Reports

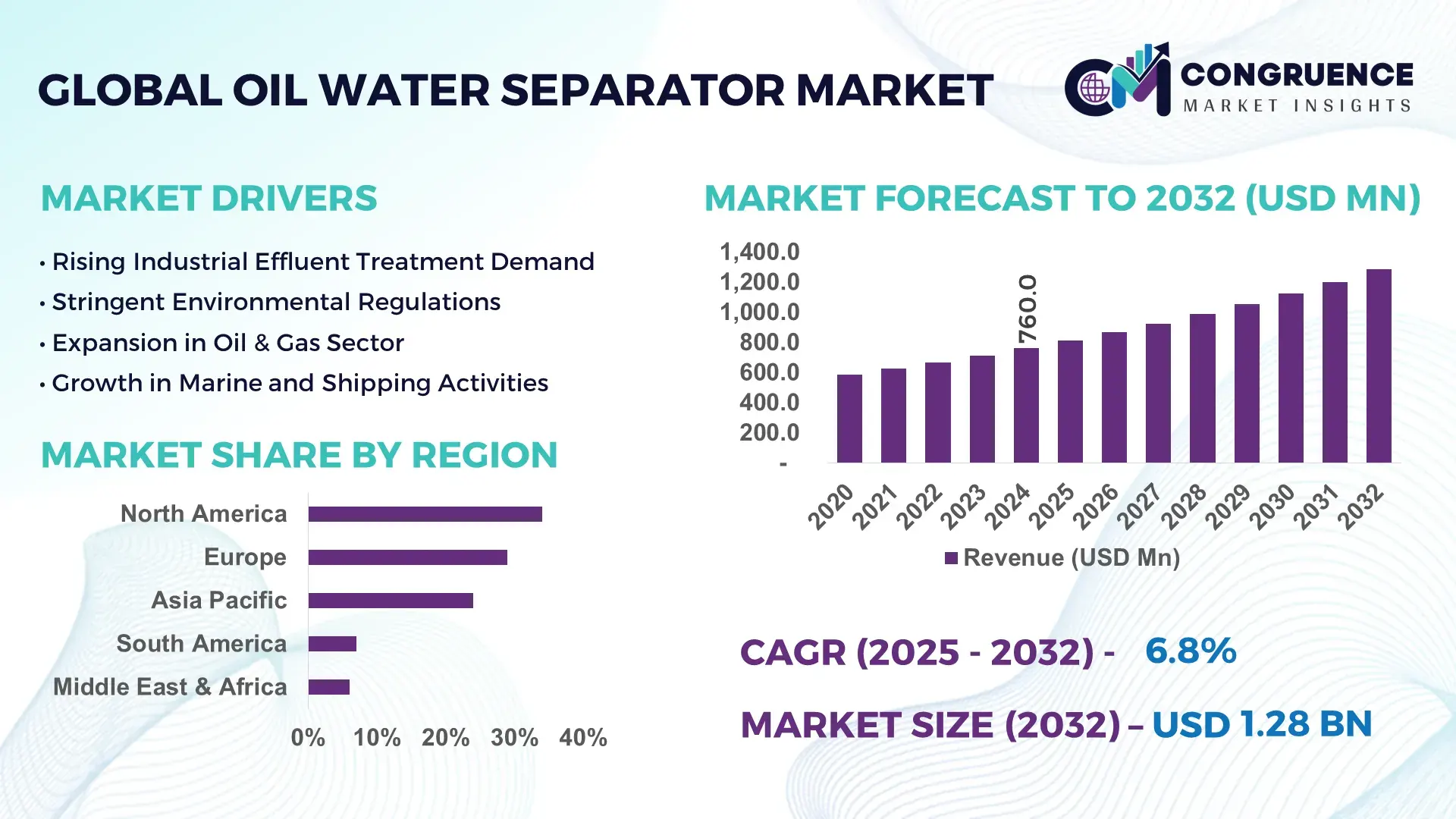

The Global Oil Water Separator Market was valued at USD 760.0 Million in 2024 and is anticipated to reach USD 1,283.5 Million by 2032, expanding at a CAGR of 6.77% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven primarily by tightening water-discharge regulations and rising industrial wastewater volumes.

The United States plays a pivotal role in the global Oil Water Separator landscape, supported by its extensive industrial infrastructure and robust environmental compliance ecosystem. The country houses more than 8,000 active wastewater treatment facilities, with over 65% utilizing advanced separation systems across petrochemical, marine, and manufacturing sectors. Investments exceeding USD 2.2 billion between 2020–2024 have focused on automated oil-water separation technologies, including coalescing and membrane-based separators tailored for high-load industrial applications. Additionally, the U.S. recorded a 22% increase in industrial wastewater recycling projects, strengthening demand for high-efficiency separators.

Market Size & Growth: Valued at USD 760.0 Million in 2024, projected to reach USD 1.28 Billion by 2032 at a 6.77% CAGR, supported by rising industrial wastewater management requirements.

Top Growth Drivers: 48% increase in industrial discharge monitoring, 37% efficiency improvement in coalescing systems, and 29% rise in compliance-driven retrofits.

Short-Term Forecast: By 2028, system performance efficiency is expected to improve by 32% through automated detection and sludge-reduction technologies.

Emerging Technologies: Advancements in membrane-integrated separators, AI-enabled monitoring platforms, and corrosion-resistant composite materials.

Regional Leaders: North America projected to reach USD 410 Million by 2032; Europe expected to hit USD 360 Million with strong industrial adoption; Asia-Pacific to reach USD 335 Million driven by expanding chemical processing.

Consumer/End-User Trends: Increasing adoption across marine, petrochemical, and food-processing sectors, with over 52% of facilities shifting toward automated separation units.

Pilot or Case Example: In 2024, a refinery pilot achieved 41% downtime reduction using an AI-enabled separation monitoring solution.

Competitive Landscape: Market leader holds approximately 12% share, with notable competitors including Alfa Laval, Parker Hannifin, Andritz, and HydroFloTech.

Regulatory & ESG Impact: Stricter discharge norms driving 35% higher investment in compliant separator installations; industries targeting 25% wastewater recycling improvements by 2030.

Investment & Funding Patterns: Over USD 500 Million invested recently in industrial water treatment upgrades and automated separation systems.

Innovation & Future Outlook: Increased integration of IoT-based sensors, hybrid separation units, and modular treatment platforms expected to shape future market evolution.

The Oil Water Separator Market is witnessing advancements in high-efficiency coalescing media, membrane innovations, and automated monitoring tools. Strong investment in industrial wastewater treatment, evolving environmental regulations, and greater adoption across petrochemical, marine, and manufacturing sectors continue to stimulate market expansion across key regions.

The Oil Water Separator Market plays a strategically vital role in ensuring industrial compliance, environmental protection, and operational continuity across sectors handling wastewater and hydrocarbon discharge. Its relevance has grown significantly as industries face tightening regulatory frameworks and escalating environmental scrutiny. Across manufacturing, marine, petrochemical, and transportation sectors, separators enable measurable reductions in oil contaminants, with advanced coalescing and membrane systems now delivering up to 42% improved separation efficiency compared to conventional gravity-based systems.

From a regional standpoint, North America dominates in volume, supported by mature industrial infrastructure, while Europe leads in adoption, with over 58% of enterprises using automated or semi-automated separation technologies. The market is transitioning toward digitally enabled operations where AI-driven monitoring platforms and sensor-integrated units improve detection accuracy by 35%. By 2027, real-time monitoring and automated back-flush systems are expected to reduce operational downtime by up to 30% across key industries.

Sustainability is becoming central to strategic pathways. Firms are targeting wastewater recycling and pollution-reduction commitments, aiming for 20–30% improvements by 2030. In 2024, an oil & gas operator in the Middle East achieved a 26% reduction in effluent contamination through an automated coalescing-separation upgrade integrated with predictive analytics.

Looking forward, the Oil Water Separator Market is positioned as a cornerstone of compliance-driven industrial modernization. It will continue to support sustainable growth, enhanced operational resilience, and long-term environmental stewardship across global industries.

The Oil Water Separator Market is characterized by steady technological progress, regulatory influence, and rising industrial demand for efficient wastewater management solutions. Industries such as petrochemicals, marine transport, food processing, and manufacturing are significantly increasing their reliance on advanced separation systems due to escalating wastewater discharge volumes, higher contamination levels, and growing enforcement of effluent standards. The adoption of automated separators, membrane-integrated systems, and IoT-enabled monitoring tools is accelerating operational efficiency and improving separation accuracy. Moreover, global investments in industrial water treatment and recycling infrastructure continue to strengthen the market’s trajectory, contributing to the adoption of next-generation oil-water separation technologies.

Rising industrial activity across petrochemical, marine, manufacturing, and power sectors is significantly increasing wastewater discharge volumes containing oil, grease, and hydrocarbons. Industries are generating over 320 billion liters of oily wastewater annually, necessitating efficient separation systems to meet stringent effluent discharge limits. The increased use of heavy-duty lubricants and hydraulic fluids leads to higher contamination loads, requiring advanced coalescing and membrane technologies capable of separation efficiencies above 90%. Moreover, industrial facilities are upgrading their treatment lines with automated separators featuring real-time monitoring, which enhances detection accuracy by 35% and reduces manual intervention. Such operational improvements and compliance needs are intensifying market demand.

Although critical for industrial wastewater management, oil-water separators can face significant operational constraints due to sludge buildup, inconsistent flow rates, corrosion, and wear from abrasive contaminants. Many older installations experience up to 28% efficiency loss over time without periodic maintenance. Membrane-based systems, while efficient, often require specialized cleaning and can exhibit fouling issues that increase downtime by 10–15% annually. Additionally, smaller facilities struggle with the costs of installing automated monitoring systems, which can raise operational budgets by 18%. These challenges reduce lifecycle performance and may delay modernization investments across resource-constrained sectors.

Growing global initiatives targeting industrial wastewater recycling are creating substantial opportunities for next-generation oil-water separation technologies. Industries are increasingly adopting closed-loop systems aimed at achieving 25–40% reductions in freshwater consumption. Advanced separators integrated with membrane filtration and AI-based monitoring can enhance recovery rates, enabling reuse of treated water for cooling, cleaning, and processing applications. Additionally, the rapid expansion of manufacturing, marine logistics, and energy sectors in Asia-Pacific—where industrial wastewater volumes are rising by 7–9% annually—presents a strong avenue for technology deployment. These trends are driving demand for high-efficiency, low-maintenance separation units capable of functioning in diverse industrial environments.

The market faces structural challenges stemming from the increasing cost of advanced separation systems, particularly those integrating membrane filtration, AI-based monitoring, and anti-corrosion materials. Prices for high-capacity systems have grown by 12–18% due to material and automation costs. Furthermore, regulatory frameworks vary widely across regions, requiring industries to meet compliance thresholds that can differ by 30–50% in pollutant limits. This lack of standardization complicates procurement, installation, and certification processes. Smaller enterprises face difficulties aligning with inspection schedules, maintenance requirements, and reporting mandates, creating operational barriers that slow widespread adoption.

Surge in Automated Monitoring and Smart Separation Units: Adoption of AI-enabled monitoring systems is increasing rapidly, with industries reporting 35% higher detection accuracy and 28% lower manual intervention after integration. Automated separators equipped with real-time sensors improved operational uptime by 22% in 2024. Global installations of smart separation units grew by 18%, driven by digital transformation initiatives across manufacturing and petrochemical sectors.

Expansion of High-Efficiency Coalescing Technologies: Next-generation coalescing media capable of delivering up to 42% improved separation efficiency saw accelerated adoption in marine and refining sectors. Demand for advanced coalescers increased by 31% due to stricter effluent regulations and the need for low-maintenance systems. Several regions recorded up to 25% reductions in oil concentrations in treated wastewater following coalescing upgrades.

Rising Integration of Membrane-Based Separation Systems: Membrane separators are gaining traction due to their ability to handle high contamination loads, with adoption increasing by 27% in 2024 across chemical and metals processing industries. New ceramic and polymeric membranes demonstrated 20–35% longer life cycles and reduced fouling rates, improving operational cost efficiency by 15%. Modular membrane systems saw particularly strong deployment in Asia-Pacific.

Growth in Industrial Water Recycling and Reuse Initiatives: Industries worldwide are increasing wastewater recycling rates, achieving 20–30% reuse improvements through hybrid membrane–coalescing systems. Manufacturing plants adopting integrated recycling achieved 19% reductions in freshwater withdrawal and 14% reductions in effluent discharge. This trend is accelerating demand for advanced separators capable of supporting closed-loop industrial operations.

The Oil Water Separator Market is segmented across type, application, and end-user categories, each reflecting distinct adoption behaviors and technical performance requirements. Product types vary from coalescing, gravity-based, and membrane-based separators to hydrocyclone and custom hybrid systems, each supporting specific industrial discharge profiles. Applications span marine operations, petrochemical effluent management, manufacturing wastewater, and food and beverage processing, driven by evolving regulatory thresholds and rising contaminant loads. End-user demand is shaped by industrial wastewater volume, automation maturity, and compliance mandates, with heavy industries such as oil & gas, chemicals, and marine logistics showing significantly higher adoption levels. Collectively, segmentation underscores the market’s shift toward automated, high-efficiency, and low-maintenance systems, supported by tightened discharge norms and increased investments in sustainable industrial water treatment.

The Oil Water Separator Market includes several key product types: coalescing separators, gravity-based units, hydrocyclone separators, membrane-based systems, and specialized hybrid solutions. Coalescing separators currently lead the market with 41% adoption, owing to their high separation efficiency, suitability for variable flow rates, and lower maintenance requirements. Gravity-based separators account for 23% adoption, commonly used in legacy installations and low-load discharge environments. Hydrocyclone separators hold 17%, offering strong performance in continuous high-pressure operations. Membrane-based separators represent the fastest-growing type, supported by advancements in ceramic and polymeric membranes, delivering improved oil rejection levels and CAGR of 8.2% attributed to their increasing use in high-contaminant industrial settings. Video-like adoption comparison format: while coalescing systems maintain 41%, membrane technologies are rising rapidly and projected to exceed 30% adoption by 2032, compared to hydrocyclone systems holding 17%. Other types, including hybrid units integrating membrane and coalescing media, collectively contribute 19%, serving niche requirements in petrochemicals and offshore operations.

Oil Water Separators are utilized across marine discharge treatment, petrochemicals, industrial manufacturing, food & beverage processing, power generation, and municipal/utility wastewater operations. The marine sector leads with 38% application share, driven by stringent bilge water discharge limits and increasing digitalization of onboard wastewater systems. Petrochemical applications account for 27%, supported by rising oily sludge production and increased investment in automated separation units. Industrial manufacturing accounts for 22%, reflecting high hydraulic and lubricating oil usage. The fastest-growing application is petrochemical wastewater processing, expanding at 7.9% CAGR, as facilities adopt membrane-integrated and AI-enabled systems to meet tightening contaminant thresholds. As a comparative adoption pattern: marine holds 38%, petrochemicals 27%, but industrial manufacturing adoption is rising fastest and expected to approach 30% by 2032. Other applications—including food & beverage, power generation, and municipal systems—hold a combined 13%, driven by stricter hygiene and environmental standards.

End-users span oil & gas, marine logistics, chemical processing, manufacturing, food & beverage, utilities, and power generation industries. The oil & gas sector dominates with 39% share, reflecting high wastewater volumes, elevated hydrocarbon content, and increased compliance-driven retrofits. Marine logistics follows with 26%, supported by global maritime pollution standards and fleet modernization. Manufacturing industries represent 21%, driven by increased use of lubricants and hydraulic oils. The fastest-growing end-user group is manufacturing, expanding at 8.4% CAGR, fueled by automation of wastewater lines, near-zero discharge policies, and integration of smart monitoring modules. As a comparative benchmark: oil & gas stands at 39%, marine at 26%, while manufacturing adoption is projected to exceed 28% by 2032. Other end-users—including food processing, utilities, and power generation—account for a combined 14%, with adoption rates increasing as sustainability targets intensify. Industry adoption statistics indicate that 34% of manufacturing plants globally implemented digital monitoring systems in 2024 to enhance separator efficiency, while 29% of marine operators adopted hybrid separation units to meet upcoming discharge thresholds.

North America accounted for the largest market share at 34% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2025 and 2032.

The global Oil Water Separator Market demonstrates significant regional variation, with adoption influenced by industrial density, environmental norms, and wastewater management maturity. Europe followed with 29% market share in 2024, driven by strict discharge standards and rising industrial retrofitting activities. Asia-Pacific captured 24% share, supported by rapid manufacturing expansion and growing marine activities. South America and the Middle East & Africa held 7% and 6% shares respectively, with rising investments in petrochemical infrastructure and port modernization. Countries such as the U.S., China, Germany, Japan, and the UAE remain critical demand centers, each contributing over 5% individually. Demand patterns also vary by end-users—North America shows high adoption from offshore oil operators, Europe from chemical industries, and Asia-Pacific from manufacturing clusters.

North America accounted for 34% market share in 2024, making it the largest regional contributor, supported by extensive oil & gas operations, maritime activities, and advanced wastewater treatment regulations. The U.S. remains the dominant country, with major demand from refineries, chemical plants, and automotive manufacturing hubs. Industries such as offshore drilling, shipping, and industrial wastewater reclamation are accelerating equipment adoption across both new installations and replacement cycles. Regulatory frameworks emphasizing lower effluent contamination levels have led to rapid modernization of separation infrastructure. Technological advancements such as automated monitoring systems, coalescing plate design enhancements, and remote diagnostics are increasingly deployed to optimize separation efficiency. A local player example includes a U.S.-based separation technology company expanding its skid-mounted separator product line for modular industrial deployment. Consumer behavior in this region shows higher enterprise adoption in healthcare, finance, and heavy industries, reflecting strong compliance-driven investment patterns.

Europe held 29% market share in 2024, led by Germany, the UK, and France, which collectively account for more than 18% of regional demand. Strict environmental standards and strong alignment with sustainability initiatives, particularly those targeting clean water, industrial emissions, and circular wastewater reuse, drive the uptake of high-efficiency separators. Industries such as automotive manufacturing, maritime shipping, and chemical processing are substantial adopters. Regulatory bodies enforcing stringent water discharge norms continue to push industries toward high-performance separation systems incorporating membrane-based coalescers and automated compliance monitoring. A leading European equipment supplier recently expanded its compact separator line for marine vessels to meet enhanced port regulatory checks. Consumer behavior also diverges regionally, with European industries demonstrating strong preference for explainable, audit-friendly treatment technologies, ensuring full traceability of effluent quality and environmental impact.

Asia-Pacific ranked third in 2024 with 24% market share, but it remains the fastest-advancing region based on volume adoption. China, India, Japan, and South Korea collectively account for over 70% of regional consumption, driven by rapid industrialization, maritime traffic expansion, and manufacturing growth. Infrastructure upgrades across petrochemical plants, industrial estates, shipyards, and power facilities are fueling the installation of next-generation separators optimized for heavy loads and variable discharge conditions. Innovation hubs in Japan and South Korea are accelerating digital transformation through IoT-enabled influent monitoring and automated sludge-handling solutions. A regional manufacturer recently introduced high-capacity coalescing separators for wastewater-heavy industries such as textiles and food processing. Consumer behavior trends show higher adoption of mobile-integrated compliance monitoring tools, with growth largely driven by e-commerce, industrial logistics, and mobile AI applications that support process automation and predictive maintenance.

South America represented 7% market share in 2024, with Brazil and Argentina accounting for nearly 68% of regional demand. Growth is strongly influenced by expanding energy activities, offshore exploration, and industrial wastewater management efforts. Infrastructure investments in petrochemicals, mining effluents, and marine transport facilities are improving adoption rates for separator units across both public and private sectors. Governments are prioritizing water conservation policies and trade incentives supporting upgrades to treatment facilities. A Brazilian industrial equipment supplier recently increased production of portable separators for on-site industrial spill control, catering to diverse manufacturing clusters. Regional consumer behavior trends indicate rising demand tied to media, language localization technologies, and industrial modernization, supporting broader adoption of automated compliance solutions across manufacturing environments.

The Middle East & Africa accounted for 6% of the global market in 2024, driven by high oil & gas activity, large desalination infrastructure, and industrial wastewater treatment requirements across the UAE, Saudi Arabia, and South Africa. Regional demand is supported by increased refinery expansions, new port developments, and construction sector growth requiring compliant effluent handling systems. Digital modernization, including remote monitoring and AI-driven system optimization, is becoming more prominent across industrial zones. A UAE-based maritime solutions provider recently incorporated advanced coalescers into offshore supply vessels to meet evolving discharge norms. Consumer behavior indicates elevated adoption within industrial hubs, driven by compliance requirements and investment in resilient, automated water treatment systems.

United States – 22% Market Share: Strong dominance due to extensive oil & gas operations, large industrial base, and stringent effluent discharge compliance requirements.

China – 18% Market Share: Leadership driven by massive manufacturing output, expanding port capacity, and high wastewater generation across industrial clusters.

The global Oil Water Separator Market is moderately consolidated yet highly competitive, with estimates indicating around 15–20 leading global manufacturers and dozens of mid-size and niche suppliers actively competing for industrial, marine, petrochemical, and wastewater-treatment contracts. The top five companies — including Alfa Laval, Parker Hannifin, GEA Group, Andritz AG and Wärtsilä Oyj Abp — collectively hold approximately 60% of the global market share, reflecting a moderately consolidated structure but leaving substantial room for smaller specialised firms and regional players.

Competitive intensity is driven by strategic initiatives such as product launches, technological upgrades, and collaborations. For instance, companies are rolling out compact, modular separators for smaller vessels and plants, and adding IoT-enabled monitoring, automated sludge-handling, and remote diagnostics to improve reliability and reduce maintenance. Mergers, acquisitions, and partnerships are being used to expand geographical footprints and service networks. Innovation trends — such as membrane-based separation, hybrid coalescing–membrane systems, and energy-efficient centrifugal units — differentiate players in high-performance segments, particularly for offshore, petrochemical, and wastewater-intensive industries.

The market remains dynamic: while large firms benefit from global distribution and R&D scale, smaller and regional manufacturers compete on customisation, responsiveness, and niche applications (e.g., small marine vessels, modular industrial plants). This diversity supports a resilient competitive ecosystem that balances consolidation with ongoing innovation and market entry opportunities.

Andritz AG

Wärtsilä Oyj Abp

Sulzer Chemtech

Donaldson Company, Inc.

Compass Water Solutions

ZCL Composites Inc.

HydroFloTech

Technology evolution in the Oil Water Separator Market is accelerating across several dimensions — separation efficiency, automation, monitoring, modularity, and environmental sustainability. The growing shift from traditional gravity-based and static coalescer units to membrane-based separators, centrifugal systems, and hybrid coalescing-membrane designs has significantly enhanced the ability to treat highly contaminated effluents, handle variable flow rates, and meet tighter discharge standards. Membrane separators now often reject oil droplets down to sub-micron sizes and extend service life by up to 30% compared to older models, reducing maintenance frequency and downtime.

Automation and smart monitoring have become critical differentiators. Many new separators incorporate IoT-enabled sensors that monitor influent water quality, flow rates, and separator health in real time; about 45% of newly installed units in 2023–2024 featured remote diagnostics or predictive-maintenance capabilities. This reduces manual oversight, improves reliability, and lowers operational costs. Further, modular and compact designs have grown in popularity — especially for marine vessels, small industrial plants, and retrofit projects — reducing installation footprint by up to 40% and enabling flexible deployment.

Energy efficiency and sustainability are also shaping technology choices. New-generation centrifugal separators consume less power per cubic meter treated and waste less sludge, aligning with corporate ESG goals and environmental regulations. In addition, hybrid systems combining coalescing, membrane, and chemical pretreatment allow for robust performance even in complex industrial wastewater streams, making them well-suited for petrochemical, manufacturing, and oil & gas sectors.

Overall, advancements in materials science, automation, and modular engineering are transforming the Oil Water Separator Market — enabling higher performance, lower lifetime costs, and greater compliance robustness. For decision-makers, investing in next-generation separator technologies translates into long-term operational efficiency, regulatory resilience, and sustainable water management.

Alfa Laval (Jan 24, 2023): Alfa Laval announced a new range of biofuel-ready high-speed separators for the marine sector, compatible with HVO and FAME blends. The release highlights equipment upgrades to handle alternative fuels and support shipowners’ decarbonization plans. Source: www.alfalaval.com

ANDRITZ (May 2024 / IFAT 2024): ANDRITZ exhibited an expanded portfolio of water/wastewater separation and automation solutions at IFAT 2024 (Munich), showcasing membrane, filtration, and digital automation offerings intended for industrial effluent and recycling applications. Source: www.andritz.com

Sulzer (Mid-2024): Sulzer’s mid-year 2024 report recorded a notable increase in order intake and sales for its Flow division, reflecting higher demand for engineered fluid-handling and separation solutions across industrial water and process markets during H1 2024. Source: www.sulzer.com

Donaldson (FY24 / product focus): Donaldson’s FY24 sustainability and product materials cite enhancements to condensate and oil-water separation product lines (Ultrasep and related condensate management systems), noting improved filtration performance and deployment across compressed-air/process condensate applications in 2024. Source: www.donaldson.com

This Oil Water Separator Market Report provides a comprehensive analysis of global and regional market dynamics, covering multiple separator types — including gravity, coalescing plate, centrifugal, hydrocyclone, and membrane-based systems — and their suitability across diverse applications such as marine wastewater, petrochemical effluent treatment, manufacturing wastewater, food & beverage processing, power generation, and municipal treatment. The report spans all major regions: North America, Europe, Asia-Pacific, South America, Middle East & Africa, offering insight into regional drivers, regulatory environments, and infrastructure maturity.

In addition to technical segmentation, the report examines end-user industries such as oil & gas, chemical, manufacturing, marine, utilities, and industrial wastewater service providers, exploring adoption patterns, retrofit cycles, and green-compliance investments. It includes analysis of installation types — above-ground, below-ground, skid-mount, and portable units — to address application-specific deployment constraints. The study also assesses emerging technologies such as IoT-enabled monitoring systems, modular compact separator designs, membrane and hybrid separation technologies, and automated sludge handling, considering their impact on operational efficiency, maintenance reduction, and lifecycle cost.

Finally, the report provides competitive landscape insights, profiling major global players, their strategic initiatives, innovation capabilities, and regional footprints, to enable decision-makers to benchmark potential partners or competitors. It further explores market opportunities tied to evolving environmental regulations, increasing wastewater volumes, and growing demand for sustainable treatment solutions — providing a holistic roadmap for investors, manufacturers, and industrial end-users seeking to align with future trends in oil-water separation.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 760.0 Million |

| Market Revenue (2032) | USD 1,283.5 Million |

| CAGR (2025–2032) | 6.77% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Regulatory & ESG Overview |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Alfa Laval, Parker Hannifin, GEA Group, Andritz AG, Wärtsilä Oyj Abp, Sulzer Chemtech, Donaldson Company, Inc., Compass Water Solutions, ZCL Composites Inc., HydroFloTech |

| Customization & Pricing | Available on Request (10% Customization Free) |