Reports

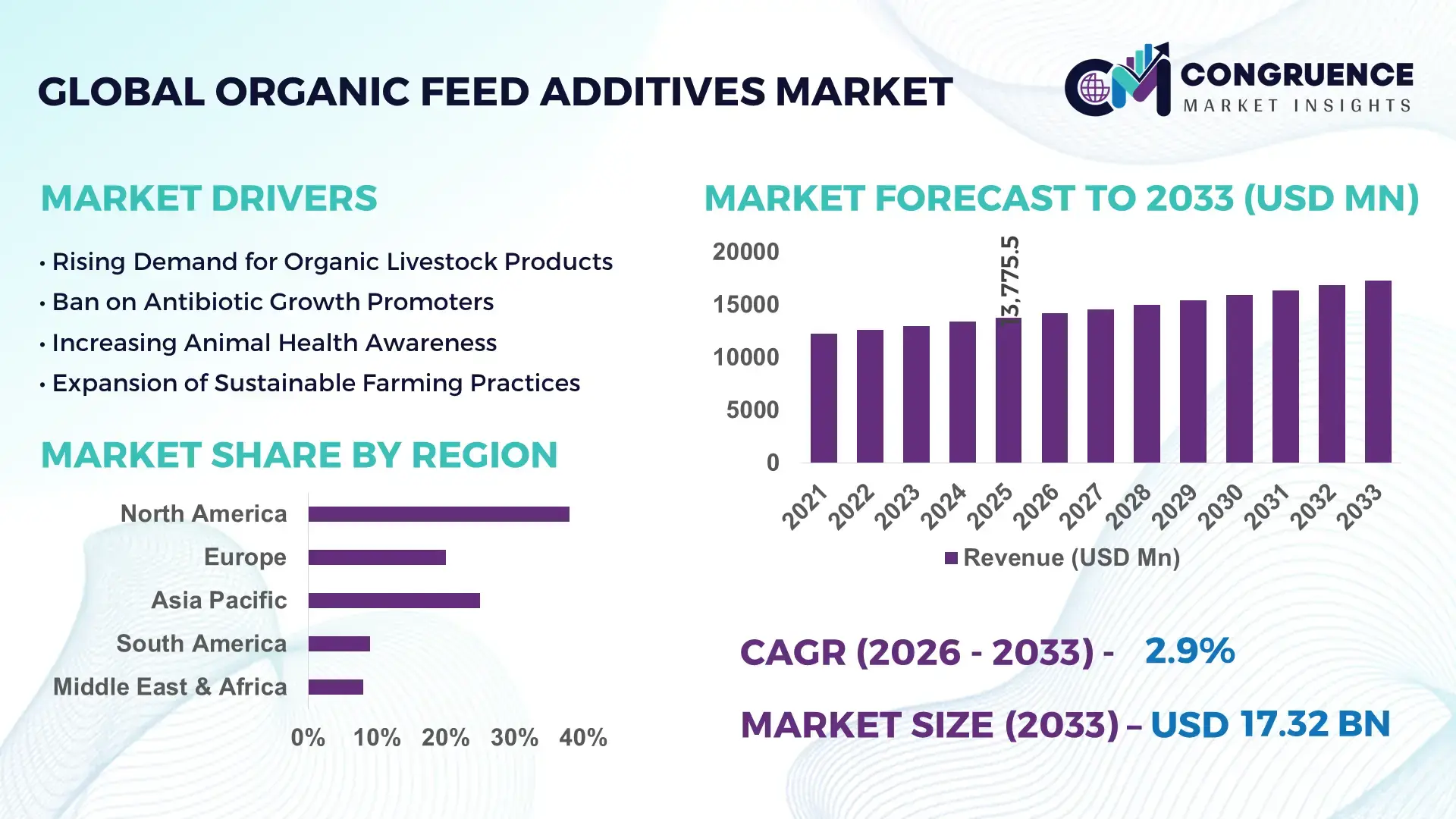

The Global Organic Feed Additives Market was valued at USD 13775.52 Million in 2025 and is anticipated to reach a value of USD 17315.34 Million by 2033 expanding at a CAGR of 2.9% between 2026 and 2033. The market expansion is primarily supported by rising demand for certified organic livestock products and antibiotic-free animal nutrition solutions.

The United States dominates the Organic Feed Additives Market with a well-established organic livestock ecosystem and advanced feed manufacturing infrastructure. The country accounts for over 17,000 certified organic farms, including more than 4 million acres dedicated to organic feed crops such as corn and soybeans. Annual organic food sales in the U.S. exceed USD 60 billion, with organic dairy and poultry representing significant end-use applications for organic feed additives. Investment in precision feed formulation technologies and enzyme-based additive production has increased by over 12% annually across leading U.S. feed mills. Additionally, more than 60% of organic poultry producers in the country utilize plant-based growth promoters and probiotic feed additives to enhance feed conversion ratios and flock health performance.

Market Size & Growth: Valued at USD 13,775.52 Million in 2025, projected to reach USD 17,315.34 Million by 2033 at 2.9% CAGR, driven by rising antibiotic-free livestock production and organic meat consumption.

Top Growth Drivers: 28% rise in organic livestock farming adoption, 22% improvement in feed efficiency using enzyme blends, 18% increase in consumer preference for chemical-free animal products.

Short-Term Forecast: By 2028, precision organic feed formulations are expected to improve feed conversion efficiency by 12% and reduce veterinary intervention costs by 9%.

Emerging Technologies: Microencapsulation of phytogenic additives, next-generation probiotic strains, AI-based feed optimization platforms.

Regional Leaders: North America projected to reach USD 5,400 Million by 2033 with strong certified farm networks; Europe to exceed USD 4,800 Million driven by strict organic regulations; Asia-Pacific anticipated to cross USD 3,900 Million supported by expanding poultry production.

Consumer/End-User Trends: Poultry accounts for over 40% of organic additive usage, followed by dairy cattle and swine, with increasing demand for plant-derived growth promoters.

Pilot Case Example: In 2024, a European poultry cooperative achieved 14% improvement in feed conversion ratio using encapsulated organic enzymes.

Competitive Landscape: Cargill holds approximately 14% share, followed by Archer Daniels Midland, DSM-Firmenich, BASF, and Alltech.

Regulatory & ESG Impact: EU organic regulation mandates 100% organic feed for certified livestock; producers targeting 20% carbon footprint reduction by 2030.

Investment & Funding Patterns: Over USD 1.2 Billion invested globally in organic feed processing and R&D facilities between 2022–2025.

Innovation & Future Outlook: Integration of bio-fermented additives, traceability-enabled supply chains, and climate-smart feed solutions shaping long-term competitiveness.

Organic Feed Additives are extensively used across poultry, dairy, swine, and aquaculture sectors, with poultry contributing nearly 40% of total demand due to rapid production cycles and high feed turnover rates. Technological innovation in enzyme blends, organic acidifiers, and phytogenic extracts has improved nutrient absorption efficiency by up to 15% in controlled feeding trials. Regulatory frameworks in North America and Europe require strict compliance with certified organic input standards, strengthening product differentiation. Asia-Pacific is witnessing accelerated adoption, particularly in India and China, where organic poultry consumption has grown by double digits annually. Future growth is linked to carbon-neutral feed strategies, bio-based preservative solutions, and digital feed traceability platforms enhancing supply chain transparency.

The Organic Feed Additives Market holds strategic relevance as global livestock producers transition toward antibiotic-free, sustainable, and traceable animal nutrition systems. With over 190 countries implementing stricter residue regulations and organic certification norms, feed manufacturers are redesigning formulations to align with premium organic livestock standards. Advanced microencapsulated phytogenic additives deliver 15% improvement in nutrient stability compared to conventional powder-based additives, reducing nutrient loss during feed processing.

North America dominates in volume, while Europe leads in adoption with nearly 45% of certified livestock enterprises incorporating fully organic feed systems. By 2028, AI-driven feed optimization platforms are expected to reduce raw material wastage by 10% and enhance productivity tracking accuracy by 18%. Firms are committing to ESG metrics such as 25% carbon emission reduction and 30% recyclable packaging integration by 2030.

In 2024, a Danish livestock integrator achieved 16% improvement in gut health performance metrics through probiotic-based organic feed solutions combined with digital monitoring systems. Strategic partnerships between biotechnology firms and feed mills are accelerating the commercialization of fermentation-derived amino acids and plant-based growth promoters. As regulatory scrutiny intensifies and consumer demand for ethically sourced meat expands, the Organic Feed Additives Market is positioned as a pillar of resilience, compliance, and sustainable growth within the global agribusiness ecosystem.

The global reduction of antibiotic growth promoters in animal husbandry is a primary growth catalyst for the Organic Feed Additives Market. Over 60 countries have introduced partial or complete bans on routine antibiotic use in feed, compelling livestock producers to adopt natural alternatives such as probiotics, phytogenic extracts, and enzyme complexes. Studies indicate that probiotic-based organic additives can improve gut health indicators by 12–18% while reducing mortality rates in poultry by nearly 8%. Retail demand for antibiotic-free poultry and dairy products has increased by over 25% in developed economies, strengthening supply chain commitments to organic feed standards. As consumer scrutiny intensifies, producers are integrating certified organic feed additives to maintain productivity while meeting regulatory compliance benchmarks.

The Organic Feed Additives Market faces constraints due to elevated certification expenses and premium pricing of organic raw materials. Certified organic crops often cost 20–35% more than conventional feedstock due to lower yields and stricter cultivation practices. Compliance audits, traceability documentation, and third-party validation processes increase operational overhead for feed manufacturers. Furthermore, organic enzyme and probiotic strains require specialized fermentation facilities, raising capital investment requirements. Small and medium-scale feed mills may struggle to absorb these incremental costs, limiting broader adoption in price-sensitive markets. Volatility in organic grain supply, particularly during climatic disruptions, can also lead to inconsistent pricing structures and production planning challenges.

Precision livestock nutrition and bio-fermentation technologies present significant growth opportunities within the Organic Feed Additives Market. Advanced fermentation platforms enable high-yield production of organic amino acids and enzymes with up to 20% improved purity levels. Digital feed analytics tools can optimize nutrient balance, improving feed conversion ratios by approximately 10% in poultry systems. Expansion of organic aquaculture, particularly in Asia-Pacific, is generating demand for marine-safe probiotic additives. In addition, carbon-neutral feed production initiatives are creating opportunities for plant-based preservative solutions and sustainable supply chain integration. Companies investing in biotechnology-driven additive innovation are well-positioned to capitalize on rising global demand for performance-enhancing yet regulation-compliant feed inputs.

Supply chain instability and climate variability pose ongoing challenges for the Organic Feed Additives Market. Organic crop production is highly sensitive to weather fluctuations, with drought events capable of reducing yields by 15–20% in certain regions. Limited availability of certified organic raw materials can disrupt additive manufacturing schedules and increase procurement lead times. International trade restrictions and logistical bottlenecks further complicate cross-border distribution of certified inputs. Additionally, maintaining strict segregation between organic and conventional supply chains requires specialized storage and transportation infrastructure, increasing operational complexity. These factors collectively impact cost stability, production consistency, and long-term scalability for organic feed additive manufacturers worldwide.

Accelerated Adoption of Phytogenic and Plant-Based Additives (Up 26% in Large-Scale Poultry Operations)

The shift toward botanical extracts and essential oil-based feed solutions has intensified, with adoption increasing by 26% across large commercial poultry farms between 2022 and 2025. Phytogenic additives are improving feed conversion ratios by 10–14% while reducing pathogen load in gut health trials by nearly 18%. More than 48% of certified organic livestock farms in Europe now incorporate plant-derived growth promoters as part of antibiotic-free nutrition programs. Standardized herbal blends with controlled active compound concentration are also reducing formulation variability by 12%, strengthening performance predictability in organic broiler and layer production systems.

Expansion of Probiotic and Microbiome-Based Feed Solutions (Used in 52% of Organic Dairy Systems)

Microbiome-optimized feed additives are being implemented in 52% of organic dairy farms in North America to enhance rumen stability and nutrient absorption. Field performance data indicate up to 15% improvement in milk yield consistency and 11% reduction in digestive disorders when multi-strain probiotics are used. Encapsulated probiotic delivery systems have extended shelf life by 20%, addressing storage and transport challenges in tropical regions. Precision microbial mapping tools are enabling livestock producers to tailor probiotic combinations based on species-specific gut microbiota composition.

Integration of Digital Feed Optimization Platforms (Improving Nutrient Efficiency by 13%)

AI-enabled feed formulation systems are improving nutrient utilization efficiency by 13% in integrated livestock enterprises. Approximately 37% of large feed manufacturers now deploy cloud-based ration balancing software that integrates organic ingredient traceability modules. These systems reduce formulation errors by 9% and minimize organic raw material wastage by nearly 8%. Blockchain-backed traceability platforms are being used in 29% of cross-border organic feed supply chains to ensure compliance with certification requirements and enhance transparency.

Rising Demand for Carbon-Neutral and Climate-Smart Feed Additives (Targeting 25% Emission Reduction by 2030)

Sustainability-driven procurement is reshaping product development, with 41% of global organic feed producers implementing carbon-footprint tracking mechanisms. Enzyme-based additives designed to reduce methane emissions in ruminants have demonstrated 12–16% emission reductions in controlled farm studies. Nearly 33% of European livestock cooperatives have committed to reducing feed-related greenhouse gas emissions by at least 25% by 2030. Biodegradable packaging adoption for organic feed additives has increased by 19%, aligning with circular economy mandates and ESG benchmarks.

The Organic Feed Additives Market is segmented by type, application, and end-user categories, reflecting diversified livestock nutrition requirements and evolving compliance standards. By type, probiotics, phytogenic additives, enzymes, organic acids, and amino acids represent the primary product clusters supporting species-specific nutritional optimization. Poultry accounts for the largest application share due to shorter production cycles and higher feed turnover rates, while dairy and swine follow closely. End-user segmentation highlights commercial livestock farms as dominant consumers, with integrated feed mills and contract farming operations contributing significantly to volume demand. Regional consumption patterns show higher penetration in North America and Europe, where over 45% of certified livestock producers rely exclusively on organic-compliant feed solutions. Emerging markets in Asia-Pacific are expanding capacity, supported by double-digit growth in organic poultry farming and increasing regulatory standardization across supply chains.

Probiotics currently account for 34% of total adoption within the Organic Feed Additives Market, leading due to their measurable impact on gut health stabilization and immunity enhancement. Field evaluations indicate probiotic supplementation reduces mortality rates by 8–12% in poultry systems. Phytogenic additives hold 27% share, widely used for natural growth promotion and pathogen control. However, enzyme-based organic additives represent the fastest-growing type, expanding at 5.6% CAGR, driven by their ability to improve nutrient digestibility by up to 15% and reduce feed waste by 10%. Organic acids and amino acids collectively contribute 39% of the remaining market share, playing niche roles in pH balance and protein optimization. Acidifiers have demonstrated 9% improvement in feed hygiene stability, particularly in swine production.

Poultry applications dominate with approximately 40% share in the Organic Feed Additives Market, supported by high-volume broiler production cycles and strict residue-free meat standards. Dairy follows with 28% share, benefiting from probiotic and enzyme formulations that improve milk yield stability by nearly 12%. Swine applications account for 18%, particularly in regions enforcing growth promoter restrictions. Aquaculture represents the fastest-growing application segment, projected to expand at 6.2% CAGR, fueled by rising organic seafood demand and increasing probiotic usage to reduce aquatic disease outbreaks by 14%. Other applications, including small ruminants and specialty livestock, collectively contribute 14% of market utilization.

Commercial livestock farms represent the leading end-user segment, accounting for 46% of total organic feed additive consumption due to scale-driven procurement strategies and compliance obligations. Integrated feed mills contribute 31%, supplying customized organic formulations to contract farmers and cooperatives. However, contract farming networks are the fastest-growing end-user group, expanding at 5.1% CAGR as retailers demand vertically traceable supply chains. Smallholder organic farms and specialty breeders collectively account for 23% of the market, with adoption rates exceeding 38% in European certified livestock clusters. Large agribusiness enterprises report 17% operational efficiency gains after integrating digital feed tracking and certified additive sourcing systems.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.4% between 2026 and 2033.

North America’s dominance is supported by over 18,000 certified organic livestock farms and more than 6 million metric tons of organic feed production annually. Europe follows with a 32% market share, driven by stringent feed compliance frameworks across 27 EU member states and over 15 million hectares of certified organic agricultural land. Asia-Pacific holds approximately 21% share, with China and India together accounting for more than 45% of regional organic poultry production. South America represents 6% of global demand, largely concentrated in Brazil and Argentina, where organic soybean cultivation exceeds 1.2 million hectares. The Middle East & Africa collectively account for 3%, supported by expanding poultry consumption exceeding 9 million metric tons annually. Cross-regional investments in fermentation-based additives increased by 17% between 2023 and 2025, reflecting a global shift toward sustainable, performance-enhancing organic feed solutions.

How Are Advanced Livestock Nutrition Standards Reshaping Competitive Dynamics?

North America holds approximately 38% of the global Organic Feed Additives Market share, supported by large-scale organic poultry and dairy production. The United States and Canada collectively produce over 7 million metric tons of organic feed annually, with poultry accounting for nearly 42% of additive utilization. Regulatory frameworks mandate 100% certified organic feed inputs for labeled livestock products, strengthening demand for compliant enzyme and probiotic solutions. Digital feed optimization platforms are deployed in nearly 35% of large feed mills, improving nutrient precision by 12%. Cargill has expanded its organic-certified additive portfolio, increasing production capacity by 15% through facility upgrades. Regional consumer behavior reflects strong demand for antibiotic-free meat and dairy, with more than 60% of surveyed consumers preferring certified organic protein products, driving stable procurement volumes across commercial livestock operations.

Why Are Stringent Livestock Compliance Policies Accelerating Innovation?

Europe accounts for approximately 32% of the Organic Feed Additives Market, led by Germany, France, the United Kingdom, Italy, and Spain. The region supports over 15 million hectares of certified organic farmland and more than 400,000 organic livestock producers. Regulatory mandates require complete traceability of feed ingredients, prompting 48% of feed manufacturers to integrate blockchain-based monitoring systems. Sustainability initiatives targeting 25% emission reductions in agriculture by 2030 have increased demand for methane-reducing enzyme additives. DSM-Firmenich has introduced advanced phytogenic blends improving feed efficiency by 11% in poultry trials. Regional consumer behavior emphasizes transparency and sustainability, with over 55% of organic meat buyers prioritizing certified eco-label compliance, thereby strengthening consistent additive adoption across cooperative farming networks.

How Is Expanding Poultry Production Driving Nutritional Modernization?

Asia-Pacific ranks third in global market share at 21% but leads in growth momentum. China, India, and Japan are the top consuming countries, collectively producing more than 14 billion poultry birds annually. Organic poultry farming in India increased by 18% between 2022 and 2025, while China expanded certified organic feed manufacturing facilities by 22% in the same period. Regional manufacturing capacity now exceeds 4 million metric tons of certified organic feed annually. Innovation hubs in Shanghai and Bangalore are developing fermentation-derived amino acids with 13% higher purity levels. Alltech has expanded its regional distribution network by 20% to support rising demand. Consumer behavior in Asia-Pacific reflects rising middle-class purchasing power, with organic meat consumption increasing by 16% in urban centers, driving additive integration across vertically integrated poultry systems.

What Role Does Export-Oriented Livestock Production Play in Market Expansion?

South America represents approximately 6% of the Organic Feed Additives Market, with Brazil and Argentina leading regional consumption. Brazil alone produces over 13 million metric tons of poultry annually, with organic-certified operations expanding by 9% between 2023 and 2025. Argentina supports over 3 million hectares of organic crop cultivation, supplying certified soy and corn for additive production. Government-backed agricultural export programs incentivize sustainable livestock production, while trade agreements facilitate organic product access to European markets. Local feed producers have invested 14% more in organic-compliant blending facilities to meet export traceability standards. Regional consumer behavior is influenced by export-driven livestock systems, where compliance with international organic certifications determines procurement strategies for feed additives.

How Is Livestock Modernization Supporting Sustainable Feed Demand?

The Middle East & Africa account for nearly 3% of global demand, with growth centered in the UAE, Saudi Arabia, and South Africa. Poultry consumption in the GCC region exceeds 4 million metric tons annually, prompting modernization of feed infrastructure. Over 28% of commercial poultry farms in the UAE have integrated organic-certified feed solutions to align with food security initiatives. South Africa supports more than 2,500 certified organic farms, increasing demand for plant-based additives. Technological modernization includes automated feed blending systems improving batch accuracy by 10%. Regional trade partnerships have reduced import tariffs on certified feed inputs by up to 8%, encouraging supply chain diversification. Consumer behavior reflects growing interest in premium organic meat products among urban populations, particularly in high-income metropolitan areas.

United States – 34% market share: Strong organic livestock production capacity exceeding 6 million metric tons of certified feed annually and strict antibiotic-free regulations drive Organic Feed Additives Market leadership.

Germany – 11% market share: Extensive organic farmland covering over 2 million hectares and high adoption of traceable feed systems support Germany’s prominent position in the Organic Feed Additives Market.

The Organic Feed Additives Market is moderately fragmented, with over 120 active global and regional competitors operating across probiotics, enzymes, phytogenic blends, and organic acid segments. The top five companies collectively account for approximately 48% of the total market share, indicating balanced competitive intensity. Strategic initiatives include more than 35 product launches between 2023 and 2025 focused on microencapsulated enzyme formulations and methane-reducing additives. Partnerships between biotechnology firms and feed mills increased by 19%, accelerating commercialization timelines. Nearly 27% of leading players have expanded fermentation capacity to improve additive purity and scalability. Vertical integration strategies are gaining prominence, with 22% of large manufacturers securing upstream organic raw material contracts to stabilize supply chains. Digital traceability adoption across major players exceeds 40%, strengthening regulatory compliance positioning. Competitive differentiation increasingly revolves around sustainability credentials, precision nutrition technologies, and species-specific performance optimization capabilities.

Cargill

Archer Daniels Midland Company

DSM-Firmenich

BASF

Alltech

Chr. Hansen

Novus International

Kemin Industries

Biomin

Nutreco

Evonik Industries

Adisseo

Technological advancement in the Organic Feed Additives Market is increasingly centered on bio-fermentation, precision nutrition analytics, and advanced delivery systems designed to enhance bioavailability and stability. Modern fermentation facilities now achieve microbial yield efficiency improvements of 18–22% through optimized strain engineering and controlled bioreactor automation. High-density fermentation allows production of probiotic concentrations exceeding 10¹¹ CFU per gram, supporting consistent gut health outcomes in poultry and ruminants.

Microencapsulation technology is transforming phytogenic and enzyme-based additives by protecting active compounds from thermal degradation during pelleting processes that often exceed 80°C. Encapsulated formulations have demonstrated 15% higher nutrient retention compared to non-coated alternatives and improved shelf stability by up to 25%. Additionally, next-generation enzyme blends incorporating xylanase, phytase, and protease complexes are delivering up to 14% improvement in feed digestibility metrics, particularly in corn-soy-based organic rations.

Digital feed optimization platforms are gaining traction, with approximately 37% of large organic feed mills integrating AI-based ration balancing systems. These platforms reduce formulation deviations by 9% and lower raw material wastage by nearly 8%. Blockchain-enabled traceability tools are now embedded in 30% of certified organic supply chains, ensuring compliance with strict labeling standards and enhancing audit transparency.

Emerging innovations include methane-reducing feed additives capable of lowering enteric emissions in dairy cattle by 12–16% in controlled farm trials. Plant-derived bioactive compounds standardized through chromatographic purification processes are also improving batch-to-batch consistency by 10%, reinforcing product reliability. Collectively, these technologies position the Organic Feed Additives Market at the intersection of sustainability, digitalization, and high-performance livestock nutrition.

• In March 2024, DSM-Firmenich announced the expansion of its methane-reducing feed additive Bovaer® into additional global markets, supported by increased production capacity. The additive demonstrated methane emission reductions of up to 30% in dairy cattle under commercial farm conditions. Source: www.dsm-firmenich.com

• In September 2024, Cargill expanded its animal nutrition operations with enhanced digital feed formulation tools integrated into its U.S. facilities, improving ration precision and traceability for organic livestock producers across more than 20 states. Source: www.cargill.com

• In February 2025, Evonik Industries introduced an upgraded probiotic solution within its GutCare portfolio, designed to enhance intestinal stability in poultry and improve feed efficiency metrics by double-digit percentages during field trials.

• In April 2025, Alltech announced the opening of a new fermentation production line to increase capacity for its yeast-based organic feed additives, strengthening supply capabilities for certified organic livestock operations in North America and Europe.

The Organic Feed Additives Market Report provides a structured and comprehensive evaluation of product categories, livestock applications, technological frameworks, and geographic demand centers shaping industry performance. The scope covers primary additive types including probiotics, phytogenic extracts, enzymes, organic acids, and amino acids, collectively representing 100% of certified organic-compliant nutritional inputs used across commercial livestock systems. Poultry applications account for approximately 40% of additive utilization, followed by dairy at 28%, swine at 18%, and aquaculture and specialty livestock comprising the remaining 14%.

Geographically, the report analyzes five key regions—North America (38% share), Europe (32%), Asia-Pacific (21%), South America (6%), and Middle East & Africa (3%)—with country-level assessments for major producers such as the United States, Germany, China, Brazil, and the UAE. The report evaluates over 120 active market participants and reviews strategic initiatives including more than 35 recent product launches and capacity expansions recorded between 2023 and 2025.

Technological coverage includes fermentation capacity expansion trends exceeding 20% efficiency gains, microencapsulation advancements improving nutrient retention by 15%, and digital feed optimization platforms adopted by over one-third of large feed mills. The study further examines ESG integration metrics, carbon-reduction targets of 25% by 2030 among leading producers, and traceability compliance adoption rates surpassing 40% in regulated markets. This broad analytical scope enables decision-makers to assess competitive positioning, operational scalability, regulatory readiness, and long-term sustainability alignment within the Organic Feed Additives Market ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

2.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Cargill, Archer Daniels Midland Company, DSM-Firmenich, BASF, Alltech, Chr. Hansen, Novus International, Kemin Industries, Biomin, Nutreco, Evonik Industries, Adisseo |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |