Reports

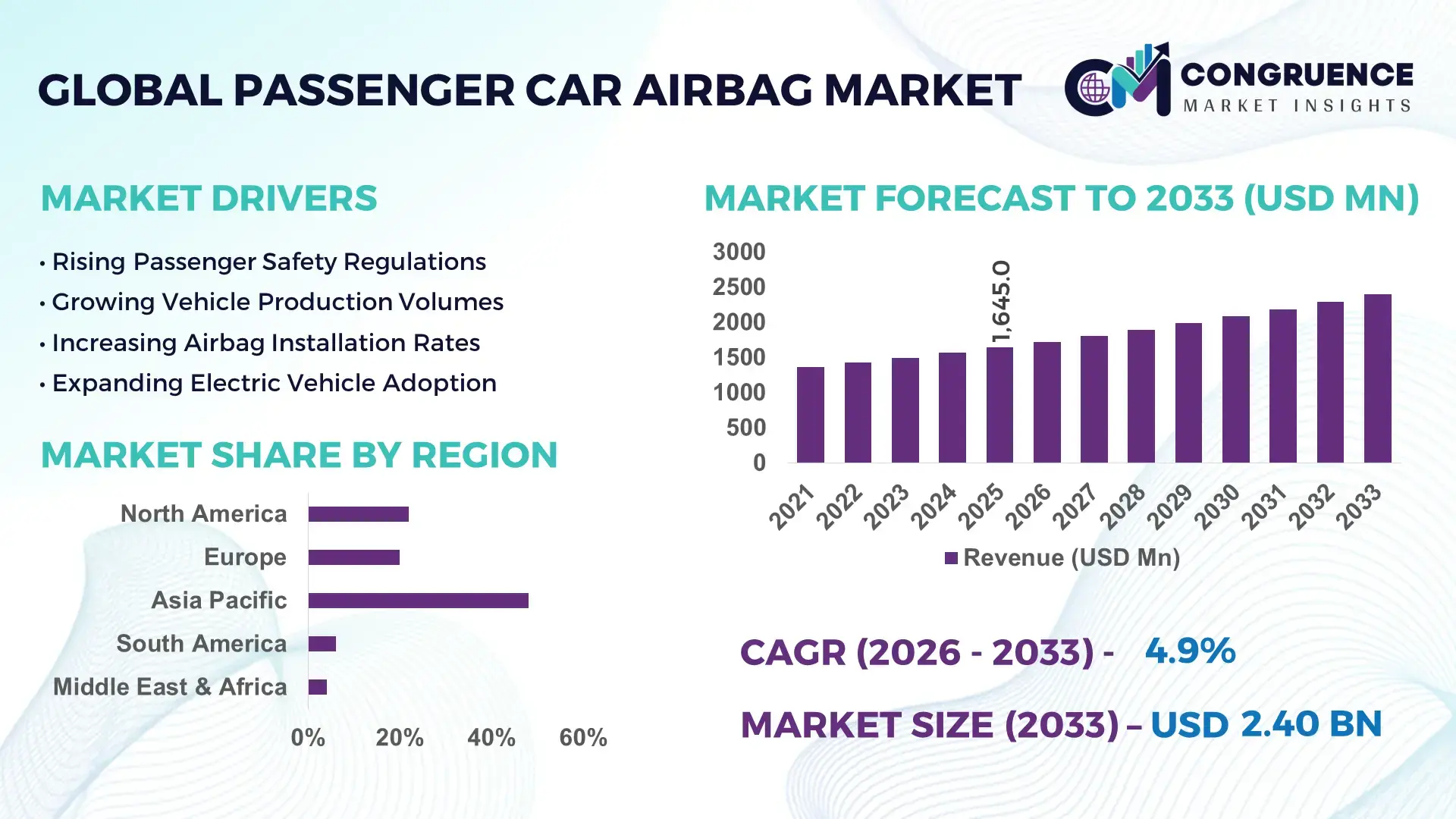

The Global Passenger Car Airbag Market was valued at USD 1,645.0 Million in 2025 and is anticipated to reach a value of USD 2,404.6 Million by 2033 expanding at a CAGR of 4.86% between 2026 and 2033. Growth is being driven by the rapid integration of multi-airbag safety architectures, stricter crash-protection regulations, and increasing installation of side-curtain and knee airbags across mid-range passenger vehicle platforms.

China remains the dominant country in the passenger car airbag ecosystem, accounting for nearly 32% of global passenger vehicle production and over 30% of airbag module demand, supported by annual vehicle output exceeding 31 million units and continued investment in advanced automotive safety manufacturing. In comparison, Germany contributes higher-value airbag engineering and premium vehicle integration, while China leads in volume deployment. Following post-pandemic supply-chain restructuring and heightened vehicle safety scrutiny, airbag fitment rates in newly launched passenger vehicles now exceed 92% across major automotive markets.

For manufacturers and suppliers, competitive advantage increasingly depends on advanced sensor integration, localized production networks, and scalable multi-airbag platform capabilities.

Market Size & Growth: USD 1,645.0 Million in 2025, reaching USD 2,404.6 Million by 2033, supported by rising multi-airbag mandates, premium safety adoption, and advanced occupant-protection systems.

Top Growth Drivers: Side-curtain airbag penetration exceeds 70%, advanced crash-sensor adoption surpasses 55%, and passenger vehicle safety compliance rates exceed 90% in major automotive markets.

Short-Term Forecast: By 2028, airbag deployment system response times are expected to improve by 15%, while module integration costs decline by nearly 8% through manufacturing optimization.

Emerging Technologies: AI-enabled crash sensing, predictive occupant detection, lightweight textile airbags, and smart electronic control units are reshaping advanced vehicle safety architectures.

Regional Leaders: Asia-Pacific exceeds USD 900 Million, Europe approaches USD 520 Million, and North America surpasses USD 430 Million, driven by safety-focused vehicle platforms and regulatory compliance.

Consumer/End-User Trends: More than 85% of new passenger vehicles now feature six or more airbags as safety awareness and vehicle ratings influence purchasing decisions.

Pilot/Case Example: In 2024, next-generation occupant sensing systems improved crash-response accuracy by approximately 20% in controlled automotive testing environments.

Competitive Landscape: Autoliv holds roughly 22% market share, followed by Joyson Safety Systems, ZF Lifetec, Toyoda Gosei, and Hyundai Mobis.

Regulatory & ESG Impact: Safety regulations have increased airbag installation rates by over 25% during the past decade while supporting safer mobility outcomes.

Investment & Funding: More than USD 1.2 Billion has been directed toward automotive safety manufacturing expansion, localization, and sensor technology partnerships.

Innovation & Future Outlook: Adaptive airbags, software-defined safety systems, and connected vehicle integration are accelerating the next phase of global passenger protection technologies.

Passenger Car Airbag Market demand is increasingly concentrated in compact SUVs, electric passenger vehicles, and premium sedan platforms where enhanced occupant protection remains a key differentiator. Recent innovations include adaptive airbag deployment algorithms, lightweight fabric modules, and AI-enabled occupant sensing systems. Airbag fitment rates have increased by more than 18% in emerging automotive markets as regulators strengthen vehicle safety requirements and manufacturers diversify supply chains, setting the stage for deeper strategic transformation across the industry.

Passenger car airbags have evolved from a compliance-driven safety component into a strategic differentiator influencing vehicle ratings, consumer purchasing decisions, and OEM competitiveness. The market is becoming increasingly important as governments tighten crash-safety requirements and automakers redesign platforms around advanced occupant-protection architectures. Supply-chain restructuring following semiconductor and component disruptions has accelerated localization strategies among major safety-system suppliers.

Technology advancement is creating measurable operational advantages. Modern AI-enabled occupant detection systems improve deployment precision by approximately 20% compared with conventional sensor-based architectures while reducing false activation risks. China and India are scaling high-volume deployment through mass-market vehicle production, whereas Germany and Japan remain leaders in premium safety engineering and integrated restraint-system innovation. More than 85% of newly launched passenger vehicles in developed automotive markets now incorporate six or more airbags as standard equipment.

Automotive suppliers are expanding sensor manufacturing capacity, strengthening OEM partnerships, and investing in predictive safety technologies. For example, leading airbag manufacturers are integrating camera-based occupant monitoring with electronic control units to optimize deployment decisions in real time. Over the next two to three years, increasing adoption of intelligent restraint systems, localized manufacturing hubs, and software-driven safety platforms will strengthen competitive positioning for companies capable of delivering high-performance, scalable, and regulation-ready passenger protection solutions.

Government safety mandates and rising consumer demand for higher vehicle safety ratings are accelerating adoption of advanced airbag systems. More than 85% of newly launched passenger vehicles in developed markets now include six or more airbags, while side-curtain airbag penetration has surpassed 70% in several high-volume automotive markets. India's strengthened passenger vehicle safety requirements and China's expanding crash-protection standards are increasing fitment rates across entry-level and mid-range vehicle segments. This regulatory shift directly increases content value per vehicle and expands opportunities for suppliers of sensors, inflators, and electronic control units. In response, manufacturers are expanding localized production facilities, investing in lightweight airbag materials, and forming strategic partnerships with OEMs to secure long-term supply contracts. The key operational advantage lies in scaling advanced protection systems without significantly increasing vehicle weight or assembly complexity.

Passenger car airbag production remains exposed to fluctuations in semiconductor availability, technical textile inputs, and specialized inflator components. Raw material costs for engineered fabrics and precision electronics have experienced periodic swings exceeding 10%, while logistics disruptions have extended component lead times by nearly 15% in some automotive supply chains. Dependence on concentrated manufacturing clusters in East Asia creates additional sourcing risks during geopolitical tensions and trade policy adjustments. These constraints directly affect production planning, inventory management, and supplier margins. To mitigate exposure, manufacturers are diversifying supplier networks, increasing regional sourcing, and securing long-term procurement agreements. A notable strategic shift involves nearshoring critical component production to reduce transit dependency and improve operational resilience, particularly for OEM programs requiring high-volume delivery consistency.

The next wave of opportunity extends beyond traditional airbag deployment toward intelligent occupant protection ecosystems. AI-enabled occupant sensing systems improve crash-response accuracy by approximately 20%, while advanced monitoring technologies can enhance deployment customization based on passenger position, weight, and seating posture. Electric vehicle platforms, which are projected to represent more than 30% of global vehicle production in key markets by the end of the decade, require redesigned safety architectures that create additional demand for adaptive restraint systems. Japan, South Korea, and China are investing heavily in smart mobility technologies, accelerating commercialization of integrated safety platforms. Companies are increasing R&D spending, collaborating with software developers, and developing predictive safety algorithms. A significant strategic opportunity lies in combining connected vehicle data with restraint systems to create proactive occupant protection capabilities rather than purely reactive deployment mechanisms.

As vehicle architectures become increasingly software-driven, integrating airbags with cameras, radar sensors, occupant monitoring systems, and centralized electronic control units creates significant engineering complexity. Advanced passenger vehicles now incorporate over 100 electronic control functions, increasing validation and interoperability requirements. Software verification activities can account for nearly 30% of development workloads in next-generation safety systems. Variations in regulatory requirements across China, Europe, India, and North America further complicate global deployment strategies. These challenges impact development timelines, certification processes, and lifecycle maintenance costs. Companies must strengthen software engineering capabilities, expand testing infrastructure, and invest in digital simulation technologies to maintain deployment consistency. The most successful suppliers will be those capable of delivering globally compliant, highly integrated safety systems while controlling engineering complexity and ensuring long-term system reliability.

Smart Occupant Detection Expansion Advanced occupant sensing systems are being integrated into more than 58% of newly launched premium passenger vehicles, while AI-assisted deployment accuracy has improved by nearly 20% compared with earlier-generation systems. Regulatory focus on occupant protection and automated safety validation is accelerating adoption. Automakers are embedding camera-based monitoring and weight-sensing technologies directly into vehicle architectures, reducing deployment errors and improving crash-response precision. Suppliers are scaling software capabilities and forming partnerships with electronics specialists to strengthen intelligent restraint system portfolios.

Localization of Safety Supply Chains Airbag manufacturers are restructuring sourcing networks as lead times for selected electronic components have fluctuated by 12–15% in recent years. China and India have expanded local safety-component manufacturing capacity, while regional procurement now accounts for more than 45% of sourcing decisions among major OEM programs. This shift improves delivery reliability and lowers logistics exposure. Companies are investing in localized inflator, sensor, and textile production to increase operational resilience and reduce dependence on concentrated export hubs.

Lightweight Material Integration Growth Lightweight airbag fabrics and compact inflator technologies are reducing system weight by approximately 8–12% without compromising deployment performance. Electric vehicle manufacturers are prioritizing weight optimization to improve driving efficiency and platform flexibility. Safety suppliers are redesigning module architectures, increasing automation in textile processing, and expanding advanced-material partnerships. A less obvious outcome is improved vehicle packaging efficiency, enabling manufacturers to integrate additional safety features within constrained cabin designs.

Multi-Airbag Platform Standardization Six-airbag configurations now represent more than 65% of new passenger vehicle launches across key automotive markets, while side-curtain airbag installation rates exceed 70% in safety-focused vehicle segments. Standardization is streamlining assembly workflows and reducing engineering complexity across vehicle platforms. Automakers are consolidating safety architectures across multiple vehicle models to improve procurement efficiency and certification consistency. In response, suppliers are expanding modular product portfolios capable of supporting both mass-market and premium vehicle programs through a common deployment framework.

Front airbags remain the leading type segment, accounting for approximately 42% of total installations due to mandatory deployment across nearly all passenger vehicle categories. Their dominance is supported by mature manufacturing ecosystems, cost efficiency, and seamless integration with electronic restraint systems. OEMs continue to prioritize front airbag optimization because they serve as the foundation of occupant protection frameworks and are essential for regulatory compliance. Leading suppliers are investing in compact inflator technologies and enhanced deployment algorithms to improve reliability while controlling vehicle integration costs. Side-curtain airbags represent the fastest-growing type segment as automakers increasingly focus on side-impact protection and advanced vehicle safety ratings. Installation rates for side-curtain systems have exceeded 70% in premium vehicle platforms and continue expanding into mid-range passenger cars. Knee airbags and side airbags are also gaining traction as manufacturers pursue higher crash-test performance and differentiated safety offerings. Meanwhile, rear-seat airbag deployments remain comparatively limited but are attracting investment in premium and family-oriented vehicle segments. Companies are expanding product portfolios and strengthening OEM partnerships to capture rising demand for comprehensive multi-airbag architectures.

OEM-installed passenger vehicle applications remain the dominant segment, representing nearly 78% of total airbag deployment volume. Demand concentration stems from mandatory safety requirements, platform standardization strategies, and growing consumer preference for vehicles equipped with multiple restraint systems. Automakers are increasingly integrating six-airbag and eight-airbag configurations as standard features, particularly in China and India where vehicle safety awareness continues to rise. This trend is strengthening long-term procurement agreements between OEMs and major safety-system suppliers. Electric passenger vehicle applications are emerging as the fastest-growing segment as manufacturers redesign cabin layouts and occupant protection strategies around new vehicle architectures. Airbag integration rates in new electric vehicle platforms have increased by approximately 18% over the past two years. Luxury vehicle applications continue to emphasize advanced occupant sensing and adaptive deployment technologies, while economy vehicle applications focus on balancing safety performance with cost control. Suppliers are responding through modular product development, scalable manufacturing, and integrated software-based deployment systems that support diverse vehicle categories.

Original Equipment Manufacturers (OEMs) represent the dominant end-user group, accounting for roughly 85% of total procurement activity due to large-scale vehicle production programs and long-term supplier contracts. Their purchasing decisions are heavily influenced by regulatory compliance, platform efficiency, and crash-test performance requirements. Leading OEMs increasingly prefer integrated safety solutions that combine airbags, occupant sensing technologies, and electronic control units within a unified architecture. This preference is encouraging suppliers to expand engineering collaboration and customized development programs. The electric vehicle manufacturer segment is the fastest-growing end-user category as next-generation vehicle platforms require redesigned restraint systems and advanced cabin protection strategies. Procurement volumes for specialized safety modules have increased by nearly 20% among major EV-focused manufacturers. Premium automotive brands continue investing in adaptive deployment technologies to differentiate vehicle offerings, while high-volume mass-market automakers focus on standardized multi-airbag architectures to improve operational efficiency. Companies are responding through localized production, strategic partnerships, and flexible pricing structures that address diverse customer requirements while securing long-term program participation.

Asia-Pacific accounted for the largest market share at 48% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.4% between 2026 and 2033.

North America represented approximately 22% of the global passenger car airbag market in 2025, supported by high airbag penetration rates, strong regulatory compliance, and widespread adoption of advanced occupant protection technologies. Passenger vehicles equipped with six or more airbags account for over 80% of new vehicle launches across the region. Automotive manufacturers are increasingly integrating airbag systems with occupant monitoring sensors and centralized vehicle electronics to improve deployment precision. Investment in next-generation safety validation and digital crash simulation platforms has accelerated development cycles while reducing testing complexity. Strategic collaborations between OEMs and safety-system suppliers continue strengthening regional deployment capabilities and product innovation pipelines.

United States Market Outlook: The United States remains the largest market in North America due to its extensive passenger vehicle production ecosystem, advanced safety regulations, and strong consumer focus on vehicle protection technologies. More than 90% of newly produced passenger vehicles incorporate comprehensive multi-airbag configurations. Automotive manufacturers are prioritizing software-enabled restraint systems, while suppliers continue expanding engineering centers focused on occupant sensing, predictive deployment algorithms, and integrated safety electronics. The country's strong testing infrastructure and premium vehicle segment support continued adoption of advanced airbag technologies.

Europe accounted for nearly 20% of global demand, supported by stringent vehicle safety regulations, premium automotive manufacturing, and advanced occupant protection standards. Vehicle safety ratings strongly influence purchasing decisions, encouraging widespread deployment of side-curtain, knee, and advanced frontal airbags. More than 75% of premium passenger vehicles launched in Europe feature enhanced occupant sensing technologies integrated with restraint systems. Manufacturers are increasingly adopting lightweight airbag materials and digital engineering tools to optimize vehicle efficiency while maintaining safety performance. Regulatory modernization and continuous safety benchmarking remain central drivers of deployment strategies across the region.

Germany Market Outlook: Germany serves as the technological center of Europe's passenger car airbag industry due to its concentration of premium automotive manufacturers and safety engineering expertise. The country contributes a significant share of European passenger vehicle production and remains a leader in integrating advanced restraint systems into luxury and performance vehicle platforms. German OEMs continue investing in adaptive deployment technologies, digital crash simulation, and software-defined safety architectures. Strong collaboration between automakers and component suppliers supports rapid commercialization of next-generation occupant protection solutions.

Asia-Pacific maintained the leading market position with approximately 48% share in 2025, supported by large-scale passenger vehicle production, expanding safety regulations, and increasing multi-airbag adoption across mass-market vehicle segments. The region accounts for more than half of global passenger vehicle manufacturing activity, creating significant deployment demand for airbag modules, sensors, and inflators. Vehicle safety upgrades in China and India are accelerating installation rates, while localized manufacturing strategies improve cost efficiency and supply-chain resilience. Automotive suppliers continue expanding production facilities and automation capabilities to support growing OEM requirements and export demand.

China Market Outlook: China remains the most influential country in the global passenger car airbag ecosystem, producing over 31 million vehicles annually and accounting for roughly one-third of worldwide passenger vehicle output. The country benefits from strong domestic demand, extensive automotive supply chains, and increasing implementation of advanced safety standards. Local manufacturers are investing heavily in intelligent restraint systems, occupant monitoring technologies, and automated production facilities. Growing electric vehicle production further strengthens demand for redesigned airbag architectures optimized for next-generation vehicle platforms.

South America accounted for nearly 6% of global market activity, supported by expanding vehicle safety awareness and increasing integration of multi-airbag systems into locally produced passenger vehicles. Regulatory improvements and consumer preference for safer vehicles are encouraging manufacturers to standardize advanced restraint systems across a wider range of vehicle models. Vehicle production recovery and modernization initiatives have strengthened deployment opportunities, although supply-chain efficiency and component localization remain ongoing priorities. Manufacturers are increasingly aligning local vehicle programs with international safety specifications to improve competitiveness and product positioning.

Brazil Market Outlook: Brazil represents the largest passenger car airbag market in South America due to its established automotive manufacturing sector and extensive vehicle assembly infrastructure. The country accounts for more than half of regional passenger vehicle production, creating substantial demand for safety components and integrated restraint systems. Automotive manufacturers continue expanding localized sourcing strategies while upgrading production lines to accommodate enhanced safety requirements. Growing adoption of advanced airbag configurations in compact passenger vehicles is improving safety technology penetration across the domestic market.

Middle East & Africa represented approximately 4% of global market demand in 2025, driven by vehicle fleet modernization, rising safety awareness, and growing investment in automotive manufacturing initiatives. Several countries are strengthening vehicle safety frameworks, encouraging broader adoption of advanced restraint systems in passenger vehicles. Import-dependent markets continue upgrading vehicle standards while local assembly activities gradually expand. Investments in industrial diversification programs and automotive infrastructure are creating new opportunities for safety-system deployment. Manufacturers are responding through distribution partnerships, localized assembly support, and expanded aftermarket service networks.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the most strategically important market within the region due to its automotive industrialization initiatives, infrastructure investment programs, and expanding vehicle assembly activities. National economic diversification efforts are encouraging development of domestic automotive capabilities and advanced manufacturing facilities. Passenger vehicle imports increasingly prioritize enhanced safety specifications, while local production projects are creating demand for globally compliant restraint systems. Continued investment in industrial zones and automotive partnerships strengthens the country's position as a future hub for vehicle safety technology deployment in the region.

The Passenger Car Airbag Market is led by global safety specialists including Autoliv, Joyson Safety Systems, ZF Lifetec, Toyoda Gosei, and Hyundai Mobis, which compete directly against regional manufacturers and emerging low-cost suppliers. Competition is primarily between technology leaders focused on advanced restraint systems and cost-focused manufacturers targeting high-volume vehicle platforms. The top five players collectively control approximately 68–72% of global market share, creating a concentrated competitive environment. Technology performance, deployment reliability, and supply-chain control have become decisive differentiators, with advanced multi-airbag systems delivering nearly 20% higher crash-response precision and lightweight designs reducing module weight by 8–12%. Companies are expanding local production, strengthening OEM partnerships, and vertically integrating inflator, textile, and sensor manufacturing to secure contracts. The competitive shift is moving toward software-enabled occupant protection and intelligent deployment systems rather than conventional hardware differentiation. High validation costs, regulatory certification requirements, and OEM qualification cycles create significant entry barriers. Winning requires integrated safety innovation, manufacturing scale, supply resilience, and deep vehicle-platform partnerships.

Joyson Safety Systems

Toyoda Gosei Co., Ltd.

ZF Lifetec

Hyundai Mobis

Ashimori Industry Co., Ltd.

Nihon Plast Co., Ltd.

Daicel Corporation

Yanfeng Automotive Safety Systems

East JoyLong Motor Airbag Co., Ltd.

Jiangsu Favour Automotive Safety Systems Co., Ltd.

Nippon Kayaku Co., Ltd.

Key Safety Systems

Tokai Rika Co., Ltd.

Passenger car airbag technology is shifting from conventional crash-triggered deployment toward intelligent occupant protection systems. AI-enabled occupant sensing, camera-based monitoring, and advanced electronic control units are increasingly integrated into vehicle safety architectures. More than 55% of premium passenger vehicle platforms now deploy enhanced occupant detection technologies, improving deployment precision by approximately 20% compared with legacy sensor-only systems. Automakers benefit from improved crash performance and reduced false deployment risks, while suppliers gain stronger differentiation through software-enabled safety capabilities.

Emerging technologies include adaptive airbags, predictive crash algorithms, and lightweight textile engineering. New-generation airbag modules reduce component weight by 8–12% while maintaining protection performance. Compared with traditional deployment architectures, integrated occupant monitoring systems provide faster decision-making and enhanced restraint customization during collisions. Adoption rates for side-curtain and advanced side-impact airbags now exceed 70% in premium vehicle segments. Companies such as Autoliv, Joyson Safety Systems, and Toyoda Gosei are strengthening investments in intelligent restraint platforms to secure long-term OEM programs.

Between 2026 and 2028, disruptive innovation will focus on autonomous vehicle safety, self-supporting center airbags, and connected occupant protection ecosystems. Suppliers capable of combining software intelligence, sensor integration, and scalable manufacturing will achieve stronger competitive positioning as vehicle safety systems become increasingly data-driven and platform-centric.

January 2026 – Toyoda Gosei announced its curtain airbag adoption on IM Motors' LS9 electric vehicle, marking its first airbag deployment with a Chinese automaker. The new design is 15% smaller while maintaining protection performance, strengthening the company's position in China's premium EV safety segment. Source: www.toyoda-gosei.com

December 2025 – Toyoda Gosei developed a self-supporting front center airbag designed for future autonomous vehicle interiors. The system eliminates dependence on center-console support structures, improving installation flexibility across vehicle platforms and enhancing occupant protection for evolving cabin layouts.

October 2025 – Toyoda Gosei launched a specialized curtain airbag for Honda's new Prelude sports coupe. The solution supports rollover protection while fitting within constrained coupe interiors, enabling advanced safety integration without compromising vehicle design requirements.

May 2026 – Autoliv announced the transfer of production from its Turkey operations as part of manufacturing optimization. The facility employs approximately 2,200 workers, representing about 4% of its global workforce, reflecting industry-wide restructuring and capacity realignment strategies.

This report provides comprehensive analysis of the Passenger Car Airbag Market across major airbag types, applications, end-user categories, and key geographic regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The study evaluates deployment patterns across frontal, side, curtain, knee, and emerging airbag technologies while assessing adoption trends across conventional passenger vehicles, premium models, and electric vehicle platforms. More than 85% of new passenger vehicle programs now incorporate multi-airbag configurations, making segmentation analysis critical for understanding evolving demand patterns.

The report further examines competitive positioning, manufacturing strategies, supply-chain developments, regulatory influences, and technology innovation. Coverage includes intelligent occupant sensing, adaptive deployment systems, lightweight materials, and software-enabled safety architectures. Strategic insights support investment prioritization, product development, regional expansion planning, partnership evaluation, and operational benchmarking between 2026 and 2033. Particular attention is given to emerging opportunities in electric mobility, connected safety ecosystems, and advanced occupant protection technologies shaping long-term industry direction.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,645.0 Million |

| Market Revenue (2033) | USD 2,404.6 Million |

| CAGR (2026–2033) | 4.86% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Autoliv Inc.; Joyson Safety Systems; Toyoda Gosei Co., Ltd.; ZF Lifetec; Hyundai Mobis; Ashimori Industry Co., Ltd.; Nihon Plast Co., Ltd.; Daicel Corporation; Yanfeng Automotive Safety Systems; East JoyLong Motor Airbag Co., Ltd.; Jiangsu Favour Automotive Safety Systems Co., Ltd.; Nippon Kayaku Co., Ltd.; Key Safety Systems; Tokai Rika Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |