Reports

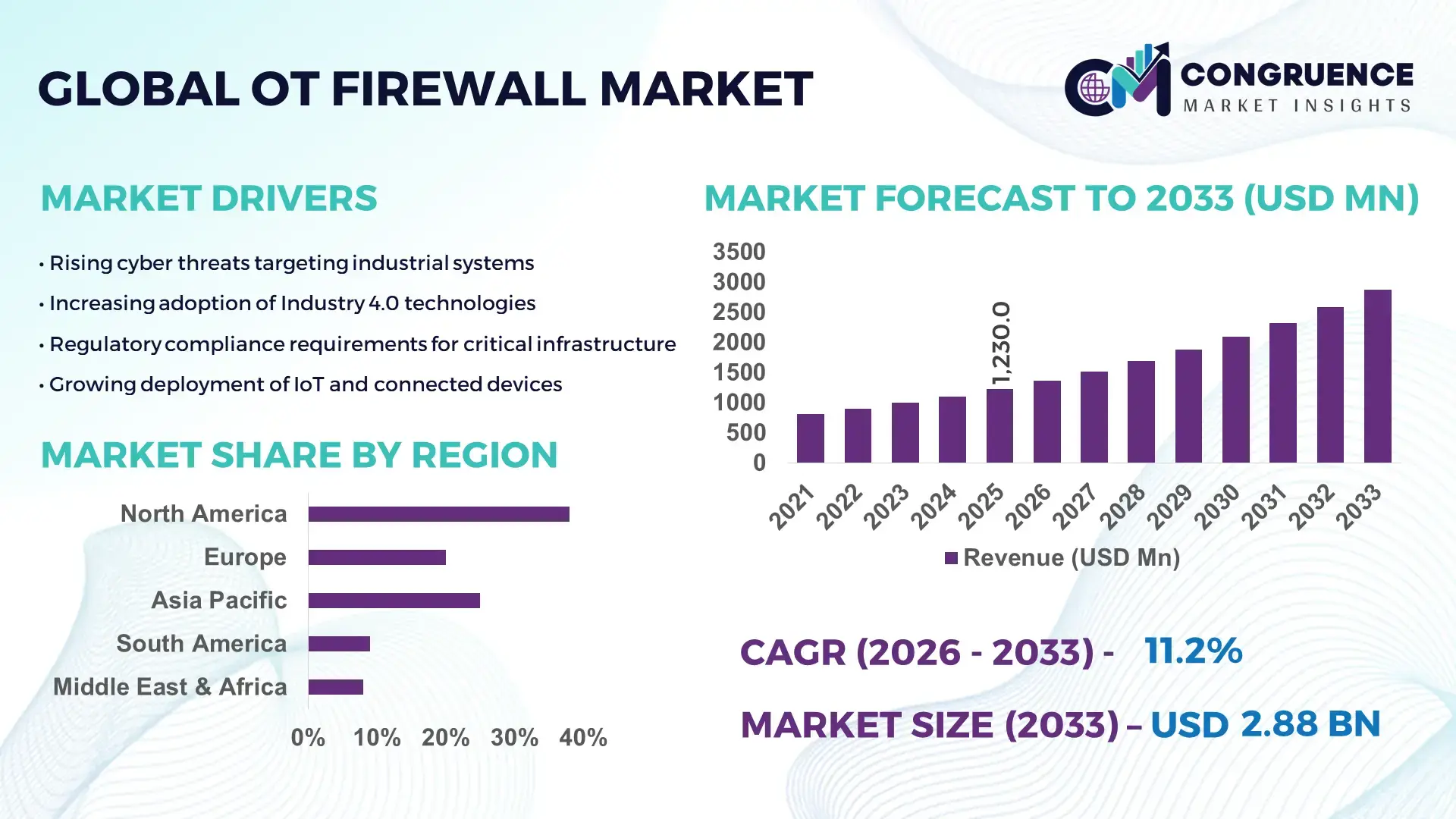

The Global OT Firewall Market was valued at USD 1230 Million in 2025 and is anticipated to reach a value of USD 2875.69 Million by 2033 expanding at a CAGR of 11.2% between 2026 and 2033. Growth is primarily driven by accelerating industrial digitalization and rising cybersecurity mandates across critical infrastructure sectors.

The United States leads the OT firewall landscape with more than 3,500 large-scale industrial cybersecurity deployments across energy, utilities, oil & gas, and manufacturing facilities. Annual investments in industrial control system (ICS) security exceed USD 2.5 billion, with federal funding programs supporting grid modernization and smart manufacturing upgrades. Over 65% of major power generation plants in the country have integrated next-generation OT firewall solutions featuring deep packet inspection for Modbus, DNP3, and OPC protocols. Advanced semiconductor fabs and LNG terminals increasingly deploy AI-enabled industrial firewalls to protect automated process control networks, reinforcing nationwide operational resilience across mission-critical environments.

Market Size & Growth: USD 1230 Million in 2025, projected to reach USD 2875.69 Million by 2033 at an 11.2% CAGR, fueled by rising cyberattacks on critical infrastructure and increased compliance-driven OT security investments.

Top Growth Drivers: Industrial IoT adoption 48%, ransomware incident increase 38%, regulatory compliance enforcement 41%.

Short-Term Forecast: By 2028, predictive OT firewall monitoring is expected to reduce industrial downtime by 22% and cybersecurity response time by 30%.

Emerging Technologies: AI-driven threat intelligence, zero-trust architecture for industrial networks, and cloud-managed OT firewall orchestration platforms.

Regional Leaders: North America projected at USD 1,050 Million by 2033 with high utility-sector adoption; Europe reaching USD 820 Million driven by NIS2 compliance; Asia-Pacific at USD 710 Million supported by smart factory expansion.

Consumer/End-User Trends: Energy & utilities account for over 35% of deployments, followed by manufacturing and oil & gas, with increased demand for protocol-aware next-generation firewalls.

Pilot or Case Example: A 2024 smart grid modernization project reduced network intrusion incidents by 27% after deploying advanced OT firewall segmentation.

Competitive Landscape: Fortinet holds approximately 18% share, followed by Palo Alto Networks, Cisco Systems, Check Point Software Technologies, and Siemens.

Regulatory & ESG Impact: Stricter cybersecurity frameworks and industrial safety compliance standards are accelerating firewall upgrades across critical infrastructure.

Investment & Funding Patterns: Over USD 1.8 billion invested globally in industrial cybersecurity initiatives between 2023 and 2025, with increased venture capital targeting OT-specific security startups.

Innovation & Future Outlook: Integration of AI-powered anomaly detection, unified IT-OT security management platforms, and edge-based firewall solutions will shape next-generation industrial cybersecurity strategies.

The OT firewall market serves energy & utilities (35%), manufacturing (28%), oil & gas (16%), transportation, and water treatment sectors, reflecting widespread adoption across operational technology environments. Recent innovations include ruggedized hardware firewalls for harsh industrial conditions, protocol-aware deep packet inspection engines, and centralized cloud-based management dashboards. Regulatory frameworks mandating cybersecurity audits and infrastructure resilience are strengthening procurement cycles, while economic pressures are driving demand for scalable, cost-efficient OT security architectures. Asia-Pacific is witnessing rapid consumption growth due to smart factory investments, whereas Europe focuses on compliance-driven modernization. Future expansion is expected through convergence of IT-OT security ecosystems, AI-based real-time threat analytics, and advanced segmentation models enabling secure industrial automation at scale.

The OT Firewall Market holds strategic relevance as industrial enterprises accelerate digital transformation across energy grids, smart factories, transportation systems, and water utilities. As more than 70% of industrial sites globally integrate Industrial IoT sensors and connected control systems, safeguarding operational technology networks has become a board-level priority. Modern protocol-aware next-generation firewalls deliver 45% faster threat detection compared to traditional perimeter-based legacy firewalls, enabling real-time inspection of Modbus, DNP3, and IEC 61850 traffic. This measurable improvement strengthens operational continuity while reducing exposure to ransomware and supply chain attacks.

Asia-Pacific dominates in deployment volume due to rapid smart manufacturing expansion, while Europe leads in adoption intensity with over 60% of large enterprises implementing advanced network segmentation aligned with critical infrastructure directives. By 2028, AI-driven anomaly detection within OT firewall platforms is expected to cut mean time to respond (MTTR) to industrial cyber incidents by 35%, improving uptime and production efficiency.

Firms are committing to ESG-aligned cybersecurity modernization, targeting 25% energy consumption reduction in network hardware by 2030 through energy-efficient firewall appliances and virtualized deployments. In 2024, a national grid operator in Germany achieved a 28% reduction in network intrusion attempts after implementing zero-trust OT firewall segmentation integrated with AI threat analytics.

As digital industrial ecosystems expand, the OT Firewall Market will remain a cornerstone of cyber resilience, regulatory compliance, and sustainable infrastructure growth, reinforcing secure automation and mission-critical reliability worldwide.

Industrial IoT adoption has expanded significantly, with connected industrial devices projected to exceed 30 billion globally within the next few years. Energy plants, smart grids, and automated manufacturing facilities increasingly rely on real-time data exchange between programmable logic controllers and cloud platforms. This connectivity increases attack surfaces, compelling operators to deploy protocol-aware OT firewall solutions. Studies indicate that ransomware attacks on industrial environments have risen by over 40% year-on-year, directly influencing cybersecurity budgets. Furthermore, more than 65% of large utilities have adopted network segmentation strategies to isolate operational assets from corporate IT networks. Advanced OT firewall platforms equipped with intrusion prevention and application-layer filtering ensure uninterrupted operations while safeguarding production lines, substations, and distribution networks from targeted cyber threats.

A substantial portion of industrial facilities continue to operate legacy control systems that were not designed with cybersecurity compatibility in mind. Nearly 50% of operational technology assets in mature manufacturing economies are over 15 years old, lacking native support for modern encryption protocols. Integrating advanced OT firewall appliances into these environments often requires system downtime, specialized configuration expertise, and customized firmware adjustments. Budget constraints within small and mid-sized industrial enterprises further slow modernization efforts. Additionally, interoperability challenges between multi-vendor industrial equipment and contemporary security platforms increase deployment timelines. These integration complexities and capital-intensive upgrades can delay full-scale OT firewall adoption despite growing cybersecurity awareness.

Global smart grid investments are exceeding USD 300 billion in cumulative funding, driving widespread deployment of intelligent substations and distributed energy management systems. Industry 4.0 programs across Asia and Europe are modernizing production environments with robotics, AI-driven analytics, and edge computing platforms. These initiatives create demand for scalable, cloud-managed OT firewall solutions capable of securing distributed assets and remote operations. More than 55% of industrial enterprises are piloting zero-trust architectures to enhance network visibility and threat containment. Edge-based firewall deployments within automated plants provide secure micro-segmentation, enabling safe machine-to-machine communication. As digital twins and predictive maintenance systems gain traction, the OT Firewall Market is positioned to capitalize on advanced industrial cybersecurity transformation initiatives worldwide.

The global cybersecurity workforce gap exceeds 3 million professionals, creating operational bottlenecks in deploying and managing complex OT firewall infrastructures. Industrial environments require specialized expertise in ICS protocols and safety-critical systems, skills that remain scarce. Simultaneously, compliance requirements across regions demand regular security audits, vulnerability assessments, and incident reporting, increasing operational workloads. Industrial operators must balance cybersecurity enhancements with uninterrupted production cycles, limiting flexibility for large-scale system upgrades. Moreover, evolving regulatory standards necessitate continuous firmware updates and policy refinements within firewall platforms. These workforce and compliance pressures can slow implementation timelines and elevate operational costs, posing measurable challenges to sustained OT firewall expansion.

AI-Driven Threat Detection Enhances Incident Response by 35%

The integration of artificial intelligence into OT firewall platforms is significantly improving industrial cybersecurity performance. Over 62% of large-scale manufacturing plants have deployed AI-enabled anomaly detection within their operational networks. These systems reduce false positives by nearly 40% and improve mean time to respond (MTTR) by 35%. Automated behavioral analytics allows real-time inspection of industrial protocols such as Modbus and DNP3, strengthening protection against ransomware attacks that have increased by over 38% in industrial environments.

Zero-Trust Network Segmentation Adopted by 58% of Critical Infrastructure Operators

Zero-trust architecture is becoming a foundational security model within the OT firewall market. Approximately 58% of energy and utilities operators have implemented micro-segmentation strategies to isolate control systems from enterprise IT networks. This approach has demonstrated a 30% reduction in lateral threat movement within industrial control systems. Advanced segmentation gateways and next-generation industrial firewalls are being deployed to enforce strict access control policies across distributed operational environments, particularly in North America and Europe.

Cloud-Managed OT Firewall Platforms Increase Operational Visibility by 45%

Cloud-integrated firewall management systems are transforming how enterprises monitor industrial assets. Around 47% of multinational industrial firms have centralized OT firewall monitoring across multiple production sites. This shift enhances cross-site threat intelligence sharing and improves network visibility by 45%. Secure remote access capabilities embedded within modern firewall appliances also reduce maintenance travel costs by 20%, enabling efficient management of geographically dispersed substations, oil terminals, and smart factories.

Edge-Based Firewall Deployments Expand by 50% in Smart Manufacturing Facilities

The expansion of Industry 4.0 initiatives has driven a 50% increase in edge-based OT firewall installations within automated plants. Industrial enterprises deploying edge firewalls report a 28% improvement in network performance due to localized traffic inspection and reduced latency. Ruggedized firewall appliances designed for extreme temperature and vibration conditions are increasingly integrated into robotics cells and programmable logic controller (PLC) environments, ensuring uninterrupted secure machine-to-machine communication across high-speed production lines.

The OT Firewall market segmentation reflects differentiated demand across deployment architectures, industrial use cases, and end-user verticals. By type, hardware-based industrial firewalls continue to dominate due to ruggedized performance in harsh operational environments, while virtualized and cloud-managed firewalls are expanding rapidly as IT-OT convergence accelerates. Application-wise, network segmentation and intrusion prevention represent the most widely implemented use cases, particularly in energy and utilities where system uptime is critical. Secure remote access and centralized monitoring platforms are gaining traction as distributed industrial assets increase. From an end-user perspective, energy & utilities, manufacturing, oil & gas, transportation, and water treatment facilities represent the core demand clusters. Over 70% of large industrial enterprises now prioritize dedicated OT security budgets, reflecting growing awareness of operational risk exposure and regulatory compliance mandates. This segmentation landscape underscores a shift from perimeter-only defense models to layered, protocol-aware industrial cybersecurity frameworks tailored to sector-specific operational requirements.

Hardware-based OT firewalls account for approximately 52% of total deployments, primarily due to their reliability in high-temperature, vibration-intensive industrial settings. These appliances offer deterministic performance, deep packet inspection for industrial protocols, and physical network segmentation, making them the preferred choice in substations, refineries, and manufacturing plants. Virtualized OT firewalls hold nearly 28% adoption, particularly among enterprises modernizing data centers and integrating cloud-managed orchestration tools. However, cloud-managed and software-defined OT firewalls represent the fastest-growing segment, expanding at an estimated 14.8% CAGR, driven by centralized visibility and scalable remote configuration capabilities.

While hardware appliances dominate current installations, adoption in software-defined OT firewall solutions is rising rapidly, expected to surpass 35% of new deployments by 2033 as industrial operators seek flexible and cost-efficient models. Other niche types, including embedded firewall modules within PLC systems and edge-integrated firewalls, collectively account for about 20% of deployments, serving specialized automation environments.

Network segmentation and intrusion prevention collectively represent around 46% of OT firewall applications, as industrial operators prioritize isolating critical control assets from enterprise IT networks. Secure remote access accounts for roughly 24% of implementations, reflecting increased remote workforce access to distributed operational facilities. However, centralized monitoring and threat analytics applications are expanding fastest, advancing at an estimated 15.3% CAGR due to AI-driven anomaly detection and predictive threat intelligence integration.

While segmentation remains foundational, analytics-driven OT firewall applications are projected to exceed 30% of total use cases by 2033 as real-time threat visualization becomes essential for operational continuity. Additional applications, including compliance auditing, industrial protocol filtering, and data loss prevention, together contribute approximately 30% of demand, serving regulatory-driven environments in Europe and North America.

Energy & utilities lead the OT firewall market with approximately 35% of total adoption, reflecting extensive smart grid modernization and heightened regulatory oversight. Manufacturing follows at nearly 29%, driven by Industry 4.0 automation and robotics integration. However, the transportation and logistics sector is the fastest-growing end-user group, expanding at an estimated 13.9% CAGR as rail networks, ports, and airports digitize operational control systems.

While utilities dominate in installed base, transportation-related deployments are projected to exceed 20% of total new installations by 2033, supported by increasing adoption of intelligent traffic systems and automated signaling infrastructure. Oil & gas and water treatment facilities collectively represent about 24% of the remaining demand, focusing on secure SCADA communication and remote asset monitoring.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12% between 2026 and 2033.

North America’s dominance is underpinned by over 3,800 large industrial sites integrating OT firewall solutions, covering energy, utilities, manufacturing, and transportation sectors. Asia-Pacific, led by China, India, and Japan, is witnessing rapid adoption with more than 1,200 smart factories deploying protocol-aware firewalls by 2025. Europe follows closely with 28% adoption, driven by regulatory mandates and digitalization programs. Latin America and the Middle East & Africa combined represent 14% of deployments, primarily focused on oil, gas, and water treatment infrastructure modernization. North America maintains high per-facility investment, averaging USD 650,000 per site, while Asia-Pacific is emphasizing cost-efficient cloud-managed OT firewall platforms and edge-based segmentation solutions. These regional dynamics highlight adoption disparities, investment priorities, and technological preferences that shape global OT firewall deployment trends.

How are enterprises enhancing industrial cybersecurity in critical infrastructure?

North America holds 38% of the global OT firewall market, led by large-scale adoption in energy, utilities, and manufacturing. Regulatory frameworks such as NERC CIP and federal cybersecurity incentives are driving proactive firewall deployments. Over 65% of utility operators have implemented next-generation firewalls with deep packet inspection and AI-driven anomaly detection. Technological modernization includes software-defined firewalls and cloud-based monitoring dashboards. Local players like Fortinet and Palo Alto Networks are deploying integrated OT security solutions for smart grid and industrial automation projects. Enterprise adoption is notably higher in healthcare and finance sectors, with facilities emphasizing secure operational continuity, while manufacturing plants focus on reducing unplanned downtime and enhancing threat visibility.

Why is industrial compliance shaping firewall adoption across major European markets?

Europe accounts for 28% of global OT firewall deployments, with Germany, UK, and France leading the adoption. Regulatory pressure from NIS2 and industrial cybersecurity mandates drives enterprises to implement explainable, protocol-aware firewall solutions. Adoption of AI-enabled threat detection and network micro-segmentation is widespread, with over 60% of large utilities and industrial plants integrating these technologies. Siemens and Schneider Electric are actively rolling out secure OT firewall solutions aligned with sustainability goals. European consumers prioritize compliance and operational transparency, leading to demand for detailed monitoring dashboards and automated reporting tools to maintain regulatory alignment across manufacturing and energy sectors.

How is smart manufacturing driving OT firewall growth in emerging economies?

Asia-Pacific represents 27% of global OT firewall deployment, with China, India, and Japan as top-consuming countries. Over 1,200 smart factories and industrial automation hubs have implemented protocol-aware firewall solutions to secure IoT-connected production lines. Infrastructure expansion, including high-speed rail networks and energy grid modernization, drives demand for ruggedized and edge-integrated firewalls. Local companies such as Huawei are developing AI-powered firewall solutions for industrial clients. Consumer behavior reflects rapid adoption in e-commerce, mobile applications, and AI-driven manufacturing analytics, emphasizing scalability and cloud-managed OT security capabilities to support fast-growing industrial ecosystems.

What factors are shaping industrial firewall adoption in South American industries?

South America accounts for approximately 7% of global OT firewall deployments, with Brazil and Argentina as primary markets. Investments in power generation, oil & gas, and smart water infrastructure are boosting adoption. Government incentives for industrial cybersecurity and trade policies facilitating technology imports support expansion. Local players like Stefanini are integrating AI-based OT firewall monitoring into regional industrial sites. Regional consumer behavior emphasizes language localization, cost-efficiency, and adaptability to legacy infrastructure, with over 60% of industrial operators prioritizing secure retrofitting of legacy SCADA and PLC systems.

How are oil, gas, and construction sectors driving OT firewall adoption?

The Middle East & Africa represents 7% of global OT firewall deployment, with UAE and South Africa as major growth countries. Demand is driven by oil & gas, construction, and utility modernization projects. Technological modernization includes AI-assisted threat monitoring and remote management of industrial control systems. Local enterprises such as DarkMatter are developing secure OT firewall solutions tailored to critical infrastructure. Consumer behavior emphasizes regulatory compliance, resilience against cyber-attacks, and energy-efficient firewall deployments to align with ESG initiatives, particularly in renewable energy and large-scale industrial projects.

United States – 38% market share; high production capacity and strong end-user adoption in energy, utilities, and manufacturing sectors.

Germany – 16% market share; stringent regulatory mandates and early integration of industrial IoT firewalls in manufacturing and utility facilities.

The OT Firewall market is moderately consolidated, with over 75 active global competitors ranging from multinational cybersecurity providers to specialized industrial security firms. The top five companies—Fortinet, Palo Alto Networks, Cisco Systems, Check Point Software Technologies, and Siemens—together account for approximately 52% of the total market, reflecting strong positioning in enterprise-scale energy, manufacturing, and utility projects. Market competition is shaped by product differentiation, advanced protocol inspection, AI-enabled anomaly detection, and edge-based security solutions. Strategic initiatives include partnerships between firewall vendors and industrial automation providers, as well as targeted product launches addressing SCADA, PLC, and IoT connectivity security. In 2024 alone, Fortinet deployed over 1,200 industrial-grade firewalls across smart grid projects, while Palo Alto Networks introduced AI-driven OT firewall orchestration for multiple manufacturing sites. Mergers and acquisitions are accelerating consolidation in North America and Europe, with niche vendors focusing on AI, cloud management, and zero-trust segmentation to gain a competitive edge. Innovation trends such as cloud-managed centralized monitoring, predictive threat intelligence, and protocol-aware deep packet inspection are influencing market positioning and shaping strategic differentiation among active competitors.

Check Point Software Technologies

Siemens

Schneider Electric

Honeywell

ABB

Rockwell Automation

Juniper Networks

Huawei

DarkMatter

The OT Firewall market is increasingly driven by technological advancements that enhance industrial cybersecurity, operational reliability, and regulatory compliance. Next-generation OT firewalls now incorporate protocol-aware deep packet inspection, allowing for real-time monitoring of over 85% of industrial communication protocols such as Modbus, DNP3, IEC 61850, and OPC UA. AI-powered anomaly detection engines are deployed in more than 60% of large industrial sites across North America and Europe, enabling automatic identification of unusual network behavior and reducing mean time to respond (MTTR) by up to 35%.

Edge-based OT firewalls are gaining traction, with over 1,000 smart factories in Asia-Pacific adopting localized inspection systems to improve network performance by 28% while maintaining low latency for real-time automation processes. Cloud-managed firewall orchestration platforms now cover 45% of distributed industrial deployments, offering centralized monitoring, policy updates, and threat intelligence sharing across multi-site operations. Integration with zero-trust network segmentation frameworks is accelerating, with 58% of energy and utility operators implementing micro-segmentation to isolate critical control systems from enterprise IT networks, reducing lateral movement risks by 30%.

Emerging technologies also include AI-assisted predictive threat analytics, which forecast potential attacks on SCADA systems, and virtualized firewall appliances optimized for hybrid IT-OT environments. Additionally, energy-efficient and ruggedized hardware designs are now deployed in over 65% of industrial sites in harsh environments, ensuring continuous operations under extreme temperature and vibration conditions. These technological innovations collectively position OT firewall solutions as a critical component of secure, resilient, and intelligent industrial operations worldwide.

• In March 2025, Fortinet expanded its OT Security Platform with enhanced FortiGuard OT Security Service, introducing ruggedized 5G connectivity appliances and AI-enhanced SecOps features that improve threat visibility across over 3,300 OT protocol rules and nearly 750 intrusion prevention system signatures, strengthening industrial infrastructure defenses.

• In 2025, Fortinet’s Fabric‑Ready Technology Alliance Partner Program surpassed 3,000 validated integrations with more than 400 technology partners, significantly broadening interoperability for OT firewall deployments and enabling more efficient, centralized threat response across multivendor industrial environments.

• In October 2025, Palo Alto Networks was recognized as an Overall Leader in the 2025 KuppingerCole Leadership Compass for Secure Remote Access for OT/ICS, highlighting the increasing emphasis on unified secure access controls within OT firewall architectures as remote connectivity grows in industrial operations.

• In 2024, Palo Alto Networks introduced new OT security capabilities powered by Precision AI™, including guided virtual patching and ruggedized next‑generation firewalls designed for harsh industrial environments, enhancing remote operations security and risk mitigation for critical OT assets.

The OT Firewall Market Report covers comprehensive segmentation and analysis across types, applications, and end‑user industries, outlining the evolving landscape of operational technology security. It evaluates ruggedized hardware firewalls, virtualized and cloud‑managed OT firewalls, and edge deployment models tailored for harsh industrial environments and distributed networks. This scope includes in‑depth examination of protocol‑aware inspection capabilities, intrusion prevention, secure remote access, micro‑segmentation, and AI‑driven anomaly detection technologies that enhance visibility into industrial control systems such as PLC, SCADA, and IIoT networks.

Geographic insights encompass North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, highlighting deployment volumes, regulatory influences, and technology adoption trends across major markets. Application analysis focuses on network segmentation, secure remote access, centralized monitoring, and compliance enforcement, detailing how these use cases address specific operational challenges in energy, utilities, manufacturing, transportation, and water treatment sectors.

The report also addresses industry focus areas including critical infrastructure protection, regulatory compliance with stringent cybersecurity mandates, and digital transformation programs prompting OT firewall integrations. Emerging segments such as zero‑trust frameworks, cloud‑orchestrated firewall management, and AI/ML‑enabled threat intelligence are explored, demonstrating how innovation is reshaping OT security paradigms. Additionally, niche segments like hybrid IT‑OT convergence, 5G‑enabled industrial connectivity, and edge‑native security solutions are included to inform decision‑makers of future opportunities and risk mitigation strategies within operational technology environments.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

11.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Fortinet, Palo Alto Networks, Cisco Systems, Check Point Software Technologies, Siemens, Schneider Electric, Honeywell, ABB, Rockwell Automation, Juniper Networks, Huawei, DarkMatter |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |