Reports

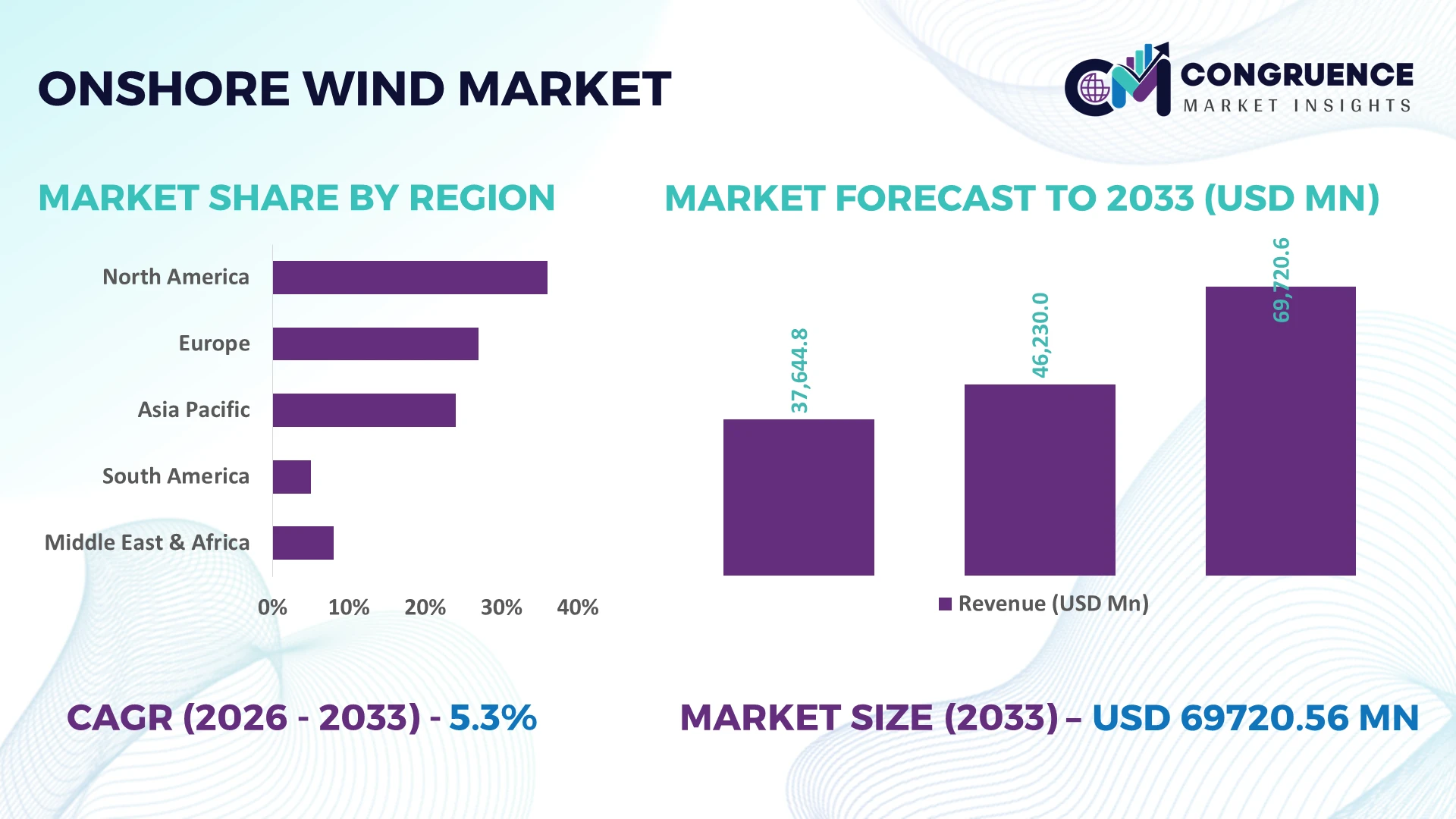

The Global Onshore Wind Market was valued at USD 46230 Million in 2025 and is anticipated to reach a value of USD 69720.56 Million by 2033 expanding at a CAGR of 5.27% between 2026 and 2033. Growth is being driven by higher-capacity turbines, grid modernization investments, digital wind farm optimization, and expanding renewable energy procurement across utility-scale power generation.

China dominates the global Onshore Wind Market with approximately 44% of worldwide installed onshore wind capacity, supported by annual installations exceeding 80 GW, strong domestic turbine manufacturing, and large-scale grid infrastructure investments. Compared with India, which is rapidly expanding through competitive renewable auctions and local manufacturing initiatives, China maintains a significantly larger deployment base. Ongoing energy security priorities following global supply chain realignments continue to accelerate strategic renewable investments across the region.

Companies expanding into markets with established manufacturing ecosystems, modern transmission infrastructure, and stable renewable policies are positioned to achieve stronger long-term project returns.

Market Size & Growth: USD 46,230 million in 2025 is projected to reach USD 69,720.56 million by 2033 at a CAGR of 5.27%, supported by larger turbine capacities and advanced grid integration.

Top Growth Drivers: Turbine efficiency improves over 15%, digital asset monitoring increases operational availability by 12%, and localized manufacturing reduces logistics costs by nearly 10%.

Short-Term Forecast: By 2028, predictive maintenance and digital monitoring reduce unplanned downtime by approximately 20%, improving operational productivity across utility-scale wind farms.

Emerging Technologies: AI-based maintenance, autonomous drone inspections, and advanced composite blades improve energy capture by nearly 8% while strengthening high-performance wind operations.

Regional Leaders: Asia Pacific exceeds USD 31 billion, Europe approaches USD 18 billion, and North America surpasses USD 13 billion, driven by transmission upgrades and regional manufacturing expansion.

Consumer & End-User Trends: More than 70% of new utility-scale renewable procurement favors long-term onshore wind power purchase agreements to improve electricity price stability.

Pilot/Case Example: In 2026, digitally optimized wind farm operations improved turbine availability by approximately 9% while reducing maintenance response times through AI-enabled performance monitoring.

Competitive Landscape: The leading manufacturer holds roughly 16% global market share, with Vestas, Goldwind, Envision Energy, Siemens Gamesa, and GE Vernova maintaining strong international project pipelines.

Regulatory & ESG Impact: Renewable energy policies support over 55% of planned utility-scale projects, while stricter carbon reduction targets continue accelerating onshore wind deployment across major economies.

Investment & Funding: Global investment exceeds USD 95 billion, supported by infrastructure partnerships, manufacturing expansion, and regional supply chain diversification following geopolitical shifts.

Innovation & Future Outlook: Next-generation modular turbines, recyclable blade materials, and AI-powered digital twins are improving asset performance while strengthening long-term operational resilience.

Growing electricity demand from industrial facilities, data centers, and large commercial users continues to strengthen demand for advanced onshore wind installations. Manufacturers are introducing larger rotor diameters, AI-enabled predictive maintenance, and lightweight blade materials that improve energy output by nearly 10%. Accelerating domestic manufacturing initiatives and resilient supply-chain strategies are further enhancing project execution, setting the stage for the market's evolving strategic landscape.

The Onshore Wind Market has become strategically important as governments, utilities, and industrial energy consumers prioritize resilient electricity generation, domestic manufacturing, and grid modernization. Supply-chain restructuring since recent geopolitical disruptions has accelerated localized turbine production and component sourcing, reducing procurement risks while improving project execution timelines. Competitive differentiation is increasingly determined by digital asset management, predictive maintenance, and higher-capacity turbine platforms that maximize energy output over the project lifecycle.

Modern onshore turbines equipped with AI-enabled condition monitoring and advanced composite blades deliver approximately 12% higher energy capture while reducing maintenance costs by nearly 18% compared with legacy turbine systems lacking digital diagnostics. China continues to lead large-scale deployment through integrated manufacturing and transmission expansion, whereas Germany emphasizes turbine repowering, grid flexibility, and digital optimization to increase output from existing wind assets. During the next two to three years, predictive maintenance adoption is expected to exceed 60% across newly commissioned utility-scale projects, improving operational availability and reducing unexpected service interruptions.

A recent utility-scale deployment integrating digital twin technology and automated blade inspection shortened maintenance planning cycles by almost 20%, enabling higher annual electricity generation. Companies are strengthening competitive positioning through localized manufacturing partnerships, advanced turbine development, and long-term service agreements, creating operational resilience while securing stronger market relevance in an increasingly technology-driven renewable energy landscape.

Rising electricity demand, national decarbonization targets, and transmission network upgrades continue to accelerate utility-scale onshore wind deployment. Turbine capacities have increased by nearly 25% over the past five years, while predictive maintenance improves operational availability by around 15% and digital monitoring lowers maintenance interventions by approximately 20%. India has expanded renewable energy auctions, encouraging domestic manufacturing and reducing import dependency for critical wind components. These structural developments improve project economics and supply resilience. In response, turbine manufacturers are expanding production facilities, forming technology partnerships, and investing in larger rotor platforms and intelligent asset management systems to strengthen competitive positioning and increase long-term operational efficiency.

Transmission bottlenecks, grid connection delays, and fluctuating raw material prices continue to constrain project execution despite strong installation pipelines. Steel and rare-earth material costs have experienced periodic fluctuations exceeding 20%, while grid connection delays extend project commissioning schedules by nearly 15% in several high-installation countries. The United Kingdom and other mature markets also face lengthy permitting procedures that affect deployment consistency. These challenges increase capital planning complexity and reduce operational predictability. Companies are responding by localizing component sourcing, securing long-term procurement agreements, expanding inventory strategies, and adopting alternative generator technologies that reduce dependence on critical materials while improving supply-chain resilience.

Repowering aging wind assets and deploying AI-enabled operational platforms present significant opportunities for improving electricity generation without proportional infrastructure expansion. Advanced control software increases turbine efficiency by approximately 10%, while digital twin technologies reduce maintenance planning time by nearly 18%. Germany continues investing in repowering projects that replace older turbines with higher-capacity models using existing sites and transmission infrastructure. Equipment manufacturers are expanding research into recyclable blade materials, autonomous inspection systems, and intelligent forecasting platforms. These innovations enhance asset utilization, lower lifecycle operating costs, and create differentiated service-based business models that strengthen long-term customer relationships.

Long-term market expansion depends on synchronizing skilled workforce availability, transmission upgrades, and increasingly digital wind farm operations. More than 30% of utilities report shortages of specialized wind technicians, while digital infrastructure investments raise cybersecurity exposure across connected operational technology environments. Grid congestion in several industrialized countries further limits efficient renewable integration during peak generation periods. These execution challenges directly influence project consistency, maintenance quality, and operational reliability. Companies must accelerate workforce development, strengthen cybersecurity frameworks, expand digital grid collaboration, and invest in intelligent transmission infrastructure to maintain competitive performance and support sustainable large-scale deployment.

Advanced Turbine Digitalization AI-enabled predictive maintenance, digital twins, and automated blade inspections are becoming standard across new wind farms. Predictive analytics improves turbine availability by approximately 15%, while maintenance planning time falls nearly 20% and inspection costs decline around 18%. Utilities in China and Spain are integrating cloud-based monitoring platforms, prompting manufacturers to expand digital service partnerships and long-term asset management offerings.

Localized Manufacturing Expansion Supply-chain diversification continues reshaping procurement strategies as manufacturers reduce dependence on imported components. Domestic sourcing has increased by nearly 25% across several major producing countries, while logistics costs have declined by approximately 12% through regional production networks. Policy incentives and trade uncertainties are encouraging companies to establish new blade, nacelle, and tower manufacturing facilities closer to project locations.

Repowering Existing Wind Assets Operators are replacing aging turbines with higher-capacity models rather than developing entirely new sites. Modern repowering projects improve electricity generation by nearly 30% while reducing maintenance frequency by approximately 15% using existing transmission infrastructure. Germany and Denmark continue prioritizing this approach, leading turbine suppliers to strengthen engineering partnerships and lifecycle service contracts for mature wind portfolios.

Grid-Integrated Smart Operations Grid operators increasingly require wind farms to provide advanced forecasting and grid support capabilities. Forecast accuracy has improved by approximately 18%, while automated dispatch systems reduce balancing costs by nearly 10%. As renewable penetration rises, developers are investing in intelligent control software, energy management platforms, and utility collaboration programs to improve network stability and operational flexibility.

Utility-Scale Turbines remain the dominant segment because they deliver the highest electricity output, stronger project economics, and seamless integration with national transmission infrastructure. More than 75% of newly commissioned onshore wind capacity is concentrated in utility-scale installations, while larger rotor diameters improve annual energy production by approximately 12%. Direct Drive Turbines continue gaining preference due to lower maintenance requirements, reducing mechanical servicing by nearly 20% compared with conventional gearbox systems. Manufacturers are expanding production of high-capacity turbine platforms while strengthening strategic partnerships with utilities and engineering contractors to improve project delivery.

Horizontal Axis Turbines continue representing the industry's mature technology standard because of proven efficiency and commercial scalability. Vertical Axis Turbines are the fastest-growing niche, supported by urban deployment, simplified maintenance, and suitability for complex wind conditions. Small-Scale Turbines maintain relevance in distributed generation and remote energy applications where grid connectivity remains limited. Companies continue diversifying product portfolios to address both large utility developments and specialized decentralized energy requirements, creating broader market opportunities.

Utility Power remains the leading application as national utilities continue expanding renewable electricity generation to strengthen grid reliability and energy security. Approximately 80% of newly installed onshore wind capacity supports utility-scale electricity networks, while advanced forecasting technologies improve operational scheduling accuracy by nearly 18%. Utilities are integrating larger turbines with digital monitoring platforms, enabling higher asset utilization and lower operating costs. Equipment suppliers continue expanding engineering capabilities and long-term maintenance agreements to support increasingly complex utility portfolios.

Industrial Power represents the fastest-growing application as manufacturers seek stable renewable electricity through captive generation and long-term power agreements. Commercial Power continues expanding among large business campuses focused on energy cost optimization, while Community Projects support localized electricity resilience through cooperative ownership structures. Rural Electrification remains strategically important in countries expanding electricity access through decentralized renewable infrastructure. Companies are adapting by offering modular deployment models, intelligent control systems, and customized financing structures to address the operational needs of different application segments.

Utilities remain the dominant end-user group because of their responsibility for large-scale electricity generation, transmission integration, and long-term renewable procurement. More than 70% of new onshore wind projects are developed for regulated utilities and public electricity providers, while digital asset management improves fleet availability by approximately 15%. Utilities continue prioritizing higher-capacity turbines and integrated monitoring platforms to optimize operational efficiency. Manufacturers are strengthening long-term service agreements and expanding localized technical support to improve lifecycle performance.

Independent Power Producers are the fastest-growing end-user segment as competitive renewable procurement and private investment accelerate project development. Industrial buyers continue increasing direct renewable electricity sourcing to improve operational resilience, while Government organizations support strategic energy transition initiatives through public infrastructure programs. Commercial users remain focused on reducing electricity costs through long-term renewable supply contracts. Companies are responding with flexible financing models, customized engineering solutions, and collaborative development partnerships that improve project scalability and strengthen competitive positioning across diverse customer groups.

Asia-Pacific accounted for the largest market share at 48.6% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a 6.8% CAGR between 2026 and 2033.

Grid Modernization Strengthens Utility Deployment

North America continues to strengthen its position through utility-scale wind repowering, domestic turbine manufacturing, and transmission modernization. The region contributes approximately 22% of global installed onshore wind capacity, supported by mature project development and expanding digital asset management. More than 65% of recently commissioned projects incorporate predictive maintenance platforms, improving operational availability while reducing maintenance interventions. Manufacturers are increasing local component production and expanding long-term service partnerships to improve supply resilience. Continued transmission upgrades and hybrid renewable integration are improving project utilization while enabling utilities to manage larger shares of variable renewable electricity with greater operational stability.

United States Market Outlook: The United States remains the regional leader because of its extensive installed wind fleet, advanced project financing ecosystem, and strong domestic manufacturing capabilities. Utility operators continue replacing older turbines with higher-capacity models, improving electricity production without significant land expansion. More than 150 GW of cumulative wind capacity supports large-scale electricity generation, while increasing investment in intelligent grid technologies and domestic blade manufacturing strengthens long-term operational competitiveness.

Repowering Drives Infrastructure Modernization

Europe remains one of the most technologically advanced onshore wind markets, supported by mature regulatory frameworks, turbine modernization, and aggressive decarbonization strategies. Approximately 25% of operating projects are entering repowering cycles, allowing operators to replace aging assets with higher-capacity turbines using existing infrastructure. Digital monitoring platforms and advanced forecasting systems continue improving grid balancing efficiency. Manufacturers are strengthening engineering partnerships and expanding recyclable turbine component development to align with circular economy objectives while improving lifecycle asset performance.

Germany Market Outlook: Germany leads the European market through large-scale repowering initiatives, strong engineering expertise, and integrated renewable energy planning. National permitting reforms are accelerating project approvals while digital grid management improves renewable integration efficiency. Thousands of legacy turbines remain eligible for replacement with modern high-capacity units, creating sustained opportunities for equipment suppliers, engineering firms, and long-term maintenance service providers.

Manufacturing Scale Supports Market Leadership

Asia-Pacific represents the world's largest onshore wind deployment and manufacturing hub, accounting for nearly 49% of global market activity. Integrated turbine manufacturing, localized supply chains, and large-scale transmission investments continue strengthening regional competitiveness. Annual installations remain among the highest globally, while localized production has reduced equipment lead times by approximately 20%. Developers continue expanding manufacturing partnerships and digital wind farm management capabilities to improve project execution and operational efficiency across rapidly expanding renewable energy portfolios.

China Market Outlook: China maintains unmatched leadership through extensive turbine manufacturing capacity, integrated supply chains, and continuous renewable infrastructure investment. Annual onshore wind installations regularly exceed 80 GW, supported by advanced transmission expansion and domestic technology development. Local manufacturers continue introducing larger turbine platforms and intelligent operating systems, reinforcing the country's competitive advantage in both domestic deployment and international equipment exports.

Competitive Renewable Procurement Expands Capacity

South America continues expanding onshore wind deployment through competitive renewable energy auctions, improving grid infrastructure, and increasing industrial electricity demand. Wind generation is becoming an essential component of national electricity systems, particularly in high-resource locations with favorable wind conditions. Recent transmission improvements have reduced grid bottlenecks, while project developers increasingly adopt digital performance monitoring to improve asset utilization. Although infrastructure limitations remain in selected markets, stronger public-private collaboration continues supporting long-term project development and operational reliability.

Brazil Market Outlook: Brazil remains the largest onshore wind market in South America due to exceptional wind resources, expanding transmission infrastructure, and strong renewable procurement programs. Capacity utilization in several northeastern wind corridors consistently exceeds international averages, supporting competitive electricity production. Domestic and international developers continue expanding partnerships while investing in localized operations, maintenance capabilities, and advanced forecasting technologies to improve project performance.

Energy Diversification Accelerates Investment

The Middle East & Africa market is advancing through national energy diversification programs, utility-scale renewable procurement, and expanding electricity infrastructure. Although the region represents a smaller global share, deployment activity continues increasing through large government-backed projects and international technology partnerships. Modern wind developments increasingly integrate digital monitoring systems and intelligent grid management, improving operational efficiency while supporting national clean energy strategies. Infrastructure modernization and localized engineering capabilities continue strengthening long-term project execution across emerging renewable energy markets.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region's strategic leader through ambitious renewable energy targets, utility-scale project development, and sustained infrastructure investment. National energy diversification programs continue expanding onshore wind deployment alongside grid modernization initiatives. Large renewable procurement programs, combined with international technology partnerships and local industrial development, are strengthening domestic project execution capabilities and positioning the country as a key future renewable energy investment destination.

The competitive landscape is shaped by Vestas, Goldwind, Envision Energy, GE Vernova, and Nordex Group, competing directly for utility-scale projects against expanding regional manufacturers in China and India. Global technology leaders emphasize turbine performance, lifecycle services, and digital asset optimization, while cost-focused regional suppliers compete through localized manufacturing and faster delivery. The top five players collectively account for approximately 58% of global installations, creating a moderately consolidated market. Competition increasingly depends on turbine efficiency, where larger rotor platforms improve annual energy production by nearly 12%, while predictive maintenance lowers operating costs by around 18% and localized sourcing reduces logistics expenses by approximately 10%. Companies are expanding manufacturing capacity, forming utility partnerships, integrating digital monitoring platforms, and strengthening vertical supply chains to secure critical components. Technology-led differentiation and supply-chain control are replacing price competition as the primary strategic advantage. High certification requirements, manufacturing scale, and long-term service capabilities remain significant entry barriers. Success depends on combining advanced turbine technology, resilient supply networks, localized production, and comprehensive lifecycle support.

Vestas

Goldwind

Envision Energy

GE Vernova

Nordex Group

Siemens Gamesa

MingYang Smart Energy

Windey Energy

SANY Renewable Energy

Enercon

Suzlon Energy

Dongfang Electric

CSIC Haizhuang Wind Power

Digitalization is transforming onshore wind operations through AI-enabled predictive maintenance, digital twins, automated inspections, and cloud-based asset management. More than 60% of newly commissioned utility-scale projects are integrating advanced monitoring platforms that improve turbine availability by approximately 15% while reducing maintenance planning time by nearly 20%. Utilities and independent power producers benefit from higher operational visibility, faster fault detection, and optimized maintenance scheduling, enabling greater electricity generation with lower lifecycle operating costs.

Next-generation turbine platforms featuring larger rotor diameters, advanced composite blades, and direct drive generators are replacing conventional gearbox-based systems. Compared with legacy turbine designs, these technologies increase annual energy capture by nearly 12% while reducing mechanical maintenance requirements by approximately 18%. Manufacturers investing in modular turbine architecture and recyclable blade materials gain stronger competitive positioning through lower operating costs, simplified servicing, and improved sustainability performance across utility-scale deployments.

Between 2026 and 2028, intelligent grid integration, autonomous drone inspections, and AI-driven power forecasting will become core competitive technologies. Deployment of digital grid synchronization tools is expected to exceed 70% across newly developed large-scale wind projects, improving dispatch accuracy and reducing balancing costs. Companies that integrate advanced software, cybersecurity, and predictive analytics with turbine engineering will achieve superior operational resilience, stronger service differentiation, and sustained competitive advantage in increasingly digital renewable energy markets.

June 2026 GE Vernova launched its 3.8 MW-154m onshore turbine in India and secured a partnership with Powerica for the 100 MW Botad Wind Farm, while expanding local manufacturing capacity to 1,500 MW annually. The move strengthens domestic production and supports faster project execution.

April 2026 GE Vernova signed agreements with BBWind and Greenvolt Power to supply 71.5 MW of onshore wind turbines for projects across Germany. The partnership expands the company's European project pipeline while reinforcing localized manufacturing and engineering capabilities.

February 2026 GE Vernova announced that it received 1.1 GW of U.S. onshore wind repowering orders booked during 2025, utilizing domestically manufactured nacelles and drivetrains. The projects extend turbine operating life while significantly reducing long-term operation and maintenance requirements.

April 2026 The Global Wind Energy Council reported China installed more than 100 GW of wind capacity during 2025, marking the first country to surpass that milestone. The achievement reinforces manufacturing leadership, accelerates global supply expansion, and strengthens export competitiveness for leading turbine manufacturers.

This report provides comprehensive analysis of the global Onshore Wind Market across major turbine types, applications, and end-user categories, covering Utility-Scale Turbines, Direct Drive Turbines, Horizontal Axis Turbines, Vertical Axis Turbines, and Small-Scale Turbines. It evaluates deployment trends across Utility Power, Industrial Power, Commercial Power, Community Projects, and Rural Electrification while assessing demand from utilities, governments, industrial operators, commercial organizations, and independent power producers. The study also compares market dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The report analyzes manufacturing expansion, digital wind farm technologies, grid modernization, predictive maintenance, and turbine innovation shaping industry competitiveness between 2026 and 2033. It incorporates operational indicators including deployment concentration, technology adoption, and evolving procurement strategies while profiling leading industry participants. Strategic insights support investment prioritization, market entry evaluation, capacity expansion planning, competitive benchmarking, partnership development, and long-term business decision-making across mature and emerging onshore wind markets.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 46230 Million |

Market Revenue in 2033 | USD 69720.56 Million |

CAGR (2026 - 2033) | 5.27% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Vestas, Goldwind, Envision Energy, GE Vernova, Nordex Group, Siemens Gamesa, MingYang Smart Energy, Windey Energy, SANY Renewable Energy, Enercon, Suzlon Energy, Dongfang Electric, CSIC Haizhuang Wind Power |

Customization & Pricing | Available on Request (10% Customization is Free) |