Reports

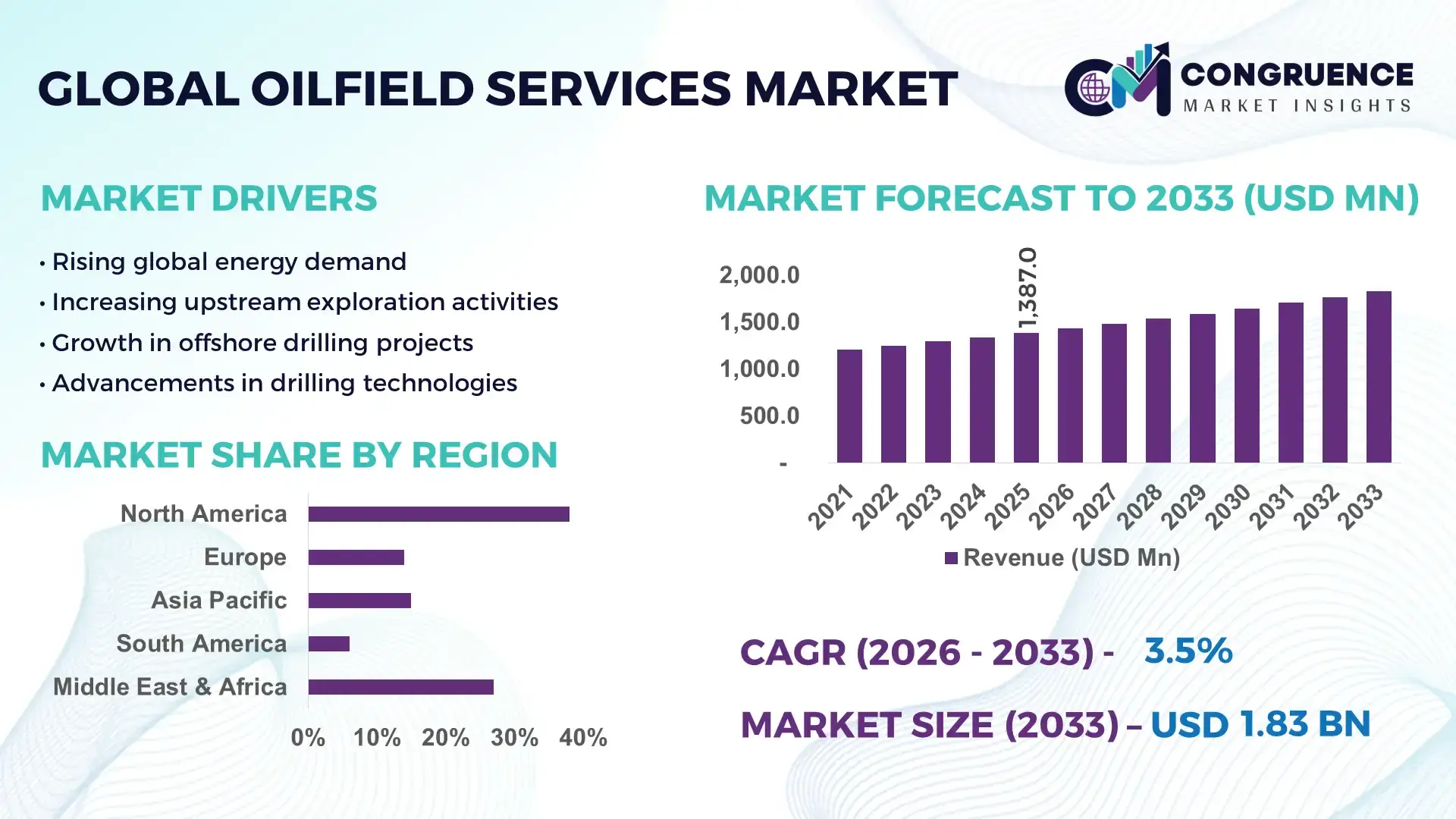

The Global Oilfield Services Market was valued at USD 1,387.0 Million in 2025 and is anticipated to reach a value of USD 1,826.4 Million by 2033 expanding at a CAGR of 3.5% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by rising upstream exploration activities and increasing demand for energy security across emerging and developed economies.

The United States dominates the Oilfield Services Market with extensive upstream infrastructure, producing over 12.9 million barrels of crude oil per day in 2025 and operating more than 600 active oil rigs. The country accounts for over 35% of global drilling activity, supported by strong investments exceeding USD 90 billion annually in upstream oilfield projects. Advanced technologies such as hydraulic fracturing, horizontal drilling, and AI-driven reservoir modeling are widely deployed, with over 70% of operators integrating digital oilfield solutions. Key applications include shale exploration, offshore deepwater drilling, and enhanced oil recovery (EOR), with over 45% of services linked to unconventional resource extraction.

Market Size & Growth: USD 1,387.0 Million in 2025, projected to reach USD 1,826.4 Million by 2033 at 3.5% CAGR, driven by rising drilling activities and energy demand.

Top Growth Drivers: 65% increase in offshore exploration, 48% efficiency improvement via digital oilfields, 52% rise in unconventional resource development.

Short-Term Forecast: By 2028, drilling efficiency is expected to improve by 22% with automation and AI integration.

Emerging Technologies: AI-based reservoir analytics, digital twins in drilling operations, and autonomous drilling rigs gaining traction.

Regional Leaders: North America (USD 620M by 2033, shale adoption), Middle East (USD 540M, large-scale upstream projects), Asia-Pacific (USD 380M, rising exploration).

Consumer/End-User Trends: Oil & gas companies account for over 75% demand, with increasing reliance on outsourced specialized services.

Pilot or Case Example: In 2025, a Middle East offshore project reduced downtime by 18% using predictive maintenance tools.

Competitive Landscape: Market leader holds ~18% share, followed by key players like Halliburton, Baker Hughes, Weatherford, and TechnipFMC.

Regulatory & ESG Impact: Over 40% firms adopting low-emission drilling technologies and carbon capture integration.

Investment & Funding Patterns: Over USD 120 billion invested globally in upstream oilfield projects with rising joint ventures.

Innovation & Future Outlook: Integration of robotics and real-time data analytics expected to enhance operational efficiency by over 25%.

Oilfield services demand is driven by drilling (40%), completion (25%), and production services (35%), with innovations such as automated rigs and smart sensors reshaping operations. Environmental compliance policies are influencing low-emission technologies, while Asia-Pacific and Middle East regions show strong consumption growth due to rising energy demand and exploration expansion.

The Oilfield Services Market plays a strategically critical role in ensuring global energy stability, supporting upstream exploration, drilling, and production activities across conventional and unconventional reserves. Increasing reliance on advanced extraction technologies has significantly improved efficiency, with AI-driven predictive maintenance reducing equipment downtime by nearly 20% compared to traditional maintenance models. Similarly, automated drilling systems deliver 30% faster well completion compared to conventional rotary drilling techniques.

North America dominates in volume due to its extensive shale production infrastructure, while the Middle East leads in adoption with over 60% of operators deploying advanced reservoir management systems. This dual dynamic reflects a market where mature regions focus on scale, while emerging regions prioritize technology integration to maximize output efficiency.

By 2028, AI-enabled drilling optimization is expected to improve operational efficiency by 25%, reducing non-productive time significantly across offshore and onshore projects. Companies are increasingly aligning with ESG commitments, with firms targeting a 35% reduction in flaring emissions and a 20% improvement in water recycling processes by 2030.

In 2025, Saudi Arabia implemented AI-based drilling optimization systems that improved drilling speed by 18% while reducing operational costs. Such micro-level implementations highlight the measurable benefits of digital transformation across oilfield operations.

Looking ahead, the Oilfield Services Market will remain a cornerstone of global energy infrastructure, enabling sustainable extraction, regulatory compliance, and operational resilience through technological advancement and strategic investment.

The Oilfield Services Market is influenced by fluctuating crude oil demand, technological advancements, and evolving energy policies. Increasing exploration in deepwater and ultra-deepwater reserves has expanded demand for specialized services such as well intervention, drilling support, and reservoir evaluation. More than 55% of new exploration projects are now focused on offshore locations, requiring high-end engineering solutions. Additionally, over 60% of oilfield operators are adopting digital technologies to improve efficiency and reduce operational risks.

Geopolitical factors and energy security concerns are also shaping the market, with governments investing heavily in domestic oil production capabilities. The rise of unconventional resources such as shale gas and tight oil has significantly altered service demand patterns, with hydraulic fracturing accounting for over 45% of total drilling services. Environmental regulations are further pushing companies to adopt cleaner technologies, influencing service innovation and operational strategies.

Rising global energy consumption continues to be a primary driver of the Oilfield Services Market, with global oil demand exceeding 102 million barrels per day in 2025. Industrialization and urbanization in emerging economies such as India and China are significantly increasing demand for petroleum products. Over 65% of energy consumption in developing nations still relies on fossil fuels, necessitating continuous exploration and production activities. Additionally, over 70% of oil companies are expanding their upstream investments to secure long-term supply, creating sustained demand for drilling, completion, and maintenance services. The expansion of offshore exploration projects, particularly in deepwater regions, has increased reliance on specialized oilfield services by more than 50%. Furthermore, the rise of unconventional resources such as shale oil has driven demand for hydraulic fracturing and horizontal drilling services, which now account for nearly 45% of total drilling operations globally.

Stringent environmental regulations are significantly impacting the Oilfield Services Market by increasing compliance costs and limiting exploration activities in sensitive regions. Governments worldwide have imposed strict emission control policies, with over 40 countries implementing carbon reduction targets that directly affect upstream oil operations. For instance, methane emission regulations in North America require operators to reduce leakage by up to 75%, necessitating costly monitoring and mitigation systems. Additionally, restrictions on offshore drilling in environmentally sensitive areas have reduced exploration opportunities by nearly 20% in certain regions. The push for renewable energy adoption is also reducing long-term investments in fossil fuel-based projects, with over 30% of global energy investments now directed toward renewable sources. These factors collectively constrain market expansion and require companies to invest heavily in sustainable technologies.

Digital transformation offers significant growth opportunities for the Oilfield Services Market, with over 60% of oil companies investing in digital oilfield technologies. The adoption of AI, IoT, and big data analytics enables real-time monitoring of drilling operations, improving efficiency by up to 25% and reducing downtime by nearly 20%. Advanced reservoir modeling tools allow operators to optimize extraction processes, increasing recovery rates by approximately 15%. The integration of autonomous drilling systems is further enhancing operational efficiency, with automated rigs capable of reducing human intervention by over 40%. Additionally, predictive maintenance technologies are helping companies minimize equipment failures, leading to cost savings of up to 18%. As digital solutions become more accessible, their adoption is expected to accelerate across both onshore and offshore operations, creating new revenue streams for service providers.

High operational costs remain a significant challenge for the Oilfield Services Market, particularly in offshore and deepwater projects. Drilling a single deepwater well can cost between USD 50 million and USD 100 million, making it financially risky for operators. Equipment maintenance, labor costs, and compliance requirements further increase overall expenditure, with operational costs rising by nearly 15% in recent years. Additionally, volatility in crude oil prices creates uncertainty, leading to reduced investment in exploration activities during price downturns. Over 40% of oilfield service contracts are affected by price fluctuations, impacting profitability and project viability. The need for advanced technologies such as automated rigs and digital monitoring systems also requires significant capital investment, limiting adoption among smaller operators. These challenges necessitate strategic cost management and innovation to maintain competitiveness.

Rapid Adoption of Digital Oilfield Technologies: Over 62% of oilfield operators globally have integrated digital monitoring systems into drilling and production processes. Real-time data analytics has reduced non-productive time by nearly 20%, while predictive maintenance tools have lowered equipment failure rates by 18%, significantly improving operational efficiency across upstream activities.

Expansion of Offshore and Deepwater Exploration: Approximately 55% of new oil exploration projects in 2025 are focused on offshore reserves, particularly in ultra-deepwater regions. Advanced subsea technologies and floating production systems have improved extraction efficiency by over 25%, supporting increased demand for specialized oilfield services.

Growth in Unconventional Resource Development: Unconventional resources such as shale and tight oil now contribute to over 45% of global drilling activities. Hydraulic fracturing and horizontal drilling technologies have improved recovery rates by 30%, driving demand for advanced completion and stimulation services.

Rising Focus on Low-Emission and Sustainable Operations: More than 40% of oilfield companies are implementing carbon reduction initiatives, including methane capture and electrified drilling rigs. These measures have reduced emissions by up to 22%, aligning operations with global sustainability targets and regulatory requirements.

The Oilfield Services Market is segmented based on type, application, and end-user, reflecting the diverse range of services required across upstream oil and gas operations. Drilling services, completion services, and production services form the core segments, each playing a critical role in the oil extraction lifecycle. Applications span onshore and offshore operations, with offshore projects increasingly demanding advanced technologies due to complex environmental conditions. End-users primarily include oil & gas exploration companies, national oil companies, and independent operators, with varying service requirements based on project scale and location. The segmentation highlights a strong shift toward technologically advanced solutions, particularly in offshore and unconventional resource development, where efficiency and precision are essential.

Drilling services dominate the Oilfield Services Market, accounting for approximately 42% of total demand due to their essential role in exploration and well development. Completion services hold around 33%, focusing on preparing wells for production, while production services contribute nearly 25%, ensuring efficient extraction and maintenance. However, production services are the fastest-growing segment, expanding at an estimated CAGR of 4.2% due to increasing emphasis on maximizing output from existing wells. Other niche services such as well intervention and reservoir evaluation collectively account for the remaining 20% share, providing specialized support for complex operations. The demand for integrated service solutions is rising, with operators preferring bundled services to improve efficiency and reduce costs.

Onshore applications lead the Oilfield Services Market with approximately 60% share, driven by extensive shale and conventional oil exploration activities. Offshore applications account for around 40%, but are growing faster with a CAGR of 4.5% due to increasing investments in deepwater and ultra-deepwater projects. Consumer adoption trends indicate that over 55% of oil companies are expanding offshore exploration portfolios, while nearly 48% are investing in advanced subsea technologies. Other applications, including enhanced oil recovery and well maintenance, collectively contribute about 30% of the market.

Oil & gas exploration companies represent the largest end-user segment, accounting for approximately 65% of market demand due to their extensive upstream operations. National oil companies contribute around 25%, while independent operators make up the remaining 10%. However, independent operators are the fastest-growing segment with a CAGR of 4.8%, driven by increased access to advanced technologies and flexible investment strategies. Adoption trends show that over 60% of large enterprises are implementing digital oilfield solutions, while nearly 45% of smaller operators are investing in automation technologies. Other end-users, including service contractors and engineering firms, collectively contribute about 20% of the market.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.6% between 2026 and 2033.

North America leads due to its advanced drilling infrastructure and high shale production, with over 600 active rigs and more than 12 million barrels per day output. The Middle East holds approximately 27% share, supported by large-scale upstream investments exceeding USD 70 billion annually. Europe accounts for around 14%, driven by offshore exploration in the North Sea, while Asia-Pacific contributes nearly 15% with increasing exploration activities in China and India. South America represents about 6%, led by Brazil’s offshore projects, and Africa contributes around 5%, driven by emerging exploration initiatives.

North America accounts for approximately 38% of the global Oilfield Services Market, driven by extensive shale exploration and advanced drilling technologies. The region’s oil and gas industry relies heavily on hydraulic fracturing and horizontal drilling, with over 70% of wells utilizing these methods. Regulatory frameworks emphasize environmental compliance, requiring methane emission reductions of up to 75%, influencing service innovation. Technological advancements such as AI-driven drilling optimization and real-time monitoring systems are widely adopted, improving efficiency by over 20%. A leading regional player has implemented automated rigs across multiple sites, reducing operational downtime by 18%. Consumer behavior reflects high enterprise adoption, particularly in energy-intensive industries, with over 65% of companies outsourcing specialized oilfield services.

Europe holds approximately 14% of the Oilfield Services Market, with key markets including the UK, Norway, and Germany. Offshore exploration in the North Sea remains a major driver, supported by strict environmental regulations and sustainability initiatives. Regulatory bodies are enforcing carbon reduction targets, with operators required to reduce emissions by up to 30%. The region is witnessing increased adoption of digital technologies, including AI and IoT-based monitoring systems, improving operational efficiency by 15%. A regional player has developed low-emission drilling solutions, reducing environmental impact significantly. Consumer behavior is influenced by regulatory pressure, leading to higher demand for sustainable and transparent oilfield services.

Asia-Pacific accounts for approximately 15% of the global market and ranks as the fastest-growing region. Major consuming countries include China, India, and Japan, with increasing investments in exploration and production activities. Infrastructure development and rising energy demand are key growth drivers, with over 50% of new projects focused on offshore reserves. Technological innovation hubs in China and India are accelerating the adoption of digital oilfield solutions, improving efficiency by 18%. A regional company has implemented automated drilling systems, reducing operational costs significantly. Consumer behavior reflects strong demand driven by industrial growth and increasing energy consumption.

South America represents around 6% of the Oilfield Services Market, with Brazil and Argentina as key contributors. Offshore oil discoveries, particularly in Brazil’s pre-salt fields, are driving demand for advanced drilling and production services. Government policies supporting energy sector investments have increased exploration activities by over 20%. Infrastructure development and trade policies are encouraging foreign investments, boosting market growth. A regional player has expanded offshore drilling capabilities, improving production efficiency by 15%. Consumer behavior is closely tied to energy demand, with increasing reliance on oilfield services for economic development.

The Middle East & Africa region accounts for approximately 27% of the global market, driven by extensive oil reserves and large-scale upstream projects. Major growth countries include Saudi Arabia, UAE, and South Africa, with significant investments in exploration and production. Technological modernization, including AI-driven reservoir management and automated drilling systems, is improving efficiency by over 20%. Local regulations encourage sustainable practices, with companies adopting low-emission technologies. A regional player has implemented digital oilfield solutions, enhancing operational performance. Consumer behavior reflects strong demand from national oil companies focused on maximizing production output.

United States – 32% Market share: driven by extensive shale production and advanced drilling technologies.

Saudi Arabia – 18% Market share: supported by large-scale upstream investments and high production capacity.

The Oilfield Services Market is moderately consolidated, with the top five companies accounting for approximately 55% of the total market share. The market includes over 150 active global and regional players, ranging from integrated service providers to specialized technology firms. Leading companies focus on strategic partnerships, mergers, and acquisitions to expand their service portfolios and geographic presence.

Innovation is a key competitive factor, with over 60% of companies investing in digital technologies such as AI, IoT, and automation to enhance operational efficiency. Product differentiation is achieved through advanced drilling solutions, reservoir management systems, and integrated service offerings. The market leader holds around 18% share, while other major players maintain strong positions through diversified services and global operations.

Competition is also influenced by regional dynamics, with local players leveraging cost advantages and market knowledge to compete with global firms. Increasing demand for sustainable and low-emission solutions is driving companies to develop environmentally friendly technologies, further intensifying competition.

Halliburton

Baker Hughes

Weatherford International

TechnipFMC

National Oilwell Varco

Saipem

Petrofac

Aker Solutions

Oceaneering International

Superior Energy Services

Helmerich & Payne

Transocean

Nabors Industries

Technological advancements are transforming the Oilfield Services Market, with digital oilfield solutions playing a central role in enhancing operational efficiency and reducing costs. Over 60% of oilfield operators have adopted AI-driven analytics platforms to optimize drilling and production processes. These systems enable real-time monitoring, predictive maintenance, and data-driven decision-making, reducing downtime by nearly 20% and improving overall efficiency.

Automation is another key trend, with autonomous drilling rigs reducing human intervention by over 40%. Robotics and remote-operated vehicles (ROVs) are widely used in offshore operations, improving safety and precision in complex environments. Digital twins are being implemented to simulate drilling operations, allowing operators to predict potential issues and optimize performance.

Advanced reservoir modeling technologies are improving recovery rates by approximately 15%, while IoT-enabled sensors provide continuous data on equipment performance and environmental conditions. The integration of blockchain technology is enhancing transparency and security in supply chain management, reducing operational risks.

Sustainability-focused technologies are also gaining traction, with electrified drilling rigs and carbon capture systems reducing emissions by up to 22%. These innovations are enabling companies to meet regulatory requirements while maintaining operational efficiency, positioning the market for long-term growth.

• In February 2025, Schlumberger (SLB) expanded its digital oilfield capabilities by advancing AI-driven platforms and cloud-based reservoir analytics, with its digital segment reporting a 20% increase in activity linked to AI and data solutions integration across global operations. Source: www.investors.com

• In October 2025, Baker Hughes reported strong growth in its Industrial and Energy Technology segment, with orders rising by 44% year-on-year to $4.14 billion and backlog reaching $32.1 billion, driven by LNG infrastructure and energy transition projects.

• In December 2025, Halliburton, along with peers including SLB and Baker Hughes, expanded into data center energy solutions, leveraging oilfield expertise to supply power generation and cooling systems, with the sector projected to reach 90 GW demand in the U.S. by 2030.

• In April 2026 (announced based on 2025 strategic direction), Baker Hughes agreed to divest its Waygate Technologies unit for approximately $1.45 billion as part of its transition strategy toward cleaner energy and core oilfield and energy technology operations.

The Oilfield Services Market Report provides a comprehensive analysis of the global industry, covering a wide range of service types including drilling, completion, production, and well intervention services. The report examines applications across onshore and offshore operations, highlighting the growing importance of deepwater and ultra-deepwater exploration projects.

Geographically, the report includes detailed insights into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering region-specific analysis of market trends, demand patterns, and technological adoption. It evaluates key industry sectors such as shale exploration, offshore drilling, and enhanced oil recovery, providing a holistic view of market dynamics.

The report also explores technological advancements, including AI-driven analytics, automation, IoT integration, and digital oilfield solutions, which are transforming operational efficiency and reducing costs. Emerging trends such as sustainability initiatives, carbon capture technologies, and electrified drilling systems are analyzed to understand their impact on the market.

Additionally, the report covers competitive landscape insights, profiling major industry players and their strategic initiatives, including partnerships, mergers, and product innovations. It provides valuable information for stakeholders, enabling informed decision-making and strategic planning in a rapidly evolving market environment.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,387.0 Million |

| Market Revenue (2033) | USD 1,826.4 Million |

| CAGR (2026–2033) | 3.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Schlumberger (SLB); Halliburton; Baker Hughes; Weatherford International; TechnipFMC; National Oilwell Varco; Saipem; Petrofac; Aker Solutions; Oceaneering International; Superior Energy Services; Helmerich & Payne; Transocean; Nabors Industries |

| Customization & Pricing | Available on Request (10% Customization Free) |