Reports

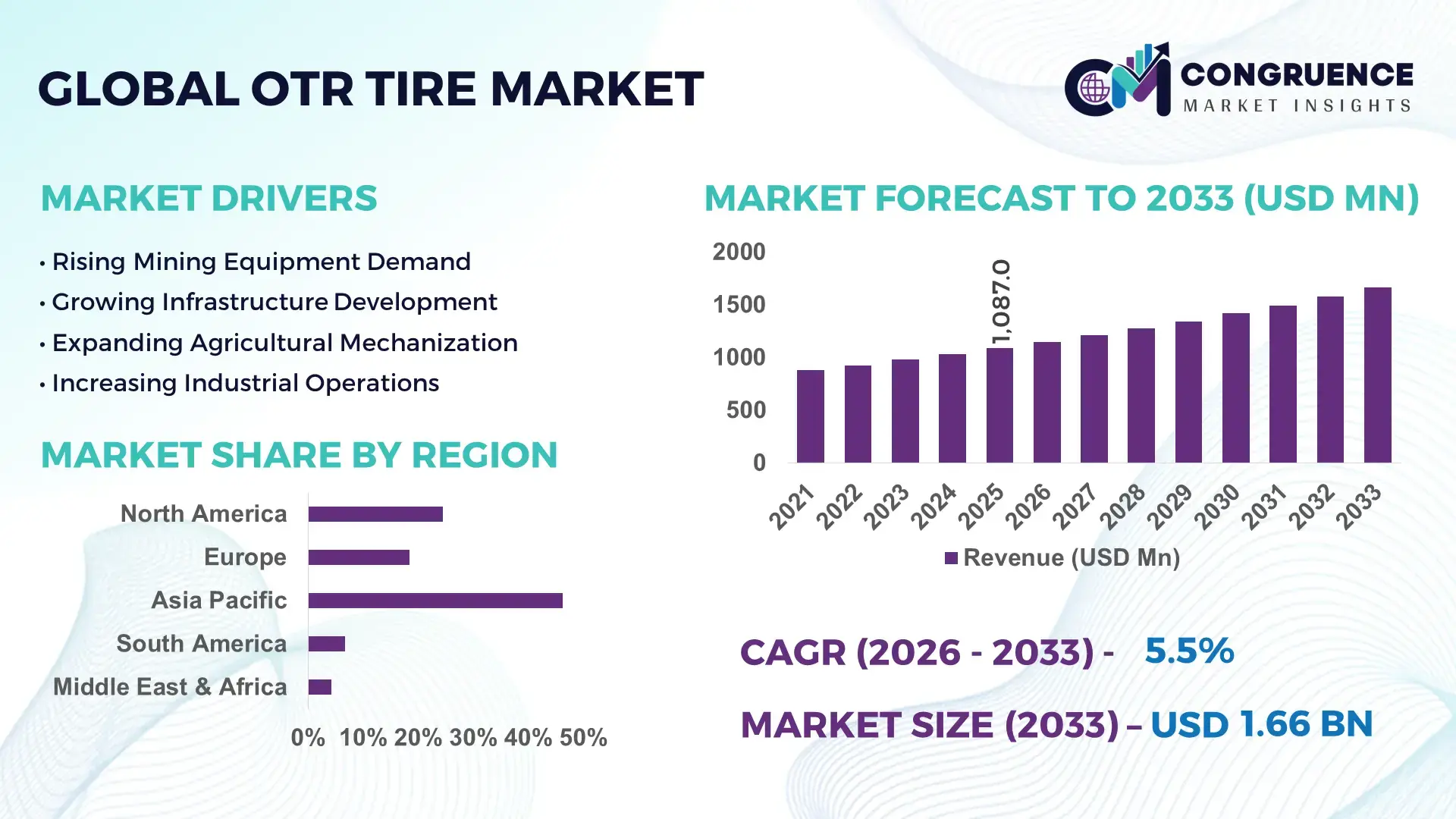

The Global OTR Tire Market was valued at USD 1,087.0 Million in 2025 and is anticipated to reach a value of USD 1,661.9 Million by 2033 expanding at a CAGR of 5.45% between 2026 and 2033. Growth is being accelerated by rising mining fleet utilization, large-scale infrastructure construction, and the integration of tire monitoring systems that reduce equipment downtime across heavy-duty operations.

China remains the dominant country in the global OTR tire landscape, accounting for approximately 32% of global OTR tire manufacturing capacity, supported by over 14,000 active mining sites and one of the world's largest construction equipment fleets. China’s output capacity exceeds India’s by nearly 2.5 times, while advanced tire monitoring adoption in large mining fleets has surpassed 35% compared with less than 20% in several emerging economies. Continued infrastructure spending under major industrial modernization programs further reinforces production leadership and aftermarket demand.

Strategically, companies are prioritizing high-capacity manufacturing, smart tire technologies, and mining-sector partnerships to secure long-term competitive advantage in heavy-equipment mobility ecosystems.

Market Size & Growth: USD 1,087.0 Million in 2025 reaching USD 1,661.9 Million by 2033 at 5.45%, supported by expanding mining activity and intelligent tire monitoring adoption.

Top Growth Drivers: Mining equipment utilization up 18%, infrastructure equipment deployment up 14%, and premium radial tire penetration up 12%.

Short-Term Forecast: By 2028, predictive tire monitoring is expected to reduce unplanned fleet downtime by nearly 20%.

Emerging Technologies: AI-driven tire analytics, sensor-enabled TPMS solutions, and advanced silica-based compounds are improving durability by 15–25%.

Regional Leaders: Asia-Pacific approaches USD 720 Million, North America exceeds USD 380 Million, and Europe nears USD 290 Million, driven by mining modernization and fleet digitization.

Consumer/End-User Trends: More than 42% of large mining operators now prioritize lifecycle cost optimization over upfront tire pricing.

Pilot/Case Example: In 2024, sensor-based fleet tire management deployments improved tire life by approximately 18% across selected mining operations.

Competitive Landscape: Top manufacturers control nearly 55% of market activity, led by Bridgestone, Michelin, Goodyear, Yokohama, and Continental.

Regulatory & ESG Impact: Tire retreading and recycling initiatives have lowered raw-material consumption by nearly 12% in industrial fleets.

Investment & Funding: Over USD 1.5 Billion has been directed toward manufacturing expansion, automation, and supply-chain localization initiatives.

Innovation & Future Outlook: Next-generation connected tires and autonomous equipment integration are reshaping high-performance off-road mobility strategies.

The OTR Tire Market serves critical demand from mining, quarrying, construction, agriculture, and industrial material-handling sectors where equipment uptime directly impacts productivity. Manufacturers are introducing sensor-integrated tires, advanced rubber compounds, and predictive maintenance platforms to improve lifecycle performance. Radial OTR tire penetration has exceeded 60% in several developed markets, while supply-chain diversification and localized manufacturing strategies are becoming increasingly important amid global raw-material sourcing adjustments, creating new opportunities for technology-led differentiation and operational resilience.

The OTR tire market has become strategically important as mining operators, infrastructure developers, and industrial fleet owners focus on maximizing equipment productivity while controlling operating costs. Large-scale infrastructure modernization programs, critical mineral extraction projects, and fleet digitalization initiatives are increasing the operational value of high-performance tire solutions. Simultaneously, supply-chain restructuring is encouraging manufacturers to expand regional production networks and reduce dependency on single-country sourcing models.

Technology is increasingly defining competitive positioning. Sensor-enabled OTR tires can improve maintenance planning accuracy by more than 25% compared with traditional manual inspection methods while reducing unexpected tire-related stoppages by nearly 20%. North America leads in digital fleet management adoption, whereas China maintains a significant advantage in manufacturing scale and production efficiency. Mining operators are increasingly integrating tire analytics platforms with fleet management systems to optimize asset utilization and extend service intervals.

Over the next two to three years, connected tire deployments are expected to expand across large mining and construction fleets as companies prioritize operational visibility and lifecycle optimization. Manufacturers are strengthening partnerships with equipment OEMs, investing in advanced materials, and expanding localized production capabilities. Organizations that combine digital tire intelligence, manufacturing scale, and aftermarket service excellence will secure stronger competitive positioning and long-term operational advantage.

Mining activity and heavy-equipment utilization remain the strongest growth catalysts for OTR tires. Global demand for critical minerals has increased by more than 20% over recent years, driving higher deployment of haul trucks, loaders, and earthmoving equipment. Radial OTR tire adoption has surpassed 60% in major mining operations due to its 15–20% longer service life and improved fuel efficiency. China and Australia continue expanding mining output, while India’s infrastructure equipment base has grown by more than 10%. The result is higher replacement cycles and stronger demand for premium-performance tires. Manufacturers are responding through capacity expansion, sensor-integrated products, and strategic OEM partnerships. A key industry shift is the integration of predictive tire monitoring, which transforms tires from consumables into data-generating operational assets that directly influence equipment productivity.

Natural rubber, synthetic rubber, and carbon black remain highly exposed to commodity price fluctuations, creating significant cost instability for OTR tire manufacturers. Raw materials typically represent 45–55% of tire production costs, while logistics expenses in some industrial corridors have risen by nearly 15% since recent global supply-chain disruptions. Southeast Asian rubber supply concentration increases procurement risk for global producers. These pressures affect pricing consistency, fleet procurement planning, and manufacturer margins. Companies are mitigating exposure through long-term sourcing agreements, regionalized production networks, and alternative material development programs. An important strategic insight is that procurement resilience is becoming nearly as important as manufacturing efficiency, particularly for suppliers serving large mining and infrastructure customers with strict equipment uptime requirements.

The emergence of connected tire ecosystems creates substantial value beyond traditional tire sales. Smart tire monitoring systems can reduce maintenance-related downtime by approximately 20% and improve tire utilization by 15–18%. Large mining operators are increasingly adopting AI-driven analytics platforms that combine pressure, temperature, and wear data for real-time fleet optimization. China and India are investing heavily in digital mining and industrial automation programs, creating fertile conditions for intelligent tire solutions. Manufacturers are expanding R&D efforts, partnering with telematics providers, and developing subscription-based fleet performance services. A less obvious opportunity lies in transforming aftermarket support into recurring digital revenue streams, allowing suppliers to strengthen customer retention while improving operational outcomes for fleet operators.

Deploying advanced tire technologies consistently across global fleets remains a complex challenge. More than 30% of industrial operators continue to rely on fragmented maintenance processes, limiting the effectiveness of predictive tire management systems. Integration between telematics platforms, fleet management software, and tire monitoring infrastructure often requires substantial investment and workforce training. Large mining sites in Australia and Canada are progressing rapidly, while smaller operators face implementation constraints. The challenge extends beyond hardware deployment to data management, analytics integration, and operational standardization. Manufacturers must invest in interoperable platforms, technician training programs, and strategic ecosystem partnerships. Companies that successfully simplify deployment complexity and improve data usability will gain a durable competitive advantage as intelligent fleet management becomes an industry standard.

Smart Tire Intelligence Expansion Connected tire monitoring is moving from pilot projects to fleet-wide deployment, with adoption among large mining operators exceeding 35% and predictive maintenance accuracy improving by nearly 25%. Tire pressure monitoring systems are reducing unexpected equipment stoppages by 15–20%, particularly in Australia’s mining sector. Companies are integrating sensor data with fleet management platforms and expanding partnerships with telematics providers to improve asset visibility and operational planning while addressing labor shortages in maintenance-intensive environments.

Localized Manufacturing Footprint Shift Supply-chain disruptions and geopolitical sourcing concerns have accelerated regional manufacturing strategies. More than 40% of major tire producers have expanded localized production or sourcing programs since recent logistics disruptions, while lead times for industrial tire deliveries have improved by approximately 18%. India and China continue attracting manufacturing investments as companies restructure procurement networks. This shift is improving inventory resilience and reducing transportation-related operational costs across mining and construction equipment supply chains.

Premium Radial Tire Migration Radial OTR tire penetration now exceeds 60% in several developed industrial markets, with premium variants delivering 15–20% longer service life than conventional alternatives. Fleet operators are prioritizing total lifecycle performance over initial acquisition costs as equipment utilization rates increase. Manufacturers are expanding advanced compound portfolios and strengthening OEM relationships, while mining enterprises increasingly standardize premium tire specifications across large fleets to improve maintenance consistency and operational efficiency.

Circular Economy and Retreading Adoption Sustainability objectives and resource efficiency targets are increasing demand for retreaded and recyclable OTR tire solutions. Retreading programs can lower tire lifecycle costs by 25–35% while reducing raw-material consumption by nearly 12%. Mining and industrial operators are implementing structured tire recovery programs in response to environmental compliance requirements and waste reduction goals. Manufacturers are investing in advanced retreading facilities, material recovery technologies, and closed-loop service models that strengthen customer retention while supporting operational sustainability targets.

Radial tires represent the leading segment within the OTR tire market, accounting for approximately 62% of total deployment due to superior durability, heat dissipation, and fuel-efficiency performance. Mining and construction operators increasingly favor radial configurations because they provide 15–20% longer service life and improved traction under heavy-load conditions. Their ability to support higher operating speeds and reduce maintenance frequency has made them the preferred choice for large fleets in China, Australia, and North America. Manufacturers continue prioritizing radial product innovation through advanced tread compounds, sensor integration, and OEM-focused partnerships. Bias tires remain strategically relevant in demanding applications where cut resistance, lower acquisition costs, and rugged operating environments are priorities. However, advanced radial tires represent the fastest-growing segment as fleet owners focus on lifecycle optimization and predictive maintenance integration. Adoption of smart radial tire systems has increased by more than 25% among large industrial operators. Companies are expanding premium product portfolios and investing in intelligent tire technologies to capture higher-value contracts. This transition reflects a broader industry movement toward performance-driven procurement and digital fleet management strategies.

Mining remains the dominant application segment, representing nearly 38% of OTR tire deployment due to the intensive utilization of haul trucks, loaders, and heavy earthmoving equipment. High equipment operating hours, harsh terrain conditions, and continuous replacement requirements sustain strong demand concentration. Mining operators increasingly deploy sensor-enabled tire monitoring systems, with adoption rates exceeding 35% among large sites. Tire manufacturers are responding through specialized mining tire portfolios, predictive maintenance capabilities, and long-term fleet service agreements. Construction is emerging as the fastest-growing application as infrastructure modernization programs accelerate equipment deployment across India, the United States, and Southeast Asia. Construction-related tire demand has expanded by approximately 12% through increased use of excavators, graders, and wheel loaders. Agriculture continues to maintain stable demand supported by mechanization trends, while industrial and port-handling applications are adopting advanced tire management solutions to reduce downtime. Companies are scaling production capacity, strengthening OEM integration, and expanding aftermarket support networks to address evolving operational requirements across diverse equipment categories.

Mining companies constitute the largest end-user group, accounting for approximately 40% of total OTR tire consumption due to extensive fleet deployment, continuous equipment utilization, and stringent productivity requirements. Large mining operators prioritize lifecycle performance, predictive maintenance, and operational uptime, leading to accelerated adoption of intelligent tire systems. More than 35% of major mining fleets now incorporate digital tire monitoring into broader fleet management frameworks. Manufacturers are targeting this segment through premium product offerings, dedicated service agreements, and integrated data analytics capabilities. Construction contractors represent the fastest-growing end-user category as infrastructure investments increase demand for earthmoving and material-handling equipment. Construction fleet expansion has exceeded 10% across several developing economies, creating sustained replacement demand. Agricultural enterprises continue adopting specialized OTR tire solutions to support mechanization, while industrial operators increasingly focus on reducing maintenance-related disruptions. Companies are tailoring product portfolios, strengthening distribution partnerships, and developing application-specific tire designs to address the operational priorities of each customer group. Future competitive positioning will increasingly depend on delivering both tire performance and fleet intelligence capabilities.

Asia-Pacific accounted for the largest market share at 46.2% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2026 and 2033.

North America represents approximately 24.5% of global OTR tire demand, supported by extensive mining, construction, and industrial equipment deployment. The region continues to lead in predictive maintenance integration, with connected tire monitoring adoption exceeding 40% among large mining operators. Equipment modernization initiatives across the United States and Canada are driving demand for premium radial OTR tires capable of supporting high-utilization fleets. Fleet operators increasingly prioritize lifecycle cost management, prompting greater deployment of sensor-enabled tire technologies. A notable market shift includes expanded partnerships between tire manufacturers and telematics providers, improving maintenance planning accuracy and reducing unplanned downtime across heavy-equipment operations.

United States Market Outlook: The United States remains the largest contributor to regional demand due to its extensive construction sector, quarrying operations, and critical mineral development projects. More than 30% of North America's heavy construction equipment fleet operates within the country, creating substantial replacement tire demand. Infrastructure modernization initiatives and advanced fleet management adoption continue strengthening market activity. Manufacturers are expanding distribution networks, investing in intelligent tire solutions, and increasing collaboration with OEMs to improve operational efficiency across mining and construction fleets.

Europe accounts for nearly 18.4% of global market activity, supported by advanced industrial operations and strong emphasis on sustainable equipment management. Tire retreading, circular economy initiatives, and environmental compliance requirements are influencing procurement strategies across mining and construction sectors. Premium radial tires account for more than 65% of industrial fleet deployments in several European countries due to their efficiency and durability advantages. Companies are increasingly investing in recyclable materials, lower-emission manufacturing processes, and digital tire management systems. Industrial operators are also adopting structured tire lifecycle programs to improve resource utilization while maintaining equipment productivity.

Germany Market Outlook: Germany serves as the region’s strategic center for advanced tire engineering, industrial equipment manufacturing, and automation-driven fleet management. The country hosts a significant concentration of construction machinery and industrial vehicle producers, supporting continuous demand for high-performance OTR tires. Advanced maintenance systems have achieved deployment rates exceeding 35% among large industrial operators. German enterprises continue strengthening smart manufacturing capabilities and sustainability-focused tire management programs, reinforcing long-term market competitiveness and technological leadership.

Asia-Pacific holds the largest market position with approximately 46.2% share, supported by extensive mining activity, large-scale infrastructure development, and dominant tire manufacturing capacity. The region accounts for more than 55% of global OTR tire production, benefiting from integrated supply chains and cost-efficient manufacturing ecosystems. Rapid deployment of construction equipment across India, China, and Southeast Asia continues strengthening replacement demand. Tire manufacturers are expanding production capacity, increasing automation investments, and developing advanced product portfolios to support high-volume industrial requirements. Infrastructure development programs and mining sector expansion remain critical operational demand drivers.

China Market Outlook: China represents the most influential country market due to its substantial manufacturing footprint, extensive mining operations, and large construction equipment base. The country contributes approximately 32% of global OTR tire manufacturing capacity and maintains one of the world's largest heavy-equipment fleets. Adoption of intelligent tire monitoring systems continues increasing among major mining enterprises. Domestic manufacturers are expanding export capabilities, investing in advanced production technologies, and strengthening OEM relationships to maintain leadership across global industrial tire supply networks.

South America contributes approximately 6.7% of global market demand, driven primarily by mining operations, agricultural mechanization, and commodity-export industries. Copper, lithium, and iron ore production activities continue increasing utilization rates for haul trucks, loaders, and support vehicles. Large mining projects have expanded demand for premium OTR tire solutions capable of operating under extreme terrain conditions. However, infrastructure bottlenecks and logistics inefficiencies continue affecting procurement cycles and inventory management. Manufacturers are responding through localized distribution strategies and stronger aftermarket support capabilities to improve service responsiveness across remote operating environments.

Brazil Market Outlook: Brazil remains the region’s most significant market due to its large mining sector, agricultural machinery deployment, and industrial equipment utilization. The country accounts for a substantial share of South American construction and mining equipment activity, creating consistent replacement demand. Expanding agricultural mechanization and infrastructure projects continue supporting tire consumption. Industry participants are strengthening dealer networks, improving inventory availability, and introducing application-specific tire solutions designed for diverse operating conditions across mining, farming, and construction sectors.

Middle East & Africa represents approximately 4.2% of global market activity but demonstrates the strongest expansion potential due to large-scale mining investments, infrastructure modernization, and industrial diversification programs. Mining fleet deployments across Africa continue increasing, while Gulf economies are investing heavily in construction, logistics, and industrial development projects. Several large infrastructure initiatives have increased heavy-equipment utilization by more than 12% in selected markets. Tire suppliers are expanding regional service capabilities, strengthening distribution partnerships, and enhancing technical support operations to capitalize on rising equipment deployment across resource-intensive industries.

Saudi Arabia Market Outlook: Saudi Arabia serves as the region’s leading growth engine through extensive infrastructure development, industrial diversification initiatives, and large-scale construction activity. Major economic transformation projects continue increasing demand for earthmoving equipment, loaders, and heavy-duty transport fleets. Industrial and logistics investments have accelerated deployment of advanced fleet management systems across key sectors. Manufacturers are expanding regional partnerships, improving service coverage, and positioning premium OTR tire solutions to support the country's evolving infrastructure and industrial modernization objectives.

The OTR tire market is led by global manufacturers such as Bridgestone Corporation, Michelin, The Goodyear Tire & Rubber Company, Yokohama Rubber Co., Ltd., and Continental AG, competing against regional manufacturers in China and India that emphasize cost efficiency and localized supply. The top five players collectively control approximately 55–60% of global market activity, creating a moderately consolidated structure. Competition is increasingly driven by technology, durability, fleet uptime, and service integration rather than price alone. Premium tire solutions can improve service life by 15–20%, while predictive monitoring platforms reduce maintenance-related downtime by nearly 20%. Leading companies are expanding production capacity, acquiring specialized OTR businesses, strengthening OEM relationships, and integrating digital fleet management capabilities. The competitive shift is moving toward connected tire ecosystems and supply-chain control. High capital requirements, advanced engineering expertise, and established aftermarket networks remain major entry barriers. Winning requires superior lifecycle performance, digital service capability, manufacturing scale, and reliable global distribution.

Michelin

Goodyear Tire & Rubber Company

Continental AG

Yokohama Rubber Co., Ltd.

Hankook Tire & Technology

Sumitomo Rubber Industries Ltd.

Trelleborg Wheel Systems

Nokian Tyres Plc

Apollo Tyres Ltd.

CEAT Limited

BKT (Balkrishna Industries Limited)

Titan International Inc.

Triangle Tyre Co., Ltd.

Digital intelligence is becoming the defining technology layer within the OTR tire industry. Connected tire monitoring systems capable of tracking pressure, temperature, and tread performance are now deployed across more than 35% of large mining fleets. These platforms reduce unplanned downtime by approximately 20% while improving maintenance planning accuracy by over 25%. Companies operating high-value equipment benefit from improved asset utilization and lower operational disruptions. Integration between tire sensors, telematics platforms, and fleet management software is becoming a standard procurement requirement for premium fleet operators.

Advanced materials technology is also reshaping tire performance. New-generation compound formulations and reinforced carcass architectures deliver 15–20% longer operational life than conventional designs while improving resistance to cuts and heat buildup. Compared with legacy bias tire technologies, advanced radial solutions improve fuel efficiency by nearly 10% and support higher load capacity. Premium manufacturers are leveraging these innovations to strengthen long-term contracts with mining and construction customers seeking measurable lifecycle advantages.

Between 2026 and 2028, AI-enabled predictive analytics, automated tire diagnostics, and integrated fleet optimization platforms will gain wider adoption. Companies investing early in connected tire ecosystems, smart maintenance infrastructure, and advanced materials development will secure stronger operational differentiation, faster service responsiveness, and higher-value customer relationships as digital fleet management becomes increasingly central to industrial equipment performance.

March 2025 – Bridgestone introduced the MASTERCORE 27.00R49 VRDU aggregate tire, extending its mining-grade technology into aggregate applications. The new design delivers enhanced load capacity and longer tire life for heavy-duty operations, improving equipment productivity and lowering replacement frequency. Source: www.bridgestoneamericas.com

February 2025 – Yokohama Rubber completed the acquisition of Goodyear’s OTR tire business, adding specialized mining and construction tire technologies spanning 25-inch to 63-inch product ranges. The transaction significantly strengthens Yokohama’s production and supply capabilities in the global off-highway tire sector.

May 2025 – Yokohama Rubber acquired a Romanian OTR tire production facility with approximately 200,000 square meters of land area and mining tire manufacturing equipment. The expansion increases European production capacity and improves supply-chain responsiveness for mining and construction customers.

August 2024 – Continental AG launched automated tread-depth measurement through its next-generation tire sensor platform, enabling daily wear monitoring and AI-based maintenance planning. The solution improves service predictability and supports more efficient fleet operations through continuous digital tire assessment.

The report provides comprehensive analysis of the global OTR tire industry across major tire types, applications, end-user categories, and regional markets. It evaluates demand patterns across mining, construction, agriculture, industrial handling, and infrastructure-related operations while examining deployment trends influencing equipment productivity and fleet performance. The assessment covers leading manufacturers, technology adoption rates, distribution strategies, production ecosystems, and emerging market opportunities. More than 60% of industrial fleet deployments are now concentrated in advanced radial tire solutions, reflecting a significant shift in operational priorities.

The study further examines regional manufacturing dynamics, intelligent tire monitoring adoption, advanced material innovations, and digital fleet management integration. Coverage extends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, including country-level competitive developments and investment activity. Strategic insights support expansion planning, procurement optimization, partnership evaluation, competitive benchmarking, and technology investment decisions. Particular emphasis is placed on connected tire ecosystems, predictive maintenance capabilities, supply-chain resilience, and evolving industrial equipment requirements expected to shape market direction between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,087.0 Million |

| Market Revenue (2033) | USD 1,661.9 Million |

| CAGR (2026–2033) | 5.45% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Bridgestone Corporation; Michelin; Goodyear Tire & Rubber Company; Continental AG; Yokohama Rubber Co., Ltd.; Hankook Tire & Technology; Sumitomo Rubber Industries Ltd.; Trelleborg Wheel Systems; Nokian Tyres Plc; Apollo Tyres Ltd.; CEAT Limited; BKT (Balkrishna Industries Limited); Titan International Inc.; Triangle Tyre Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |