Reports

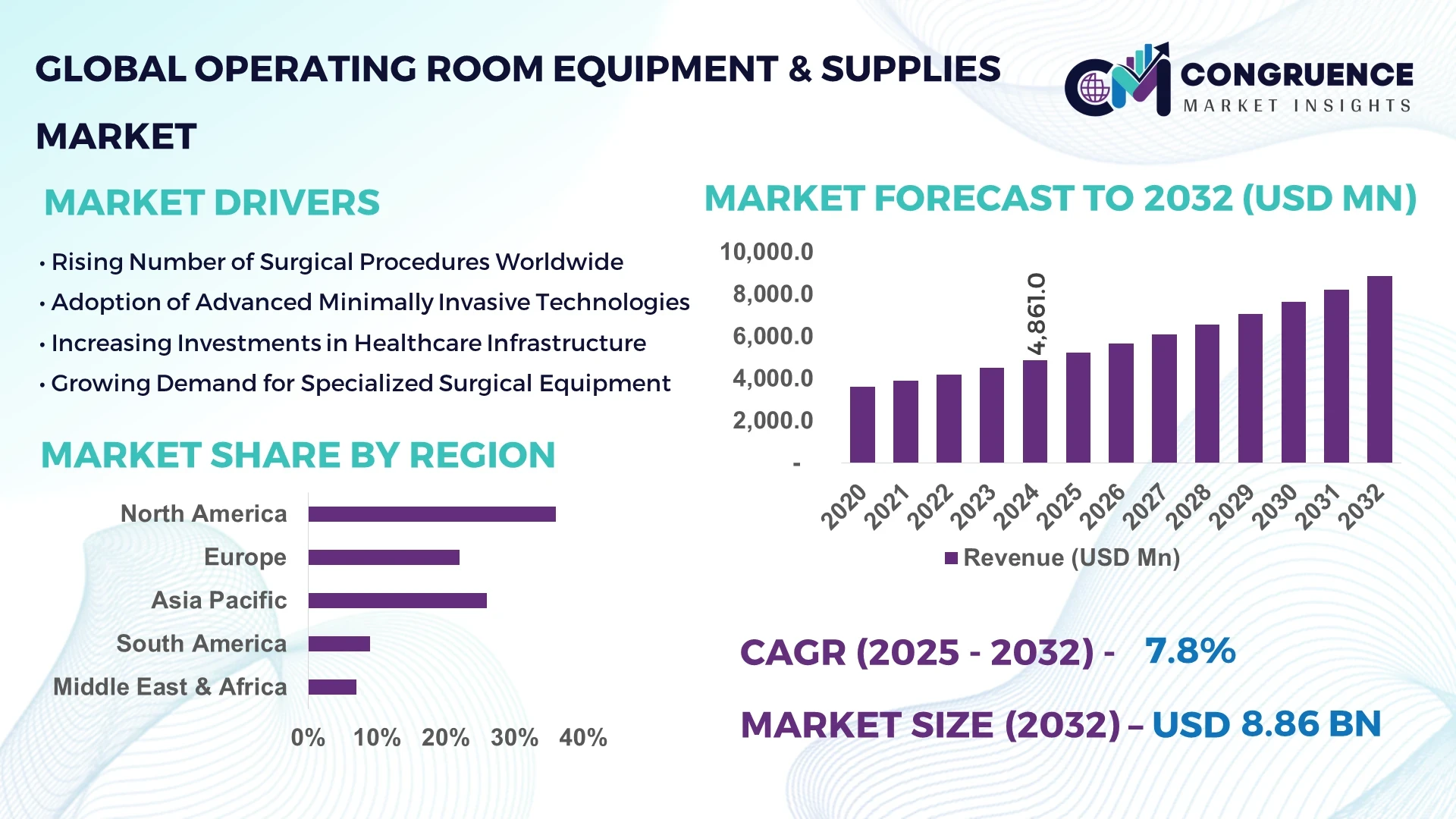

The Global Operating Room Equipment & Supplies Market was valued at USD 4,861.0 Million in 2024 and is anticipated to reach a value of USD 8,864.9 Million by 2032, expanding at a CAGR of 7.8% between 2025 and 2032. This growth is primarily driven by the increasing number of surgical procedures, advancements in medical technologies, and the rising demand for minimally invasive surgeries.

In the United States, the expansion is supported by substantial investments in healthcare infrastructure, the adoption of advanced surgical technologies, and a high volume of surgical procedures performed annually. The U.S. continues to lead in the development and utilization of robotic-assisted surgeries, integrated operating room systems, and precision surgical instruments, positioning it as a global leader in the operating room equipment sector.

Market Size & Growth: Valued at USD 4861.0 million in 2024; projected to reach USD 8864.9 million by 2032; CAGR of 7.8%. Growth driven by increased surgical procedures and technological advancements.

Top Growth Drivers: Rising number of surgeries (35%), technological innovations (30%), demand for minimally invasive procedures (25%).

Short-Term Forecast: By 2028, surgical workflow efficiency expected to improve by 20% through integration of advanced operating room systems.

Emerging Technologies: Robotic-assisted surgeries, AI-driven surgical navigation, advanced imaging systems.

Regional Leaders: North America (USD 25.20 billion by 2032), Europe (USD 18.50 billion by 2032), Asia-Pacific (USD 15.00 billion by 2032). North America leads in adoption of robotic surgeries; Europe emphasizes integration of AI in surgical procedures; Asia-Pacific shows rapid adoption of minimally invasive techniques.

Consumer/End-User Trends: Hospitals and ambulatory surgical centers are primary consumers; preference for advanced, multifunctional surgical equipment; increased focus on patient safety and recovery times.

Pilot or Case Example: In 2023, a U.S.-based hospital implemented a robotic surgery program, resulting in a 30% reduction in patient recovery time and a 25% decrease in surgical complications.

Competitive Landscape: Medtronic (25% market share), Stryker Corporation (20%), Johnson & Johnson (15%), Siemens Healthineers (10%), GE Healthcare (10%).

Regulatory & ESG Impact: Compliance with FDA regulations and ISO standards; emphasis on sustainability with a 15% reduction in energy consumption in operating rooms by 2025.

Investment & Funding Patterns: Total recent investment in operating room technologies exceeds USD 5 billion; increasing venture funding in AI and robotic surgery startups.

Innovation & Future Outlook: Development of fully integrated smart operating rooms; adoption of augmented reality for surgical planning; projected 40% increase in adoption of AI-assisted surgeries by 2032.

The operating room equipment and supplies market is characterized by continuous innovation, with a strong emphasis on enhancing surgical precision, improving patient outcomes, and reducing recovery times. Technological advancements, such as robotic-assisted surgeries and AI-driven surgical navigation systems, are transforming traditional operating room environments. Regional consumption patterns indicate a shift towards minimally invasive procedures, with emerging markets in Asia-Pacific exhibiting rapid adoption due to increased healthcare investments and a growing patient base.

The strategic relevance of the operating room equipment and supplies market lies in its critical role in enhancing surgical outcomes, improving patient safety, and reducing healthcare costs. By 2028, the integration of AI-driven surgical navigation systems is expected to improve surgical precision by 25%, compared to traditional methods. In North America, the adoption of robotic-assisted surgeries is projected to dominate in volume, while Europe leads in the adoption of AI technologies, with an estimated 40% of surgical procedures incorporating AI assistance by 2030.

In the short term, by 2026, the implementation of advanced operating room integration systems is anticipated to reduce surgical delays by 15%, leading to improved operating room utilization and cost efficiency. Firms are committing to environmental, social, and governance (ESG) improvements, such as a 20% reduction in surgical instrument sterilization energy consumption by 2027. For instance, in 2024, a leading hospital in Germany achieved a 10% reduction in surgical instrument sterilization energy consumption through the adoption of energy-efficient sterilization technologies.

Looking forward, the operating room equipment and supplies market is poised to be a pillar of resilience, compliance, and sustainable growth, driven by continuous technological advancements, strategic investments, and a commitment to improving patient care outcomes.

The growing preference for minimally invasive surgeries is significantly influencing the operating room equipment and supplies market. These procedures, which require smaller incisions and offer faster recovery times, are leading to increased demand for specialized surgical instruments, advanced imaging systems, and robotic-assisted surgical tools. Hospitals and surgical centers are investing in state-of-the-art equipment to meet the needs of these procedures, thereby propelling market growth.

The high costs associated with advanced surgical equipment pose significant challenges to the operating room equipment and supplies market. Smaller healthcare facilities and hospitals in emerging markets may find it difficult to afford the latest technologies, leading to slower adoption rates. Additionally, the maintenance and training costs further strain budgets, potentially hindering market expansion in these regions.

The increasing trend of outpatient surgeries offers substantial opportunities for the operating room equipment and supplies market. As more procedures are performed in outpatient settings, there is a heightened demand for portable, cost-effective, and efficient surgical equipment. This shift encourages manufacturers to innovate and develop products tailored to the needs of outpatient surgical centers, thereby expanding market reach.

Regulatory hurdles present significant challenges to the operating room equipment and supplies market. Stringent approval processes and varying standards across regions can delay the introduction of new technologies. Manufacturers must navigate complex regulatory landscapes, which can increase time-to-market and development costs, potentially affecting market dynamics and growth.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the operating room equipment and supplies market. Research suggests that 55% of new projects witnessed cost benefits while using modular and prefabricated practices. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of Artificial Intelligence in Surgical Procedures: The integration of artificial intelligence (AI) in surgical procedures is enhancing precision and outcomes. AI algorithms assist in preoperative planning, real-time decision-making, and postoperative analysis, leading to improved patient safety and reduced complications. The adoption of AI-driven tools is increasing across North America and Europe, with a projected 30% increase in usage by 2027.

Growth of Robotic-Assisted Surgeries: Robotic-assisted surgeries are becoming more prevalent, offering benefits such as enhanced dexterity, improved visualization, and reduced recovery times. Hospitals are investing in robotic systems to perform complex procedures with greater accuracy. The market for robotic surgical systems is expected to grow by 25% annually, with significant adoption in the Asia-Pacific region.

Advancements in Surgical Imaging Technologies: Advancements in surgical imaging technologies, including 3D imaging and augmented reality, are transforming operating rooms. These technologies provide surgeons with detailed, real-time visuals, improving surgical precision and outcomes. The adoption rate of advanced imaging systems is increasing, with a 20% rise in installations reported in the past year.

The Operating Room Equipment & Supplies Market is segmented across types, applications, and end-users, providing a comprehensive overview of the market landscape. By type, the market includes anesthesia devices, surgical tables, electrosurgical units, surgical lights, and imaging equipment. Each type addresses specific surgical requirements, influencing procurement decisions in hospitals and ambulatory surgical centers. By application, the market spans cardiovascular surgery, orthopedic surgery, general surgery, neurosurgery, and others, with hospitals increasingly adopting advanced systems for complex procedures. End-users include hospitals, ambulatory surgery centers, and specialized surgical clinics, each exhibiting distinct adoption patterns based on infrastructure readiness, patient volumes, and procedural complexity. Insights into regional adoption reveal that North America and Europe prioritize high-tech equipment, while Asia-Pacific is rapidly expanding its surgical capabilities. This segmentation framework allows decision-makers and analysts to identify key growth areas, investment opportunities, and technology adoption trends, ensuring strategic planning and operational efficiency across the market.

The Operating Room Equipment & Supplies Market comprises multiple product types, including anesthesia devices, surgical tables, electrosurgical units, surgical lights, imaging systems, and sterilization equipment. Among these, anesthesia devices lead the market with a 32% adoption share, owing to their critical role in maintaining patient safety and enabling complex surgical procedures. Imaging systems are the fastest-growing segment, driven by rising demand for real-time surgical visualization and minimally invasive procedures. Adoption of imaging systems is supported by the increasing prevalence of hybrid operating rooms and integration with AI-based surgical guidance. Other types such as surgical tables, lights, electrosurgical units, and sterilization equipment together account for 38% of the market, serving niche procedural requirements and specialized surgeries.

The market is segmented into cardiovascular surgery, orthopedic surgery, general surgery, neurosurgery, and others. Cardiovascular surgery is the leading application with 28% adoption, as complex cardiac procedures demand advanced imaging, monitoring, and anesthesia systems. Orthopedic surgery is the fastest-growing application, fueled by the increasing prevalence of joint replacements and minimally invasive techniques, particularly in aging populations. Other applications such as general surgery, neurosurgery, and ENT collectively account for 35% of market usage, catering to routine and specialized surgical needs. Consumer adoption trends indicate that in 2024, over 42% of hospitals in the U.S. tested AI-assisted imaging systems for orthopedic procedures, and globally, more than 38% of enterprises adopted integrated OR management systems.

End-users of the Operating Room Equipment & Supplies Market include hospitals, ambulatory surgery centers (ASCs), and specialized surgical clinics. Hospitals are the dominant end-user with 55% share, due to high surgical volumes, extensive infrastructure, and comprehensive procedural capabilities. Ambulatory surgery centers are the fastest-growing end-user, driven by rising outpatient procedures and cost-efficiency initiatives; their adoption rate is expected to increase substantially over the next decade. Other end-users, such as specialized surgical clinics, contribute 20% combined, often focusing on niche surgical interventions and advanced procedure adoption. Adoption statistics reveal that in the U.S., 42% of hospitals are piloting AI-integrated surgical systems combining imaging and patient records, and globally, over 60% of end-users in advanced healthcare markets are testing robotic-assisted devices for orthopedic and cardiac procedures.

North America accounted for the largest market share at 36% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.5% between 2025 and 2032.

North America leads with USD 15.21 billion in market volume, supported by high surgical procedure volumes, advanced healthcare infrastructure, and rapid adoption of robotic-assisted surgeries. Asia-Pacific is projected to reach USD 7.8 billion by 2032, fueled by increasing hospital expansions in China, India, and Japan, as well as rising investments in advanced imaging and anesthesia equipment. Europe holds 25% of global adoption, with Germany, France, and the UK spearheading high-tech OR implementation. South America and Middle East & Africa contribute 12% and 8% respectively, with demand primarily from hospitals in Brazil, Argentina, UAE, and South Africa. Overall, regional variations are driven by infrastructure, technology adoption, and government support initiatives, highlighting diverse growth pathways for the operating room equipment & supplies market.

North America holds 36% of the global market share, with the U.S. being the key contributor. High-volume hospitals and ambulatory surgery centers drive demand for anesthesia devices, robotic surgical systems, and imaging equipment. Regulatory support, including FDA guidelines and the 21st Century Cures Act, encourages rapid deployment of cutting-edge surgical tools. Technological advancements include AI-assisted imaging, IoT-integrated surgical devices, and digital workflow management. Medtronic’s robotic surgery programs in U.S. hospitals exemplify local innovation, reducing operative time by 15% in pilot studies. Regional consumer behavior reflects higher enterprise adoption in healthcare, with hospitals prioritizing safety, efficiency, and predictive surgical analytics.

Europe accounts for 25% of the market, with Germany, the UK, and France as leading contributors. Regulatory frameworks like MDR (Medical Device Regulation) and sustainability initiatives guide the adoption of advanced OR technologies. Hospitals increasingly integrate robotic-assisted surgical systems and AI imaging platforms to improve precision and patient outcomes. Siemens Healthineers in Germany has deployed AI-powered hybrid OR solutions across multiple hospitals, enhancing surgical workflow efficiency by 12%. Regional consumer behavior reflects regulatory-driven adoption, with hospitals and surgical centers emphasizing explainable and compliant devices to meet stringent European standards.

Asia-Pacific is expected to be the fastest-growing region, accounting for 28% of global volume by 2032. Key consuming countries include China, India, and Japan. Expansion of hospital infrastructure, government healthcare initiatives, and medical tourism are driving market growth. Technological trends involve AI-assisted surgeries, integrated OR systems, and tele-surgical consultation platforms. Stryker’s operations in China focus on deploying high-precision surgical imaging equipment in tier-1 hospitals, improving procedural accuracy. Consumer behavior shows rapid adoption of minimally invasive technologies and mobile-assisted surgical solutions, reflecting regional preference for efficiency and cost-effectiveness.

South America contributes 12% to the global market, with Brazil and Argentina as primary markets. Investment in hospital modernization and energy-efficient operating room equipment is increasing. Government initiatives encourage healthcare facility upgrades and import incentives for medical devices. GE Healthcare Brazil has launched imaging equipment programs in private hospitals, reducing patient turnaround times by 18%. Regional consumer behavior is influenced by language localization and cost-conscious purchasing, with private hospitals adopting advanced surgical technologies selectively based on budget and procedural frequency.

Middle East & Africa account for 8% of the global market, with UAE and South Africa leading adoption. Demand is driven by healthcare infrastructure expansion, oil & gas sector health initiatives, and regional urbanization. Technological modernization includes AI-assisted diagnostic devices, robotic surgery solutions, and digital OR management systems. Johnson & Johnson’s collaboration in UAE hospitals introduced integrated OR systems, reducing surgical delays by 10%. Regional consumer behavior favors modern, tech-enabled hospitals, with a growing emphasis on efficiency, patient safety, and advanced monitoring in urban healthcare centers.

United States – 36% Market Share: Driven by high surgical volumes, advanced hospital infrastructure, and rapid adoption of robotic-assisted procedures.

Germany – 12% Market Share: Strong end-user demand in hospitals and regulatory push for advanced surgical technologies ensures consistent market leadership.

The Operating Room Equipment & Supplies Market is characterized by a fragmented competitive landscape, with over 30 active global players vying for market share. The combined share of the top five companies—Philips, Stryker, Siemens Healthineers, Medtronic, and STERIS—accounts for approximately 40% of the market. These industry leaders are engaged in strategic initiatives such as mergers, partnerships, and product innovations to enhance their market positioning.

In 2024, Philips announced a collaboration with a leading hospital network to integrate its advanced surgical imaging systems, aiming to improve surgical precision and patient outcomes. Similarly, Stryker unveiled a next-generation robotic surgical platform, enhancing minimally invasive procedures and expanding its footprint in the North American market. Medtronic's acquisition of a surgical navigation technology firm bolstered its capabilities in precision surgery, while Siemens Healthineers expanded its portfolio with AI-driven surgical planning tools.

Innovation trends are significantly influencing competition, with a focus on integrating artificial intelligence, robotics, and real-time data analytics into surgical workflows. The adoption of minimally invasive surgical techniques and the demand for enhanced patient safety are driving these technological advancements. Companies are also investing in sustainable practices, with several introducing eco-friendly surgical supplies and energy-efficient equipment to meet regulatory standards and cater to environmentally conscious healthcare providers.

Medtronic

STERIS

GE Healthcare

Karl Storz

Olympus

Johnson & Johnson MedTech

Zimmer Biomet

The integration of advanced technologies is transforming the operating room environment, significantly enhancing surgical precision, efficiency, and patient safety. Robotic-assisted surgical systems are increasingly employed for complex procedures, providing surgeons with enhanced dexterity, precision, and control. These systems are especially prevalent in urology, orthopedics, and gynecology, enabling minimally invasive procedures and reducing patient recovery times.

Artificial intelligence (AI) and machine learning are also shaping the market by supporting surgical planning, real-time decision-making, and predictive analytics. AI algorithms assist in identifying optimal surgical approaches, anticipating complications, and enhancing patient outcomes. Augmented reality (AR) and virtual reality (VR) technologies are increasingly utilized for surgical training and procedural simulations, allowing medical professionals to practice complex procedures in immersive environments before performing them on patients.

The Internet of Things (IoT) is enabling real-time monitoring of surgical instruments and patient vitals, ensuring seamless communication and coordination among surgical teams. IoT integration helps optimize workflow efficiency and enhances patient safety. Additionally, there is growing demand for sustainable surgical supplies, with manufacturers developing biodegradable and recyclable instruments to minimize environmental impact and meet regulatory requirements. These technological innovations collectively drive market growth and redefine operating room practices for hospitals and surgical centers worldwide.

In September 2024, Medtronic announced the launch of its next-generation robotic surgical system, designed to enhance precision and reduce recovery times for patients undergoing minimally invasive procedures. Source: www.medtronic.com

In November 2024, Stryker expanded its product portfolio by acquiring a leading surgical navigation technology company, aiming to enhance its capabilities in precision surgery and strengthen its position in the global market. Source: www.stryker.com

In January 2025, Siemens Healthineers unveiled a new AI-driven surgical planning tool, enabling real-time decision-making and improved patient outcomes during complex surgical procedures. Source: www.siemens-healthineers.com

The Operating Room Equipment & Supplies Market Report provides a comprehensive assessment of the global market, covering multiple product segments, applications, end-users, and technological innovations. The report examines key product categories, including surgical instruments, anesthesia equipment, operating tables, surgical imaging devices, and operating room lighting, providing insights into usage patterns and adoption trends. It also focuses on end-users such as hospitals, ambulatory surgical centers, and specialty clinics, highlighting the varying demands of different healthcare environments and their impact on procurement decisions.

The report offers regional analysis, exploring market dynamics across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. It identifies key growth drivers, infrastructure trends, and emerging opportunities specific to each region. Technological advancements are highlighted, including robotic-assisted surgery, AI integration, IoT-enabled devices, and digital OR management systems, emphasizing their role in enhancing surgical efficiency and patient outcomes.

Furthermore, the report addresses the competitive landscape, profiling leading market players and their strategic initiatives, including product launches, partnerships, and technological innovations. Emerging and niche segments, such as eco-friendly surgical supplies and hybrid operating rooms, are also examined. Overall, the report serves as a crucial resource for stakeholders, offering actionable insights for informed decision-making, strategic planning, and investment prioritization in the operating room equipment and supplies market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 4,861.0 Million |

| Market Revenue (2032) | USD 8,864.9 Million |

| CAGR (2025–2032) | 7.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Philips, Stryker, Siemens Healthineers, Medtronic, STERIS, GE Healthcare, Karl Storz, Olympus, Johnson & Johnson MedTech, Zimmer Biomet |

| Customization & Pricing | Available on Request (10% Customization is Free) |