Reports

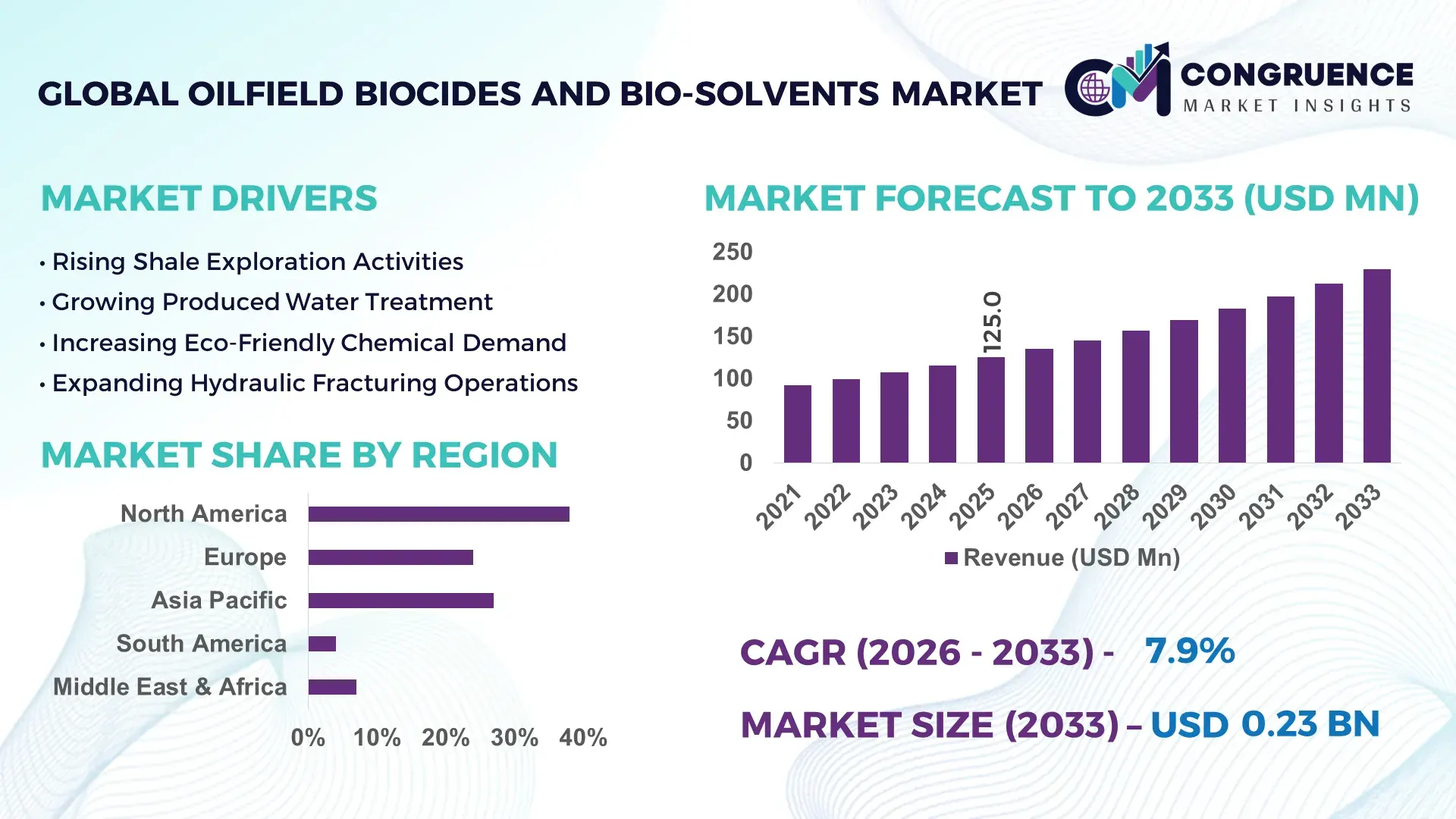

The Global Oilfield Biocides and Bio-Solvents Market was valued at USD 125.0 Million in 2025 and is anticipated to reach a value of USD 229.7 Million by 2033 expanding at a CAGR of 7.9% between 2026 and 2033. Rising deployment of advanced microbial control chemicals across shale extraction and enhanced oil recovery operations is accelerating market penetration, with over 42% of offshore operators integrating low-toxicity bio-solvent formulations to reduce corrosion and production downtime. Between 2024 and 2026, geopolitical energy security concerns linked to Red Sea shipping disruptions and OPEC+ production adjustments forced oilfield operators to localize chemical sourcing and optimize reservoir maintenance programs. Digital monitoring integration in upstream assets increased by 31%, enabling real-time microbial contamination management and reducing fluid treatment cycles by nearly 18% across mature wells. Compared with conventional solvent systems, next-generation bio-solvents improve biodegradability performance by more than 45% while reducing hazardous waste handling requirements.

The United States dominates the global Oilfield Biocides and Bio-Solvents Market with approximately 34% share, supported by aggressive shale production expansion in the Permian Basin and Gulf Coast offshore activity. More than 58% of North American unconventional wells now utilize advanced biocide treatment programs integrated with automated injection systems. The country recorded over USD 3.2 billion in upstream chemical optimization investments between 2024 and 2025, while high-salinity hydraulic fracturing operations increased specialty biocide consumption by 27%. Strong adoption by independent exploration firms, combined with AI-driven reservoir monitoring deployment across nearly 40% of large operators, continues to strengthen U.S. leadership compared with slower modernization cycles in Latin America and parts of Africa.

As upstream operators prioritize operational continuity, compliance efficiency, and lower environmental impact simultaneously, the Oilfield Biocides and Bio-Solvents Market is transforming into a strategic performance optimization segment rather than a conventional oilfield chemical category.

Market Size & Growth: USD 125.0 million in 2025 reaching USD 229.7 million by 2033, driven by 42% rise in low-toxicity drilling fluid adoption across advanced oilfields.

Top Growth Drivers: Offshore microbial control demand up 31%, shale treatment integration up 27%, and sustainable solvent usage rising 36% globally.

Short-Term Forecast: By 2028, automated chemical injection systems are projected to reduce well-maintenance downtime by 22% across mature assets.

Emerging Technologies: AI-enabled reservoir monitoring, bio-based solvent engineering, and automated dosing platforms improved treatment precision by 28%.

Regional Leaders: North America leads at USD 78 million equivalent demand, Asia-Pacific expands through 33% refinery modernization, while Middle East deployment rises 25%.

Consumer/End-User Trends: Over 58% of unconventional well operators now prioritize biodegradable treatment chemicals for compliance-focused production operations.

Pilot/Case Example: In 2025, a Gulf offshore deployment reduced bacterial corrosion incidents by 37% using advanced oxidizing biocide formulations.

Competitive Landscape: Top players control nearly 46% market share, with Baker Hughes, SLB, Halliburton, Clariant, and Solenis leading expansion strategies.

Regulatory & ESG Impact: Environmental discharge standards lowered hazardous solvent usage by 29% across offshore operations between 2024 and 2026.

Investment & Funding: More than USD 1.1 billion was allocated toward upstream chemical optimization and localized supply chain partnerships globally.

Innovation & Future Outlook: High-performance bio-solvents with 45% improved biodegradability are redefining next-generation sustainable oilfield treatment systems.

Oilfield Biocides and Bio-Solvents demand remains heavily concentrated in upstream drilling and hydraulic fracturing operations, which collectively contribute nearly 61% of total chemical consumption due to aggressive microbial control requirements and corrosion prevention needs. Advanced oxidizing formulations improved fluid stability by 24%, while bio-based solvent integration increased by 33% across offshore assets. North America and the Middle East continue dominating operational deployment, whereas Asia-Pacific is rapidly scaling localized production capabilities amid supply chain diversification and stricter environmental treatment standards. The accelerating shift toward automated chemical dosing and environmentally optimized production systems is setting the foundation for deeper strategic transformation across global oilfield operations.

The Oilfield Biocides and Bio-Solvents Market is rapidly transforming into a strategic operational pillar for upstream oil & gas operators seeking production stability, lower asset degradation, and regulatory resilience simultaneously. Intensifying microbial contamination in unconventional wells, combined with stricter offshore discharge frameworks, is accelerating the integration of high-performance treatment chemicals into core production infrastructure. Operators are no longer treating biocides and bio-solvents as auxiliary consumables; they are now deploying them as performance-critical solutions directly linked to uptime optimization, corrosion control, and drilling efficiency.

Global supply chain restructuring between 2024 and 2026 forced energy companies to localize specialty chemical procurement, particularly after shipping disruptions in the Red Sea and tightening environmental mandates in offshore regions. This shift is transforming procurement models, with over 39% of major upstream operators prioritizing regional chemical manufacturing partnerships to reduce operational delays and treatment inconsistencies.

AI-enabled automated dosing systems improve treatment efficiency by 34% while reducing chemical waste handling costs by 26% compared to legacy manual injection systems. North America leads in production volume and unconventional well deployment, while Europe leads in sustainable formulation innovation, with nearly 41% of operators integrating biodegradable solvent technologies into offshore drilling systems. Asia-Pacific, meanwhile, is accelerating refinery-linked deployment capacity through aggressive domestic chemical manufacturing expansion. Within the next three years, predictive microbial monitoring integration is expected to reduce unplanned well intervention frequency by nearly 21%, significantly improving production continuity across mature reservoirs. ESG positioning is also becoming a competitive advantage, as low-toxicity bio-solvent programs reduce hazardous disposal requirements by 32%, strengthening regulatory compliance and improving access to environmentally sensitive offshore projects.

A 2025 Middle East offshore pilot project demonstrated a 36% reduction in bacterial corrosion events after integrating advanced oxidizing biocides with real-time reservoir analytics. Simultaneously, leading oilfield service companies are shifting capital allocation toward sustainable chemical portfolios, regional blending facilities, and digital treatment optimization platforms to strengthen long-term competitive positioning. The companies dominating this market are not simply expanding chemical sales; they are optimizing upstream operational ecosystems, accelerating compliance adaptation, and transforming reservoir management into a data-driven performance strategy that defines future competitive advantage.

The Oilfield Biocides and Bio-Solvents Market is being reshaped by the convergence of environmental regulation, upstream operational efficiency demands, and the rapid modernization of unconventional oil extraction infrastructure. Oilfield operators are increasingly prioritizing advanced microbial control solutions as bacterial contamination and corrosion-related downtime continue affecting production continuity across offshore and shale assets. More than 48% of mature wells globally now require continuous fluid treatment programs due to higher water injection intensity and reservoir aging patterns. The market is also witnessing a structural transition from traditional solvent-based formulations toward biodegradable and low-toxicity alternatives, particularly in offshore drilling regions facing tighter environmental discharge rules. North America continues dominating demand due to large-scale shale operations, while Asia-Pacific is accelerating local production and deployment capacity through refinery-linked infrastructure expansion. Simultaneously, automation and AI-enabled reservoir monitoring systems are redefining chemical treatment precision, enabling operators to optimize dosing cycles and reduce operational waste by nearly 20%. Growing geopolitical instability affecting chemical supply chains is further forcing companies to regionalize sourcing, strengthen strategic partnerships, and accelerate investment in localized blending facilities. As upstream operators balance productivity targets with sustainability pressures, Oilfield Biocides and Bio-Solvents are becoming increasingly central to operational resilience and long-term field economics.

The accelerating intensity of hydraulic fracturing, water injection, and offshore drilling operations is significantly increasing microbial contamination risks across upstream oil infrastructure. More than 52% of unconventional wells now experience elevated sulfate-reducing bacterial activity, directly increasing corrosion frequency and production instability. This structural shift is forcing operators to integrate advanced biocide treatment systems capable of maintaining fluid integrity under high-temperature and high-salinity conditions. Simultaneously, the transition toward longer horizontal wells increased chemical treatment demand by nearly 29% between 2024 and 2026. Red Sea shipping disruptions and global energy security concerns further accelerated localized upstream chemical sourcing, pushing major operators toward regional supply partnerships and inventory optimization strategies. As a direct business response, leading oilfield service providers expanded automated dosing infrastructure deployment by over 31% to improve treatment precision and reduce operational downtime. Companies are also accelerating investment in low-toxicity bio-solvents to meet tightening offshore discharge standards while improving well productivity. The market is therefore shifting from reactive chemical usage toward predictive reservoir protection strategies integrated with digital monitoring platforms.

The Oilfield Biocides and Bio-Solvents Market faces significant structural constraints due to volatile specialty chemical feedstock pricing and increasingly stringent environmental regulations governing offshore drilling operations. Key active ingredients used in oxidizing and non-oxidizing biocides experienced price fluctuations exceeding 24% during 2024–2025 due to supply concentration in limited manufacturing hubs. At the same time, stricter wastewater discharge frameworks increased compliance-related operating costs for offshore operators by nearly 18%. Infrastructure limitations in emerging drilling regions continue delaying high-performance treatment adoption, particularly where local blending and chemical storage capabilities remain underdeveloped. These operational bottlenecks are directly affecting deployment scalability, extending procurement cycles, and increasing inventory management complexity for upstream operators. In response, companies are diversifying supplier networks, negotiating long-term procurement agreements, and increasing investment in bio-based alternatives with improved environmental profiles. Several major producers are also redesigning formulations to reduce dependency on high-volatility feedstocks. However, balancing regulatory compliance with operational affordability remains a persistent challenge, especially for mid-sized exploration firms operating under cost-sensitive production models.

The rapid shift toward environmentally optimized drilling systems is creating high-impact opportunities for advanced bio-solvent and biodegradable biocide technologies across both offshore and unconventional extraction markets. More than 43% of newly commissioned offshore projects now prioritize low-toxicity chemical programs to strengthen regulatory compliance and reduce hazardous disposal requirements. Simultaneously, AI-integrated treatment optimization platforms improved microbial detection speed by 35%, enabling more precise dosing and lower chemical waste generation. Asia-Pacific and Middle Eastern operators are aggressively expanding localized production infrastructure, creating new demand pockets for region-specific chemical formulations optimized for high-temperature reservoirs and saline conditions. A major non-obvious upside is emerging through automated treatment analytics, which reduced fluid maintenance costs by nearly 22% in pilot deployments while improving equipment lifespan. Companies are responding through accelerated R&D investment, strategic partnerships with digital monitoring firms, and expansion of sustainable formulation portfolios. The market is increasingly rewarding suppliers capable of combining environmental performance, operational precision, and supply chain reliability into integrated treatment ecosystems that strengthen long-term customer retention.

One of the most critical challenges in the Oilfield Biocides and Bio-Solvents Market is maintaining treatment consistency across highly variable reservoir conditions, particularly in ultra-deepwater and high-salinity unconventional wells. More than 33% of operators report inconsistent biocide performance due to temperature fluctuations, fluid incompatibility, and rapidly evolving microbial resistance patterns. These operational inconsistencies increase intervention frequency and raise chemical optimization costs by approximately 19%. At the same time, global logistics disruptions and regional infrastructure gaps continue constraining scalable deployment, especially in emerging production zones lacking advanced storage and dosing systems. Offshore compliance pressures are intensifying further, with nearly 28% of operators facing stricter environmental audit requirements between 2024 and 2026. Companies must therefore solve a dual challenge: improving formulation adaptability while simultaneously reducing environmental impact and operational complexity. Competitive survival increasingly depends on investment in next-generation formulation science, digital reservoir analytics, and strategic partnerships capable of supporting flexible, localized treatment deployment across diverse oilfield environments.

31% Increase in Automated Chemical Injection Deployment Reshaping Upstream Operations: Oilfield operators are rapidly deploying automated dosing and monitoring systems to optimize microbial treatment precision across offshore and shale assets. More than 46% of large upstream facilities integrated sensor-driven injection platforms during 2025, reducing chemical overuse by 21% and maintenance downtime by 18%. Companies are restructuring field operations around predictive treatment scheduling, particularly as labor shortages and offshore compliance pressure intensify across mature production regions.

42% Growth in Biodegradable Solvent Utilization Redefining Offshore Compliance Strategies: Advanced bio-solvent adoption accelerated sharply as environmental discharge regulations tightened across North America and Europe. Nearly 39% of offshore drilling contractors transitioned toward low-toxicity solvent systems, improving biodegradability performance by 45% while reducing hazardous disposal volumes by 26%. Chemical suppliers are scaling localized blending partnerships and reformulating product portfolios to align with stricter operational sustainability requirements and shifting procurement standards.

27% Expansion in Asia-Pacific Localized Production Accelerating Supply Chain Realignment: Energy security concerns and global shipping disruptions forced operators to diversify specialty chemical sourcing strategies. Asia-Pacific manufacturers increased localized oilfield chemical production capacity by 27%, while regional procurement contracts rose 24% between 2024 and 2026. This shift is optimizing delivery timelines and reducing dependency on cross-border chemical imports, particularly for high-volume shale and offshore treatment programs.

34% Improvement in Reservoir Analytics Adoption Optimizing Treatment Efficiency: AI-enabled microbial detection and reservoir analytics platforms are redefining execution-level chemical management across advanced oilfields. Real-time treatment adjustment systems improved contamination response speed by 34% and reduced unnecessary chemical cycling by 17%. Operators are increasingly partnering with digital infrastructure providers to integrate analytics directly into upstream production systems, creating a competitive divide between technologically optimized assets and conventionally managed operations.

The Oilfield Biocides and Bio-Solvents Market is segmented by type, application, and end-user, with demand heavily concentrated in high-intensity upstream production environments requiring continuous microbial control and environmentally optimized chemical treatment. Oxidizing biocides continue dominating due to broad-spectrum effectiveness and lower operational complexity, accounting for nearly 44% of total product demand. However, bio-based solvent formulations are rapidly gaining traction as offshore operators strengthen sustainability compliance strategies and reduce hazardous waste exposure. Application demand remains strongest in drilling fluids and hydraulic fracturing operations, which collectively contribute over 57% of market consumption due to high water handling intensity and bacterial contamination risk. Large integrated oil & gas operators continue representing the dominant end-user segment because of large-scale deployment capacity and automated treatment integration. Meanwhile, independent shale producers are accelerating adoption of digitally optimized treatment systems to reduce downtime and improve fluid stability. Across all segments, companies are increasingly prioritizing localized production, AI-driven treatment monitoring, and sustainable formulation innovation to capture long-term operational and regulatory advantage.

Oxidizing biocides dominate the Oilfield Biocides and Bio-Solvents Market with approximately 44% share due to their rapid microbial elimination capability, lower residue formation, and compatibility with large-scale hydraulic fracturing systems. Their scalability and relatively lower operational complexity make them the preferred choice across offshore and unconventional extraction environments where continuous fluid treatment is critical. Non-oxidizing biocides remain strategically important in high-temperature reservoirs and complex drilling systems, accounting for nearly 31% of market demand due to their longer residual effectiveness and compatibility with sensitive fluid chemistries. Bio-based solvents are emerging as the fastest-advancing segment, supported by a 36% increase in offshore sustainability-driven deployment programs between 2024 and 2026. Compared with conventional petroleum-derived solvents, bio-solvents improve biodegradability performance by over 45% while reducing hazardous waste management requirements. The remaining 25% share consists of specialty hybrid formulations and customized treatment blends designed for high-salinity and ultra-deepwater applications. Demand is clearly shifting toward environmentally optimized and digitally integrated treatment solutions, forcing chemical suppliers to expand low-toxicity portfolios, increase regional blending capacity, and accelerate formulation innovation. Companies investing aggressively in sustainable high-performance chemistries are positioning themselves to capture the next wave of offshore and unconventional oilfield modernization.

• According to a 2025 report by the International Association of Oil & Gas Producers, advanced oxidizing biocide systems were adopted across over 61% of offshore drilling programs, resulting in nearly 28% improvement in microbial contamination control efficiency, reinforcing their growing strategic importance.

Drilling fluids remain the leading application segment in the Oilfield Biocides and Bio-Solvents Market, contributing approximately 38% of total demand due to the critical requirement for microbial stability, corrosion prevention, and fluid integrity maintenance during high-pressure drilling operations. Hydraulic fracturing represents the fastest-evolving application area, supported by a 33% increase in unconventional shale treatment activity and rising water reuse intensity across North America and the Middle East. Operators are increasingly integrating advanced biocide programs into fracturing systems to reduce bacterial growth and maintain well productivity under high-salinity conditions. Produced water treatment and enhanced oil recovery applications collectively account for nearly 41% of total market utilization, supported by expanding water recycling initiatives and aging reservoir management requirements. Compared with mature drilling fluid applications, produced water treatment is experiencing stronger operational transformation through AI-driven monitoring systems and automated chemical injection platforms. Companies are repositioning product portfolios toward multi-functional treatment solutions capable of improving water reuse efficiency while reducing operational downtime. The market is therefore shifting toward integrated application-specific chemical ecosystems where performance optimization, environmental compliance, and digital monitoring capabilities increasingly define purchasing decisions and competitive positioning.

• According to a 2025 report by the International Energy Forum, advanced produced water treatment solutions were deployed across more than 4,800 upstream facilities, improving operational fluid recycling efficiency by 31%, highlighting rapid operational adoption.

Large integrated oil & gas companies dominate the Oilfield Biocides and Bio-Solvents Market with approximately 49% share due to their extensive offshore infrastructure, large-scale unconventional extraction activities, and continuous investment in advanced reservoir management systems. These operators maintain high treatment intensity across mature and high-output fields, making microbial control and sustainable chemical optimization central to operational continuity strategies. Independent shale producers are emerging as the fastest-expanding end-user group, driven by a 34% increase in digitally integrated hydraulic fracturing operations and rising demand for cost-efficient fluid treatment systems. Oilfield service providers and regional exploration firms collectively account for nearly 51% of market demand, with adoption patterns increasingly influenced by localized sourcing strategies and environmental compliance requirements. Compared with large multinational operators, mid-sized exploration firms prioritize modular, lower-cost treatment programs with faster deployment flexibility. Companies are responding through customized chemical formulations, strategic pricing models, and regional supply partnerships optimized for shale-intensive and offshore-sensitive operations. Future demand is clearly shifting toward digitally monitored, low-toxicity treatment systems capable of reducing maintenance frequency and improving reservoir productivity under increasingly strict operational and regulatory conditions.

• According to a 2025 report by the Society of Petroleum Engineers, adoption among independent shale operators increased by 29%, with more than 3,200 upstream sites implementing automated microbial treatment solutions, leading to 23% improvement in operational efficiency, indicating a strong shift in demand dynamics.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2026 and 2033.

North America continues leading global demand due to large-scale shale extraction, offshore drilling intensity, and rapid deployment of automated chemical treatment systems. Europe holds approximately 24% share, driven by strict offshore environmental regulations and accelerated adoption of biodegradable solvent technologies. Asia-Pacific contributes nearly 27% of global demand and is rapidly strengthening its position through refinery expansion, localized chemical production, and rising offshore exploration activity in China, India, and Southeast Asia. Meanwhile, the Middle East & Africa account for 7% share supported by upstream modernization investments, while South America represents 4% with growing deepwater activity in Brazil. Supply chain localization and tightening environmental standards are reshaping regional competitive dynamics, pushing global chemical suppliers toward regional manufacturing expansion and digitally integrated treatment partnerships.

North America holds approximately 38% of the global Oilfield Biocides and Bio-Solvents Market, driven by extensive shale production activity across the Permian Basin, Eagle Ford, and Canadian unconventional reserves. More than 58% of unconventional wells in the region now utilize automated microbial treatment systems integrated with real-time monitoring platforms. Tightening offshore wastewater discharge standards and rising water reuse intensity are forcing operators to adopt biodegradable solvent formulations and high-efficiency oxidizing biocides. Upstream digital optimization deployments increased by 31% between 2024 and 2026, significantly improving treatment precision and operational continuity. Major oilfield service companies are expanding regional blending infrastructure and AI-enabled dosing capabilities to reduce downtime and supply chain dependency. Enterprise buyers increasingly prioritize integrated performance contracts over standalone chemical procurement, reinforcing North America’s position as the highest-value strategic deployment market globally.

Europe accounts for nearly 24% of the global Oilfield Biocides and Bio-Solvents Market, supported by offshore production activity in Norway, the United Kingdom, and the North Sea region. Strict environmental discharge regulations under evolving EU sustainability frameworks are accelerating the replacement of conventional solvents with biodegradable alternatives, with low-toxicity formulation adoption increasing by 37% between 2024 and 2026. Operators are prioritizing advanced microbial control systems capable of reducing hazardous waste generation and improving compliance reporting efficiency. More than 41% of offshore treatment contracts now include sustainability-linked procurement conditions. Chemical suppliers are responding through localized production partnerships and advanced formulation redesign focused on lower environmental impact. Enterprise purchasing behavior remains strongly compliance-driven, with operators favoring premium high-performance treatment systems that optimize operational efficiency while strengthening regulatory alignment and long-term offshore project viability.

Asia-Pacific represents approximately 27% of the global Oilfield Biocides and Bio-Solvents Market and is rapidly strengthening its strategic position through aggressive refinery expansion, offshore exploration growth, and localized chemical manufacturing. China, India, and Southeast Asian producers are increasing upstream treatment deployment intensity as water recycling and high-salinity drilling operations expand across regional energy infrastructure. Localized specialty chemical production capacity increased by 27% between 2024 and 2026, significantly reducing import dependency and improving delivery responsiveness. More than 33% of new offshore treatment contracts now prioritize regionally manufactured formulations to strengthen supply chain stability. Operators across the region continue prioritizing cost-efficient, scalable, and rapidly deployable treatment systems capable of supporting high-volume extraction environments. This combination of scale, infrastructure growth, and operational acceleration is positioning Asia-Pacific as the most critical expansion market for global oilfield chemical suppliers.

South America contributes nearly 4% of the global Oilfield Biocides and Bio-Solvents Market, with Brazil leading regional demand due to expanding offshore deepwater exploration and increasing produced water treatment requirements. Argentina is also strengthening unconventional drilling activity, driving higher deployment of microbial control solutions across shale-intensive operations. However, limited regional chemical processing infrastructure and fluctuating import costs continue constraining large-scale deployment efficiency, increasing procurement lead times by approximately 16%. Despite these limitations, offshore treatment adoption increased by 22% between 2024 and 2026 as operators focused on reducing corrosion-related production losses. Regional buyers remain highly price-sensitive and increasingly prioritize modular, lower-cost treatment systems with localized technical support. The region presents a strong long-term expansion opportunity, but companies must balance infrastructure limitations with strategic investment in regional supply partnerships and operational customization.

The Middle East & Africa account for nearly 7% of the global Oilfield Biocides and Bio-Solvents Market, supported by extensive upstream modernization programs in Saudi Arabia, the UAE, and emerging African offshore projects. Rising water injection intensity and large-scale enhanced oil recovery programs are accelerating demand for advanced microbial treatment systems and high-performance bio-solvents. Regional upstream digital monitoring integration increased by 25% between 2024 and 2026, improving treatment efficiency and reducing fluid maintenance frequency. National oil companies are aggressively expanding strategic partnerships with global oilfield chemical suppliers to strengthen localized production and optimize reservoir management performance. Enterprise buyers prioritize high-durability treatment systems capable of operating under extreme temperature and salinity conditions. Accelerating infrastructure investment and operational modernization are positioning the region as a strategically important market for long-term upstream chemical deployment and production optimization initiatives.

United States – 34% Market share: Dominates due to extensive shale production, advanced upstream digital integration, and large-scale offshore drilling operations.

China – 16% Market share: Holds a major position through aggressive refinery expansion, localized specialty chemical manufacturing, and rising offshore exploration activity.

The Oilfield Biocides and Bio-Solvents Market is dominated by global oilfield chemical leaders including SLB, Baker Hughes, Halliburton, Clariant, Solenis, and Nalco Water, while regional formulators and localized specialty chemical suppliers compete aggressively on pricing and delivery responsiveness. The top five players collectively control nearly 46% of global market activity through vertically integrated production networks, proprietary microbial treatment technologies, and long-term upstream contracts.

Competition is increasingly shifting from commodity chemical supply toward digitally optimized reservoir treatment ecosystems. Global leaders are competing on automation, sustainability performance, and formulation efficiency, while regional suppliers focus on lower-cost customized blends and rapid fulfillment. More than 41% of large offshore contracts now prioritize biodegradable formulations and AI-enabled monitoring compatibility, forcing suppliers to accelerate innovation cycles. Integrated dosing systems reduced chemical waste by 21%, giving technology-driven players a measurable operational advantage over conventional suppliers.

Companies are actively expanding regional blending infrastructure, securing raw material partnerships, and strengthening upstream digital integration capabilities. Market consolidation and supply chain localization are reshaping competitive positioning, while strict environmental qualification standards remain a major entry barrier. Winning in this market now requires scalable sustainable chemistry, localized execution speed, and digitally integrated treatment performance capable of improving upstream operational continuity under increasingly complex reservoir conditions.

Baker Hughes

Halliburton

Clariant AG

Solenis

Nalco Water

BASF SE

Kemira Oyj

Innospec Inc.

Solvay SA

Lubrizol Corporation

Stepan Company

Evonik Industries AG

Flotek Industries

The Oilfield Biocides and Bio-Solvents Market is undergoing rapid technological transformation as operators prioritize microbial control precision, automated treatment optimization, and environmentally compliant fluid management. AI-enabled reservoir analytics platforms are now integrated across nearly 39% of advanced upstream operations, improving contamination detection speed by 34% and reducing unnecessary chemical injection cycles by 17%. Real-time monitoring systems connected with automated dosing infrastructure are redefining upstream maintenance strategies, particularly across offshore and unconventional wells where fluid instability directly impacts production continuity.

Bio-based solvent engineering is emerging as a major disruptive technology area. Compared with conventional petroleum-derived solvent systems, advanced biodegradable formulations improve environmental performance by over 45% while lowering hazardous waste handling requirements by approximately 26%. Operators deploying low-toxicity solvent systems are gaining stronger regulatory positioning in environmentally sensitive offshore regions, particularly in Europe and North America. This transition is benefiting companies with specialized formulation expertise and scalable regional manufacturing capabilities.

Controlled-release microbial treatment technologies are also accelerating deployment across shale-intensive operations. Advanced prolonged-action biocide systems improved bacterial suppression efficiency by nearly 29% in high-salinity reservoirs while extending treatment duration significantly compared with legacy liquid injection systems. Suppliers integrating reservoir analytics with long-duration treatment chemistries are gaining competitive advantage through lower intervention frequency and improved operational stability.

Between 2026 and 2028, the market will increasingly shift toward autonomous treatment optimization ecosystems combining AI analytics, digital reservoir monitoring, and sustainable formulation science. Companies acting early on integrated digital-chemical platforms will strengthen contract retention, improve upstream productivity metrics, and capture the next phase of offshore and unconventional production modernization.

February 2024 – Baker Hughes and Dussur inaugurated the Saudi Petrolite Chemicals facility in Jubail to localize oilfield chemical production, including solvents and specialty treatment solutions. The project exceeded 70% Saudization targets and strengthened regional supply-chain responsiveness for upstream operators. The expansion accelerated localized manufacturing and reduced delivery lead times across Middle Eastern oilfields. [Localization Push] Source: www.bakerhughes.com

July 2024 – Baker Hughes secured multiple Petrobras contracts covering production chemicals, completion fluids, and offshore mature asset solutions in Brazil’s pre-salt and post-salt fields. The integrated deployment strategy supported operational cost reduction and enhanced production continuity across deepwater assets. The agreement strengthened Baker Hughes’ offshore chemicals footprint in Latin America. [Deepwater Expansion]

October 2025 – SLB announced the acquisition of RESMAN Energy Technology to strengthen wireless reservoir surveillance and chemical tracer analytics capabilities. The technology delivers detection precision at parts-per-trillion levels, enabling advanced production optimization and reservoir monitoring. The move accelerated SLB’s digital integration strategy across production chemicals and recovery operations. [Digital Reservoir Shift]

January 2026 – SLB expanded AI-powered production optimization deployment across ADNOC-operated fields using the Lumi data and AI platform. The system processes millions of real-time operational data points, enabling engineers to optimize wells within minutes instead of days. The deployment significantly improved upstream workflow integration and production efficiency at scale. [AI Production Scaling]

The Oilfield Biocides and Bio-Solvents Market Report delivers a comprehensive analysis of upstream chemical treatment technologies, operational deployment trends, and strategic competitive positioning across global oil & gas production environments. The report covers detailed segmentation by type, application, and end-user, including oxidizing biocides, non-oxidizing biocides, biodegradable solvents, drilling fluids, hydraulic fracturing, produced water treatment, integrated oil companies, and independent shale operators. Geographic analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with execution-level insights into regional production dynamics, regulatory transformation, and localized supply-chain expansion.

The study evaluates more than 25 operational indicators and technology adoption signals, including automated dosing penetration, offshore sustainability deployment rates, digital monitoring integration levels, and biodegradable solvent utilization trends. Over 58% of unconventional upstream operators analyzed within the report now prioritize automated microbial treatment systems, while low-toxicity solvent adoption surpassed 40% across environmentally sensitive offshore operations. The report also profiles major global oilfield chemical providers, regional formulation specialists, and digitally integrated treatment innovators shaping competitive dynamics.

From a strategic perspective, the report supports investment planning, regional expansion, procurement optimization, product development, and competitive benchmarking between 2026 and 2033. Special emphasis is placed on AI-enabled treatment systems, localized blending infrastructure, sustainable formulation technologies, and advanced reservoir analytics transforming future upstream operational performance.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 125.0 Million |

| Market Revenue (2033) | USD 229.7 Million |

| CAGR (2026–2033) | 7.9% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | SLB; Baker Hughes; Halliburton; Clariant AG; Solenis; Nalco Water; BASF SE; Kemira Oyj; Innospec Inc.; Solvay SA; Lubrizol Corporation; Stepan Company; Evonik Industries AG; Flotek Industries |

| Customization & Pricing | Available on Request (10% Customization Free) |