Reports

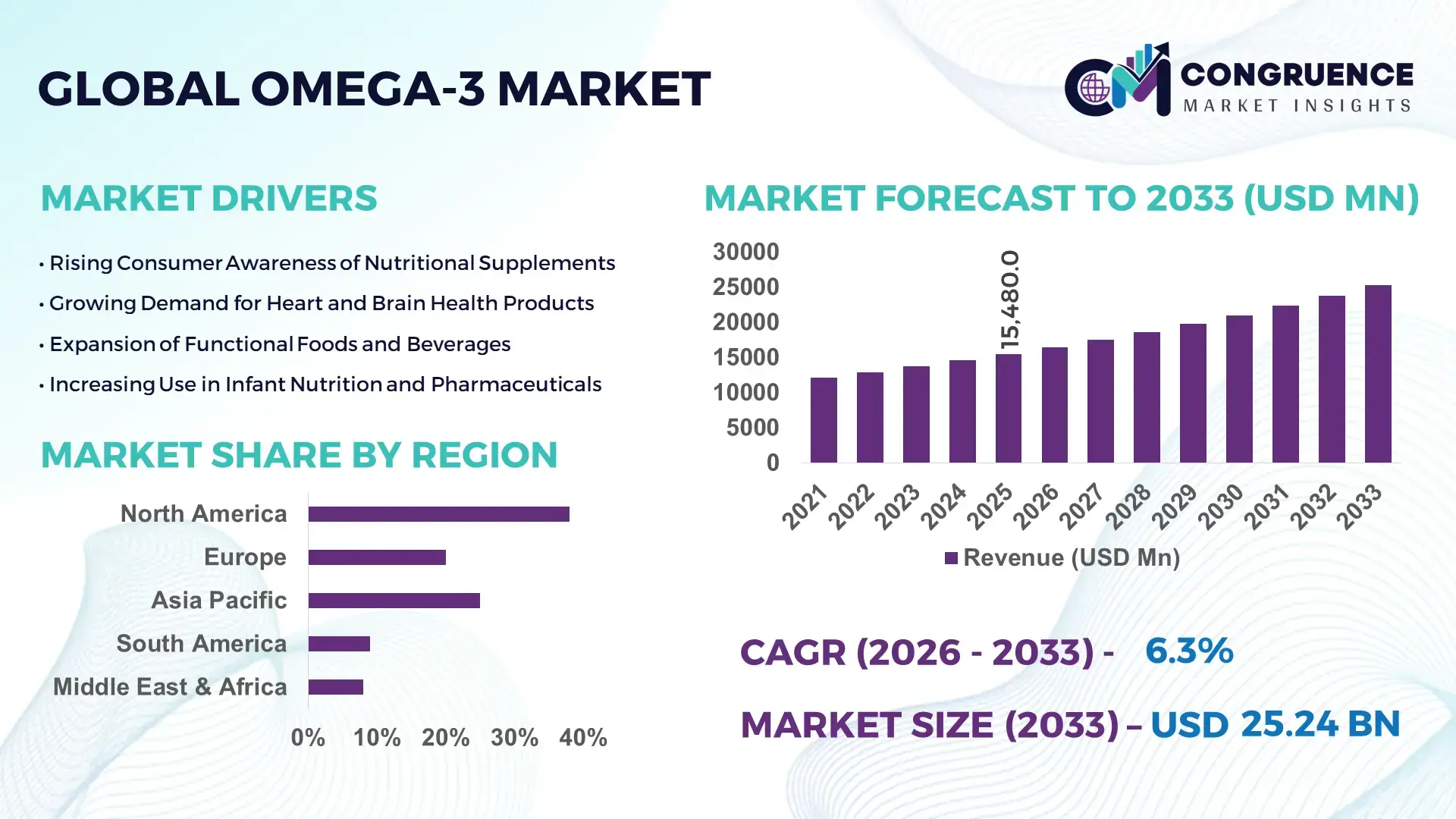

The Global Omega-3 Market was valued at USD 15480 Million in 2025 and is anticipated to reach a value of USD 25236.96 Million by 2033 expanding at a CAGR of 6.3% between 2026 and 2033. Rising consumer awareness of cardiovascular health benefits and the growing integration of omega-3 ingredients in functional foods, nutraceuticals, and clinical nutrition products are accelerating market expansion worldwide.

The United States remains a pivotal hub for the Omega-3 market with advanced production technologies and large-scale nutraceutical manufacturing capacity. The country produces over 200,000 metric tons of fish oil annually for dietary supplements, pharmaceuticals, and fortified food products. Omega-3 dietary supplements are consumed by more than 18% of adults in the U.S., according to health nutrition surveys. Significant investments exceeding USD 1 billion have been directed toward algae-based omega-3 production facilities and biotechnology innovations. The pharmaceutical and infant nutrition sectors account for nearly 35% of omega-3 ingredient applications in the country, while functional food manufacturers integrate DHA and EPA oils into dairy alternatives, beverages, and sports nutrition products.

• Market Size & Growth: The Omega-3 Market stood at USD 15,480 Million in 2025 and is projected to reach USD 25,236.96 Million by 2033, expanding at a CAGR of 6.3% due to rising adoption of functional nutrition, dietary supplements, and preventive healthcare products.

• Top Growth Drivers: Functional food adoption increased by 42%, preventive health supplement usage rose by 37%, and clinical nutrition demand expanded by 31%.

• Short-Term Forecast: By 2028, omega-3 ingredient formulation efficiency in nutraceutical manufacturing is expected to improve by nearly 18%, while production costs could decline by around 12%.

• Emerging Technologies: Algae-based omega-3 extraction, microencapsulation for enhanced bioavailability, and precision fermentation technologies are transforming sustainable omega-3 production.

• Regional Leaders: North America is projected to reach approximately USD 8.6 Billion by 2033 due to strong supplement consumption, Europe could surpass USD 7.4 Billion driven by pharmaceutical-grade omega-3 applications, while Asia-Pacific may exceed USD 6.9 Billion with rapid functional food adoption.

• Consumer/End-User Trends: Nutraceutical companies, pharmaceutical manufacturers, and infant nutrition brands collectively account for over 65% of global omega-3 ingredient consumption.

• Pilot or Case Example: In 2024, a large-scale algae-derived DHA production pilot improved omega-3 yield efficiency by nearly 22% through advanced fermentation systems.

• Competitive Landscape: DSM-Firmenich holds roughly 17% share, followed by BASF SE, Croda International, Cargill Incorporated, and Pelagia AS as prominent global suppliers.

• Regulatory & ESG Impact: Governments are promoting sustainable marine sourcing and algae-based omega-3 alternatives to reduce pressure on global fish stocks by up to 20% over the next decade.

• Investment & Funding Patterns: Over USD 2.4 Billion has been invested globally in omega-3 biotechnology, algae cultivation systems, and nutraceutical manufacturing expansion since 2022.

• Innovation & Future Outlook: Advances in encapsulation technology, plant-based omega-3 oils, and high-purity EPA/DHA formulations are shaping next-generation functional nutrition and pharmaceutical applications.

The Omega-3 market is strongly influenced by key industry sectors including nutraceuticals, functional foods, pharmaceuticals, and animal nutrition. Nutraceutical applications account for nearly 40% of global demand, while functional food and beverage formulations contribute about 25%. Technological innovation such as enzymatic concentration processes and high-purity EPA/DHA isolation techniques has improved omega-3 stability and absorption. Regulatory frameworks promoting heart-health labeling and sustainable marine sourcing continue to support industry growth. Asia-Pacific markets are witnessing accelerated consumption due to rising disposable income and preventive healthcare awareness, while European manufacturers are expanding algae-derived omega-3 production to address environmental concerns and supply stability.

The Omega-3 Market holds strategic importance in global nutrition, pharmaceutical innovation, and preventive healthcare systems. Nutraceutical manufacturers are increasingly integrating advanced algae-based omega-3 production to ensure sustainable supply chains. Precision fermentation technology delivers nearly 28% higher DHA yield compared to traditional fish-oil extraction methods, improving production efficiency and reducing marine resource dependence. North America dominates in production volume, while Europe leads in regulatory adoption with more than 45% of nutraceutical enterprises implementing certified sustainable omega-3 sourcing frameworks.

In the short term, industry adoption of microencapsulation technology is expected to improve omega-3 ingredient stability and shelf life by nearly 20% by 2027, supporting expanded applications in beverages, dairy products, and clinical nutrition formulations. Companies are also committing to ESG targets, including reducing fish-derived raw material dependency by 30% by 2030 through algae cultivation and plant-based omega-3 alternatives. In 2024, a biotechnology initiative in Norway improved omega-3 extraction efficiency by 24% using advanced enzymatic processing techniques. These developments position the Omega-3 Market as a critical component supporting sustainable nutrition, regulatory compliance, and resilient global health supply chains.

Growing consumer focus on preventive healthcare is significantly accelerating omega-3 consumption worldwide. Clinical studies indicate that omega-3 fatty acids can reduce triglyceride levels by up to 30%, increasing their use in cardiovascular health supplements and prescription formulations. Over 60% of global nutraceutical manufacturers now incorporate omega-3 ingredients into dietary supplements, fortified foods, and medical nutrition products. In addition, infant nutrition companies increasingly include DHA-rich oils in formula products, as DHA supports brain and visual development during early childhood. Rising adoption of sports nutrition and cognitive health supplements is also contributing to demand, with omega-3 formulations widely used in performance recovery and mental wellness products.

Omega-3 production remains partially dependent on marine resources such as anchovies, sardines, and mackerel, creating supply volatility linked to environmental conditions and fishing regulations. Global fish oil production fluctuates between 900,000 and 1.1 million metric tons annually due to seasonal catch variations and sustainability restrictions. Climate change and stricter fisheries management policies have reduced fish harvesting quotas in several regions, limiting raw material availability for omega-3 extraction. Additionally, purification and concentration processes required to produce pharmaceutical-grade EPA and DHA significantly increase processing complexity and production costs, creating barriers for small and mid-scale manufacturers entering the market.

The rapid development of algae-based omega-3 production presents a major growth opportunity for the industry. Microalgae cultivation systems can produce high-purity DHA oils without relying on marine fish stocks, supporting sustainable supply chains. Commercial algae farms currently generate more than 70,000 metric tons of omega-3 oils annually, with capacity expected to expand as biotechnology companies invest in large-scale photobioreactor facilities. These plant-based omega-3 alternatives are particularly attractive for vegan nutraceutical products and environmentally conscious consumers. In addition, algae-derived omega-3 ingredients offer improved traceability and purity levels, making them suitable for pharmaceutical formulations and premium functional nutrition applications.

The Omega-3 market faces stringent regulatory requirements related to product purity, contaminant levels, and labeling standards across multiple jurisdictions. Manufacturers must comply with strict limits on heavy metals, oxidation levels, and environmental contaminants in fish-derived oils. Advanced purification technologies such as molecular distillation are necessary to meet pharmaceutical and nutraceutical grade specifications, increasing production complexity. Furthermore, regulatory authorities in regions such as Europe and North America require detailed clinical evidence to support health claims related to cardiovascular and cognitive benefits. These compliance requirements raise operational costs and extend product approval timelines, creating significant barriers for new omega-3 product launches and international market expansion.

• Rapid Expansion of Algae-Based Omega-3 Production:

Algae-derived omega-3 oils are gaining substantial momentum as companies seek sustainable alternatives to fish-based raw materials. Global microalgae cultivation capacity exceeded 80,000 metric tons of omega-3 oils in 2024, representing a production increase of nearly 35% compared to 2021 levels. More than 40% of new omega-3 manufacturing projects now include algae fermentation systems to reduce marine resource dependency. Pharmaceutical-grade DHA extracted from algae demonstrates purity levels exceeding 95%, supporting expanded use in clinical nutrition and infant formula applications. In Europe alone, algae-based omega-3 products account for approximately 28% of newly launched vegan dietary supplements, reflecting strong consumer demand for plant-based nutrition solutions and environmentally responsible ingredient sourcing.

• Surge in Functional Food and Beverage Fortification:

Food and beverage manufacturers are increasingly incorporating omega-3 fatty acids into everyday consumer products. Nearly 32% of newly introduced functional dairy products globally now contain added EPA or DHA ingredients. In North America, fortified beverages containing omega-3 oils grew by 26% in product launches between 2022 and 2024. Microencapsulation technologies are enabling omega-3 oils to remain stable in high-temperature processing environments, improving shelf stability by approximately 18%. Breakfast cereals, dairy alternatives, and nutrition bars represent nearly 22% of new omega-3 fortified food launches globally, reflecting the growing demand for preventive health foods and convenient nutritional supplementation.

• Growing Adoption in Clinical Nutrition and Pharmaceutical Applications:

Clinical nutrition products incorporating omega-3 ingredients are expanding rapidly as healthcare providers emphasize preventive care and cardiovascular management. Approximately 48% of prescription lipid management therapies now include purified EPA formulations targeting triglyceride reduction. Omega-3 fatty acids have demonstrated the ability to reduce triglyceride levels by up to 30% in controlled clinical applications. Hospitals and clinical nutrition providers are also incorporating DHA-enriched formulations into enteral feeding products, with adoption rates increasing by nearly 21% across hospital nutrition programs since 2021. Pharmaceutical manufacturers are investing heavily in high-purity EPA and DHA extraction technologies to support new therapeutic formulations and regulatory-compliant drug development.

• Increased Investment in Sustainable Marine Sourcing Technologies:

Sustainability has become a central priority across the omega-3 value chain, prompting increased investments in responsible marine harvesting and traceability technologies. More than 65% of global fish oil producers have implemented certified sustainable fishing programs to ensure responsible resource management. Digital traceability systems now track over 70% of fish-derived omega-3 supply chains in developed markets, improving transparency and regulatory compliance. Advanced molecular distillation processes have improved contaminant removal efficiency by nearly 40%, ensuring pharmaceutical-grade purity standards. Additionally, governments in several regions have introduced sustainability frameworks aimed at reducing overfishing risks while supporting stable omega-3 supply chains for food, nutraceutical, and pharmaceutical industries.

The Omega-3 market is segmented by type, application, and end-user industries, each contributing to diverse demand patterns across healthcare, nutrition, and food manufacturing sectors. Product types primarily include EPA, DHA, and ALA formulations used in dietary supplements, pharmaceuticals, and fortified foods. Applications range from functional foods and nutraceuticals to clinical nutrition and animal feed solutions. End-user demand is dominated by nutraceutical manufacturers, followed by pharmaceutical companies and food producers incorporating omega-3 ingredients into health-focused products. Growing interest in preventive healthcare, plant-based nutrition alternatives, and high-purity omega-3 formulations is reshaping segmentation dynamics, with algae-derived omega-3 ingredients gaining increasing traction among health-conscious consumers and sustainable food manufacturers.

The Omega-3 market includes several product types, primarily eicosapentaenoic acid (EPA), docosahexaenoic acid (DHA), and alpha-linolenic acid (ALA), each serving distinct nutritional and pharmaceutical applications. DHA currently represents the leading product type, accounting for nearly 44% of global omega-3 ingredient adoption due to its critical role in infant brain development, cognitive health, and vision support. DHA oils are widely integrated into infant formula, dietary supplements, and clinical nutrition products. EPA holds approximately 31% of the market and is increasingly used in cardiovascular health formulations due to its effectiveness in reducing triglyceride levels and supporting heart health. However, ALA-based omega-3 products derived from plant oils such as flaxseed and chia are emerging as the fastest-growing segment, expanding at an estimated CAGR of 8.1%. Growth is largely driven by increasing vegan dietary preferences and consumer demand for plant-based nutrition alternatives.

Other omega-3 formulations, including combined EPA-DHA blends and specialty concentrates used in pharmaceutical therapies, collectively contribute about 25% of the market. These products are commonly utilized in clinical nutrition and prescription cardiovascular treatments.

The Omega-3 market serves several key application sectors including dietary supplements, functional foods and beverages, pharmaceuticals, and animal nutrition. Dietary supplements currently represent the dominant application, accounting for nearly 46% of global omega-3 consumption. The popularity of preventive healthcare and heart health supplements has driven widespread adoption of omega-3 capsules, soft gels, and liquid formulations among adults and aging populations. Functional foods and beverages hold around 27% of the application landscape, including omega-3 fortified dairy products, breakfast cereals, beverages, and nutrition bars. However, pharmaceutical applications are the fastest-growing segment, expanding at an estimated CAGR of 7.6% due to increasing clinical evidence supporting EPA and DHA in cardiovascular and metabolic health treatments.

Other applications including infant nutrition and animal feed collectively represent approximately 27% of market usage. Infant formula manufacturers increasingly incorporate DHA oils to support brain development, while aquaculture and pet nutrition sectors integrate omega-3 ingredients to improve animal health and product quality.

End-user demand in the Omega-3 market is led by nutraceutical manufacturers, pharmaceutical companies, food and beverage producers, and animal nutrition suppliers. Nutraceutical companies account for the largest share, representing nearly 42% of global omega-3 ingredient consumption due to widespread production of dietary supplements targeting heart health, cognitive performance, and immune support. Pharmaceutical companies hold approximately 28% of the market as purified EPA and DHA ingredients are incorporated into prescription cardiovascular treatments and clinical nutrition therapies. However, the food and beverage industry is emerging as the fastest-growing end-user segment, expanding at an estimated CAGR of 7.4% as manufacturers introduce omega-3 fortified functional foods, dairy alternatives, and sports nutrition products.

Other end-users including aquaculture and pet nutrition sectors collectively contribute about 30% of the market. Omega-3 enriched feed formulations are increasingly used in aquaculture to improve fish health and enhance nutritional value for consumers. Adoption of omega-3 enriched pet nutrition products has also increased by nearly 18% over the past three years.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

North America recorded omega-3 consumption exceeding 420,000 metric tons in 2025 due to strong dietary supplement demand and advanced nutraceutical manufacturing capacity. Europe held approximately 29% share supported by strict nutrition labeling regulations and sustainable marine sourcing initiatives. Asia-Pacific accounted for nearly 24% of global demand with rapid growth in functional foods and infant nutrition products across China, India, and Japan. South America represented around 6% of global consumption due to strong fish oil production infrastructure in Peru and Chile, while the Middle East & Africa contributed nearly 3% supported by expanding pharmaceutical and dietary supplement distribution networks.

How Is Preventive Healthcare Adoption Transforming Demand for Nutritional Lipids?

North America holds approximately 38% of global Omega-3 market consumption, driven primarily by the nutraceutical, pharmaceutical, and functional food industries. The United States alone accounts for nearly 75% of regional demand as more than 18% of adults regularly consume omega-3 dietary supplements. Government-backed nutritional guidelines encouraging cardiovascular health awareness continue to stimulate demand for EPA and DHA formulations. Technological advancements such as microencapsulation and molecular distillation have improved omega-3 ingredient stability by nearly 20%, supporting broader food and beverage applications. A leading regional player, DSM-Firmenich, has expanded algae-derived omega-3 production capacity in the United States to supply pharmaceutical-grade DHA oils. Consumer behavior reflects strong preventive healthcare adoption, with omega-3 supplements commonly used in wellness, sports nutrition, and cardiovascular health management.

What Factors Are Accelerating Sustainable Nutraceutical Ingredient Innovation?

Europe represents nearly 29% of the global Omega-3 market, with strong demand across Germany, the United Kingdom, and France. The region’s strict regulatory framework for food safety and nutritional labeling has accelerated adoption of high-purity omega-3 ingredients in pharmaceuticals and fortified foods. Sustainability initiatives promoted by European regulatory bodies encourage responsible marine harvesting and algae-based omega-3 production technologies. Microalgae cultivation systems across Scandinavia and Western Europe have increased plant-based DHA production by more than 25% since 2022. Croda International has expanded specialty lipid manufacturing facilities in the region to produce pharmaceutical-grade omega-3 oils. Consumer behavior reflects high awareness of preventive healthcare, with more than 35% of health supplement consumers in Western Europe preferring sustainably sourced omega-3 products.

Why Is Rapid Nutritional Supplement Adoption Driving Industry Expansion?

Asia-Pacific accounts for approximately 24% of global omega-3 consumption and represents one of the fastest expanding markets for nutritional lipids. China, Japan, and India collectively account for more than 60% of regional demand due to increasing healthcare awareness and expanding nutraceutical manufacturing industries. Regional manufacturing infrastructure for fish oil refining and algae-based omega-3 production has expanded by nearly 30% over the past five years. Japan leads in clinical nutrition adoption while China has emerged as a major omega-3 supplement manufacturing hub producing over 120,000 metric tons annually. Local player GC Rieber VivoMega has strengthened supply chains across the region by expanding processing facilities. Consumer behavior in Asia-Pacific is strongly influenced by e-commerce health product distribution and rising demand for preventive healthcare supplements.

How Are Marine Resource Industries Supporting Nutritional Ingredient Production?

South America contributes around 6% of the global Omega-3 market and remains a crucial hub for marine-based omega-3 raw material production. Peru and Chile collectively produce more than 300,000 metric tons of fish oil annually, supplying raw materials for nutraceutical and pharmaceutical manufacturers worldwide. Government fisheries regulations encourage sustainable harvesting practices and improved marine ecosystem management. Regional infrastructure investments in fish oil processing facilities have increased omega-3 extraction efficiency by nearly 18% over the last four years. A key regional supplier, TASA, continues expanding advanced fish oil processing capabilities to support global supply chains. Consumer demand across South America is growing steadily as functional foods and dietary supplements gain popularity in urban markets.

What Role Does Health Awareness Play in Nutritional Supplement Expansion?

The Middle East & Africa represent roughly 3% of the global Omega-3 market but are witnessing rising demand driven by expanding healthcare infrastructure and increasing awareness of preventive nutrition. The United Arab Emirates and South Africa are emerging as major consumption hubs for omega-3 dietary supplements and functional nutrition products. Regional pharmaceutical import volumes for nutritional lipids increased by nearly 14% between 2022 and 2024. Technological modernization in food processing industries is enabling integration of omega-3 ingredients into dairy products and infant nutrition formulations. A regional nutrition company in the UAE has introduced fortified dairy beverages enriched with DHA oils to meet rising consumer demand. Consumer behavior across the region reflects growing adoption of wellness supplements and preventive health products.

• United States – 31% market share: Strong nutraceutical manufacturing capacity, high dietary supplement consumption, and advanced biotechnology investments supporting omega-3 production.

• China – 18% market share: Large-scale fish oil refining infrastructure and rapidly expanding omega-3 supplement manufacturing industry driven by rising healthcare awareness.

The Omega-3 market is moderately consolidated with more than 70 active global and regional manufacturers operating across the value chain, including fish oil producers, algae-based omega-3 manufacturers, nutraceutical suppliers, and pharmaceutical ingredient companies. The top five companies collectively account for nearly 48% of global market activity, reflecting strong technological capabilities and vertically integrated supply chains. Leading firms continue to invest in sustainable raw material sourcing, algae fermentation technologies, and high-purity EPA and DHA concentration processes to maintain competitive positioning.

Strategic collaborations and acquisitions have increased significantly, with more than 15 partnership agreements announced between biotechnology companies and nutraceutical manufacturers since 2022. Companies are focusing on expanding production capacity for algae-derived omega-3 oils to reduce dependency on marine fisheries and support vegan nutrition markets. Innovation is also a major competitive differentiator, with over 120 patents related to omega-3 encapsulation, purification, and fermentation technologies filed globally during the past five years.

Manufacturers are introducing advanced microencapsulation techniques that enhance omega-3 stability by nearly 20% in food processing applications. In addition, pharmaceutical companies are investing heavily in clinical-grade EPA formulations targeting cardiovascular and metabolic health treatments. These developments are intensifying competition while simultaneously expanding technological capabilities and product differentiation within the global Omega-3 market.

DSM-Firmenich

BASF SE

Croda International Plc

Cargill Incorporated

Pelagia AS

GC Rieber Oils

KD Pharma Group

Omega Protein Corporation

Epax Norway AS

Aker BioMarine

Polaris Nutritional Lipids

Golden Omega SA

Technological innovation is rapidly transforming the Omega-3 market through advanced extraction, purification, and sustainable production methods. Molecular distillation remains one of the most widely used purification technologies, capable of removing up to 95% of contaminants such as heavy metals and oxidation compounds from fish-derived oils. Supercritical CO₂ extraction is increasingly used in high-purity EPA and DHA production, delivering extraction efficiency improvements of nearly 20% while preserving fatty acid stability. Microencapsulation technology has emerged as a critical solution for integrating omega-3 ingredients into functional foods and beverages. Encapsulation techniques improve oxidative stability by approximately 30% and extend product shelf life by more than 12 months in fortified dairy, bakery, and beverage products. This technology also enables controlled release of omega-3 fatty acids, improving bioavailability in clinical nutrition applications.

Biotechnology advancements are also reshaping production systems. Microalgae fermentation platforms now produce DHA concentrations exceeding 40% lipid content in controlled photobioreactors, significantly reducing dependence on marine fisheries. Precision fermentation technologies are enabling large-scale plant-based omega-3 production, supporting vegan nutraceutical products and sustainable aquaculture feed. Additionally, digital quality monitoring systems integrated with chromatography-based testing allow real-time purity verification and oxidation control during manufacturing. These innovations are helping omega-3 manufacturers meet strict pharmaceutical-grade quality standards while improving production efficiency and environmental sustainability.

• In April 2024, Aker BioMarine launched PL+ Krill Oil, a next-generation phospholipid-based omega-3 ingredient designed to enhance bioavailability and stability in nutraceutical applications. The product utilizes advanced purification and concentration technology to improve absorption efficiency and support cardiovascular and cognitive health formulations. Source: www.akerbiomarine.com

• In September 2024, Golden Omega announced the expansion of its omega-3 production facility in Arica, Chile, increasing fish oil processing capacity by nearly 20%. The upgrade included advanced molecular distillation systems and automated quality control technologies to enhance EPA and DHA concentration capabilities. Source: www.goldenomega.com

• In January 2025, DSM-Firmenich introduced a new algae-derived omega-3 ingredient under its life’sOMEGA portfolio, designed for plant-based nutraceutical and functional food formulations. The innovation utilizes fermentation-based microalgae technology to produce high-purity DHA oils suitable for vegan dietary supplements and fortified beverages. Source: www.dsm-firmenich.com

• In February 2025, KD Pharma Group expanded its pharmaceutical-grade omega-3 manufacturing capabilities at its Germany facility, installing advanced chromatographic purification systems capable of producing EPA concentrations above 90%. The expansion aims to support growing demand for prescription omega-3 therapies targeting cardiovascular and metabolic health conditions. Source: www.kd-pharma.com

The Omega-3 Market Report provides a comprehensive analysis of the global industry covering multiple product types including EPA, DHA, and ALA formulations used across nutraceuticals, pharmaceuticals, functional foods, and animal nutrition sectors. The report evaluates over 15 major product categories and more than 30 application areas ranging from dietary supplements and infant nutrition to clinical therapeutics and aquaculture feed formulations.

Geographically, the report assesses market dynamics across five major regions and more than 20 key countries, examining consumption trends, production infrastructure, and regulatory frameworks shaping omega-3 adoption. It analyzes supply chain structures including fish oil harvesting, algae-based omega-3 production, refining processes, and ingredient distribution networks. The report also explores emerging technological developments such as microalgae fermentation, precision lipid purification, molecular distillation, and encapsulation systems that are improving omega-3 ingredient stability and bioavailability.

Additionally, the study evaluates competitive positioning of more than 70 global manufacturers, highlighting innovation pipelines, strategic partnerships, product launches, and capacity expansions influencing the market landscape. The report further examines sustainability initiatives including responsible marine sourcing, algae-based production alternatives, and environmental compliance strategies shaping the long-term evolution of the Omega-3 market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

6.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

DSM-Firmenich, BASF SE, Croda International Plc, Cargill Incorporated, Pelagia AS, GC Rieber Oils, KD Pharma Group, Omega Protein Corporation, Epax Norway AS, Aker BioMarine, Polaris Nutritional Lipids, Golden Omega SA |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |