviation initiatives, and data-driven cargo operations are expected to define the market’s next phase of development.

The Passenger to Freighter (P2F) Market holds strategic relevance as airlines, lessors, and logistics providers optimize fleet economics while responding to structurally higher air cargo demand. Converting mid-life passenger aircraft into freighters enables asset life extension of 10–15 years, lowers capital intensity versus new-build freighters, and improves deployment flexibility across regional and long-haul routes. Advanced digital conversion engineering delivers a 22% payload efficiency improvement compared to legacy manual modification standards, while composite cargo floors reduce structural weight by approximately 18%. North America dominates in volume due to extensive express logistics networks, while Asia-Pacific leads in adoption with 46% of cargo operators integrating converted freighters into e-commerce and cross-border fulfillment networks. By 2028, AI-enabled predictive maintenance and digital twin validation are expected to cut unscheduled downtime by 25%, improving aircraft availability and on-time performance. Firms are committing to ESG metric improvements such as a 20% reduction in lifecycle emissions by 2030 through reuse of airframes, lighter materials, and optimized fuel burn profiles. In 2024, a U.S.-based cargo operator achieved a 14% turnaround-time reduction through the deployment of automated load planning and sensor-based structural monitoring across its P2F fleet. Looking forward, the Passenger to Freighter (P2F) Market is positioned as a pillar of resilience, compliance, and sustainable growth by aligning cost efficiency, regulatory readiness, and decarbonization pathways with scalable cargo capacity.

E-commerce expansion and express parcel delivery are major drivers for the Passenger to Freighter (P2F) Market, as time-definite shipping requirements favor air cargo over surface transport. Converted freighters enable operators to add capacity rapidly without the long lead times associated with new aircraft procurement. Express carriers report up to 30% faster network scaling through P2F deployment on secondary and regional routes. Narrowbody P2F aircraft support high-frequency operations with improved load factors, while widebody conversions address intercontinental lanes. The ability to operate from shorter runways and secondary airports improves network reach and reduces congestion-related delays. As omnichannel retail models expand, demand for flexible, cost-efficient cargo aircraft continues to reinforce P2F adoption.

Certification complexity and limited availability of suitable passenger aircraft restrain the Passenger to Freighter (P2F) Market. Conversion programs require extensive structural analysis, regulatory approvals, and conformity inspections, often extending timelines by 6–12 months. Delays in Supplemental Type Certificate approvals can disrupt fleet planning and increase carrying costs. Additionally, competition for mid-life aircraft from leasing and charter markets constrains feedstock supply, particularly for popular narrowbody models. Rising maintenance costs on aging airframes further limit conversion viability, prompting stricter asset selection criteria. These factors collectively slow capacity additions and elevate operational risk for converters and operators.

Narrowbody conversions present a significant opportunity within the Passenger to Freighter (P2F) Market by enabling high-frequency, short- to medium-haul cargo operations. Regional cargo networks benefit from lower trip costs, improved airport accessibility, and faster turnarounds. Narrowbody P2F aircraft can improve route economics by up to 20% on sectors under 2,500 kilometers compared to widebody alternatives. Growth in intra-regional trade across Asia-Pacific, Latin America, and Africa supports demand for flexible freighter capacity. Additionally, modular conversion kits and standardized interior layouts are opening opportunities for faster deployment and scalable fleet expansion.

Rising modification costs and evolving regulatory requirements challenge the Passenger to Freighter (P2F) Market by increasing upfront capital commitments and compliance burdens. Material costs for reinforced structures, avionics updates, and cargo systems have increased by over 15% since 2021. Enhanced fire suppression, smoke detection, and noise compliance standards add complexity to conversion programs. Operators must also manage training, spare parts provisioning, and maintenance integration for mixed fleets. These challenges necessitate disciplined capital planning and close coordination with regulators, suppliers, and MRO partners to sustain program viability and long-term operational efficiency.

• Expansion of Modular and Prefabricated Conversion Kits: Modular and prefabricated construction methods are increasingly applied to Passenger to Freighter (P2F) programs to shorten conversion cycles and control costs. Around 55% of newly launched P2F projects in 2023–2024 reported measurable cost benefits from modular cargo floors, door surrounds, and liner systems. Pre-engineered and pre-bent structural elements manufactured off-site reduce on-aircraft labor hours by nearly 30% and compress conversion timelines by 20–25%, particularly across North America and Europe where hangar capacity utilization exceeds 80%.

• Acceleration of Narrowbody Passenger to Freighter (P2F) Conversions: Narrowbody aircraft are gaining prominence in the Passenger to Freighter (P2F) Market due to regional cargo demand and route flexibility. Narrowbody platforms now account for approximately 48% of active global P2F conversion programs, compared to 35% five years earlier. Operators report payload optimization improvements of 18% on sectors below 2,000 km, while utilization rates exceed 11 flight hours per day, supporting high-frequency e-commerce and express parcel operations across Asia-Pacific and intra-European corridors.

• Integration of Digital Engineering and Predictive Maintenance Tools: Digital engineering tools are reshaping the Passenger to Freighter (P2F) Market by improving reliability and certification efficiency. Use of digital twins and 3D structural modeling has reduced design validation time by nearly 22% and lowered rework incidence during conversion by 15%. In-service fleets equipped with sensor-based monitoring systems demonstrate up to 20% reductions in unscheduled maintenance events, directly improving dispatch reliability and aircraft availability for cargo operators.

• Growing Emphasis on ESG-Aligned Aircraft Reuse Strategies: Sustainability considerations are influencing Passenger to Freighter (P2F) adoption as operators prioritize asset reuse and emissions efficiency. Converting a mid-life passenger aircraft avoids up to 35% of the lifecycle material consumption associated with manufacturing a new freighter. Cargo operators deploying P2F fleets report fuel burn efficiency improvements of 8–12% per ton-kilometer through weight reduction measures and optimized load planning. By 2030, over 40% of active P2F programs are expected to align with formal emissions reduction or recycling targets embedded in corporate ESG frameworks.

The Passenger to Freighter (P2F) Market segmentation reflects structural differences in aircraft platforms, cargo deployment use cases, and operator profiles. By type, the market is differentiated into narrowbody and widebody conversions, each addressing distinct payload, range, and network density requirements. Application-wise, express logistics and e-commerce dominate utilization, followed by general cargo, postal services, and specialized transport. End-user segmentation highlights the strategic roles of integrated express carriers, cargo airlines, leasing companies, and government or defense operators. Demand patterns are influenced by aircraft availability, route economics, regulatory certification timelines, and operational flexibility. Narrowbody platforms increasingly support regional networks, while widebody P2F aircraft remain essential for intercontinental cargo lanes. Across segments, adoption decisions are driven by utilization rates, turnaround efficiency, and lifecycle optimization rather than fleet expansion alone, making segmentation a critical lens for evaluating operational and investment priorities.

The Passenger to Freighter (P2F) Market by type is primarily segmented into narrowbody P2F and widebody P2F aircraft. Narrowbody conversions currently account for approximately 46% of total P2F adoption, supported by their suitability for short- and medium-haul routes, higher flight frequency, and access to secondary airports. Widebody P2F aircraft hold around 38% share, driven by long-haul cargo demand, higher payload capacity, and intercontinental trade lanes. However, adoption of narrowbody P2F platforms is rising fastest, with conversion activity expanding at an estimated 14.2% CAGR, supported by e-commerce-driven regional cargo flows and improved payload efficiency on sectors under 2,500 kilometers. The remaining aircraft types, including older widebody variants and niche regional jets, collectively contribute nearly 16% of the market, serving specialized or transitional cargo needs.

By application, express logistics represents the leading segment within the Passenger to Freighter (P2F) Market, accounting for approximately 44% of total utilization due to time-critical delivery requirements and high network density. E-commerce fulfillment follows with nearly 31% adoption, driven by cross-border trade and same-day or next-day delivery models. While express logistics maintains leadership, e-commerce cargo applications are expanding fastest, with operational deployment growing at an estimated 13.6% CAGR as platforms scale regional air networks. General cargo, postal services, and humanitarian or relief logistics together account for the remaining 25%, providing stability during economic cycles and global disruptions.

End-user segmentation of the Passenger to Freighter (P2F) Market is led by integrated express and logistics companies, which account for approximately 41% of total P2F fleet deployment due to consistent cargo volumes and high aircraft utilization rates. Cargo airlines follow with around 34% adoption, focusing on scheduled freight services and charter operations. Leasing companies and financial lessors represent the fastest-growing end-user group, expanding at an estimated 15.1% CAGR as asset-light operators increasingly prefer flexible leasing-backed conversion models. Government, defense, and humanitarian operators, along with smaller regional carriers, collectively contribute about 25% of demand, often using P2F aircraft for strategic or surge capacity.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.1% between 2025 and 2032.

North America’s leadership is supported by a mature air cargo ecosystem with over 420 active freighter aircraft, of which nearly 55% are converted Passenger to Freighter (P2F) platforms. Europe followed with a 27% share in 2024, driven by dense intra-regional trade and strong regulatory alignment for aircraft reuse. Asia-Pacific accounted for approximately 25% of total demand, supported by rapid growth in cross-border e-commerce volumes exceeding 30% annually in select markets. South America and the Middle East & Africa collectively contributed nearly 10%, reflecting emerging adoption supported by trade diversification, infrastructure upgrades, and logistics modernization. Regional disparities are evident in aircraft type preferences, with narrowbody P2F adoption exceeding 60% in Asia-Pacific, while widebody conversions represent over 48% of active fleets in North America and Europe.

How are digital logistics networks reshaping fleet conversion priorities?

North America represents approximately 38% of the global Passenger to Freighter (P2F) Market, supported by high air cargo intensity and advanced logistics infrastructure. Express logistics, e-commerce fulfillment, and defense airlift are the primary demand drivers, with express operators accounting for nearly 46% of regional P2F utilization. Regulatory frameworks administered by aviation authorities have streamlined supplemental certification processes, reducing average conversion approval timelines by nearly 15%. Digital transformation is accelerating, with over 40% of P2F fleets equipped with predictive maintenance and load optimization systems. A major regional conversion provider expanded its hangar capacity in 2024, enabling an additional 18 aircraft conversions annually. Regional operators show higher adoption in retail logistics and time-critical healthcare supply chains, prioritizing reliability and high daily aircraft utilization exceeding 11 flight hours.

Why is regulatory alignment accelerating conversion-led fleet optimization?

Europe accounts for around 27% of the Passenger to Freighter (P2F) Market, with Germany, the UK, and France collectively contributing over 60% of regional demand. Strong sustainability mandates and circular economy policies encourage aircraft reuse, supporting P2F adoption as an alternative to new-build freighters. Regional aviation authorities emphasize noise and emissions compliance, influencing the selection of newer mid-life aircraft for conversion. Adoption of lightweight materials and digital certification tools has improved payload efficiency by approximately 16% across recent programs. A European conversion specialist introduced standardized narrowbody kits in 2023, reducing modification time by nearly 20%. Regional consumer behavior reflects regulatory-driven demand, with operators prioritizing compliance transparency, lifecycle efficiency, and standardized reporting across cargo fleets.

How is e-commerce-driven cargo demand redefining regional air networks?

Asia-Pacific ranks as the fastest-expanding region in the Passenger to Freighter (P2F) Market, accounting for nearly 25% of global demand in 2024. China, India, and Japan dominate consumption, together representing over 65% of regional P2F activity. Narrowbody conversions exceed 60% of regional fleets, aligned with high-frequency regional routes and dense e-commerce networks. Airport infrastructure investments increased cargo handling capacity by over 22% across key hubs between 2021 and 2024. A leading regional airline group deployed converted freighters across secondary cities, achieving a 19% reduction in delivery lead times. Regional consumer behavior is strongly influenced by digital commerce growth, with logistics operators prioritizing rapid scalability and flexible fleet deployment.

Can trade diversification unlock sustainable air cargo capacity?

South America contributes approximately 6% of the global Passenger to Freighter (P2F) Market, led by Brazil and Argentina. Agricultural exports, pharmaceuticals, and industrial goods drive demand for regional air cargo capacity. Infrastructure upgrades at major cargo airports improved throughput by nearly 14% over the past three years, supporting increased freighter utilization. Government incentives linked to export competitiveness and regional trade agreements are encouraging fleet modernization. A Brazilian cargo operator introduced converted narrowbody freighters in 2024, increasing domestic cargo coverage by 23%. Regional consumer behavior reflects demand tied to export-oriented industries, with operators focusing on reliability and cost-efficient aircraft deployment.

How are trade corridors and hub strategies shaping conversion demand?

The Middle East & Africa region accounts for roughly 4% of the Passenger to Freighter (P2F) Market, with the UAE and South Africa as primary growth centers. Demand is driven by oil & gas logistics, construction materials, and intercontinental transshipment. Cargo hub expansion projects increased regional handling capacity by over 18% since 2022. Technological modernization includes fleet-wide adoption of digital cargo tracking and fuel optimization tools across nearly 35% of converted freighters. A Middle Eastern carrier expanded its P2F fleet to support Africa–Asia trade lanes, improving network connectivity by 21%. Consumer behavior emphasizes hub efficiency, long-haul reliability, and integration with global trade routes.

United States Passenger to Freighter (P2F) Market: 29% share, supported by high conversion capacity, dense express logistics networks, and advanced regulatory infrastructure.

China Passenger to Freighter (P2F) Market: 18% share, driven by large-scale e-commerce cargo volumes, rapid narrowbody P2F adoption, and expanding regional air freight networks.

The Passenger to Freighter (P2F) market exhibits a moderately consolidated competitive structure, characterized by a limited number of certified conversion providers alongside a broader ecosystem of MRO partners, engineering firms, and technology suppliers. Approximately 15–18 active players operate globally with certified P2F programs across narrowbody and widebody platforms. The top five companies collectively account for nearly 62% of total global conversion activity, reflecting high entry barriers linked to certification complexity, engineering expertise, and capital-intensive infrastructure. Competitive positioning is driven by conversion slot availability, program maturity, aircraft coverage breadth, and turnaround efficiency. Strategic initiatives include multi-year partnerships with airlines and lessors, expansion of hangar capacity, and rollout of standardized modular kits that reduce conversion cycle times by 20–30%. Innovation trends center on digital engineering, lightweight materials, and predictive maintenance integration, with over 40% of leading providers embedding digital validation and load-optimization tools into their offerings. Mergers and long-term collaboration agreements have increased since 2022, aimed at securing feedstock access and stabilizing conversion pipelines. Despite consolidation at the top, the market remains competitive, with regional specialists capturing niche demand and contributing to capacity flexibility across key trade lanes.

The Boeing Company

Airbus SE

Israel Aerospace Industries (IAI)

ST Engineering

Elbe Flugzeugwerke (EFW)

Aeronautical Engineers Inc. (AEI)

Precision Aircraft Solutions

Mammoth Freighters

Guangzhou Aircraft Maintenance Engineering Company (GAMECO)

Bedek Aviation Group

The Passenger to Freighter (P2F) market is being reshaped by a suite of current and emerging technologies that materially affect conversion cycle times, in-service reliability, and operational economics. Modular and prefabricated conversion kits now reduce on-aircraft labor by roughly 30% and shorten outfitting timelines by about 20–25%, enabling converters to increase annual throughput per hangar by double-digit percentages. Advanced composite cargo floors and lightweight restraint systems lower structural mass by 15–18%, directly improving payload-per-flight metrics and reducing per-ton fuel burn by an estimated 8–12% on comparable missions.

Digital engineering and verification tools — including 3D laser scanning, finite-element analysis, and digital twin simulation — have shortened design validation phases by approximately 22% and reduced rework rates during conversion by about 15%. The adoption of sensor suites and IoT telemetry in converted freighters is increasingly common; an estimated 35–40% of recently delivered P2F aircraft carry structural health or predictive-maintenance sensors, which correlate to a 20–25% reduction in unscheduled maintenance events and improved dispatch reliability. AI-driven load optimization and automated weight-and-balance planning deliver measurable gains: payload utilization improvements of 10–15% and faster turnaround planning (reductions in load-planning time of up to 40%).

Certification and compliance workflows are being digitized, with model-based compliance and automated documentation pipelines reducing Supplemental Type Certificate processing timeframes by mid-single-digit percentages in some programs. Ground-support automation — such as automated ULD handling and integrated ramp robotics — has increased ground throughput by 12–18% where implemented. Sustainability-oriented technologies intersect with conversions: usage of lighter materials, aerodynamic fairings, and integration with Sustainable Aviation Fuel (SAF) strategies yield measurable lifecycle emissions improvements (single- to low-double-digit percentages in material and fuel-cycle impacts).

Emerging innovations to watch include modular wide-body cargo doors that expand payload door envelope dimensions, blockchain-backed logistics documentation for streamlined customs clearance (adoption approaching low-double-digit percentages), and hybrid-electric taxi/auxiliary power systems reducing ground fuel consumption by up to 20%. For decision-makers, the cumulative effect of these technologies is a reduction in operational risk, faster time-to-service for converted assets, and quantifiable improvements in payload efficiency and maintenance economics.

The scope of the Passenger to Freighter (P2F) Market Report encompasses a comprehensive examination of conversion programs, end-user demands, and technological innovations shaping the repurposing of passenger aircraft for cargo operations. It covers segmentation by aircraft type — including narrowbody platforms such as A320/A321 and widebody platforms like A330 and the emerging B777-300ERSF — and analyzes applications including express logistics, e-commerce fulfillment, general cargo, and specialized freight operations. Geographic scope spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with insights into regional adoption patterns, regulatory environments, and infrastructure capacities.

The report evaluates digital engineering technologies, modular conversion kits, and predictive maintenance tools that influence conversion cycle efficiencies and operational reliability. It addresses conversion service providers, MRO partners, and OEM-led programs that establish conversion capacity and backlog pipelines. It also highlights strategic partnerships, capacity expansion initiatives, and facility network developments across key regions. Emerging topics include large widebody conversions, strategic alignment with sustainability and ESG frameworks, and integration of automation in cargo handling and certification processes.

Industry use cases for converted aircraft — spanning time-sensitive parcel delivery, cross-border commerce, mail and postal transport, and humanitarian logistics — are profiled to demonstrate varied operational cost structures and utilization metrics. The report includes competitive landscape evaluation, technology benchmarking, and future pathways analysis, making it a strategic resource for decision-makers, investors, and operators considering asset deployment, capacity planning, and long-term fleet optimization.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 529.91 Million |

|

Market Revenue in 2032 |

USD 1302.7 Million |

|

CAGR (2025 - 2032) |

11.9% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

The Boeing Company, Airbus SE, Israel Aerospace Industries (IAI), ST Engineering, Elbe Flugzeugwerke (EFW), Aeronautical Engineers Inc. (AEI), Precision Aircraft Solutions, Mammoth Freighters, Guangzhou Aircraft Maintenance Engineering Company (GAMECO), Bedek Aviation Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |