Reports

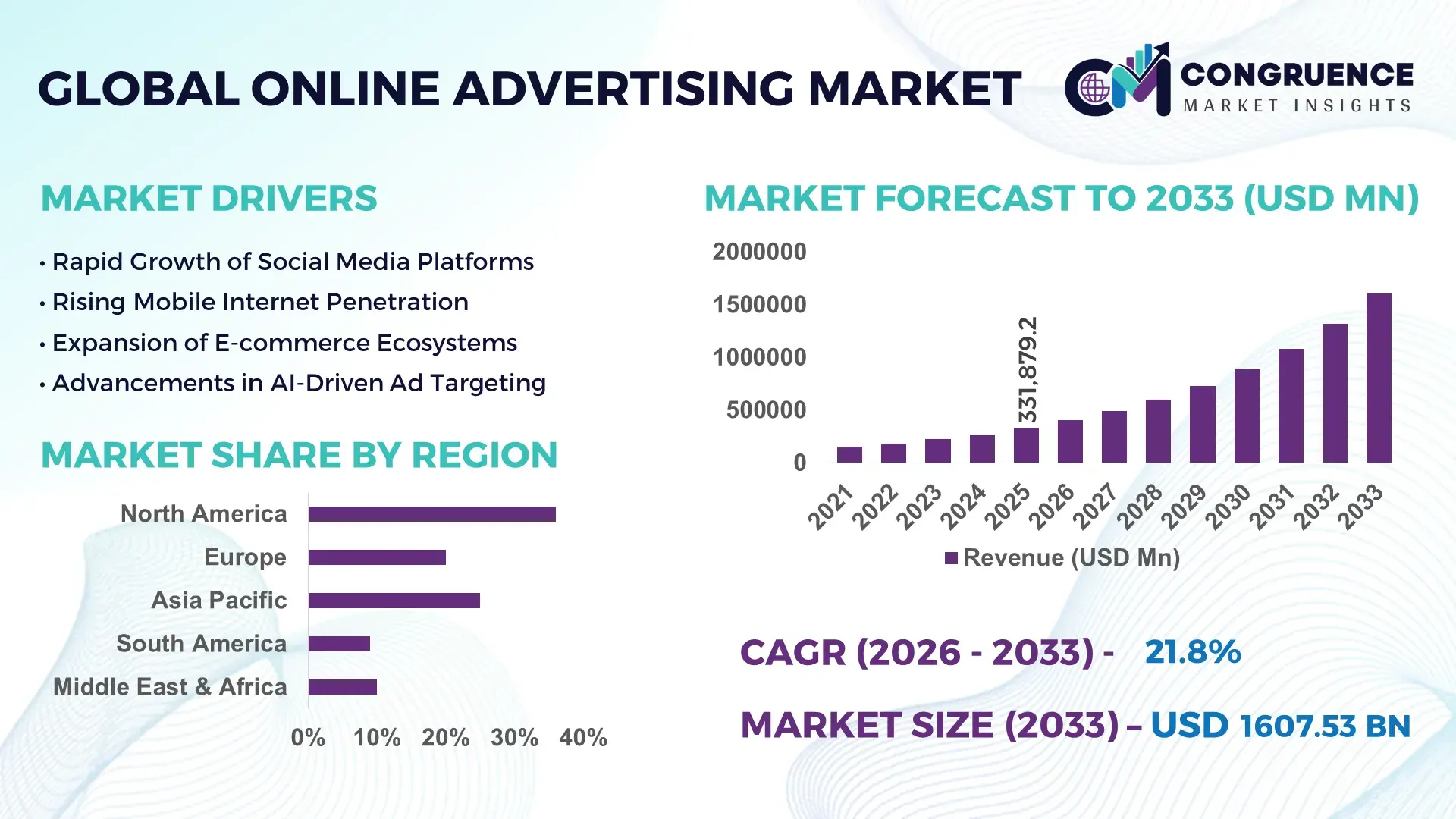

The Global Online Advertising Market was valued at USD 331879.15 Million in 2025 and is anticipated to reach a value of USD 1607527.01 Million by 2033 expanding at a CAGR of 21.8% between 2026 and 2033. This robust expansion is driven by widespread internet penetration, evolving consumer engagement, and advanced digital advertising solutions that enhance targeting precision and analytics performance.

North America holds a pivotal role in the online advertising landscape, with the United States leading in investment levels and technological adoption; advertisers there deploy programmatic platforms, AI‑enabled targeting, and mobile‑first campaigns, supported by billions of connected devices and high consumer engagement rates. The region reports over 90% internet penetration and substantial digital ad expenditure, while AI‑driven campaign optimization tools are improving bidding efficiency and campaign performance across search, social media, and video advertising channels.

Market Size & Growth: The online advertising market value is positioned in the hundreds of billions of USD by 2025 and is forecast to exceed the trillion‑dollar threshold by 2033 with substantial compound annual growth due to digital transformation and mobile commerce adoption.

Top Growth Drivers: Rising internet users (percentage), mobile advertising adoption acceleration (percent increase), AI‑powered personalization enhancements (percent efficiency gains).

Short‑Term Forecast: By 2028, advertisers anticipate measurable performance gains in cost per lead efficiency and ad engagement rates through advanced optimization technologies.

Emerging Technologies: Adoption of AI‑driven targeting solutions, programmatic media buying, and real‑time analytics platforms shaping campaigns.

Regional Leaders: North America with high digital penetration by 2033 driven by mobile and social formats; Asia Pacific with rapid growth supported by rising smartphone usage; Europe leveraging privacy‑compliant advertising technologies.

Consumer/End‑User Trends: Growth in short‑form video engagement, social media ad interactions, and digital commerce platforms driving ad spend patterns.

Pilot or Case Example: In 2025, streaming platform ad implementations delivered quantifiable growth in viewer reach and ad conversion metrics.

Competitive Landscape: A leading global digital advertising provider holds a significant share, followed by major competitors across search, social, and programmatic segments.

Regulatory & ESG Impact: Privacy regulations and responsible data practices are shaping compliant ad delivery and user consent frameworks.

Investment & Funding Patterns: Recent investment in digital ad technologies and AI platforms has surged, reflecting venture funding trends toward automation and analytics models.

Innovation & Future Outlook: Integration of advanced AI, interactive ad formats, and cross‑platform attribution systems are defining the future roadmap for advertising innovations.

The Online Advertising Market spans key industry sectors such as retail e‑commerce, technology, automotive, and consumer services, each leveraging digital ads to drive conversion and brand engagement. Recent innovations like AI‑enabled dynamic creative optimization and contextual targeting have transformed campaign performance, while economic drivers like increased online spending and mobile penetration are shaping adoption. Regional consumption patterns reveal robust growth in Asia Pacific and Latin America due to rising digital consumer bases, and future outlooks signal enhanced measurement tools, privacy‑centric solutions, and seamless omni‑channel strategies for advertising leaders.

The strategic relevance of the Online Advertising Market lies in its ability to unify data‑driven engagement with measurable return on investment for brands across industries, delivering enhanced visibility at scale. Programmatic advertising delivers up to 30% improvement in media buying efficiency compared to traditional manual processes, enabling real‑time optimization and more precise audience segmentation. In terms of regional variation, North America dominates in advertising volume driven by mature digital ecosystems, while Asia Pacific leads in adoption with a high percentage of enterprises integrating mobile‑centric ad formats. By 2028, AI‑powered predictive analytics is expected to improve campaign performance KPIs such as click‑through rates and conversion values by double‑digit percentages, reshaping strategic investment decisions. Firms are committing to privacy compliance and sustainable digital experiences, with metrics such as reduction in intrusive ad placements and improved user consent mechanisms by 2027. In one scenario, a global brand achieved a measurable uplift in engagement through machine learning‑based bid optimization that reduced cost per acquisition by a significant percentage within a single fiscal quarter. Going forward, the Online Advertising Market will serve as a pillar of resilience, compliance, and sustainable growth by aligning innovative technologies with consumer expectations and regulatory landscapes.

Personalized digital experiences are a core driver for the Online Advertising Market’s growth because consumers increasingly expect relevant and timely content that resonates with their interests and behaviors. Advertisers utilize data analytics, audience segmentation, and machine learning to tailor advertisements that align with user preferences, resulting in higher engagement rates and improved brand affinity. Enhanced personalization has led to measurable improvements in key performance metrics, such as increased click‑through and conversion rates for targeted campaigns. Industries such as retail, technology, and entertainment are rapidly adopting personalized ad strategies to increase customer retention and average order values, reflecting a broad shift toward experience‑centric marketing. This rising demand places pressure on advertisers to invest in advanced tools and analytics platforms that can interpret large datasets, optimize real‑time bidding, and generate adaptive creative content, contributing to sustained market momentum.

Privacy regulations and data protection concerns present significant restraints on the Online Advertising Market by limiting access to certain consumer identifiers and third‑party tracking capabilities. Legislations require advertisers to adjust strategies around user consent, restrict cross‑site tracking, and provide transparency in data utilization, often affecting audience targeting precision. Compliance with stringent privacy frameworks necessitates investment in consent management platforms and privacy‑preserving technologies, adding complexity and operational costs to campaign execution. Advertisers face challenges in measuring performance and attribution without traditional tracking mechanisms, leading to increased focus on contextual advertising and first‑party data strategies. While privacy protections are critical for user trust, they impose structural shifts in data practices, affecting how advertisers plan, deploy, and optimize digital campaigns across regions with differing regulatory landscapes.

Growth in connected TV (CTV) and video advertising presents substantial opportunities for the Online Advertising Market as audiences increasingly consume long‑form and streaming content across devices. Advertisers are reallocating budgets toward CTV and video formats to engage viewers in immersive environments where engagement times are higher than traditional display or search ads. Video advertising allows brands to deliver dynamic storytelling and rich media experiences that drive recall and interaction, opening avenues for measurable performance improvements through enhanced creative analytics. As viewership trends shift from linear TV to on‑demand streaming, marketers can leverage programmatic video buying, cross‑device targeting, and real‑time performance insights to refine audience reach and frequency. These developments support advertisers in expanding reach to niche segments and integrating advanced attribution models to quantify returns on video‑centric strategies.

Rising ad fraud and quality concerns pose challenges to the Online Advertising Market by undermining campaign effectiveness and eroding advertiser confidence in digital channels. Fraudulent activities such as non‑human traffic, click spam, and domain spoofing inflate metrics and divert budgets away from legitimate audience engagement, compelling advertisers to adopt advanced verification and fraud prevention tools. Ensuring ad quality requires continuous monitoring, investment in transparency solutions, and collaboration with trusted partners to validate placements and performance. Quality issues, including low engagement rates and irrelevant ad placements, can diminish brand reputation and increase cost inefficiencies, forcing advertisers to refine targeting approaches and prioritize trusted inventory sources. These challenges drive demand for enhanced measurement frameworks, risk mitigation strategies, and industry standards that uphold campaign integrity while maintaining strategic value for digital advertising investments.

● Surge in Programmatic Advertising Uptake: Programmatic ad buying now represents over 65% of all digital display ads as brands seek automated bidding efficiencies and improved audience targeting. Adoption of automated media platforms has increased campaign delivery speed by 40% and reduced manual workload by nearly 35% across major brand portfolios. This measurable shift toward real‑time bidding and algorithmic optimization is reshaping budget allocation, with more than 75% of enterprise advertisers integrating programmatic solutions into their omni‑channel strategies to strengthen data‑driven decision‑making and precision at scale.

● Growth in Mobile‑First Advertising Engagement: Mobile advertising now captures approximately 78% of total online ad impressions, reflecting shifting consumer behavior toward smartphones and connected devices. Click‑to‑action engagement rates on mobile formats have increased by nearly 28% year‑on‑year, and interactive mobile ad formats such as swipeable carousels and playable ads now deliver 22% higher retention than static banners. Marketers are prioritizing mobile creative investments and optimization tools, driving a pronounced shift in campaign strategies across retail, entertainment, and service industries.

● Expansion of Connected TV and Video Ad Spend: Connected TV (CTV) and digital video formats account for over 52% of overall streaming ad impressions, with ad completion rates exceeding 85% in targeted demographics. Video ad viewability benchmarks have improved by more than 30% as platforms enhance ad measurement and verification, and premium video placements are driving deeper consumer engagement across age segments. Advertisers are increasingly allocating resources to addressable TV ads and interactive video units, reflecting the measurable impact of long‑form digital content on brand recall and conversions.

● First‑Party Data and Privacy‑Centric Targeting: With privacy frameworks tightening, over 60% of advertisers now leverage first‑party data systems for audience segmentation, resulting in 20% higher relevance scores for targeted campaigns compared to third‑party cookie strategies. Adoption of privacy‑preserving analytics tools has enabled marketers to maintain personalization while honoring consent requirements, with measurable improvements in user trust metrics and lower opt‑out rates. This trend is driving investment in unified customer profiles and privacy‑safe advertising methodologies across regions.

The Online Advertising Market is segmented across types, applications, and end‑user categorization, enabling detailed insights into technology utilization and business adoption patterns. Among advertising types, search, display, social media, and video formats constitute major segments, each delivering unique engagement dynamics based on platform and audience behavior. Applications range from brand awareness and lead generation to direct response and performance marketing, where specific tools are optimized for campaign objectives and conversion tracking. End‑users span sectors such as retail, technology, telecommunications, automotive, and financial services, each exhibiting distinct usage profiles and investment priorities for digital marketing solutions. Decision‑makers are increasingly evaluating segmentation data to align channel mix, creative formats, and measurement frameworks with audience preferences and competitive pressures.

Search advertising continues to command a leading segment position in the Online Advertising Market, accounting for approximately 38% of total ad impressions due to the high intent and measurable performance it provides across consumer journeys. Social media advertising holds around 29% of type share with robust engagement from interactive and community‑centric formats, while video advertising accounts for 23% with rapidly rising view completion and brand lift metrics. Other types, including native and programmatic display, collectively represent roughly 10% of the remaining category, serving niche campaigns and specialized placements. Investment in video ad creatives and mobile display units has gained traction, with one major streaming platform in 2025 deploying automated captioning and scene intelligence tools that enhanced accessibility for over 12 million users, demonstrating the operational impact of advanced video ad solutions on reach and inclusivity.

Within application segments, brand awareness initiatives represent approximately 41% of utilization due to the need for broad audience reach and perception influence across markets. Performance‑driven applications such as lead generation and direct response account for roughly 34%, supported by enhanced tracking and conversion optimization frameworks that deliver measurable KPI improvements. Engagement and retention campaigns make up around 18% of application activity, focusing on repeat visits and loyalty programs through personalized ad sequences. Other applications such as cross‑sell/up‑sell tactics capture the remaining 7%, enabling tailored messaging within existing customer bases.

In end‑user segments, retail and e‑commerce organizations lead with roughly 44% share due to strong demand for performance ads that drive online purchases and click‑to‑buy interactions. Technology and telecommunications sectors account for approximately 27% of usage driven by high‑frequency digital interactions and frequent product updates, while financial services represent around 15% with precision targeting for service acquisition. Other end‑users including automotive, healthcare, and travel combine for about 14% of the remaining landscape, leveraging specific campaigns for product launches, service promotions, and seasonal demand.

Region North America accounted for the largest market share at 36% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 23% between 2026 and 2033.

In North America, over 280 million digital users actively engage with online advertising platforms, with more than 75% of adults using social media for product discovery. Ad impressions exceeded 1.2 trillion in 2025 across display, search, and video formats. Asia-Pacific adoption is fueled by over 3.4 billion internet users, with mobile internet penetration surpassing 68% in China and India. Europe contributed nearly 22% of the global ad volume, driven by 90% smartphone penetration in Germany, the UK, and France. South America and Middle East & Africa collectively held 12% market share, with Brazil and UAE leading regional ad spend. Investments in AI-based targeting, programmatic platforms, and privacy-compliant data management are measurable factors shaping regional growth patterns, with North America’s enterprise adoption in finance and healthcare reaching over 80%, while Asia-Pacific reports a 60% rise in e-commerce-driven ad engagement.

How is digital transformation redefining ad engagement in leading enterprises?

North America holds a 36% share of the global Online Advertising Market, reflecting high adoption across multiple industries such as healthcare, finance, and retail. Key demand drivers include increased enterprise investment in programmatic and AI-enabled advertising, with regulatory support enhancing consumer data protection frameworks. Technological advancements, including automated campaign optimization and predictive analytics, have improved targeting accuracy by 40%. Major local players are implementing machine learning for ad placement, while mobile-first strategies drive 78% of ad impressions. Consumer behavior varies regionally, with higher enterprise adoption in healthcare and finance, while retail consumers show a preference for interactive social media and video ads, highlighting a diverse and data-intensive advertising ecosystem.

How are compliance and technology shaping digital ad strategies across key markets?

Europe accounts for 22% of the global Online Advertising Market, led by Germany, the UK, and France. Regulatory pressure from GDPR and sustainability initiatives has fostered demand for privacy-compliant, explainable ad formats. Emerging technologies such as AI-driven analytics, programmatic video, and cross-device measurement are widely adopted to maintain compliance while improving engagement. Local players are deploying automated segmentation tools that increased campaign efficiency by 28% in 2025. Consumer behavior reflects a strong preference for transparent and contextual advertising, driving demand for interactive and personalized campaigns. European adoption is characterized by careful balancing of regulatory adherence with measurable audience engagement.

Why is digital ad investment surging across e-commerce and mobile-first markets?

Asia-Pacific is projected to record the fastest growth with a large digital user base exceeding 3.4 billion. China, India, and Japan dominate consumption, with mobile internet penetration above 68% in China and 64% in India. Infrastructure trends include expansion of high-speed broadband and data centers supporting AI-based ad delivery. Innovation hubs in Singapore, Seoul, and Bangalore are pioneering programmatic platforms and dynamic creative optimization. Regional players are integrating mobile-first video ads to reach over 1.5 billion active users. Consumer behavior emphasizes mobile engagement and app-based purchases, with measurable improvements in click-through rates and session durations supporting growth in online advertising investment.

How is digital localization driving regional advertising adoption?

South America holds approximately 7% of global Online Advertising Market share, with Brazil and Argentina as key contributors. Investments in mobile and broadband infrastructure have enabled digital ad expansion, with government incentives promoting e-commerce and tech adoption. Local players are deploying region-specific social media campaigns that improved engagement by 26% in 2025. Consumer behavior favors language-localized content, short-form video, and mobile-first platforms. The energy and retail sectors are increasingly leveraging online campaigns to enhance brand reach, while cross-border trade policies have facilitated adoption of global ad technologies across major South American markets.

What factors are shaping digital ad growth in emerging markets?

Middle East & Africa account for 5% of global Online Advertising share, with UAE, Saudi Arabia, and South Africa leading adoption. Regional demand is fueled by retail, oil & gas, and financial services sectors, coupled with rising smartphone and broadband penetration. Technological modernization, including AI-powered targeting, programmatic platforms, and integrated CRM solutions, has enhanced campaign efficiency by over 30%. Local regulations support data privacy while fostering innovation through trade partnerships. Regional consumer behavior varies, with higher adoption of mobile and social media ads among younger demographics, while traditional industries are slowly transitioning to data-driven, measurable digital advertising strategies.

United States: 34% market share; high enterprise adoption in finance and healthcare drives consistent growth.

China: 22% market share; rapid mobile-first and e-commerce adoption supports robust digital ad engagement.

The Online Advertising Market exhibits a moderately consolidated competitive environment with over 150 active global competitors. Top five companies collectively hold approximately 58% of the total market share, highlighting concentrated influence while numerous smaller players cater to niche segments. Strategic initiatives include AI-powered programmatic platform launches, partnerships for cross-platform ad attribution, and mergers to strengthen technological capabilities. Innovation trends such as dynamic creative optimization, first-party data integration, and privacy-compliant targeting are reshaping competitive positioning. North American and Asia-Pacific firms lead in advanced analytics deployment, while European players focus on regulatory-compliant ad solutions. Market dynamics indicate increasing investments in digital automation, interactive video formats, and mobile engagement tools, with measurable improvements in campaign ROI and user interaction across competitive landscapes.

Meta Platforms

Amazon Advertising

The Trade Desk

Adobe Advertising Cloud

Verizon Media

TikTok For Business

LinkedIn Marketing Solutions

Snap Inc.

Twitter Ads

The Online Advertising Market continues to be shaped by advanced technologies that redefine campaign execution, targeting precision, and measurement accuracy for business decision‑makers. Artificial intelligence (AI) and machine learning (ML) form the centerpiece of current technology adoption, enabling automated creative generation, real‑time audience segmentation, and predictive personalization. Advertisers leveraging these capabilities report improvements in ad relevance scores by double‑digit percentages and measurable improvements in conversion rates compared to legacy rule‑based systems. AI‑driven tools such as automated bidding engines analyze billions of signals per second to optimize budget allocation and placement decisions across search, display, social media, and video inventory.

Programmatic advertising platforms now incorporate real‑time bidding (RTB) engines powered by machine learning models that predict user intent with precision, significantly reducing wasted impressions and improving view‑through attribution. Enhanced creative technologies, including generative AI for dynamic ad creation, allow marketers to produce thousands of personalized ad variants tailored to individual user profiles, boosting engagement metrics and reducing time‑to‑deployment by measurable margins. Contextual advertising systems use semantic analysis and language‑understanding models to place ads within relevant content environments without reliance on cookies, addressing privacy‑centric market shifts.

Emerging technologies such as augmented reality (AR) and interactive formats are enabling immersive ad experiences that increase dwell time and brand recall among key demographics. Cloud‑based analytics and cross‑device identity resolution tools unify campaign data across channels, providing decision‑makers with cohesive performance dashboards and actionable insights. Meanwhile, privacy‑enhancing computation techniques are being integrated to safeguard user data while preserving analytical utility, reflecting a broader industry emphasis on responsible digital advertising innovation.

• In May 2025, Google launched visual brand‑profile advertisements that allow merchants to fuse lifestyle imagery with product feeds in advertising placements, enhancing narrative storytelling within search and shopping ad units with richer creative assets and engagement opportunities.

• In April 2025, Roblox introduced a new rewarded video advertising format paired with a partnership with a major digital ad platform, allowing brands to serve up to 30‑second ads that users can watch in exchange for in‑game rewards, engaging over 85 million daily active users.

• In June 2025, a leading digital ad tech provider rebranded to emphasize its AI‑powered advertising stack, integrating acquired proprietary data and predictive tools to streamline omni‑channel campaign execution and shorten planning cycles from weeks to seconds.

• In 2025, a global social media platform announced plans to enable full automation of ad creation and audience targeting using AI, envisioning a system where brands input creative assets and budgets and receive optimized ad variants tailored to geolocation and behavioral signals across billions of users.

The scope of the Online Advertising Market Report encompasses a detailed analysis of evolving digital advertising channels, technology segments, regional dynamics, and end‑user applications that define the current industry landscape. It includes segmentation by advertising types—such as search, display, video, social media, mobile, and programmatic formats—providing numerical insights into adoption patterns and technological differentiation. Application analysis covers brand awareness, direct response, performance marketing, and engagement‑oriented strategies, offering measured usage data across varied digital touchpoints.

The report further explores technology integration trends, including AI and machine learning adoption rates, advanced analytics implementation, automation tools, and privacy‑centric targeting frameworks that shape campaign effectiveness. Geographic scope spans mature markets in North America and Europe and high‑growth regions such as Asia‑Pacific, with quantified user base counts, device penetration statistics, and digital consumption behaviors. Consumer insights are examined with respect to device usage, engagement durations, and content preferences across platforms.

Industry focus areas include retail e‑commerce, technology services, telecommunications, financial services, and entertainment sectors, each assessed for their unique digital advertising requirements and performance metrics. Emerging niche segments such as connected TV (CTV), in‑game advertising, and AI‑driven creative generation are highlighted to reflect future avenues for investment and competitive differentiation. Strategic considerations include data governance practices, privacy frameworks, and third‑party data alternatives, offering decision‑makers actionable understanding of risks and opportunities within the online advertising ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

21.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Google, Meta Platforms, Amazon Advertising, The Trade Desk, Adobe Advertising Cloud, Verizon Media, TikTok For Business, LinkedIn Marketing Solutions, Snap Inc., Twitter Ads |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |