Reports

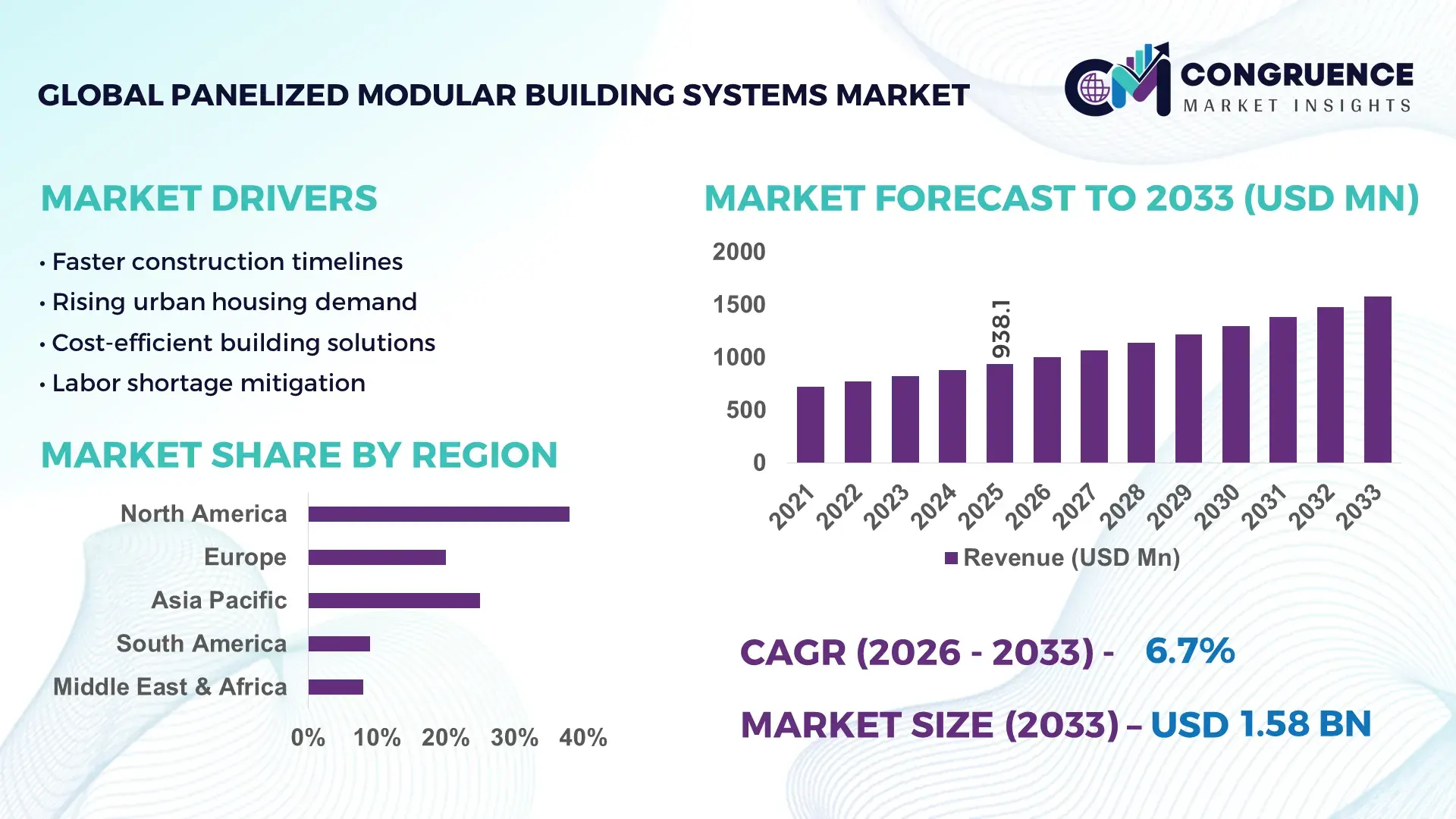

The Global Panelized Modular Building Systems Market was valued at USD 938.11 Million in 2025 and is anticipated to reach a value of USD 1576.05 Million by 2033 expanding at a CAGR of 6.7% between 2026 and 2033. Growth is driven by rising demand for faster construction timelines, sustainable building solutions, and cost-efficient modular infrastructure.

The United States leads the Panelized Modular Building Systems Market with advanced manufacturing capabilities and significant investment in prefabricated construction technologies. The country hosts over 120 large-scale panelized system manufacturing facilities, producing more than 2 million modular panels annually. Technological advancements include precision CNC fabrication, automated panel assembly, and integrated BIM (Building Information Modeling) planning tools. Key industry applications span residential housing, educational institutions, healthcare facilities, and commercial offices, with urban development projects driving strong adoption. Consumer adoption is notable in metropolitan regions, where over 42% of newly constructed single-family homes incorporate modular panels for improved energy efficiency and reduced construction time.

Market Size & Growth: Valued at USD 938.11 Million in 2025 and projected to reach USD 1576.05 Million by 2033 at a CAGR of 6.7%, fueled by urbanization and sustainability-driven construction.

Top Growth Drivers: Construction speed +35%, energy efficiency improvement +28%, labor cost reduction +22%.

Short-Term Forecast: By 2028, automated panel fabrication is expected to reduce material waste by 18% and construction downtime by 15%.

Emerging Technologies: CNC panel cutting, BIM-integrated design, smart sensor-enabled modular systems.

Regional Leaders: North America projected at USD 612 Million by 2033 with high residential adoption, Europe at USD 412 Million driven by eco-compliant commercial projects, Asia-Pacific at USD 352 Million with government-supported modular housing programs.

Consumer/End-User Trends: Residential developers and public infrastructure projects increasingly prefer panelized solutions for faster timelines and predictable quality.

Pilot or Case Example: In 2024, a California residential project reduced construction time by 20% using fully integrated panelized systems.

Competitive Landscape: Market leader Laing O’Rourke holds approximately 16% share, followed by Skanska, Katerra, Sekisui House, and Red Sea Housing Services.

Regulatory & ESG Impact: Incentives for sustainable construction, energy-efficient building codes, and carbon emission reduction policies are boosting market adoption.

Investment & Funding Patterns: Over USD 450 Million invested recently in automated panelized plant facilities, with rising project financing and venture funding for innovative modular startups.

Innovation & Future Outlook: Integration of AI in design optimization, hybrid timber-concrete panels, and prefabricated smart housing solutions are shaping market expansion.

The Panelized Modular Building Systems Market is seeing widespread adoption across residential, commercial, and institutional sectors. Technological innovations such as precision CNC manufacturing, AI-driven panel design, and prefabricated hybrid materials are improving construction efficiency and quality. Regional consumption trends show rapid uptake in North America and Europe due to sustainability regulations and labor cost pressures, while Asia-Pacific benefits from government-supported urban housing projects. Emerging trends include smart panel integration, eco-friendly composite materials, and scalable modular construction for disaster-resilient infrastructure, positioning the market for sustained growth in the next decade.

The Panelized Modular Building Systems Market is strategically relevant as it enables faster, more efficient construction while reducing labor costs and material waste. Advanced CNC-cut timber panels deliver 18% higher precision compared to traditional on-site framing, enhancing structural consistency and reducing rework. North America dominates in volume due to established modular infrastructure, while Europe leads in adoption, with over 37% of commercial construction enterprises integrating panelized systems into their projects. By 2028, AI-driven design optimization is expected to improve panel utilization and reduce material waste by 20%, streamlining the supply chain from factory to site.

Firms are committing to ESG improvements such as 25% reduction in construction-site timber waste and increased recycling of off-cuts by 2027. In 2024, a California-based residential developer achieved a 15% reduction in labor hours through automated panelized assembly combined with BIM integration, demonstrating measurable operational efficiency. Panelized modular systems are increasingly applied across residential, commercial, and educational facilities, providing scalable solutions for urban expansion while meeting environmental and regulatory standards. Forward-looking strategies involve integrating smart sensors, sustainable composite materials, and AI-driven logistics, positioning the Panelized Modular Building Systems Market as a pillar of resilience, compliance, and sustainable growth.

Rapid urbanization and rising housing shortages have accelerated adoption of panelized modular systems. In metropolitan areas, panelized construction reduces on-site assembly time by up to 30%, allowing developers to complete projects faster and minimize labor costs. Residential developers report that prefabricated panels cut material waste by 18% compared to conventional construction. Governments in North America and Asia-Pacific are incentivizing modular housing programs, leading to over 40% of new urban housing projects incorporating panelized panels in 2024. Commercial facilities, including offices and educational institutions, are increasingly deploying panelized modular systems for quick, code-compliant construction, further driving market growth.

High upfront capital expenditure for automated panel fabrication plants and CNC machinery limits entry for smaller construction firms. Establishing reliable supply chains for raw timber or composite materials is critical, and shortages or transport delays can stall projects. In Europe, 2024 data shows that 28% of mid-sized developers delay panelized projects due to material sourcing or logistics constraints. Additionally, skilled labor trained in modular assembly is limited in certain regions, further constraining adoption. While long-term savings are significant, initial financial and logistical hurdles continue to restrain faster market expansion, particularly in emerging markets with fragmented construction ecosystems.

The market is poised to benefit from incorporating smart materials, such as thermally insulated hybrid panels and sensors for structural monitoring. These innovations improve energy efficiency and operational safety in residential and commercial buildings. In 2025, pilot projects using cross-laminated timber panels with embedded sensor networks reported a 12% improvement in thermal regulation and a 9% reduction in maintenance interventions. Government incentives for green buildings and eco-certified construction materials in Europe and North America present opportunities for panelized modular manufacturers to differentiate products. The rising demand for disaster-resilient housing and sustainable urban development further expands growth prospects for innovative panelized solutions.

Fluctuating timber and composite material costs impact manufacturing profitability and project budgeting. In 2025, North American suppliers reported a 14% increase in softwood pricing, affecting panelized system cost structures. Regulatory compliance, including adherence to fire safety, seismic standards, and energy efficiency codes, increases project planning complexity and engineering costs. In emerging markets, inconsistent building codes can delay approvals for panelized modular projects. Transportation and handling of large panels also pose logistical challenges, with regional infrastructure constraints contributing to potential project delays. These combined factors create operational and financial barriers, requiring strategic planning and risk mitigation for sustainable market growth.

• Expansion of Prefabricated Residential Solutions: The use of prefabricated panelized systems in residential projects has increased substantially, with 48% of newly built single-family homes in North America in 2025 incorporating panelized panels for faster construction. Automated off-site fabrication reduced labor requirements by 22% and construction timelines by approximately 18%, allowing developers to accelerate project delivery while maintaining quality and compliance with energy codes.

• Integration of Smart Building Technologies: Over 35% of new commercial and institutional panelized modular projects in Europe now incorporate embedded sensors and IoT-enabled panels for real-time monitoring of structural integrity, energy consumption, and environmental conditions. These systems have delivered measurable performance improvements, including up to 12% enhanced thermal efficiency and a 9% reduction in maintenance interventions during the first year of operation.

• Adoption of Sustainable and Low-Carbon Materials: Approximately 42% of panelized modular building manufacturers in Asia-Pacific have shifted to engineered timber and hybrid composite panels to meet sustainability targets. These materials reduce embodied carbon by up to 28% compared to traditional construction materials, supporting regional green building regulations and investor ESG commitments. The trend is particularly strong in metropolitan areas with high-density urban development projects.

• Technological Automation and Process Optimization: CNC machining, automated panel assembly, and BIM-integrated workflows are now deployed in over 60% of large-scale panelized production facilities globally. This trend has improved precision by 18%, decreased material waste by 15%, and shortened production cycles, enabling manufacturers to meet increasing project demand efficiently while ensuring standardized quality across multiple sites.

The Panelized Modular Building Systems Market is segmented by product type, application, and end-user, providing a detailed understanding of market dynamics and adoption patterns. By type, the market includes structural wall panels, floor panels, roof panels, and hybrid composite panels, each serving specific construction needs. Applications span residential housing, commercial offices, educational institutions, healthcare facilities, and public infrastructure projects. End-user segmentation highlights developers, contractors, government agencies, and institutional buyers, illustrating varying adoption trends based on project scale, sustainability requirements, and construction speed priorities. Regional variations also influence segmentation, with metropolitan areas emphasizing residential and commercial applications, while emerging markets prioritize government-led infrastructure initiatives. Understanding these segments enables decision-makers to tailor investments, optimize production planning, and align product offerings with evolving market demand.

Structural wall panels currently account for 44% of market adoption, making them the leading product type due to their essential role in load-bearing construction and quick on-site assembly. Floor panels hold a 26% share, widely used for rapid multi-story residential and commercial builds. Roof panels contribute approximately 15% of adoption, primarily in residential and institutional projects, while hybrid composite panels, including timber-concrete combinations, currently make up 15% but are the fastest-growing segment due to improved thermal efficiency, fire resistance, and sustainability credentials. These panels are increasingly deployed in urban housing projects in North America and Europe.

Residential construction leads with a 52% adoption rate, driven by the demand for faster housing delivery and improved energy efficiency in metropolitan regions. Commercial office buildings hold a 21% share, with developers utilizing panelized systems for predictable timelines and high-quality finishes. Educational and healthcare facilities account for 17%, where compliance with regulatory standards and sustainable construction is critical. Public infrastructure projects contribute 10%, mainly in modular administrative buildings or emergency shelters. The fastest-growing application is commercial modular offices, benefiting from AI-enabled design optimization and pre-assembled panel kits, which reduce project downtime by up to 15%.

Developers represent the leading end-user segment with 48% adoption, reflecting their focus on rapid construction, cost efficiency, and quality control. Government and municipal agencies contribute 22%, primarily in educational, healthcare, and emergency infrastructure projects. Contractors account for 18%, leveraging pre-fabricated panels to streamline multi-site construction, while institutional buyers, including hospitals and universities, hold 12%, emphasizing compliance and sustainability. The fastest-growing end-user segment is mid-size commercial contractors, driven by demand for pre-engineered panel systems that reduce on-site labor by 20–25%.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

North America led with approximately 360,000 modular panels produced in 2025, with over 45% of residential developers adopting panelized modular systems for multi-family housing and commercial offices. Asia-Pacific currently ranks second in volume at 280,000 units, with China and India contributing 65% of regional demand due to government-supported urban housing and infrastructure programs. Europe follows closely with 210,000 units, led by Germany, the UK, and France. South America and Middle East & Africa collectively account for 12% of global production, with growing adoption in public infrastructure and commercial applications. Regional trends indicate high enterprise adoption in North America, regulatory-driven green construction in Europe, and fast urbanization-driven demand in Asia-Pacific.

How is North America leveraging modular systems for faster and sustainable construction?

North America holds approximately 38% of the global market, driven by residential housing, commercial offices, and educational projects. Government incentives promoting energy-efficient construction and sustainable building materials have accelerated adoption. Technological advancements such as CNC-cut panels, BIM-integrated design, and automated on-site assembly are widely implemented. Local player Laing O’Rourke operates advanced prefabrication facilities producing over 90,000 panels annually, improving precision and reducing labor costs by 20%. Enterprise adoption is higher in healthcare and finance sectors, where speed and compliance are critical. Regional consumer behavior shows growing preference for sustainable, high-quality modular housing and mixed-use commercial developments.

What is driving panelized modular system adoption across key European markets?

Europe accounts for roughly 26% of the global market, with Germany, the UK, and France leading adoption. Regulatory pressure for energy-efficient and low-carbon construction has increased demand for panelized modular systems. Emerging technologies such as hybrid timber-concrete panels and IoT-enabled monitoring systems are being integrated into commercial and educational projects. Sekisui House and Skanska have deployed smart panelized facilities across multiple European cities, reducing construction timelines by 15%. European consumers prioritize compliance and sustainability, with 42% of developers in Germany and the UK specifying eco-certified panels for urban housing and institutional projects.

Why is Asia-Pacific emerging as a major hub for panelized modular buildings?

Asia-Pacific holds a market volume of 280,000 units in 2025, with China, India, and Japan as top consumers. The region is characterized by rapid urbanization, large-scale infrastructure development, and expansion of residential complexes. Manufacturers are increasingly investing in automated panel factories and prefabrication hubs. Local player Red Sea Housing Services is producing 35,000 panels annually in India for multi-family housing projects. Regional consumer behavior reflects strong government-backed adoption, with 55% of urban housing projects in China utilizing modular panels for speed, cost efficiency, and energy compliance.

How is South America integrating panelized modular systems in infrastructure projects?

South America accounts for 7% of the global market, with Brazil and Argentina as key contributors. Government incentives for affordable housing and infrastructure modernization are driving panelized system adoption. Construction of public offices and healthcare facilities increasingly uses prefabricated wall and floor panels to reduce timelines and labor costs. Local manufacturer Construmod has launched pilot projects in São Paulo, producing 6,500 panels for multi-story residential buildings. Regional consumer behavior indicates growing demand for modular systems in urban centers, particularly where rapid development is paired with government housing initiatives.

What factors are shaping panelized modular building adoption in Middle East & Africa?

Middle East & Africa represents 5% of the market, with UAE and South Africa leading regional adoption. The oil & gas, commercial, and government infrastructure sectors are the primary drivers. Technological modernization includes CNC panel cutting, automated assembly, and lightweight composite panels. Local player Red Sea Housing Services is expanding modular production facilities in Johannesburg, providing panels for emergency housing and commercial projects. Consumer behavior varies: the UAE prioritizes luxury and energy-efficient panelized buildings, while South Africa focuses on affordable, rapid-deployment housing. Trade partnerships and regional regulations supporting sustainability also boost adoption.

United States: 38% market share – High production capacity and extensive adoption in residential and commercial projects.

China: 27% market share – Strong government-supported urban housing programs and rapid infrastructure development driving demand.

The Panelized Modular Building Systems market is moderately fragmented, with over 120 active competitors globally, ranging from large-scale manufacturers to regional modular construction specialists. The top five players—Laing O’Rourke, Sekisui House, Skanska, Red Sea Housing Services, and Katerra—collectively hold approximately 42% of the market, reflecting both competitive intensity and opportunities for smaller entrants. Strategic initiatives in the market include collaborations between technology providers and construction firms, launches of automated panel fabrication facilities, and integration of BIM and IoT-enabled panels to enhance efficiency and sustainability. In 2025, at least 18 new partnerships were established globally to streamline prefabrication logistics and expand product offerings across residential, commercial, and institutional sectors. Innovation trends such as hybrid timber-concrete panels, AI-optimized design layouts, and digital supply chain platforms are shaping competitive positioning, enabling firms to reduce material waste by 15–20% and accelerate project delivery by up to 18%. Market players are also increasingly aligning with ESG-focused construction and green certification programs to differentiate products and gain regulatory compliance advantages.

Red Sea Housing Services

Katerra

BMarko Structures

Champion Homes

ModSpace

Algeco Scotsman

ICON Build

The Panelized Modular Building Systems market is witnessing rapid technological evolution, driven by automation, smart materials, and digital design integration. CNC (computer numerical control) machining is widely adopted, enabling the precise cutting of structural wall, floor, and roof panels, which has improved dimensional accuracy by up to 18% and reduced material waste by 15% in large-scale projects. Automated panel assembly lines are increasingly deployed, allowing factories to produce over 90,000 panels annually with consistent quality and faster turnaround times.

BIM (Building Information Modeling) integration has become a critical enabler for design, logistics, and on-site assembly. Over 62% of commercial and residential projects in North America now utilize BIM workflows to optimize panel layouts, detect design conflicts, and streamline supply chain planning, reducing assembly errors by 12–14%. Smart sensors embedded in hybrid panels monitor structural integrity, temperature, and moisture levels in real-time, enhancing building safety and operational efficiency.

Emerging materials, such as cross-laminated timber (CLT) and hybrid timber-concrete composites, are enhancing fire resistance, thermal performance, and environmental sustainability. In Asia-Pacific, over 35% of new residential developments have adopted engineered timber panels, reducing embodied carbon by approximately 28%. AI-driven design software is also being applied to optimize panel dimensions and reduce on-site labor requirements, resulting in a reported 20% decrease in project assembly time during pilot programs in 2024. Additionally, 3D printing and robotic fabrication technologies are gradually being integrated into modular panel production, supporting custom design applications and complex architectural requirements. These innovations are transforming the market by enabling faster, safer, and more sustainable panelized construction solutions.

• In April 2024, the National Association of Home Builders (NAHB) launched a dedicated educational video series on panelized and off‑site construction methods, aimed at informing builders and developers about best practices, digital integration, and efficiency improvements within modular panel workflows.

• In February 2024, Timber Age Systems secured USD 3.9 million in Colorado Proposition 123 funding to establish a new CLT (cross‑laminated timber) panel factory in Mancos, projecting production capacity of 122 homes annually and supporting a statewide push for affordable, sustainable housing.

• In March 2025, Bechtel Corp. completed the acquisition of Modular Build Solutions Ltd., expanding its panelized modular wall and floor system portfolio and increasing manufacturing capacity to support large‑scale urban construction projects.

• In September 2025, Bouygues Construction partnered with PlanGrid to integrate real‑time assembly tracking and digital workflow optimization into panelized modular building operations, enhancing quality control and on‑site coordination across multiple construction sites.

The Panelized Modular Building Systems Market Report provides a focused analysis of product types, applications, regions, technologies, and end-users. It covers structural wall panels, floor panels, roof panels, hybrid composites, and high-insulation systems, evaluated for performance, assembly efficiency, and safety compliance. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional adoption patterns, regulatory influences, and infrastructure deployment trends. Applications include residential, commercial, healthcare, educational, government, and specialized facilities such as climate-controlled or disaster-resilient structures.

Technological insights examine BIM integration, AI-enabled design, CNC and robotic fabrication, IoT monitoring, and advanced materials like cross-laminated timber and hybrid composites. The report also addresses supply chain logistics, quality assurance practices, and lean manufacturing methods that optimize production and delivery timelines. End-user analysis profiles developers, contractors, institutional buyers, and integrated construction firms, focusing on procurement behavior, adoption trends, and project requirements. Niche segments, including smart modular systems and rapid deployment solutions, are evaluated to guide strategic planning, investment decisions, and competitive positioning within the evolving market landscape.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD V2025 Million |

Market Revenue in 2033 | USD V2033 Million |

CAGR (2026 - 2033) | 6.7% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Laing O’Rourke, Sekisui House, Skanska, Red Sea Housing Services, Katerra, BMarko Structures, Champion Homes, ModSpace, Algeco Scotsman, ICON Build |

Customization & Pricing | Available on Request (10% Customization is Free) |