Reports

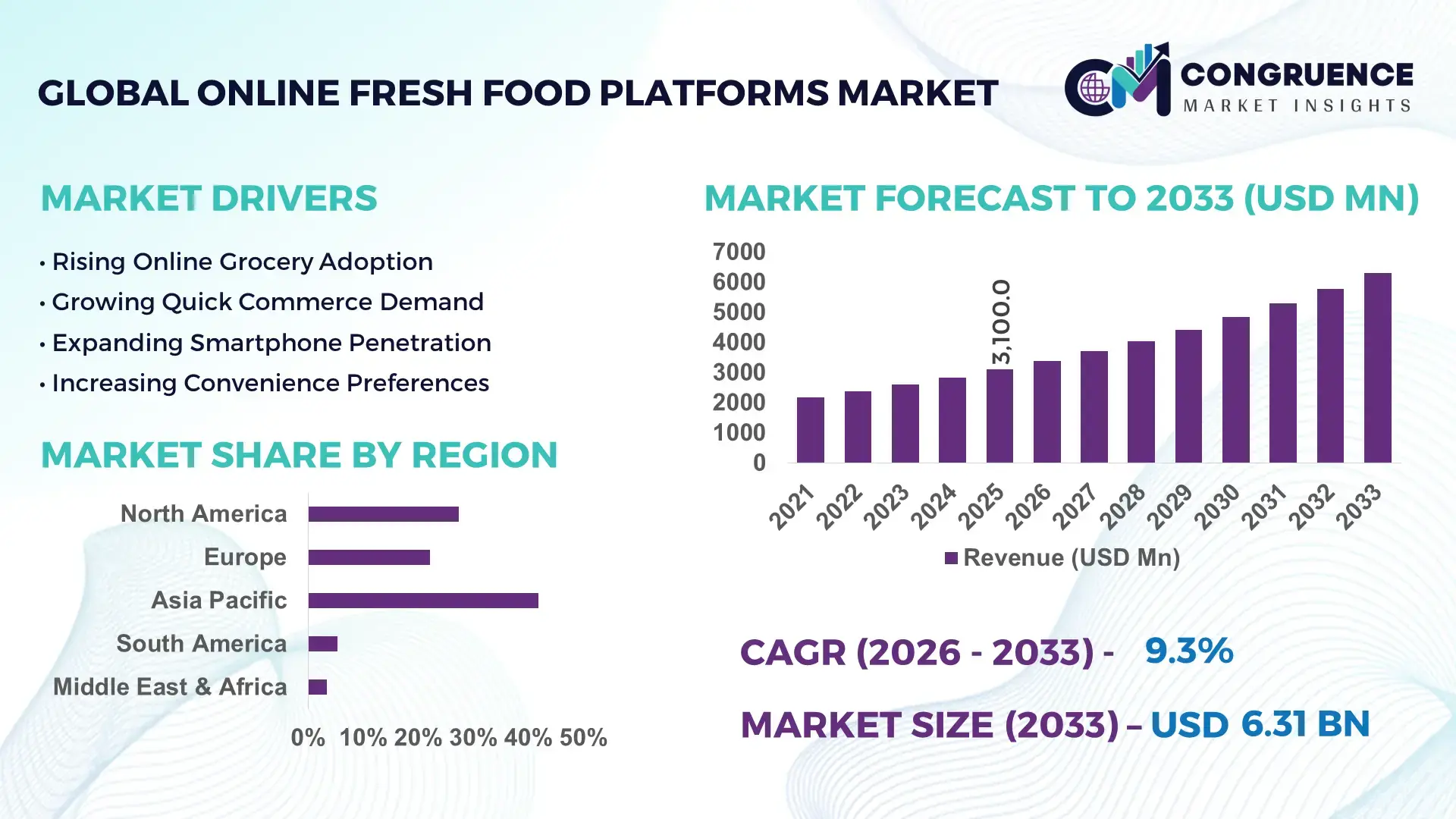

The Global Online Fresh Food Platforms Market was valued at USD 3,100.0 Million in 2025 and is anticipated to reach a value of USD 6,314.3 Million by 2033 expanding at a CAGR of 9.3% between 2026 and 2033. Growth is being accelerated by rapid dark-store deployment, AI-enabled demand forecasting, and last-mile cold-chain optimization that reduces fresh produce spoilage and delivery turnaround times.

China remains the dominant country in the global online fresh food platforms ecosystem, accounting for approximately 34% of total platform transaction volume, supported by more than 1,800 urban fulfillment hubs and strong penetration of mobile commerce. Compared with the United States, where online grocery adoption is near 23% of households, China exceeds 38% in major metropolitan areas. Continued investments in digital logistics infrastructure and food traceability systems, reinforced by post-pandemic supply-chain modernization initiatives, are strengthening operational scale and customer retention across the sector.

Strategically, market leaders are prioritizing integrated fulfillment networks and predictive inventory systems to secure delivery efficiency, product freshness, and competitive differentiation.

Market Size & Growth: Valued at USD 3,100.0 Million in 2025 and projected to reach USD 6,314.3 Million by 2033, supported by AI-driven inventory planning and expanding cold-chain logistics networks at a CAGR of 9.3%.

Top Growth Drivers: Same-day delivery demand (+32%), digital grocery adoption (+27%), and smart fulfillment deployment (+24%) are accelerating platform expansion.

Short-Term Forecast: By 2028, order fulfillment efficiency is expected to improve by 18% while fresh-food wastage rates decline by nearly 15%.

Emerging Technologies: AI forecasting, automated micro-fulfillment centers, and IoT-based cold-chain monitoring are improving inventory accuracy by over 20%.

Regional Leaders: Asia Pacific (~USD 2.6 Billion), North America (~USD 1.8 Billion), and Europe (~USD 1.2 Billion) lead adoption through advanced logistics, digital retail integration, and premium fresh-food subscriptions.

Consumer/End-User Trends: More than 41% of urban consumers now purchase fresh groceries online at least once per week.

Pilot/Case Example: In 2024, AI-powered fulfillment initiatives reduced stock-out incidents by approximately 22% and shortened delivery windows by 17%.

Competitive Landscape: Top operators collectively control nearly 38% market share, with leading participants including Instacart, Walmart, JD.com, Alibaba Freshippo, and Ocado.

Regulatory & ESG Impact: Digital food traceability programs improved supply-chain visibility by 30% while supporting food-safety compliance requirements.

Investment & Funding: More than USD 2.4 Billion in platform, logistics, and fulfillment investments supported regional expansion and strategic partnerships.

Innovation & Future Outlook: Autonomous delivery pilots, predictive replenishment systems, and hyperlocal fulfillment models are reshaping the high-growth global marketplace.

Online Fresh Food Platforms are becoming a critical channel for fresh produce, dairy, seafood, and organic food distribution as consumers prioritize convenience, transparency, and delivery speed. AI-powered inventory optimization and real-time cold-chain monitoring are improving fulfillment accuracy, while nearly 45% of urban online grocery users now expect same-day delivery. Ongoing food traceability requirements and supply-chain resilience initiatives are also encouraging platforms to strengthen logistics ecosystems, creating a foundation for broader strategic transformation.

Online Fresh Food Platforms are becoming strategically important because they sit at the intersection of digital commerce, food security, and modern logistics transformation. Retailers, food producers, and logistics providers increasingly view these platforms as critical infrastructure for customer acquisition and operational efficiency. The market is benefiting from supply-chain restructuring efforts that prioritize localized sourcing, inventory visibility, and rapid fulfillment capabilities. As consumer expectations shift toward convenience and freshness, platform operators are investing heavily in integrated fulfillment ecosystems rather than standalone e-commerce models.

Technology adoption is creating measurable operational advantages. AI-enabled demand forecasting can improve inventory accuracy by approximately 20–25% compared with conventional replenishment systems while reducing fresh-product waste by nearly 15%. China continues to lead in fulfillment density and transaction scale, whereas the United States is focusing on automation-led productivity improvements and subscription-based grocery ecosystems. This contrast reflects different competitive priorities but a shared emphasis on logistics modernization and customer retention.

A practical example is the deployment of micro-fulfillment centers near urban demand clusters, reducing delivery times by up to 30% while increasing order processing capacity. Over the next two to three years, companies are expected to expand partnerships with cold-chain providers, local farms, and technology vendors to improve service reliability. Organizations that successfully combine data intelligence, fulfillment efficiency, and scalable sourcing networks will secure stronger competitive positioning and long-term market relevance.

The strongest growth catalyst is the integration of AI-based inventory management with advanced cold-chain infrastructure. Digital demand forecasting systems have improved stock accuracy by 20–25%, while smart temperature-monitoring solutions have reduced spoilage rates by nearly 15%. China and India are witnessing accelerated investment in urban fulfillment hubs as online grocery penetration expands. The shift toward same-day and next-day delivery models is forcing operators to redesign logistics networks for speed and freshness. As a result, companies are expanding micro-fulfillment facilities, partnering with local producers, and deploying predictive analytics platforms. A key strategic insight is that fulfillment efficiency has become a stronger competitive differentiator than pricing alone, pushing market participants toward technology-led operational optimization.

Fresh-food distribution remains operationally intensive due to temperature-control requirements, inventory perishability, and fragmented sourcing networks. Last-mile logistics can represent 35–50% of total fulfillment expenses, while fresh-product spoilage still ranges between 8% and 12% in many developing markets. In countries with uneven cold-chain infrastructure, delivery consistency becomes difficult to maintain at scale. These factors directly affect profitability and expansion economics. To reduce exposure, companies are diversifying supplier networks, establishing regional fulfillment centers, and implementing automated route optimization technologies. A significant operational insight is that platform scalability increasingly depends on logistics efficiency rather than customer acquisition alone, making infrastructure investment a critical competitive requirement.

A major opportunity lies in combining hyperlocal sourcing models with predictive retail technologies. AI-driven recommendation engines can increase basket values by approximately 12–18%, while automated replenishment systems improve repeat purchase rates by more than 20%. India, Indonesia, and Vietnam present substantial untapped demand as digital payment adoption and urban grocery digitization continue to expand. Emerging technologies such as digital food traceability and blockchain-enabled sourcing verification are creating new value propositions for consumers seeking transparency. Companies are responding through ecosystem partnerships with farms, logistics providers, and retail chains. A non-obvious strategic advantage is that localized sourcing can simultaneously reduce delivery distances, improve freshness metrics, and strengthen supply resilience.

The principal long-term challenge is maintaining operational consistency as platform networks become larger and more complex. Delivery volumes in major metropolitan markets are growing by more than 20% annually, increasing pressure on workforce management, inventory synchronization, and fulfillment infrastructure. Cybersecurity risks have also intensified as customer transaction data and supplier systems become increasingly interconnected. In addition, maintaining cold-chain integrity across multi-city networks remains technically demanding. Companies must invest in automation, real-time monitoring platforms, and workforce training programs to sustain service quality. A critical strategic insight is that future competitiveness will depend not only on growth scale but on the ability to deliver uniform freshness, reliability, and customer experience across geographically diverse operating environments.

AI-Driven Inventory Precision AI-powered forecasting engines are reducing stock-out rates by 20–25% while improving inventory accuracy by nearly 22% across large grocery platforms. Operators in China and the United States are integrating demand-sensing algorithms directly into procurement workflows to synchronize sourcing with real-time consumption patterns. Rising pressure to reduce food waste and improve margin performance is accelerating deployment. Companies are expanding analytics partnerships and automating replenishment decisions, resulting in faster inventory turnover and more efficient cold-chain utilization.

Micro-Fulfillment Network Expansion Urban fulfillment restructuring is becoming a defining operational trend as delivery expectations tighten. Micro-fulfillment centers have shortened average delivery windows by 25–30% and increased order-processing capacity by approximately 18%. Labor availability challenges and rising transportation costs are prompting retailers to position inventory closer to demand clusters. Major operators are scaling compact automated facilities, restructuring warehouse footprints, and integrating robotics into picking processes to improve throughput while controlling logistics expenses.

Traceability and Compliance Integration Digital food traceability adoption has increased by more than 28% as regulators strengthen food-safety monitoring requirements. QR-based tracking, IoT-enabled temperature monitoring, and supplier-verification systems are becoming standard across fresh-food supply chains. Beyond compliance, a non-obvious benefit is stronger consumer trust and reduced dispute management costs. Platform providers are responding through supplier digitization programs, blockchain-enabled verification pilots, and end-to-end visibility initiatives that improve accountability across sourcing networks.

Hyperlocal Sourcing Optimization Hyperlocal procurement models are expanding rapidly, with locally sourced product volumes increasing by nearly 20% among leading platforms. Supply-chain disruptions and transportation volatility have encouraged operators to shorten sourcing distances and diversify supplier bases. This shift improves freshness metrics while reducing fulfillment complexity and spoilage exposure. Companies are forming partnerships with regional farms, producer cooperatives, and local distributors to strengthen supply resilience, improve delivery consistency, and create differentiated product assortments for urban consumers.

Marketplace Platforms remain the leading segment due to their scalable operating structure, extensive supplier ecosystems, and lower inventory ownership requirements. These platforms account for approximately 45% of market activity, supported by broad product selection and rapid geographic expansion capabilities. Their asset-light approach enables faster onboarding of local producers and retailers while maintaining competitive pricing. Companies continue strengthening marketplace ecosystems through integrated payment systems, logistics partnerships, and AI-based recommendation engines that improve customer retention and order frequency. Quick Commerce Platforms represent the fastest-growing segment as consumer expectations increasingly shift toward ultra-fast fulfillment. Adoption rates for rapid-delivery services have increased by nearly 30% in major metropolitan markets where convenience and time sensitivity influence purchasing behavior. Meanwhile, Direct-to-Consumer (D2C) Platforms retain strategic relevance through premium product differentiation and stronger brand control, while Subscription-Based Platforms are gaining traction among recurring grocery buyers seeking predictable deliveries. Companies are increasing investments in dark stores, fulfillment automation, and membership programs to capture evolving demand patterns and improve operational efficiency.

Grocery and Daily Essentials remains the leading application segment due to high purchase frequency, recurring household demand, and broad product coverage. The category represents nearly 50% of platform transaction activity, supported by consumer preference for routine replenishment and convenient home delivery. Companies are expanding SKU availability, improving inventory visibility, and integrating automated replenishment features to strengthen engagement. The segment also benefits from strong operational efficiency because delivery routes can be optimized around predictable purchasing behavior. Fresh Produce Delivery is emerging as the fastest-growing application as consumers place greater emphasis on freshness, quality assurance, and traceable sourcing. Order volumes in this category have increased by approximately 25%, supported by improvements in cold-chain infrastructure and quality-monitoring technologies. Dairy & Bakery Products continue to maintain stable demand due to frequent consumption cycles, while Meat & Seafood Delivery is experiencing increasing adoption through enhanced temperature-controlled logistics networks. Platform operators are investing in freshness monitoring, supplier integration, and fulfillment upgrades to improve service reliability and reduce spoilage-related losses across these evolving application categories.

Urban Households constitute the largest end-user segment because of dense population clusters, digital payment adoption, and strong demand for convenience-oriented grocery services. This group accounts for approximately 55% of platform utilization, supported by frequent purchasing patterns and higher acceptance of same-day delivery models. Companies target these consumers through loyalty programs, personalized recommendations, and subscription-based delivery offerings. The concentration of demand in major metropolitan areas also enables operators to achieve higher route density and improved fulfillment economics. Young Professionals and Dual-Income Families represent the fastest-growing end-user segment, with adoption increasing by nearly 28% as time-constrained consumers prioritize convenience and delivery reliability. Families with Children continue to generate substantial order volumes due to recurring grocery needs, while Senior Consumers are gradually increasing adoption through simplified interfaces and assisted ordering services. Platform providers are responding with customized pricing plans, targeted promotions, and expanded product assortments tailored to specific household requirements. Future demand is increasingly shifting toward digitally engaged consumer groups that value speed, transparency, and seamless purchasing experiences.

Asia-Pacific accounted for the largest market share at 41.8% in 2025 however, South America is expected to register the fastest growth, expanding at a CAGR of 11.1% between 2026 and 2033.

North America represented approximately 27.4% of the global market in 2025, supported by mature e-commerce infrastructure, high digital grocery penetration, and advanced cold-chain logistics capabilities. The region is witnessing accelerated deployment of AI-powered inventory planning and automated micro-fulfillment centers designed to improve order accuracy and delivery speed. More than 35% of large grocery operators have integrated predictive demand forecasting into fresh-food workflows. Strategic partnerships between retailers, logistics providers, and technology firms continue to strengthen fulfillment density across metropolitan areas. Investments in temperature-controlled delivery fleets and last-mile optimization platforms are helping operators reduce spoilage while improving service consistency and customer retention.

United States Market Outlook: The United States remains the largest contributor to regional demand due to its extensive grocery retail ecosystem, advanced logistics infrastructure, and strong consumer adoption of online food purchasing. Same-day and next-day delivery services are now available across most major metropolitan markets, with online grocery usage exceeding 23% of households. Enterprise investment is increasingly focused on automation, AI-enabled forecasting, and fulfillment network modernization. Large retailers are expanding dark-store capacity and integrating supplier data platforms to improve inventory visibility and strengthen operational responsiveness.

Europe accounted for nearly 22.1% of market activity, supported by strong food safety standards, established retail networks, and increasing adoption of traceability technologies. Regulatory emphasis on supply-chain transparency and food waste reduction is accelerating investment in digital monitoring systems and smart logistics infrastructure. More than 30% of leading grocery platforms have expanded supplier-traceability capabilities during the last two years. Retailers are integrating carbon-efficiency metrics, route optimization technologies, and automated inventory controls into fulfillment operations. The region’s focus on operational sustainability is creating differentiation through improved freshness management, compliance performance, and consumer trust.

Germany Market Outlook: Germany serves as the region’s strategic anchor due to its advanced logistics capabilities, highly organized retail sector, and strong digital infrastructure. The country has become a leading adopter of automated warehouse systems and data-driven inventory management. More than 40% of large grocery distribution centers have implemented advanced automation technologies to improve throughput and inventory accuracy. Operators continue to strengthen local sourcing networks and temperature-controlled logistics systems, supporting efficient fresh-food distribution while aligning with evolving sustainability and traceability requirements.

Asia-Pacific held the largest share of the global market at 41.8% in 2025, supported by dense urban populations, widespread mobile commerce adoption, and extensive fulfillment infrastructure. The region leads in transaction volume, platform deployment, and digital grocery engagement. Large-scale investments in fulfillment hubs, cold-chain facilities, and AI-enabled logistics networks continue to strengthen operational capacity. Online grocery adoption exceeds 35% in several major metropolitan markets, while platform operators are expanding hyperlocal sourcing models to improve freshness and delivery efficiency. The combination of scale, technology integration, and logistics modernization positions the region as the industry's primary operational benchmark.

China Market Outlook: China remains the most influential market globally, supported by advanced digital ecosystems, high-frequency online purchasing behavior, and extensive fulfillment infrastructure. The country operates thousands of urban fulfillment and distribution facilities designed to support rapid fresh-food delivery. Online grocery penetration exceeds 38% in leading cities, significantly outpacing many developed markets. Major platform operators continue investing in AI-driven demand forecasting, smart warehousing, and integrated supplier ecosystems. These capabilities enable high order density, reduced fulfillment costs, and strong operational scalability across diverse consumer segments.

South America is emerging as a high-potential market driven by expanding internet penetration, rising digital payment adoption, and growing urban consumer demand for convenience-oriented grocery services. The region accounted for approximately 5.3% of global market activity in 2025. Platform operators are investing in localized fulfillment models and strategic delivery partnerships to overcome infrastructure limitations. Digital grocery order volumes have increased by more than 20% across several major cities. While cold-chain coverage remains uneven in some markets, investments in logistics modernization and urban delivery networks are steadily improving service reliability and platform accessibility.

Brazil Market Outlook: Brazil represents the largest market in the region due to its sizable consumer base, expanding e-commerce ecosystem, and increasing adoption of app-based grocery purchasing. Large metropolitan areas such as São Paulo and Rio de Janeiro are driving demand through dense population clusters and improving delivery infrastructure. Online grocery engagement has increased significantly among middle-income households, prompting operators to expand fulfillment footprints and local sourcing partnerships. Continued investment in digital payments, warehouse modernization, and last-mile logistics is strengthening the country's position as South America's primary growth engine.

The Middle East & Africa accounted for approximately 3.4% of global market activity in 2025 and is benefiting from investments in logistics infrastructure, smart retail initiatives, and digital commerce modernization. Urban centers are witnessing increased deployment of temperature-controlled storage facilities and technology-enabled delivery networks. Governments and private enterprises are supporting digital transformation programs that improve food distribution efficiency and supply-chain visibility. Several leading operators have expanded fulfillment capabilities by more than 15% through strategic infrastructure investments and logistics partnerships. Market development remains concentrated in economically diversified countries with advanced retail and technology ecosystems.

United Arab Emirates Market Outlook: The United Arab Emirates serves as the region’s leading market due to its highly developed logistics infrastructure, strong digital commerce adoption, and supportive business environment. The country functions as a regional distribution hub, enabling efficient movement of imported and locally sourced fresh food products. High smartphone penetration and widespread digital payment usage continue to support online grocery adoption. Operators are investing in automated fulfillment facilities, advanced cold-chain assets, and integrated delivery platforms to enhance service quality and reduce delivery times, strengthening the country's leadership position within the regional ecosystem.

The Online Fresh Food Platforms Market is characterized by competition between global platform leaders such as Instacart, JD.com, Alibaba Freshippo, Ocado, and Walmart’s online grocery ecosystem, versus regional delivery specialists and hyperlocal commerce operators. The top five players collectively control approximately 38–42% of global platform activity, creating a moderately concentrated market structure. Competition centers on fulfillment speed, AI-driven inventory accuracy, supply-chain integration, and customer retention rather than price alone. Leading operators have improved inventory precision by 20–25% through predictive analytics, while automated fulfillment systems reduce order-processing times by nearly 30%. JD.com competes through vertically integrated logistics networks, Instacart through technology and retail partnerships, and Ocado through automation-led fulfillment capabilities. Competitive activity increasingly involves ecosystem expansion, retailer partnerships, micro-fulfillment deployment, and digital traceability investments. Technology-enabled personalization and rapid delivery models are reshaping market leadership positions. The current competitive shift favors operators controlling both data and fulfillment infrastructure. The primary entry barrier remains cold-chain logistics investment and fulfillment density. Winning requires superior execution across technology, logistics, supplier integration, and last-mile delivery performance.

JD.com

Ocado Group

Alibaba Freshippo

Walmart Grocery

Amazon Fresh

Meituan

DoorDash

Picnic Technologies

BigBasket

Rohlik Group

Carrefour eCommerce

Tesco Online Grocery

HelloFresh Market

Online Fresh Food Platforms are increasingly built around AI-driven demand forecasting, intelligent inventory optimization, and real-time fulfillment orchestration. Advanced forecasting systems improve inventory accuracy by 20–25% and reduce fresh-product spoilage by nearly 15%. More than 40% of large-scale grocery platforms have deployed machine-learning tools to align procurement, replenishment, and delivery workflows. Companies with high transaction volumes benefit most because forecasting precision directly improves fulfillment efficiency and customer retention.

The market is rapidly transitioning from conventional warehouse management systems toward automated micro-fulfillment and robotics-enabled order processing. Compared with traditional manual picking operations, automated fulfillment solutions improve processing productivity by approximately 30% while reducing labor-related operating costs by 15–20%. IoT-enabled cold-chain monitoring is also gaining adoption, with sensor-based temperature tracking improving product quality consistency across complex logistics networks. Operators integrating these technologies achieve stronger delivery reliability and lower wastage rates.

Between 2026 and 2028, disruptive technologies including autonomous delivery systems, digital twins, blockchain-based food traceability, and generative AI shopping assistants are expected to reshape platform operations. AI-powered personalization engines already influence over 25% of product recommendation interactions. Companies that combine automation, predictive intelligence, and supply-chain visibility will secure significant operational and competitive advantages as fulfillment expectations continue to intensify.

March 2025 – Instacart launched its AI-powered Smart Shop platform, using generative AI and machine learning to personalize grocery discovery and nutrition-based recommendations. The system analyzes shopping behavior to improve product relevance and streamline purchasing decisions, strengthening customer engagement and platform differentiation. Source: www.company.instacart.com

June 2025 – Instacart FoodStorm expanded deployment to more than 2,800 grocery stores across North America, more than doubling platform reach since late 2024. The rollout enhanced prepared-food ordering and fresh-counter operations, improving workflow efficiency and order management capabilities for participating retailers.

November 2025 – Kroger and Instacart expanded their strategic partnership, extending fulfillment services across nearly 2,700 stores and introducing new AI-enabled shopping experiences. The initiative strengthens delivery coverage, operational efficiency, and digital grocery accessibility while reinforcing Instacart's position as Kroger's primary fulfillment partner.

May 2026 – JD.com reported continued expansion of its integrated logistics and on-demand delivery ecosystem, supported by 4.9% year-over-year business growth. The company strengthened synergies between retail, logistics, and food-delivery operations, improving platform engagement and fulfillment efficiency across its digital commerce network.

This report provides comprehensive analysis of the Online Fresh Food Platforms Market across major platform types, applications, end-user categories, and key geographic regions. The study evaluates Marketplace Platforms, Quick Commerce Platforms, Direct-to-Consumer Platforms, and Subscription-Based Models, while assessing demand across grocery essentials, fresh produce, dairy products, meat, seafood, and specialized food categories. Regional assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, representing more than 95% of global platform deployment activity.

The report further examines technology adoption patterns including AI forecasting, fulfillment automation, cold-chain monitoring, traceability solutions, and digital logistics integration. Competitive benchmarking covers leading platform operators, supply-chain strategies, partnership activity, and deployment trends. Strategic insights support investment evaluation, market-entry planning, expansion prioritization, operational optimization, and competitive positioning. Special attention is given to emerging fulfillment models, hyperlocal sourcing networks, automation deployment, and evolving consumer purchasing behavior expected to influence market direction between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 3,100.0 Million |

| Market Revenue (2033) | USD 6,314.3 Million |

| CAGR (2026–2033) | 9.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Instacart; JD.com; Ocado Group; Alibaba Freshippo; Walmart Grocery; Amazon Fresh; Meituan; DoorDash; Picnic Technologies; BigBasket; Rohlik Group; Carrefour eCommerce; Tesco Online Grocery; HelloFresh Market |

| Customization & Pricing | Available on Request (10% Customization Free) |