Reports

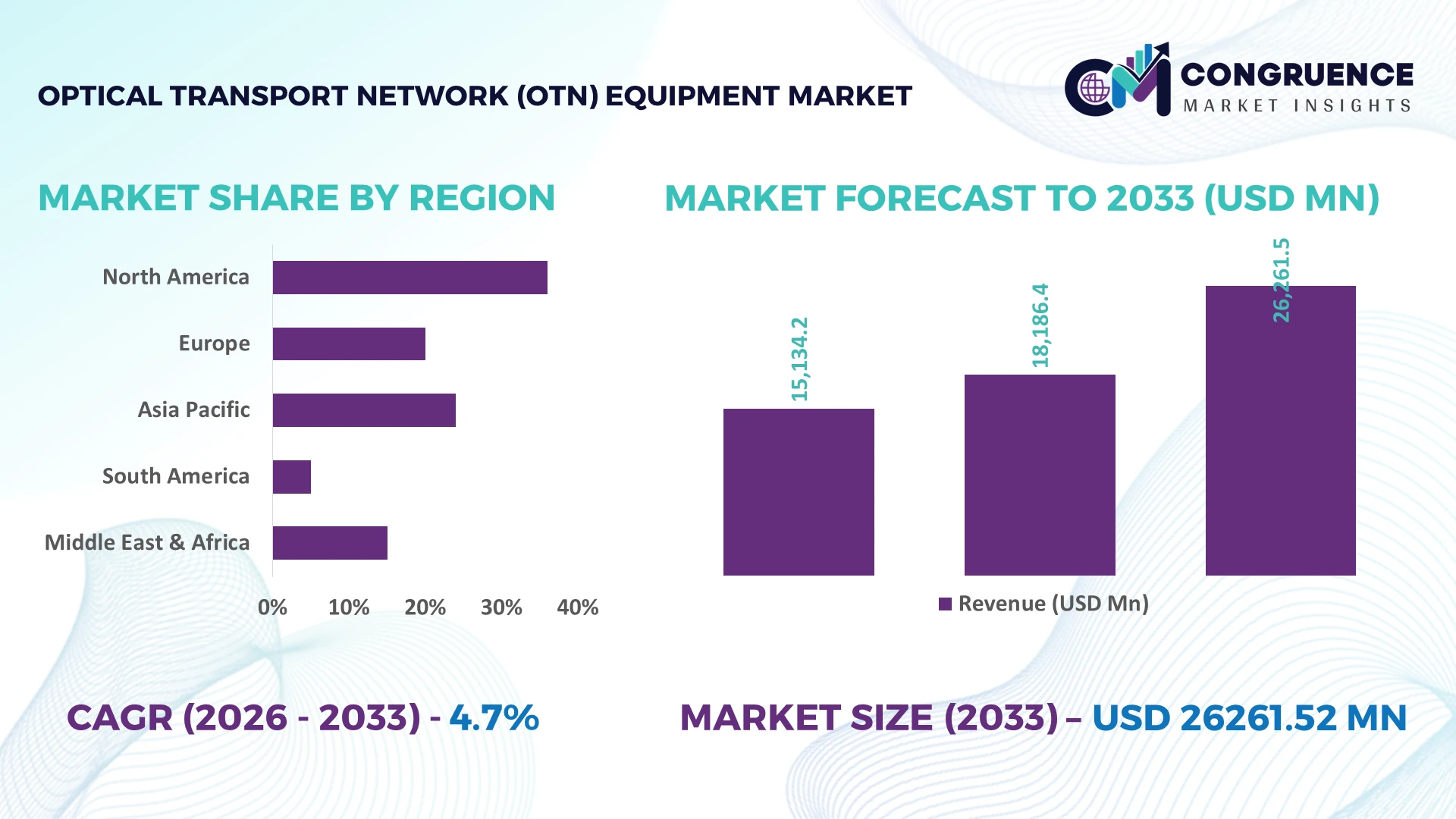

The Global Optical Transport Network (OTN) Equipment Market was valued at USD 18186.39 Million in 2025 and is anticipated to reach a value of USD 26261.52 Million by 2033 expanding at a CAGR of 4.7% between 2026 and 2033. Rising deployment of AI-ready data centers, 800G coherent optical networks, hyperscale cloud connectivity, and national fiber backbone modernization programs is accelerating advanced Optical Transport Network (OTN) equipment adoption across telecom and enterprise infrastructure.

China dominates the global Optical Transport Network (OTN) Equipment Market, accounting for nearly 38% of installed optical transport infrastructure, supported by over 4.6 million operational 5G base stations, large-scale cloud investments, and nationwide backbone expansion. In comparison, the United States leads in hyperscale data center interconnect deployments with over 35% of global hyperscale capacity, while China's metro and long-haul optical deployments remain substantially higher. Continued digital infrastructure investments amid ongoing global technology supply-chain realignment reinforce China's leadership in high-capacity optical networking.

Organizations investing in scalable OTN infrastructure, intelligent transport automation, and next-generation optical capacity will secure stronger network resilience and long-term competitive advantage.

Market Size & Growth: USD 18,186.39 Million (2025) to USD 26,261.52 Million (2033) at 4.7% CAGR, supported by AI data center expansion and 800G optical network deployment.

Top Growth Drivers: AI traffic (+34%), hyperscale cloud connectivity (+29%), and fiber backbone modernization (+24%) remain the three strongest growth catalysts.

Short-Term Forecast: By 2028, intelligent OTN automation is expected to reduce network provisioning time by 35% while improving bandwidth utilization by 22%.

Emerging Technologies: AI-driven network management, coherent 800G optics, and software-defined transport improve transmission efficiency by over 30%.

Regional Leaders: Asia-Pacific exceeds USD 10 Billion, North America surpasses USD 7 Billion, while Europe approaches USD 5 Billion through cloud and edge infrastructure expansion.

Consumer/End-User Trends: More than 68% of hyperscale operators prioritize programmable OTN platforms for low-latency AI, cloud, and enterprise connectivity.

Pilot/Case Example: A 2026 national backbone modernization program increased optical transmission efficiency by 27% and reduced service interruptions by 18%.

Competitive Landscape: Huawei leads with approximately 18% market share, followed by Ciena, Nokia, Cisco, and Infinera competing through technology innovation and network performance.

Regulatory & ESG Impact: Energy-efficient optical platforms reduce network power consumption by nearly 20% while supporting national digital infrastructure and sustainability targets.

Investment & Funding: More than USD 8 Billion has been committed to fiber expansion, strategic partnerships, and advanced optical transport deployment amid global supply-chain diversification.

Innovation & Future Outlook: Open optical networking, AI-assisted automation, and programmable transport architectures are driving the next phase of high-capacity digital infrastructure.

The Optical Transport Network (OTN) Equipment Market continues to benefit from increasing investments across hyperscale data centers, telecom backbone modernization, financial networks, and government digital infrastructure. Recent innovations in AI-powered optical network management and coherent 800G transmission are improving bandwidth efficiency by more than 30%, while regional supply-chain diversification and infrastructure security initiatives are accelerating advanced optical transport deployments, setting the foundation for the strategic market analysis that follows.

Optical Transport Network (OTN) equipment has become a strategic infrastructure priority as telecom operators, hyperscale cloud providers, and governments expand high-capacity digital connectivity to support AI computing, cloud services, and critical enterprise applications. Infrastructure modernization and technology supply-chain restructuring are shifting procurement toward programmable optical platforms that improve network resilience while reducing dependence on legacy transport architectures. This transition is strengthening competitive positioning for vendors capable of delivering scalable, software-driven optical ecosystems.

Modern coherent 800G OTN platforms deliver up to 40% higher spectral efficiency and reduce power consumption by nearly 20% compared with legacy 100G transport systems, lowering operational costs while increasing network capacity. China continues leading large-scale backbone deployments through nationwide digital infrastructure programs, whereas the United States remains the innovation leader in hyperscale data center interconnect and AI-driven optical networking. Over the next two to three years, automation-enabled optical management is expected to exceed 60% adoption among new backbone deployments, improving network utilization and accelerating service provisioning.

Telecom operators are deploying intelligent OTN equipment to interconnect AI data centers while manufacturers expand partnerships for programmable optical software and coherent transmission technologies. Companies prioritizing integrated hardware, automation, and open networking architectures will strengthen operational flexibility, reduce lifecycle costs, and establish durable competitive advantages across evolving digital infrastructure markets.

Rapid AI infrastructure expansion and hyperscale cloud investment are transforming demand for advanced Optical Transport Network (OTN) equipment. Global IP traffic continues rising by more than 25% annually, while deployment of coherent 800G optical solutions has increased by approximately 35% across major telecom backbone projects. China and the United States are accelerating national fiber modernization and data center interconnection programs to support low-latency digital services. These structural shifts are driving operators toward programmable optical transport with automated traffic management and higher bandwidth efficiency. Equipment manufacturers are responding through expanded R&D, strategic semiconductor partnerships, and software-defined networking integration, enabling faster deployment cycles and differentiated service capabilities. Vendors combining intelligent automation with scalable optical architectures are securing stronger positions in enterprise, cloud, and carrier infrastructure procurement.

Interoperability challenges between legacy transmission infrastructure and next-generation optical platforms remain a significant barrier to efficient deployment. More than 45% of existing carrier networks still rely on mixed-vendor architectures, increasing integration complexity and extending deployment timelines by nearly 20%. Semiconductor component availability and advanced optical module sourcing continue to experience periodic constraints, particularly for high-performance coherent optics manufactured in specialized facilities. These factors raise implementation costs and complicate large-scale modernization projects. Vendors are reducing operational risks by localizing component sourcing, expanding multi-vendor interoperability testing, and securing long-term supply agreements with photonic component manufacturers. Organizations adopting open optical standards and modular network architectures achieve greater procurement flexibility while minimizing infrastructure migration risks.

The convergence of AI-driven network automation, edge computing, and programmable transport is creating new value opportunities beyond traditional telecom infrastructure. Intelligent optical orchestration can reduce network operating costs by approximately 25% while increasing bandwidth utilization by nearly 30% through predictive traffic optimization. India and Japan are expanding digital infrastructure investments to strengthen cloud connectivity and industrial digitalization, creating demand for scalable metro and long-haul optical transport. Vendors are accelerating innovation through silicon photonics, open networking ecosystems, and strategic partnerships with cloud service providers. An emerging competitive advantage lies in delivering software-centric optical platforms capable of supporting enterprise AI workloads, private cloud interconnection, and low-latency industrial communications from a unified transport architecture.

Successfully scaling intelligent Optical Transport Network deployments requires overcoming increasing architectural complexity across cloud, edge, and legacy network environments. More than 50% of operators identify multi-domain orchestration as a primary deployment challenge, while cybersecurity investment in optical infrastructure has risen by over 18% as critical communications become more software-driven. Workforce shortages in advanced optical engineering and network automation further delay implementation of sophisticated transport architectures. Companies are responding through AI-enabled network management platforms, workforce development initiatives, and collaborative ecosystem partnerships that improve interoperability and operational visibility. Organizations capable of simplifying large-scale optical integration while maintaining secure, resilient network operations will achieve sustainable competitive differentiation in increasingly digital infrastructure markets.

AI-Driven Optical Network Automation: Telecom operators are embedding AI into optical transport operations, reducing fault detection time by nearly 45% and improving network utilization by approximately 28%. Large carriers in the United States and Japan are integrating predictive analytics into transport controllers to automate provisioning and maintenance workflows. Vendors are expanding software partnerships and automation capabilities to shorten deployment cycles, reduce operational expenditure, and address skilled workforce shortages affecting network management.

Rapid 800G Transport Migration: Deployment of coherent 800G optical transmission has increased by over 35%, while spectral efficiency has improved by nearly 40% compared with conventional 100G platforms. Demand is accelerating as AI clusters require high-capacity interconnects between hyperscale facilities. Equipment suppliers are restructuring product portfolios around programmable transport platforms, investing in advanced digital signal processors, and expanding interoperability testing to support multi-vendor backbone environments with lower energy consumption.

Open Optical Ecosystem Expansion: Adoption of open networking architectures has grown by roughly 30%, reducing multi-vendor integration costs by nearly 18% and accelerating service activation. European telecom operators are prioritizing interoperable transport layers following evolving digital infrastructure requirements, while enterprises increasingly seek flexible procurement strategies. Manufacturers are strengthening ecosystem partnerships, standardizing optical interfaces, and introducing software-defined management platforms that simplify network upgrades without extensive hardware replacement.

Edge Connectivity Driving Deployment: Edge computing deployments connected through optical transport have expanded by approximately 32%, while low-latency enterprise traffic has increased by nearly 26%. Manufacturing hubs in China and India are integrating distributed edge facilities with metro optical networks to support industrial automation and AI applications. Equipment providers are scaling compact OTN platforms, optimizing metro deployment strategies, and expanding regional production capacity to improve supply resilience and shorten equipment delivery timelines.

OTN Switches represent the leading segment because they provide high-capacity traffic aggregation, intelligent routing, and scalable network management across carrier and enterprise backbone infrastructure. More than 42% of newly deployed transport networks integrate advanced switching platforms to improve bandwidth allocation and reduce operational complexity. WDM Equipment continues serving long-haul transmission with strong deployment across national backbone projects, while OTN Multiplexers remain essential for efficient bandwidth consolidation. Optical Cross-Connects maintain strategic importance in large carrier networks where dynamic traffic engineering and service flexibility are operational priorities.

Optical Transponders are the fastest-growing segment as coherent 400G and 800G deployments expand across hyperscale cloud connectivity and AI infrastructure. Adoption has increased by approximately 34%, supported by demand for higher spectral efficiency and lower power consumption. Vendors are accelerating silicon photonics innovation, expanding programmable transponder portfolios, and strengthening technology partnerships to improve interoperability across multi-vendor environments. Investment priorities increasingly favor intelligent transport platforms capable of supporting software-defined optical networks while reducing lifecycle operating costs.

Long-Haul Networks continue leading application demand because national backbone expansion, submarine connectivity, and cross-country fiber modernization require resilient, high-capacity optical transport infrastructure. Nearly 44% of large-scale OTN deployments support long-distance transmission where reliability and bandwidth efficiency remain critical. Metro Networks continue expanding through smart city initiatives, while 5G Networks rely on OTN equipment to support high-capacity mobile backhaul with increasingly automated transport management.

Cloud Connectivity represents the fastest-growing application as AI workloads and hyperscale computing require scalable, low-latency interconnection between distributed data centers. Deployment has expanded by approximately 36%, while enterprise cloud traffic transported over optical backbone infrastructure has increased by nearly 30%. Data Centers are integrating programmable OTN solutions to improve operational efficiency and reduce provisioning delays. Vendors are responding through cloud partnerships, software-defined transport integration, and modular deployment models that support rapidly evolving enterprise connectivity requirements.

Telecom Operators remain the largest end-user group because nationwide fiber backbone deployment, 5G transport, and enterprise connectivity continue requiring high-capacity optical infrastructure. Approximately 48% of new OTN equipment installations are deployed by carrier networks modernizing transport architectures and increasing automation. Government organizations continue investing in secure national communications infrastructure, while Enterprises adopt OTN solutions to strengthen mission-critical connectivity across manufacturing, finance, and healthcare environments.

Cloud Providers represent the fastest-growing end-user segment as hyperscale facilities require scalable optical interconnection for AI computing clusters and distributed workloads. Demand has increased by nearly 38%, while Data Center Operators have expanded optical transport deployment by approximately 31% to improve bandwidth availability and network resilience. Equipment manufacturers are introducing customized optical platforms, strengthening cloud ecosystem partnerships, and developing flexible commercial models to capture rapidly expanding digital infrastructure investment while differentiating through automation and service performance.

Asia-Pacific accounted for the largest market share at 42.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a 6.3% CAGR between 2026 and 2033.

AI Data Center Interconnect Accelerates Optical Infrastructure

North America represents one of the most technologically advanced Optical Transport Network (OTN) equipment markets, supported by hyperscale cloud expansion, AI infrastructure deployment, and nationwide fiber modernization. The region contributes approximately 28% of global demand, with the United States accounting for the majority of carrier and enterprise deployments. Large-scale investment in data center interconnection and coherent optical networking continues to increase deployment density across metro and long-haul networks. More than 65% of newly commissioned hyperscale facilities incorporate programmable optical transport to support high-bandwidth AI workloads. Equipment vendors are strengthening cloud partnerships, expanding software-defined networking capabilities, and integrating automation to improve network efficiency and reduce operational complexity.

United States Market Outlook: The United States remains the regional technology leader due to its concentration of hyperscale cloud providers, advanced telecom infrastructure, and AI computing investments. More than one-third of global hyperscale data center capacity is located in the country, creating sustained demand for high-capacity optical transport solutions. Operators continue replacing legacy transport equipment with coherent optical platforms supporting 400G and 800G transmission, while enterprise digital transformation programs strengthen long-term procurement opportunities for programmable OTN infrastructure.

Network Modernization Driven by Open Optical Standards

Europe continues strengthening optical transport infrastructure through digital connectivity initiatives, open networking adoption, and cross-border backbone modernization. The region contributes nearly 22% of global deployment activity, supported by increasing enterprise cloud connectivity and carrier network upgrades. Telecom operators are prioritizing interoperable optical architectures that simplify multi-vendor integration while improving operational flexibility. More than 30% of recent backbone modernization projects incorporate software-defined transport management to enhance network utilization and reduce maintenance complexity. Equipment suppliers are expanding collaboration with network operators to accelerate deployment of intelligent optical platforms across national broadband infrastructure.

Germany Market Outlook: Germany leads the European market through strong industrial digitalization, advanced telecommunications infrastructure, and continuous investment in fiber backbone expansion. Manufacturing enterprises, automotive companies, and cloud operators increasingly require resilient optical transport for mission-critical communications. National broadband expansion and enterprise connectivity programs continue driving coherent optical deployments, while domestic operators invest in programmable transport technologies to improve operational efficiency and support growing industrial data traffic.

Large-Scale Infrastructure Deployment Sustains Regional Leadership

Asia-Pacific remains the largest Optical Transport Network (OTN) equipment market, accounting for approximately 42.8% of global deployment volume. Extensive fiber expansion, rapid 5G infrastructure rollout, hyperscale cloud development, and government-backed digital transformation programs continue driving large-scale optical transport investment. Regional manufacturers benefit from integrated production ecosystems and strong domestic demand, enabling faster commercialization of advanced optical technologies. More than 50% of newly deployed long-haul transport networks in major economies now incorporate coherent optical transmission platforms. Vendors continue expanding manufacturing capacity, silicon photonics development, and strategic carrier partnerships to maintain technology leadership.

China Market Outlook: China dominates regional demand through nationwide backbone modernization, extensive cloud infrastructure, and large-scale telecom investment. With more than 4.6 million operational 5G base stations and continuous expansion of AI computing facilities, the country requires high-capacity optical transport across metro and long-haul networks. Domestic equipment manufacturers continue investing in programmable optical platforms and advanced coherent transmission technologies while strengthening vertically integrated production capabilities that enhance supply-chain resilience.

Fiber Backbone Expansion Supports Enterprise Connectivity

South America is steadily expanding Optical Transport Network deployment as telecom operators modernize national backbone infrastructure and improve enterprise connectivity. The region represents approximately 5% of global market activity, supported by increasing fiber deployment and cloud service adoption. Investment remains concentrated around metropolitan corridors where bandwidth demand continues rising across financial services, government, and industrial sectors. Recent backbone projects have improved transmission capacity by nearly 20%, although infrastructure disparities between urban and remote areas continue influencing deployment speed. Equipment suppliers are strengthening regional distribution partnerships and localized technical support to improve implementation efficiency.

Brazil Market Outlook: Brazil remains the largest regional market because of its extensive telecommunications network, expanding cloud infrastructure, and increasing enterprise digitalization. National fiber backbone expansion and data center investment continue supporting higher demand for programmable optical transport platforms. Domestic operators are upgrading transport infrastructure to accommodate growing cloud connectivity and enterprise traffic while collaborating with technology vendors to improve network resilience and service quality across major commercial centers.

Digital Infrastructure Investment Reshapes Optical Networks

Middle East & Africa is rapidly strengthening optical transport infrastructure through digital economy initiatives, hyperscale data center investment, and international connectivity projects. The region contributes nearly 7% of global deployment activity while recording the fastest operational expansion supported by smart city development and subsea cable integration. Governments and telecom operators continue modernizing backbone infrastructure to support cloud computing, enterprise services, and AI-enabled digital platforms. Several national network projects have increased backbone transmission capacity by more than 25%, encouraging equipment manufacturers to expand partnerships and regional service capabilities.

Saudi Arabia Market Outlook: Saudi Arabia leads regional investment through Vision 2030 digital transformation initiatives, large-scale data center construction, and advanced telecommunications modernization. National operators continue deploying high-capacity optical transport to support cloud services, industrial automation, and smart infrastructure. Expanding hyperscale facilities and nationwide fiber projects are increasing demand for intelligent OTN platforms, while strategic technology partnerships strengthen domestic deployment capabilities and long-term infrastructure competitiveness.

Huawei, Ciena, Nokia, Cisco, and Infinera compete for leadership in high-capacity optical transport, while regional manufacturers challenge primarily on pricing and localized deployment support. OEMs compete against network solution specialists through integrated hardware, software automation, and lifecycle service capabilities, whereas component suppliers differentiate through photonic innovation and coherent optical technology. The top five companies collectively control approximately 68% of global market activity, reflecting a concentrated technology-driven landscape. Competition increasingly depends on transmission performance, AI-enabled network management, supply-chain resilience, and interoperability, with programmable platforms reducing operating costs by nearly 20%, coherent optics improving spectral efficiency by around 40%, and deployment automation shortening provisioning time by approximately 35%. Companies are strengthening positions through manufacturing expansion, strategic cloud partnerships, silicon photonics investment, and vertical integration of optical components. Competitive momentum is shifting toward open optical networking and software-defined transport, increasing pressure on vendors with proprietary ecosystems. Success requires scalable innovation, resilient supply chains, rapid product commercialization, and seamless multi-vendor interoperability.

Huawei Technologies

Ciena Corporation

Nokia Corporation

Cisco Systems

Infinera Corporation

Fujitsu Limited

NEC Corporation

ZTE Corporation

ADVA Network Security

Juniper Networks

Ribbon Communications

Ekinops

Ericsson

Arista Networks

Current technology development is centered on coherent 400G and 800G optical transmission, AI-enabled network orchestration, and software-defined transport architectures. More than 60% of newly deployed backbone projects now incorporate programmable optical control, improving bandwidth utilization by approximately 30% while reducing manual provisioning effort by nearly 35%. Open optical interfaces are also accelerating interoperability between multi-vendor transport environments, enabling operators to modernize networks without replacing existing infrastructure. These capabilities are becoming essential for telecom operators, hyperscale cloud providers, and large enterprises managing high-capacity digital traffic.

Emerging technologies include silicon photonics, coherent pluggable optics, digital twins for optical network optimization, and AI-assisted predictive maintenance. Compared with legacy 100G transport systems, modern coherent 800G platforms deliver nearly 40% higher spectral efficiency while lowering energy consumption by approximately 20%. Vendors with vertically integrated photonic design and programmable networking software gain a stronger competitive position by delivering lower operational costs, faster deployment, and simplified lifecycle management across carrier and enterprise optical networks.

Between 2026 and 2028, intelligent automation, open networking ecosystems, and integrated optical software platforms will redefine procurement priorities. Adoption of AI-assisted transport management is expected to exceed 70% across new backbone deployments, enabling predictive capacity planning, automated fault isolation, and dynamic traffic optimization. Organizations investing early in programmable optical infrastructure, coherent transmission innovation, and cloud-integrated transport platforms will achieve superior operational resilience, improved service agility, and stronger competitive differentiation as digital infrastructure becomes increasingly bandwidth intensive.

March 2026 – Ciena unveiled AI-focused optical networking innovations including Hyper-Rail Photonics, 1600ZR/ZR+ pluggables, and full-spectrum coherent transponders delivering up to 32× higher fiber density while reducing power consumption by 75%, strengthening hyperscale AI data center connectivity. Source: ciena.com

March 2026 – Huawei introduced its Next Generation OTN portfolio for AI-centric optical networks, featuring intelligent performance optimization that extends transmission distance by 20% and AI-based energy management reducing average power consumption by 40%, enhancing operator network efficiency. Source: huawei.com

February 2025 – Nokia received European regulatory approval for its acquisition of Infinera, creating the world's second-largest optical networking supplier with an estimated 20% market share, expanding its competitive position in AI-driven optical transport infrastructure. Source: reuters.com

March 2024 – Nokia launched a metro-edge optical transport portfolio featuring 100G, 400G, and 800G coherent pluggables alongside compact transport platforms, enabling substantially lower power per bit while accelerating high-capacity edge network deployments for telecom and enterprise operators. Source: nokia.com

This report delivers comprehensive analysis of the Optical Transport Network (OTN) Equipment Market across OTN Switches, OTN Multiplexers, Optical Transponders, Optical Cross-Connects, and WDM Equipment. It evaluates deployment across Long-Haul Networks, Metro Networks, Data Centers, 5G Networks, and Cloud Connectivity, while assessing demand from Telecom Operators, Cloud Providers, Enterprises, Government organizations, and Data Center Operators. The study covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting deployment concentration, technology adoption, and competitive positioning across mature and emerging markets.

The report examines coherent optical transmission, programmable networking, AI-enabled network automation, software-defined transport, and silicon photonics, supported by operational indicators including deployment trends exceeding 60% for programmable optical platforms in new backbone projects. It provides strategic insights into competitive benchmarking, investment priorities, supply-chain evolution, technology roadmaps, partnership strategies, and expansion opportunities, enabling stakeholders to strengthen market positioning and make informed business decisions throughout the 2026–2033 planning horizon.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 18186.39 Million |

Market Revenue in 2033 | USD 26261.52 Million |

CAGR (2026 - 2033) | 4.7% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Huawei Technologies, Ciena Corporation, Nokia Corporation, Cisco Systems, Infinera Corporation, Fujitsu Limited, NEC Corporation, ZTE Corporation, ADVA Network Security, Juniper Networks, Ribbon Communications, Ekinops, Ericsson, Arista Networks |

Customization & Pricing | Available on Request (10% Customization is Free) |