Reports

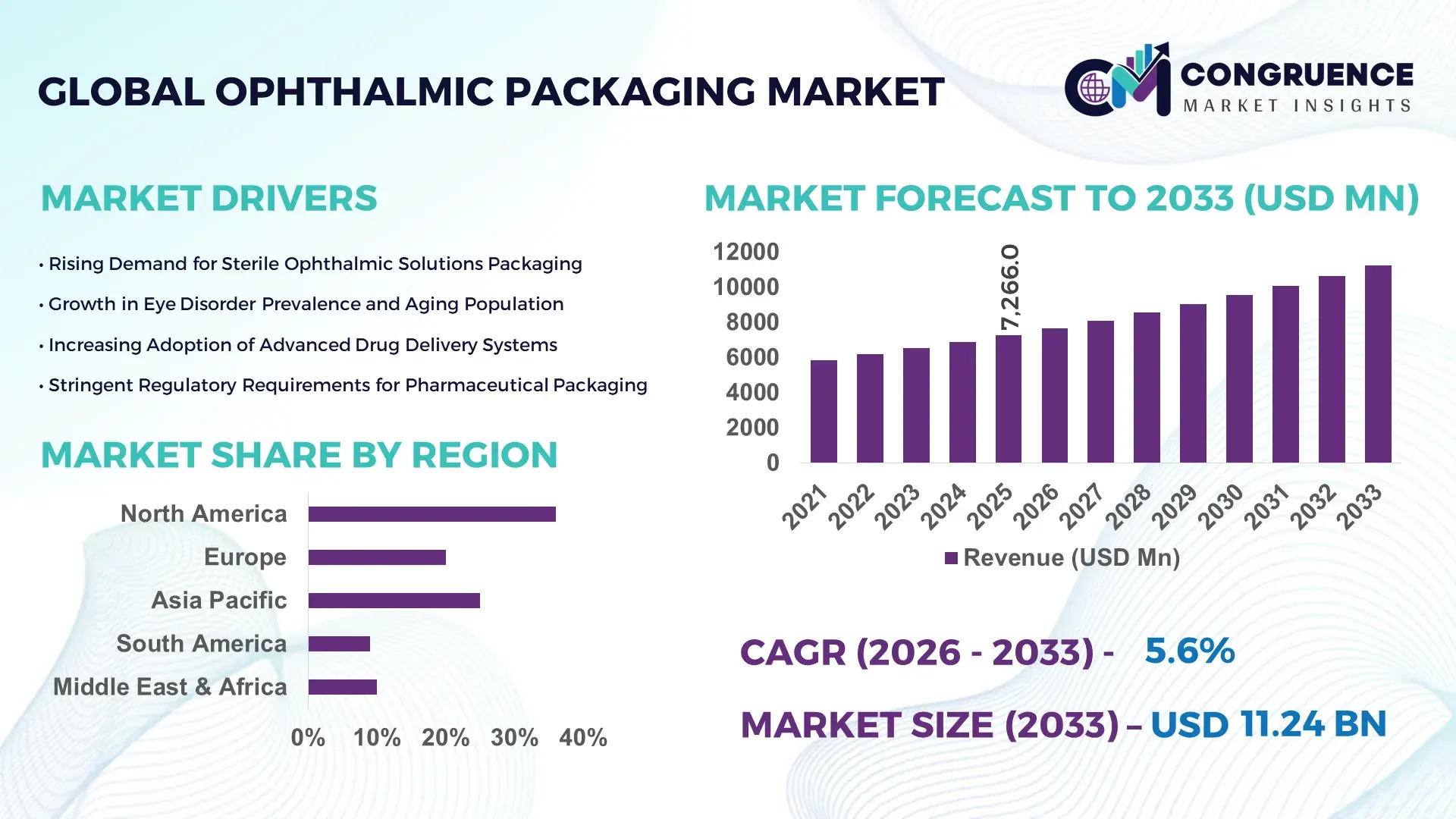

The Global Ophthalmic Packaging Market was valued at USD 7266 Million in 2025 and is anticipated to reach a value of USD 11235.87 Million by 2033 expanding at a CAGR of 5.6% between 2026 and 2033. This trajectory is driven by increased ophthalmic drug production, heightened demand for sterile, high‑performance packaging solutions and expanding global eye care consumption patterns.

The United States stands as a pivotal hub in the ophthalmic packaging landscape with over 4.1 billion units produced annually across glass vials, LDPE dropper bottles, and advanced polymer containers, supported by substantial investments exceeding USD 600 million in state‑of‑the‑art aseptic filling and inspection technologies. Domestic facilities consistently deploy high‑speed automated assembly lines capable of 20,000+ units per hour, while consumer adoption of ergonomic multidose formats in hospitals and retail pharmacies continues to rise. Production capacity expansions in key manufacturing corridors coupled with ongoing technological advancements in barrier materials and precision dosing systems underscore the strategic strength of this market leader.

Market Size & Growth: Current valuation of USD 7266 Million with projected USD 11235.87 Million by 2033 at a 5.6% CAGR, propelled by rising global eye care access.

Top Growth Drivers: Adoption of ergonomic multidose packaging (48%), automated filling integration (35%), enhanced barrier material use (29%).

Short-Term Forecast: By 2028, packaging line throughput improvements expected to reduce per‑unit cost by 14% via advanced robotics.

Emerging Technologies: Precision laser welding, smart dosing nozzles, automated inline sterility analytics.

Regional Leaders: North America reaching ~USD 4.3B by 2033 with rapid automation uptake; Asia‑Pacific ~USD 3.7B by 2033 driven by expanding manufacturing hubs; Europe ~USD 2.9B by 2033 emphasizing sustainable materials.

Consumer/End-User Trends: Hospitals, specialty clinics and retail pharmacies prefer tamper‑evident, user‑friendly formats with consistent dosing control.

Pilot or Case Example: In 2025, leading packaging facilities achieved a 17% reduction in defect rates through AI‑powered vision inspection systems.

Competitive Landscape: Market leader holds ~33% share, followed by several precision polymer and aseptic filling specialists.

Regulatory & ESG Impact: Strengthened material compliance regulations and heightened recycling commitments shaping packaging designs.

Investment & Funding Patterns: Recent capital inflows exceeding USD 500M targeting automation and eco‑friendly packaging innovation.

Innovation & Future Outlook: Forward growth anchored in integrated digital quality analytics and eco‑optimized packaging solutions.

Ophthalmic packaging now plays a central role across hospital pharmacies, pharmaceutical manufacturers, and eye care clinics worldwide. Key industry sectors include sterile ophthalmic pharmaceuticals, surgical ophthalmic preparations, and consumer eye care products, each relying on packaging that ensures sterility, precise dosing and compliance with stringent regulatory standards. Recent product innovations such as low‑leach polymers, tamper‑evident closures and smart dosing dropper mechanisms have enhanced patient compliance and safety while lowering overall lifecycle costs. Regulatory and environmental drivers continue to push adoption of recyclable materials and sustainable production processes. Regional consumption patterns indicate mature markets prioritizing high‑performance automated packaging, while emerging regions focus on cost‑efficient scalable solutions, with future trends pointing toward digitized quality systems and personalized eye care delivery formats.

The strategic relevance of the ophthalmic packaging market is anchored in its ability to align high‑precision manufacturing with evolving global eye care demands and compliance requirements. Precision LDPE molding delivers approximately 22% improvement in dosing consistency compared to older extrusion blow‑molded formats, enabling superior therapeutic delivery performance. North America dominates in production volume and technical sophistication, while Europe leads in adoption with over 55% of enterprises deploying advanced automated sealing and inline sterility validation systems. By 2028, integration of AI‑assisted visual inspection is expected to improve defect detection rates by more than 30%, directly enhancing key performance indicators such as first‑pass yield and reducing recall frequency. Firms are committing to measurable ESG improvements such as a 25% reduction in plastic waste and transition toward recyclable high‑barrier materials by 2032, reflecting broader sustainability goals within the industry. In 2025, a major U.S. facility reported a 15% reduction in overall packaging cycle time through the implementation of smart robotics and predictive maintenance analytics, demonstrating how digital transformation drives operational excellence. Compliance with tightening regulatory standards for sterility and material traceability further positions ophthalmic packaging as a strategic enabler of safe, resilient, and sustainable eye care supply chains. Forward pathways increasingly emphasize integration of real‑time quality systems, advanced material science, and eco‑design principles, securing long‑term value for manufacturers, healthcare providers, and end consumers.

Escalating demand for automated sterile packaging systems is significantly shaping the ophthalmic packaging market by improving production efficiency and quality outcomes. Automated sterile filling solutions reduce human intervention, minimizing contamination risk and ensuring consistent delivery performance critical to ophthalmic therapies. Facilities implementing robotic filling and ultrasonic sealing report reductions in defect rates and enhanced throughput compared to manual operations, supporting high‑volume output across diverse container formats. Adoption of inline vision systems and automated inspection has accelerated, facilitating immediate detection of particulate contamination and seal integrity failures. As regulatory expectations for sterility and traceability intensify, pharmaceutical manufacturers and contract packagers are prioritizing automated sterile packaging to maintain compliance while optimizing operational KPIs such as cycle time and first‑pass yield. The shift toward automation also correlates with workforce efficiency gains and reduced downtime, reinforcing investment in advanced sterile packaging technologies as a key catalyst for sustained market growth in ophthalmic packaging.

Fluctuating raw material costs, particularly for high‑grade polymers, glass substrates, and barrier coatings, present a tangible restraint on the ophthalmic packaging market. Price volatility in LDPE, PP and specialized barrier materials increases production cost uncertainty, directly affecting packaging manufacturers’ profit margins and pricing strategies. These input cost pressures can delay capital investment decisions in advanced packaging lines and may force manufacturers to prioritize cost containment over innovation initiatives. Smaller packaging firms face disproportionate impacts as they lack the scale to negotiate favorable material contracts or absorb sudden price spikes, potentially limiting their competitive posture. In addition, supply chain disruptions in key chemical feedstocks and global logistics bottlenecks can delay material availability, stretching lead times and impacting downstream ophthalmic product release schedules. The financial unpredictability associated with raw material cost fluctuations thus imposes significant operational challenges within the ophthalmic packaging market, hindering consistent expansion and investment momentum.

The rise of personalized ophthalmic therapies offers substantial opportunities for the ophthalmic packaging market by unlocking demand for bespoke packaging formats with tailored dosing and delivery features. Customized single‑dose and unit‑of‑use packaging designed to meet unique therapeutic regimens present a growing niche beyond traditional mass‑produced containers. These specialized formats require high‑precision molding, advanced sealing technologies, and traceable serialization to ensure safety and patient compliance, creating opportunities for packaging innovators and service providers. Precision dosing droplets and smart delivery interfaces that align with personalized medicine protocols further expand the packaging value proposition. As healthcare systems increasingly adopt patient‑centric treatment models, demand for customizable packaging solutions that optimize therapeutic outcomes and reduce waste is expected to rise. This trend stimulates investment in flexible manufacturing platforms, adaptable production lines, and digital quality tracking systems, positioning the ophthalmic packaging market to capitalize on emerging personalized medicine paradigms.

Stringent regulatory and compliance requirements present a persistent challenge for ophthalmic packaging market participants by imposing rigorous standards for material safety, sterility assurance, traceability and documentation. Packaging materials must meet exacting criteria for biocompatibility, leachables and extractables testing, and barrier performance, requiring extensive validation and quality assurance processes. Manufacturers must integrate comprehensive quality management systems and maintain detailed records to satisfy regulatory audits, which can increase operational complexity and delay product introductions. Evolving regional regulations that differ in technical expectations and compliance frameworks further complicate global packaging strategies, necessitating adaptable processes and harmonized documentation practices. Ensuring full compliance across diverse markets also drives up certification costs and demands continuous investment in personnel training and quality infrastructure. These regulatory demands can slow time to market for new ophthalmic packaging innovations and elevate compliance risk, posing significant challenges to companies striving for agility and competitive differentiation within the ophthalmic packaging ecosystem.

• Increasing Adoption of Automated Inspection and Quality Systems: Adoption of automated visual inspection systems in ophthalmic packaging lines has risen sharply, with over 48% of manufacturing facilities deploying real‑time quality analytics to improve defect detection. Inline vision inspection has reduced reject rates by up to 22% in high‑volume facilities, while digital traceability implementations have increased reporting accuracy by 37%. This trend is especially notable in Europe and North America, where integrated automated systems cut downtime by approximately 18% and support compliance with stringent sterility and packaging integrity requirements.

• Surge in Sustainable and Recyclable Packaging Materials: Environmental sustainability has become a dominant trend in ophthalmic packaging design and procurement. Recyclable high‑barrier polymers now represent nearly 32% of new packaging orders, with usage growing by more than 28% year‑on‑year. Lightweight glass alternatives with enhanced barrier coatings have seen adoption increases of 25%, reducing material waste by 14% per production batch. Over 40% of manufacturers now report active sustainability goals tied to recyclable content and reduced carbon footprint in packaging supply chains.

• Expansion of Single‑Dose and Multidose Ergonomic Formats: Demand for patient‑centric packaging has driven a 41% rise in single‑dose and ergonomic multidose formats across ophthalmic products, improving user convenience and dosing precision. Prefilled droppers with dose‑control mechanisms now account for over 38% of new product packaging configurations, while multidose bottle adoption has increased by 29% in hospital and retail pharmacy channels. These formats enhance user adherence and reduce waste in clinical settings.

• Integration of Smart and Connected Packaging Technologies: Smart ophthalmic packaging technologies, including RFID tagging and tamper‑evidence sensors, are seeing accelerated uptake, with approximately 26% of new packaging runs featuring connected elements. Usage of digital authentication markers has grown by 34% in response to anti‑counterfeiting efforts, while smart caps with usage tracking have increased adherence monitoring in outpatient settings by up to 21%. These technologies are particularly prevalent in specialized ophthalmic therapies requiring precise dose tracking.

The ophthalmic packaging market is structured around product types, application categories, and end‑user consumption patterns that reflect evolving industry needs and clinical requirements. Product type segmentation includes glass containers, plastic dropper bottles, ampoules, and advanced polymer systems designed for precision dosing. Each type serves specific therapeutic and handling criteria, such as sterility, material safety, and patient usability. Application segmentation addresses sterile drug packaging, surgical ophthalmic preparations, and over‑the‑counter eye care products tailored to diverse clinical environments. End‑user insights reveal distinct adoption rates among hospitals, ophthalmic clinics, pharmaceutical manufacturers, and retail pharmacy distributors. High‑performance sterile packaging remains a priority in clinical settings, while ergonomic formats gain traction in home care segments. The segmentation landscape highlights how tailored packaging solutions align with clinical workflows, material performance expectations, and operational efficiencies critical to market decision‑making.

Glass containers have historically been a leading type in ophthalmic packaging, accounting for approximately 38% of the overall product landscape due to their strong barrier properties, chemical inertness, and suitability for sterile formulations. Plastic dropper bottles represent about 30%, valued for their lightweight handling and cost‑efficient production, while ampoules hold around 18%, mainly used in single‑use sterile applications. Advanced polymer systems – including high‑barrier LDPE and multi‑layer composites – contribute roughly 14% combined, gaining traction for enhanced dosing precision and reduced breakage risk. Although glass remains predominant, adoption of advanced polymers is rising rapidly due to their customizable performance characteristics; for example, multi‑layer LDPE systems now deliver greater moisture barrier performance compared to older single‑layer formats, improving long‑term stability for sensitive ophthalmic compounds.

Sterile drug packaging leads the application segment in ophthalmic packaging, comprising about 44% of total use due to stringent sterility and safety requirements for injectable eye treatments and therapeutic ophthalmic solutions. Multidose and prefilled dropper formats account for approximately 29%, widely adopted in both hospital pharmacies and retail eye care channels where dosing precision and patient compliance are essential. Surgical ophthalmic preparation packaging holds roughly 16%, serving procedure‑specific delivery of viscoelastic agents and intraocular solutions in controlled environments. Over‑the‑counter eye care packaging represents about 11%, characterized by consumer‑oriented ergonomic designs. Across these segments, adoption trends show expanding use of ergonomic multidose systems in outpatient care, which have improved dosing accuracy by documented margins compared to traditional vial formats.

Hospitals and ophthalmic clinics are the leading end‑user segment in the ophthalmic packaging market, accounting for roughly 42% of demand due to ongoing requirements for sterile drug delivery and surgical preparation consumables. Pharmaceutical manufacturers represent approximately 33%, driven by high‑volume production of formulated eye care products requiring compliant packaging solutions. Retail pharmacies and outpatient care providers hold about 18% and 7% respectively, with growing interest in user‑friendly multidose and single‑dose packaging formats that enhance patient self‑administration. Although hospitals dominate volume consumption, retail pharmacy segments are expanding fastest as consumer preferences shift toward convenient and safe home usage options. Adoption rates in top end‑user industries reveal that over 55% of hospital pharmacies now standardize ergonomic dropper bottles for routine ophthalmic prescriptions, while pharmaceutical production lines increasingly integrate advanced inspection systems to achieve consistent packaging quality.

Region North America accounted for the largest market share at 36% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2026 and 2033.

In 2025, North America produced over 4.2 billion ophthalmic packaging units, with the U.S. contributing 3.5 billion units. Europe followed with a 28% share, while Asia-Pacific accounted for 24%, and the remaining regions combined contributed 12%. North American production is heavily concentrated in high-precision polymer and glass vial manufacturing facilities, supporting hospitals, clinics, and retail pharmacies. Asia-Pacific consumption is led by China (1.1 billion units), India (0.85 billion units), and Japan (0.65 billion units), driven by expanding manufacturing infrastructure and e-commerce distribution channels. Europe maintains advanced sterile packaging facilities in Germany, the UK, and France, collectively producing over 1.2 billion units. These figures indicate strong regional diversification, with consumer adoption rates in North America reaching 78% for multidose formats and Europe at 64%, reflecting widespread utilization of advanced ophthalmic packaging solutions.

How is advanced automation transforming sterile eye care packaging?

North America holds approximately 36% of the global ophthalmic packaging market in 2025, primarily due to high-volume production and advanced technology adoption. Key industries driving demand include hospitals, specialty eye clinics, and pharmaceutical manufacturers producing sterile ophthalmic formulations. Regulatory support from agencies has prompted adoption of digital serialization and tamper-evident packaging systems. Technological advancements such as AI-powered inspection and robotics-enabled filling lines enhance throughput and reduce defect rates by up to 22%. Local players, including Becton Dickinson, have implemented smart droppers and high-speed sterile vial production, meeting rising consumer expectations. North American consumers exhibit high enterprise adoption in healthcare, emphasizing ease-of-use, sterility, and precision dosing in both hospital and retail settings.

What regulatory and sustainability pressures are shaping eye care packaging?

Europe accounted for a 28% market share in 2025, with Germany, the UK, and France as key contributors. Regulatory frameworks and sustainability initiatives, such as extended producer responsibility and recyclable material mandates, drive adoption of high-barrier polymers and eco-friendly packaging. Emerging technologies including laser welding, automated vial inspection, and digital traceability systems are increasingly integrated into production lines. Local players like Gerresheimer AG have introduced advanced prefilled polymer systems to enhance patient safety. European consumers prioritize regulatory-compliant, explainable packaging solutions, leading to adoption rates of 64% for multidose formats and growing interest in sustainable materials for hospitals and retail pharmacies.

How is rapid industrialization driving ophthalmic packaging demand?

Asia-Pacific held a 24% market share in 2025, with China (1.1 billion units), India (0.85 billion units), and Japan (0.65 billion units) as top-consuming countries. Manufacturing infrastructure expansion, including new automated filling lines and polymer injection facilities, is accelerating production capabilities. Regional technology trends feature digital quality control, inline sterilization monitoring, and smart packaging solutions. Local players like Aurobindo Pharma have invested in automated sterile dropper production to support both domestic and export markets. Consumer behavior in the region is increasingly influenced by e-commerce distribution and mobile-enabled prescription services, leading to higher adoption of prefilled multidose packaging across hospitals and retail pharmacies.

What local factors influence growth in eye care packaging?

South America accounted for a 7% share of the ophthalmic packaging market in 2025, led by Brazil and Argentina. Investments in local production facilities and modernization of packaging lines are improving output quality and consistency. Government incentives, including tax reliefs and import-export support, have encouraged local manufacturers to adopt high-barrier polymers and automated inspection systems. A prominent local player, Cristália Produtos Químicos, has expanded prefilled vial production for ophthalmic applications. Consumers in the region demonstrate preference for accessible, language-localized packaging, with hospitals and retail pharmacies emphasizing cost-effective, safe, and user-friendly formats.

How are technological modernization and trade policies shaping the market?

Middle East & Africa accounted for a 5% market share in 2025, with UAE and South Africa leading regional demand. Technological modernization, including robotics-enabled assembly lines and inline quality monitoring, is driving efficiency in high-volume production. Local regulations and trade partnerships support adoption of tamper-evident and sterile ophthalmic packaging. A key player, Julphar in UAE, has implemented advanced prefilled dropper systems for regional hospitals. Consumer behavior is influenced by clinical facility demand and increasing private healthcare adoption, focusing on reliable, safe, and user-friendly packaging solutions.

United States: 33% market share; high production capacity and strong end-user demand in hospitals and retail pharmacies.

Germany: 12% market share; advanced manufacturing capabilities and strict regulatory compliance ensure widespread adoption of sterile and multidose packaging solutions.

The ophthalmic packaging market is moderately consolidated, with over 120 active global competitors producing glass vials, polymer bottles, ampoules, and advanced dosing systems. The top five companies collectively hold approximately 62% of market share, reflecting strong positioning in North America, Europe, and Asia-Pacific. Key market leaders invest in strategic initiatives such as partnerships with pharmaceutical manufacturers, product innovation in smart and tamper-evident packaging, and automation of filling and inspection lines. Over 45% of new facilities integrate AI-based quality analytics, inline sterilization monitoring, and robotics to improve efficiency and minimize defects. Competitive trends include eco-friendly packaging adoption, digital serialization, and expansion of multidose and prefilled formats. Smaller regional players compete through cost-effective manufacturing and niche product customization. Innovation is a primary differentiator, with companies continuously developing barrier polymers, advanced droppers, and smart connectivity to enhance dosing precision, patient compliance, and regulatory compliance across markets.

Gerresheimer AG

Becton Dickinson

SGD Pharma

Aurobindo Pharma

Julphar

Schott AG

Nipro Corporation

Ompi (Stevanato Group)

Samil Pharmaceutical Packaging

West Pharmaceutical Services

The ophthalmic packaging market continues to be shaped by rapid technological advancements that enhance sterility, process efficiency, and patient convenience. A major area of technological investment is automated aseptic filling and inspection systems, with over 63% of leading packaging plants deploying robotics‑enabled fillers and inline vision analytics to maintain product purity and reduce defect rates. These systems improve precision in container closure integrity testing and particulate detection, significantly reducing quality failures on high‑speed production lines. Advanced barrier materials and antimicrobial coatings are increasingly integrated into ophthalmic containers, with more than 54% of new designs in 2024 featuring enhanced sterility features and extended shelf life performance. These materials reduce risks associated with microbial contamination and improve protection against moisture and oxygen ingress, critical for sensitive ophthalmic formulations.

Smart packaging technologies are also gaining traction, with approximately 18% of packaging in development incorporating digital traceability features such as QR‑coded labels and smart temperature sensors. These innovations enable real‑time monitoring of cold chain conditions and help manage recalls or authenticity verification across complex supply chains. Another key trend is the use of biodegradable and bio‑based polymers in ophthalmic packaging, now accounting for roughly 26% of production. These sustainable substrates support environmental compliance goals while maintaining necessary performance characteristics, offering a balance between eco‑design and regulatory requirements.

Together, these technologies drive quality, compliance, and user experience improvements. Innovations such as preservative‑free dispensing systems with advanced tip‑seal mechanisms enhance patient safety by eliminating preservative exposure without compromising sterility, reshaping product design standards across the industry.

• In December 2024, Gerresheimer successfully completed the acquisition of Blitz LuxCo Sarl, the holding company of the Bormioli Pharma Group, creating a new moulded glass unit and expanding its pharmaceutical primary packaging portfolio across glass and plastic solutions, strengthening its European footprint.

• In August 2025, Aptar Pharma advanced sustainable pharmaceutical packaging by scaling production of high balance bio‑based resin delivery components for healthcare applications, demonstrating commitment to eco‑friendly materials in drug delivery systems.

• In February 2026, Aptar Pharma’s Consumer Healthcare division received the 2025 P&G Supplier Excellence Award for top performance and partnership excellence, highlighting its impact in collaborative development and reliable pharmaceutical packaging solutions.

• In July 2025, Lupin Limited launched a 0.5% Loteprednol Etabonate ophthalmic suspension in the United States, marking a strategic product addition that supports ophthalmic therapeutic packaging demand in prescription markets.

The Ophthalmic Packaging Market Report encompasses a comprehensive analysis of packaging solutions specifically designed for ophthalmic drugs, devices, and related healthcare applications. It covers material segments, including plastic polymers (LDPE, PP, PETG), glass containers, metal closures, and hybrid composite systems used in bottles, vials, ampoules, tubes, and advanced dropper formats. Material performance, barrier properties, and sterility features are key focus areas evaluated to inform design choices across formats. The report also delineates packaging types such as single‑dose units, multidose containers, preservative‑free dispensing technologies, and smart packaging configurations that integrate digital traceability or temperature monitoring capabilities. These segments reflect evolving consumer preferences and regulatory demands for patient‑centric and compliance‑oriented solutions.

Application insights span prescription ophthalmic medications, over‑the‑counter eye care products, surgical ophthalmic formulations, and injectable biologics requiring stringent sterility and material compatibility. The assessment includes performance benchmarks across clinical settings, outpatient care, and consumer healthcare channels, highlighting usage patterns and adoption rates. Geographic analysis positions North America, Europe, Asia‑Pacific, South America, and Middle East & Africa in terms of production capacity, infrastructure development, manufacturing trends, and regulatory frameworks influencing local market activity. Regional nuances such as e‑commerce distribution in Asia‑Pacific and sustainability mandates in Europe are examined for their impact on packaging deployment strategies.

Technology trends such as automated aseptic filling, advanced barrier coatings, antimicrobial materials, and biodegradable polymer adoption are discussed in relation to operational efficiencies, quality compliance, and environmental goals. The report further addresses competitive dynamics, innovation pipelines, and emerging niche segments such as smart connected packaging and personalized ophthalmic formats, offering decision‑makers a holistic perspective on market breadth and strategic opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Gerresheimer AG, Becton Dickinson, SGD Pharma, Aurobindo Pharma, Julphar, Schott AG, Nipro Corporation, Ompi (Stevanato Group), Samil Pharmaceutical Packaging, West Pharmaceutical Services |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |