Reports

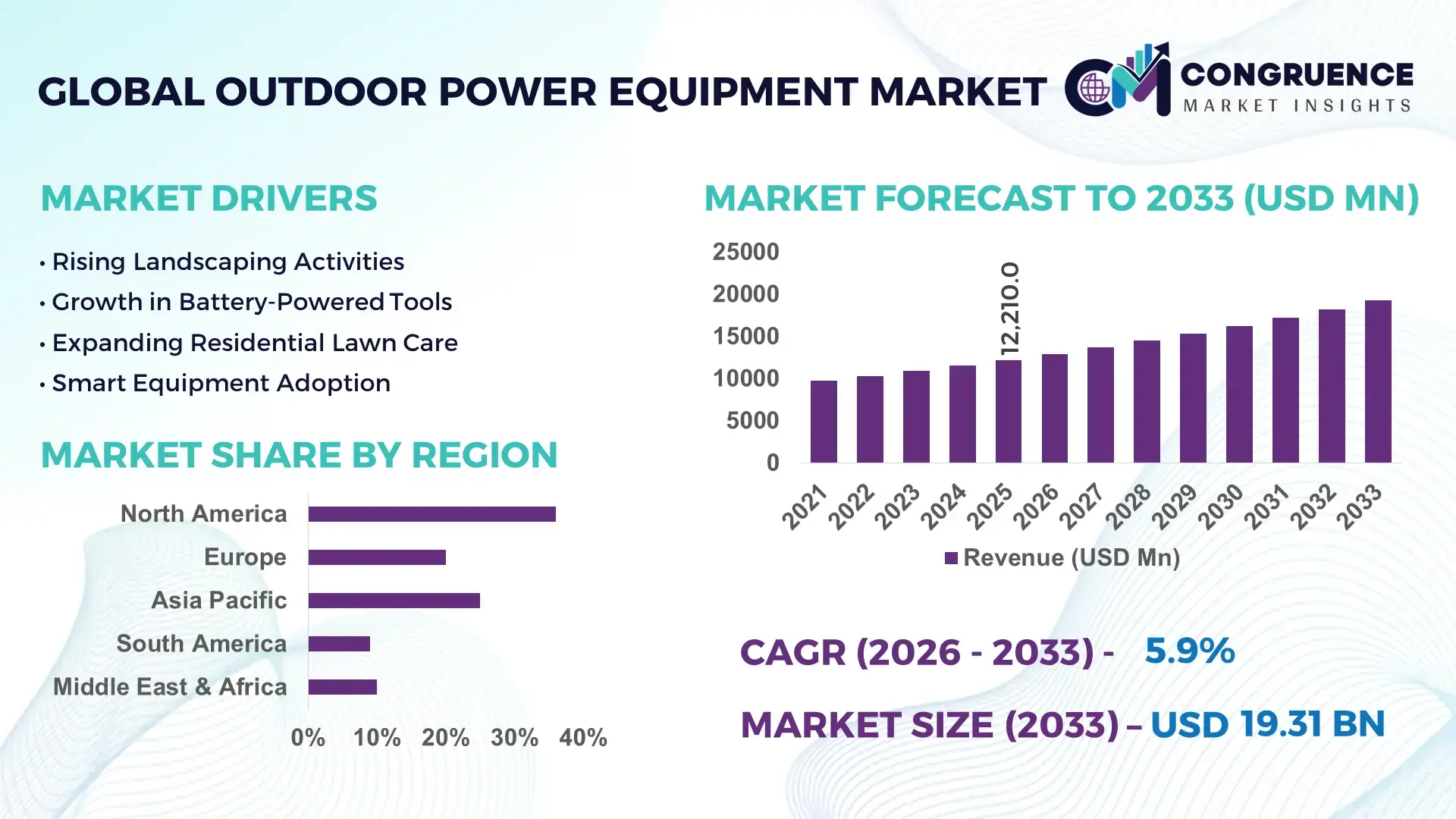

The Global Outdoor Power Equipment Market was valued at USD 12210 Million in 2025 and is anticipated to reach a value of USD 19314.49 Million by 2033 expanding at a CAGR of 5.9% between 2026 and 2033.

Rapid electrification of landscaping and turf maintenance equipment is strengthening market expansion, with battery-powered outdoor systems reducing operating expenses by nearly 21% and lowering maintenance frequency by approximately 28% compared with conventional gasoline-powered equipment. Between 2024 and 2026, stricter emission-control regulations across North America and Europe accelerated replacement demand for low-noise cordless equipment, while manufacturers diversified sourcing operations toward Southeast Asia and Mexico following Red Sea logistics disruptions and rising trans-Pacific freight costs.

The United States continues to dominate the global outdoor power equipment market with nearly 32% share of total industry demand, supported by large-scale residential landscaping, municipal green infrastructure investments, and commercial turf maintenance contracts. More than USD 1.5 billion was allocated toward robotic mowing systems, lithium-ion battery integration, and smart equipment manufacturing upgrades between 2024 and 2026. Commercial landscaping applications represent approximately 44% of total equipment utilization, while cordless outdoor tools surpassed 48% household adoption in 2025. Compared with traditional fuel-powered systems, advanced electric outdoor equipment reduces operational noise by over 35%, improving deployment across urban municipalities and regulated residential zones.

Manufacturers expanding battery technology capabilities, localized production networks, and AI-enabled fleet management platforms are securing stronger long-term positioning across commercial landscaping and municipal infrastructure maintenance contracts.

Market Size & Growth: The global outdoor power equipment market was valued at USD 12210 Million in 2025 and is projected to reach USD 19314.49 Million by 2033 at a CAGR of 5.9%, supported by rapid battery-powered equipment adoption and commercial landscaping modernization.

Top Growth Drivers: Battery-powered equipment demand increased by 26%, robotic mower installations rose 18%, and commercial fleet electrification expanded by 22% between 2024 and 2026.

Short-Term Forecast: By 2027, AI-enabled fleet monitoring systems are expected to reduce maintenance downtime by 17% and improve operational efficiency by nearly 21% across professional landscaping operations.

Emerging Technologies: Autonomous mowing systems, IoT-enabled diagnostics, and high-density lithium-ion batteries improved equipment productivity by more than 24% across commercial outdoor maintenance applications.

Regional Leaders: North America is projected to exceed USD 6.3 Billion through high cordless equipment penetration, Europe is approaching USD 4.1 Billion due to emission-control regulations, and Asia-Pacific is crossing USD 5 Billion with expanding urban infrastructure projects.

Consumer/End-User Trends: More than 48% of residential consumers shifted toward cordless outdoor tools, while connected equipment procurement among commercial landscaping firms increased by 29% in 2025.

Pilot/Case Example: A 2025 municipal landscaping modernization program in North America reduced fuel consumption by 23% and lowered operational noise levels by 34% through battery-powered mower deployment.

Competitive Landscape: Leading manufacturers collectively account for nearly 38% of global industry share, with competitive expansion focused on robotic systems, battery platforms, and connected outdoor equipment portfolios.

Regulatory & ESG Impact: Urban emission-control regulations and municipal noise restrictions reduced gasoline-powered equipment utilization by 14% across several metropolitan landscaping projects between 2024 and 2026.

Investment & Funding: Industry-wide investments exceeded USD 3.2 billion in 2025, led by battery production expansion, automation partnerships, and regional manufacturing facility upgrades.

Innovation & Future Outlook: Next-generation robotic landscaping systems, AI-driven predictive servicing, and swappable battery ecosystems are accelerating strategic transition toward fully connected outdoor maintenance operations.

Commercial landscaping contributes nearly 44% of total outdoor power equipment demand, followed by residential lawn maintenance and municipal infrastructure applications. Battery-powered equipment adoption exceeded 48% across residential users in 2025, while robotic mowing systems recorded installation growth of 18% due to rising labor optimization requirements. North America maintains leadership through large-scale landscaping activity, whereas Asia-Pacific is witnessing faster equipment deployment linked to urban infrastructure expansion and localized manufacturing investments. Increasing regulatory pressure on fuel-powered equipment and ongoing supply chain regionalization are accelerating innovation in cordless systems, smart diagnostics, and autonomous outdoor maintenance technologies, creating a stronger foundation for long-term competitive differentiation and operational efficiency strategies.

The outdoor power equipment market is rapidly transforming into a high-priority investment segment as electrification, automation, and smart landscaping technologies redefine operational efficiency across residential, commercial, and municipal applications. Competitive intensity is accelerating as manufacturers shift from conventional fuel-powered machinery toward connected, battery-driven ecosystems capable of lowering servicing costs, optimizing fleet productivity, and meeting tightening environmental regulations. Global supply chain restructuring and stricter emission-control policies between 2024 and 2026 are forcing manufacturers to regionalize production, secure battery supply partnerships, and accelerate low-noise equipment deployment across urban markets. Advanced lithium-ion outdoor systems improve operational efficiency by nearly 24% while reducing annual maintenance costs by approximately 28% compared to legacy gasoline-powered equipment. North America leads in overall equipment volume, while Europe leads in electrified equipment adoption with nearly 46% penetration across professional landscaping operations.

Over the next two to three years, AI-enabled fleet monitoring and autonomous mowing technologies are expected to reduce equipment downtime by 18% and improve workforce productivity by more than 20%. Sustainability positioning is also becoming a measurable competitive advantage, with battery-powered outdoor systems lowering carbon emissions by nearly 32% and strengthening access to municipal procurement contracts with strict compliance requirements. In 2025, a large-scale municipal landscaping modernization program in Northern Europe reduced fuel consumption by 25% through robotic mower deployment and centralized fleet analytics integration. Simultaneously, leading manufacturers are increasing capital allocation toward battery platforms, robotics partnerships, and regional assembly expansion to secure long-term supply resilience and technology leadership.

Battery-powered outdoor equipment is becoming the core growth engine of the market as commercial landscaping firms prioritize lower operating costs, reduced maintenance, and compliance with tightening emission regulations. Cordless equipment adoption increased by 26% between 2024 and 2026, while robotic mower deployment rose nearly 18% across municipal landscaping projects. Compared with gasoline-powered systems, advanced electric equipment lowers maintenance expenses by approximately 27% and reduces operational noise by over 35%. Fuel price volatility and stricter urban noise restrictions are forcing rapid replacement cycles across North America and Europe. In response, manufacturers are expanding lithium-ion production capacity, increasing investment in robotic platforms, and strengthening regional assembly operations in Southeast Asia and Mexico to stabilize supply chains and improve delivery efficiency.

Battery dependency and raw material volatility continue constraining large-scale market expansion, particularly across price-sensitive residential equipment categories. Lithium-ion battery systems account for nearly 35% of total production cost in premium cordless outdoor equipment, while battery component prices increased by approximately 19% between 2024 and 2025. Global logistics disruptions also increased equipment lead times by nearly 14% across several major markets. Supply concentration across limited lithium-processing regions is increasing procurement risks for manufacturers and dealers. To reduce exposure, companies are securing long-term mineral agreements, diversifying supplier networks, and investing in alternative battery chemistries with lower rare-earth dependency to improve long-term production stability and margin control.

Connected landscaping ecosystems are creating a major growth opportunity as contractors and municipalities invest in automation, predictive maintenance, and AI-enabled fleet management. Smart fleet systems improve equipment utilization by nearly 22%, while autonomous mowing technologies reduce labor dependency by approximately 19% across large-scale commercial operations. IoT-enabled diagnostics also lower unplanned downtime by nearly 17%. Asia-Pacific is emerging as a high-growth deployment region due to expanding urban infrastructure and rising residential landscaping activity. Manufacturers are increasing R&D investment in robotics, swappable battery systems, and connected maintenance platforms to build recurring service-based revenue models and strengthen long-term ecosystem control.

Infrastructure limitations and performance consistency remain major execution barriers for large-scale electrification across the outdoor power equipment market. High-capacity battery systems require nearly 30% longer recharge time compared with fuel refueling processes, reducing operational flexibility for commercial landscaping fleets. Battery efficiency losses exceeding 20% during cold-weather conditions are also slowing adoption across several North American and European markets. Limited charging infrastructure and growing cybersecurity concerns linked to connected equipment platforms are further constraining enterprise-scale deployment. To remain competitive, manufacturers are accelerating investment in fast-charging systems, thermal battery management technologies, and secure connected fleet platforms capable of supporting reliable long-term commercial operations.

48% cordless adoption is reshaping residential and municipal equipment purchasing patterns. Contractors are replacing gasoline-powered systems with battery-driven platforms that reduce maintenance costs by 27% and operational noise by over 35%. Manufacturers are expanding regional battery assembly and restructuring dealer inventories toward cordless portfolios.

22% growth in robotic mower deployment is redefining commercial landscaping operations. Large contractors and municipalities are reducing labor dependency by nearly 19% through autonomous mowing systems and AI-enabled route optimization. Companies are accelerating robotics partnerships and predictive servicing integration.

31% increase in connected fleet monitoring adoption is shifting equipment management toward real-time analytics. Smart diagnostics platforms are reducing unexpected downtime by 17% while improving maintenance scheduling efficiency across commercial fleets. Contractors are prioritizing software compatibility over traditional engine-based differentiation.

26% expansion in Asia-Pacific equipment demand is forcing regional manufacturing realignment. Urban landscaping growth and localized infrastructure projects are increasing demand for compact electric equipment. Manufacturers are expanding Southeast Asian assembly operations to improve supply stability and delivery speed amid global logistics pressure.

The outdoor power equipment market is segmented by type, application, and end-user, with demand increasingly shifting toward cordless, automated, and connected equipment categories. Lawn mowers continue leading overall product demand due to strong residential and commercial landscaping usage, while trimmers, robotic equipment, and battery-powered tools are gaining faster adoption across urban maintenance operations. Lawn care and landscaping account for nearly 58% of application demand, supported by rising municipal green infrastructure projects and commercial fleet modernization. Commercial users remain the dominant end-user segment due to recurring maintenance requirements and high equipment utilization rates, while municipal procurement is accelerating through emission-control policies and low-noise equipment mandates. Residential cordless equipment adoption exceeded 48% in 2025, pushing manufacturers to expand battery-focused product portfolios and localized production strategies.

Lawn mowers dominate the outdoor power equipment market with nearly 38% share due to extensive residential usage, commercial landscaping demand, and rapid robotic integration. Their dominance is supported by broad scalability, higher replacement frequency, and increasing adoption of cordless platforms that lower maintenance costs by approximately 27%. Trimmers and edgers are the fastest-growing segment, expanding by nearly 21% between 2024 and 2026 due to rising urban landscaping activity and strong demand for lightweight battery-powered equipment. Compared with lawn mowers, trimmers offer lower ownership costs and faster electrification adoption across residential users. Chainsaws maintain stable demand in forestry applications, while blowers and snow throwers collectively account for approximately 29% of total product demand due to seasonal and municipal maintenance requirements.

Manufacturers are prioritizing robotic mowing systems, commercial-grade battery platforms, and compact cordless equipment to capture shifting demand toward low-noise and high-efficiency outdoor maintenance solutions.

“According to a 2025 report by the Outdoor Power Equipment Institute, battery-powered lawn mowers were adopted by over 46% of residential landscaping users, resulting in nearly 28% lower annual maintenance costs and improved operational efficiency, reinforcing their growing strategic importance.”

Lawn care leads the market with nearly 34% share due to recurring residential maintenance activity and large-scale commercial landscaping contracts. Usage concentration remains strongest across North America and Europe where professional turf maintenance services continue expanding through connected and cordless equipment deployment. Landscaping is the fastest-growing application segment, recording nearly 23% growth between 2024 and 2026 as municipalities and contractors increase adoption of robotic mowing systems and AI-enabled fleet management. Compared with traditional lawn care operations, landscaping applications are shifting faster toward automation and labor optimization technologies. Gardening, forestry, and snow removal collectively account for approximately 41% of total application demand, maintaining strategic relevance across seasonal and land management operations.

Manufacturers are expanding autonomous landscaping platforms, battery-powered maintenance systems, and fleet optimization solutions to capture rising demand for efficient outdoor maintenance operations.

“According to a 2025 report by the National Association of Landscape Professionals, smart landscaping equipment was deployed across more than 52,000 commercial maintenance operations, improving workforce productivity by nearly 24%, highlighting its rapid operational adoption.”

Commercial users dominate the outdoor power equipment market with approximately 42% share due to continuous landscaping operations, fleet-based equipment utilization, and high replacement frequency. Commercial contractors increasingly prioritize connected fleet platforms and battery-powered systems to reduce maintenance downtime and improve operational efficiency. Municipal users are emerging as the fastest-growing end-user segment, with adoption increasing by nearly 20% between 2024 and 2026 due to stricter urban emission regulations and low-noise equipment mandates. Compared with residential buyers focused on affordability, municipal procurement emphasizes compliance, durability, and fleet optimization capabilities. Residential and agriculture segments collectively account for nearly 39% of total market demand, supported by rising cordless equipment adoption and compact land maintenance requirements.

Manufacturers are introducing subscription-based servicing models, commercial battery platforms, and customized municipal fleet solutions to strengthen long-term customer retention and operational scalability.

“According to a 2025 report by the American Public Works Association, adoption among municipal landscaping departments increased by 21%, with over 18,000 organizations implementing battery-powered maintenance equipment, leading to nearly 26% fuel cost optimization and improved operational efficiency, indicating a strong shift in demand dynamics.”

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2026 and 2033.

North America continues leading global demand due to strong commercial landscaping activity, high residential equipment ownership, and rapid deployment of cordless outdoor systems. Europe accounts for nearly 28% of total market demand and leads in electrified equipment adoption through strict emission-control regulations and low-noise municipal maintenance policies. Asia-Pacific holds approximately 24% share and is accelerating through localized manufacturing expansion, infrastructure modernization, and rising landscaping demand across China, Japan, and India. South America and the Middle East & Africa are witnessing targeted growth through infrastructure upgrades and municipal maintenance investments. Supply chain regionalization and battery production expansion are forcing manufacturers to diversify assembly operations, with companies prioritizing Asia-Pacific production scalability and Europe-focused electrified equipment innovation.

North America holds approximately 36% of the global outdoor power equipment market, supported by large-scale commercial landscaping operations, strong residential lawn maintenance culture, and expanding municipal infrastructure spending. Commercial landscaping fleets account for nearly 43% of total equipment utilization, while cordless equipment adoption exceeded 49% in 2025 due to lower maintenance costs and emission-compliance advantages. Tightening urban noise regulations and stricter emission standards are accelerating replacement cycles for gasoline-powered systems across major cities. Contractors are increasingly deploying robotic mowing systems and AI-enabled fleet monitoring platforms that improve workforce productivity by approximately 18% and reduce servicing downtime. Manufacturers are expanding regional battery assembly operations and dealer distribution networks to strengthen delivery efficiency and inventory responsiveness. Commercial buyers continue prioritizing connected diagnostics, runtime efficiency, and low-maintenance systems, making North America a strategic investment center for battery-powered innovation and large-scale fleet modernization.

Europe represents nearly 28% of the global outdoor power equipment market and remains the leading region for electrified landscaping equipment adoption. Germany, France, and Nordic countries are driving demand through strict urban emission regulations, sustainability mandates, and low-noise municipal maintenance requirements. Battery-powered equipment adoption across professional landscaping operations surpassed 46% in 2025, significantly higher than several global markets. Compliance-driven procurement is forcing contractors and municipalities to replace fuel-powered fleets with cordless and robotic alternatives capable of reducing operational noise by more than 35%. Manufacturers are increasing investment in recyclable battery systems, compact electric equipment platforms, and regional servicing infrastructure to align with sustainability-focused purchasing behavior. Enterprise buyers increasingly prioritize compliance performance, operational efficiency, and carbon reduction capabilities, positioning Europe as a major innovation hub for advanced outdoor maintenance technologies and connected electrified equipment deployment.

Asia-Pacific accounts for nearly 24% of the global outdoor power equipment market and is emerging as the fastest-expanding regional hub for both production and equipment demand. China, Japan, and India are driving large-scale deployment through rapid urban landscaping expansion, infrastructure development, and localized manufacturing investments. Regional production capacity increased by approximately 22% between 2024 and 2026 as manufacturers shifted assembly operations closer to component suppliers and export channels. Cost-efficient manufacturing ecosystems and faster scalability are strengthening the region’s position within global supply chains, while battery-powered equipment adoption increased by nearly 27% due to expanding residential landscaping activity and municipal maintenance projects. Manufacturers are prioritizing Asia-Pacific for regional assembly expansion, supplier diversification, and high-volume equipment production to improve operational flexibility, reduce logistics dependency, and strengthen global delivery efficiency.

South America represents approximately 7% of the global outdoor power equipment market, with Brazil and Argentina leading regional demand through agricultural land maintenance, commercial gardening, and municipal landscaping operations. Landscaping and forestry-related equipment utilization increased by nearly 16% between 2024 and 2026 as urban green infrastructure projects expanded across metropolitan areas. However, high import dependency and currency volatility continue constraining large-scale equipment modernization across price-sensitive markets. Battery-powered equipment adoption remains below 30% due to infrastructure limitations and higher upfront ownership costs compared with conventional fuel-powered systems. Manufacturers are responding through localized dealer partnerships, compact product portfolios, and flexible financing strategies designed for regional affordability. South America presents strong long-term expansion potential, but operational scalability remains closely tied to cost optimization and localized supply stability.

The Middle East & Africa accounts for nearly 5% of global outdoor power equipment demand, supported by large-scale infrastructure development, commercial landscaping expansion, and municipal modernization programs. The UAE, Saudi Arabia, and South Africa are leading deployment across tourism infrastructure, smart city projects, and public green space maintenance operations. Government-backed infrastructure investments increased landscaping equipment procurement by approximately 18% between 2024 and 2026, while battery-powered maintenance system adoption expanded by nearly 14% across urban municipalities. Contractors are increasingly deploying compact electric equipment to reduce operational noise and improve maintenance efficiency within densely developed commercial zones. Manufacturers are strengthening regional distributor networks, municipal partnerships, and localized servicing capabilities to capture infrastructure-driven demand growth. The region is emerging as a strategic expansion market for companies targeting long-term urban development and smart infrastructure maintenance projects.

The outdoor power equipment market is highly competitive, with global leaders such as Deere & Company, Husqvarna, Toro, STIHL, and Honda competing against regional manufacturers and battery-focused equipment innovators. The top five players collectively account for nearly 52% of global market share, with competition increasingly centered on electrification speed, robotic integration, supply chain control, and connected fleet technologies. Premium manufacturers are differentiating through AI-enabled diagnostics, autonomous mowing systems, and high-capacity lithium-ion platforms that reduce maintenance requirements by nearly 27% and improve operational uptime by approximately 18%. At the same time, regional competitors are aggressively competing on pricing flexibility, localized servicing, and compact cordless product portfolios.

The competitive landscape is rapidly shifting toward battery ecosystem ownership and vertical integration. Leading companies are expanding battery assembly operations, forming robotics partnerships, and regionalizing production networks to reduce logistics exposure and improve inventory responsiveness. Rising investment requirements in battery infrastructure, software integration, and autonomous systems are increasing entry barriers for smaller manufacturers.

Long-term competitive success now depends on combining scalable electrification, connected fleet intelligence, and supply chain resilience into integrated outdoor maintenance ecosystems.

Deere & Company

Husqvarna Group

The Toro Company

STIHL Holding AG & Co. KG

Honda Motor Co., Ltd.

Ariens Company

Briggs & Stratton

Kubota Corporation

Makita Corporation

Stanley Black & Decker, Inc.

Techtronic Industries Co. Ltd.

Yamabiko Corporation

Greenworks Tools

Generac Holdings Inc.

Battery-powered outdoor equipment remains the dominant technology shift transforming the market, with cordless system adoption surpassing 48% across residential applications and expanding rapidly in commercial landscaping fleets. Advanced lithium-ion platforms reduce maintenance expenses by nearly 27% and lower operational noise by over 35% compared with legacy gasoline-powered equipment. Manufacturers are integrating fast-charging systems, thermal battery management, and swappable battery architectures to improve runtime consistency and fleet utilization. Companies with strong battery ecosystem control are gaining competitive advantage through lower servicing costs and faster product deployment cycles.

Autonomous mowing systems and AI-enabled fleet management platforms are emerging as high-impact operational technologies across municipal and commercial landscaping operations. Robotic mower deployment increased by approximately 22% between 2024 and 2026 as contractors prioritized labor optimization and predictive maintenance capabilities. AI-driven diagnostics reduce unexpected equipment downtime by nearly 17% while improving route efficiency by approximately 16%. Integration between robotics, fleet analytics, and connected maintenance software is reshaping equipment procurement decisions, particularly among large commercial contractors focused on operational scalability.

Between 2026 and 2028, vision-based navigation systems, IoT-connected diagnostics, and software-centric fleet platforms are expected to redefine outdoor maintenance operations. Compared with traditional manually operated systems, autonomous landscaping technologies improve workforce productivity by over 20% while reducing fuel dependency and servicing intervals. Manufacturers are accelerating investment in robotics partnerships, connected fleet ecosystems, and localized battery production to strengthen supply resilience, improve equipment intelligence, and secure long-term leadership within electrified outdoor maintenance infrastructure.

October 2024 – The Toro Company introduced autonomous mowing systems and connected fleet technologies at Equip Expo 2024, targeting commercial landscaping efficiency improvements exceeding 20% through AI-enabled maintenance optimization and battery-powered equipment integration. The launch strengthened Toro’s smart outdoor equipment positioning. [Autonomous Expansion] Source: Toro Newsroom

December 2024 – The Toro Company accelerated deployment of Haven robotic mowers and GeoLink autonomous fairway systems while advancing its AMP initiative targeting USD 100 million operational savings by 2027. The expansion reinforced competitive focus on robotic landscaping and AI-driven fleet productivity technologies. [Robotics Acceleration] Source: The Toro Company

July 2025 – Husqvarna reported an 8.6% increase in operating profit driven by strong robotic mower demand and operational efficiency improvements. The company intensified investment in connected robotic landscaping equipment, accelerating the industry shift toward automated outdoor maintenance systems. [Robotic Demand Surge] Source: Reuters

September 2023 / Spring 2024 rollout – Lowe’s and The Toro Company expanded nationwide retail distribution of battery-powered outdoor equipment and zero-turn mowers across U.S. stores, increasing consumer accessibility and accelerating cordless equipment penetration within residential landscaping applications. [Retail Distribution Shift] Source: Lowe’s Corporate

The Outdoor Power Equipment Market report provides comprehensive analysis across key product categories including lawn mowers, chainsaws, trimmers and edgers, blowers, and snow throwers, while evaluating major applications such as lawn care, landscaping, gardening, forestry, and snow removal. The study also assesses demand patterns across residential, commercial, municipal, and agriculture end-users. Regional coverage includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with strategic focus on manufacturing shifts, electrification trends, and evolving commercial landscaping requirements.

The report delivers detailed insight into battery-powered equipment adoption, robotic mowing deployment, connected fleet management systems, and AI-enabled diagnostics technologies shaping operational transformation between 2026 and 2033. Battery-powered equipment adoption exceeded 48% across residential users in 2025, while robotic mower deployment increased by nearly 22% across commercial landscaping operations. The study profiles major global manufacturers, evaluates supply chain regionalization trends, and tracks technology integration strategies influencing competitive positioning.

The report supports investment planning, production expansion, product portfolio optimization, and regional market entry decisions by identifying high-demand equipment categories, emerging operational technologies, and evolving procurement behavior across commercial and municipal maintenance ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 12210 Million |

|

Market Revenue in 2033 |

USD 19314.49 Million |

|

CAGR (2026 - 2033) |

5.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Deere & Company, Husqvarna Group, The Toro Company, STIHL Holding AG & Co. KG, Honda Motor Co., Ltd., Ariens Company, Briggs & Stratton, Kubota Corporation, Makita Corporation, Stanley Black & Decker, Inc., Techtronic Industries Co. Ltd., Yamabiko Corporation, Greenworks Tools, Generac Holdings Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |