Reports

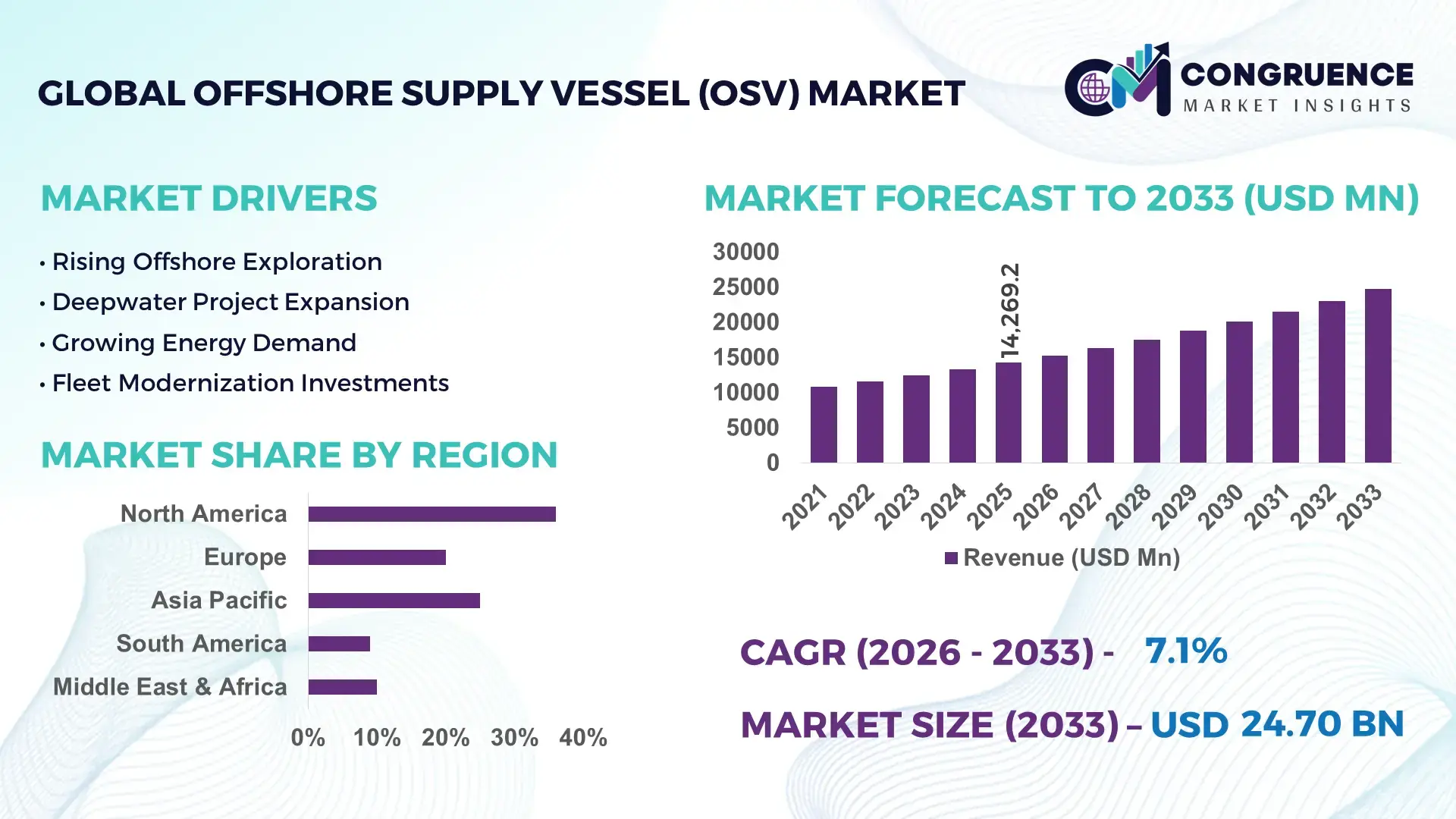

The Global Offshore Supply Vessel (OSV) Market was valued at USD 14269.19 Million in 2025 and is anticipated to reach a value of USD 24701.03 Million by 2033 expanding at a CAGR of 7.1% between 2026 and 2033. Growth is being accelerated by deepwater offshore exploration programs, expanding offshore wind installation fleets, and rising demand for advanced platform support vessels equipped with hybrid propulsion and digital fleet management systems.

Norway remains the dominant country in the Offshore Supply Vessel (OSV) Market, accounting for approximately 18% of the global advanced OSV fleet, supported by substantial investments in offshore energy infrastructure and vessel electrification programs. More than 35% of newly contracted North Sea support vessels incorporate hybrid or low-emission technologies, strengthening operational efficiency and regulatory compliance. Compared with Brazil, where offshore pre-salt developments continue driving vessel utilization above 80% in key basins, Norway maintains a stronger concentration of technologically advanced vessels and higher digital fleet integration rates. The ongoing focus on energy security following disruptions linked to the Russia-Ukraine geopolitical environment has further reinforced offshore project commitments and vessel deployment activity across European waters.

Market participants that prioritize technologically advanced, fuel-efficient fleets and strategic positioning near high-investment offshore energy hubs are securing stronger contract visibility and long-term operational advantages.

Market Size & Growth: USD 14,269.19 million in 2025 reaching USD 24,701.03 million by 2033 at 7.1% CAGR, driven by offshore wind expansion and deepwater energy investments.

Top Growth Drivers: Deepwater exploration (+28%), offshore wind installations (+31%), and fleet digitalization adoption (+22%) continue accelerating vessel demand.

Short-Term Forecast: By 2028, fuel costs decline 12% while fleet utilization efficiency improves 15% through hybrid propulsion integration.

Emerging Technologies: AI-based route optimization, autonomous monitoring systems, and hybrid-electric propulsion improve operational performance by 10–18%.

Regional Leaders: Europe exceeds USD 7.2 billion, Asia-Pacific USD 6.5 billion, and Latin America USD 4.8 billion, supported by offshore project expansion.

Consumer/End-User Trends: More than 40% of offshore operators prioritize low-emission vessels and digital fleet management capabilities.

Pilot/Case Example: 2025 hybrid OSV deployments in the North Sea reduced fuel consumption by approximately 18% during offshore operations.

Competitive Landscape: Top operators collectively hold nearly 35% market share alongside leading global fleet service providers and specialized vessel owners.

Regulatory & ESG Impact: Emission-reduction initiatives cut vessel carbon intensity by nearly 20%, supporting compliance and contract competitiveness.

Investment & Funding: Over USD 5 billion in fleet modernization, offshore wind logistics, and regional expansion projects amid supply-chain realignment.

Innovation & Future Outlook: Next-generation autonomous support systems and alternative-fuel vessels are expected to increase fleet productivity by over 15%.

The Offshore Supply Vessel (OSV) Market is experiencing strong demand from offshore oil, gas, and renewable energy projects requiring reliable logistics and platform support services. Advanced hybrid propulsion systems, AI-enabled fleet optimization, and predictive maintenance technologies are improving vessel performance and reducing operating costs by nearly 15%. Growing offshore wind developments, stricter emission regulations, and evolving supply-chain requirements are reshaping fleet investment strategies, setting the stage for deeper strategic market evaluation.

The Offshore Supply Vessel (OSV) Market is becoming strategically important as offshore energy operators prioritize logistics reliability, asset utilization, and operational resilience across deepwater oil, gas, and offshore wind developments. Competitive differentiation increasingly depends on vessel efficiency, digital fleet visibility, and low-emission capabilities rather than fleet size alone. A notable market shift is the integration of digital fleet management platforms, enabling operators to optimize routing, maintenance scheduling, and fuel consumption while strengthening supply-chain continuity in high-activity offshore corridors.

Technology modernization is reshaping fleet economics. Hybrid-powered OSVs typically reduce fuel consumption by 15–20% compared with conventional diesel-powered vessels while lowering maintenance requirements through predictive monitoring systems. Norway continues to lead in advanced vessel deployment and electrification initiatives, whereas Brazil focuses on large-scale offshore support capacity linked to pre-salt field developments. More than 35% of newly contracted high-specification vessels now incorporate digital monitoring technologies, reflecting a clear industry transition toward data-driven operations and asset optimization.

Recent deployments supporting offshore wind installation projects have demonstrated measurable gains in vessel utilization and scheduling efficiency. Companies are expanding strategic partnerships with technology providers, investing in fleet retrofits, and prioritizing multi-purpose vessel capabilities. Over the next two to three years, digital integration and low-emission vessel adoption are expected to accelerate, reinforcing competitive positioning for operators capable of delivering reliable, technology-enabled offshore support services.

Rising investment in offshore energy infrastructure remains the primary growth catalyst for the Offshore Supply Vessel (OSV) Market. Deepwater exploration activity has increased by nearly 25% over the past several years, while offshore wind project pipelines have expanded by more than 30%, creating sustained demand for platform supply vessels, anchor handlers, and crew transfer operations. Norway and Brazil continue advancing large offshore developments that require high-specification vessel support and year-round logistics capabilities. The growing adoption of hybrid propulsion technologies, now incorporated in approximately 35% of newly contracted advanced vessels, is improving operational efficiency and contract attractiveness. In response, vessel operators are pursuing fleet modernization programs, strategic partnerships, and targeted vessel acquisitions. A key strategic insight is that operators with technologically advanced fleets are securing longer contract durations and stronger utilization rates in premium offshore markets.

High capital intensity and fleet availability constraints continue limiting operational scalability across the Offshore Supply Vessel (OSV) Market. New vessel construction costs have increased by approximately 20–25% compared with pre-disruption levels due to elevated steel prices, equipment costs, and shipyard capacity constraints. In Singapore and South Korea, extended delivery schedules have pushed lead times upward by nearly 30%, delaying fleet expansion plans. At the same time, stricter environmental compliance requirements are increasing retrofit expenditures for aging vessels. These pressures directly affect profitability, charter competitiveness, and deployment flexibility. To mitigate risk, operators are adopting long-term charter agreements, diversifying shipyard relationships, and prioritizing vessel refurbishment programs. A significant operational insight is that companies extending asset life through targeted upgrades often achieve better capital efficiency than pursuing aggressive newbuild strategies.

Digital transformation and offshore renewable energy logistics present substantial opportunities for OSV operators. AI-enabled fleet optimization platforms can improve route efficiency by 12–18%, while predictive maintenance systems reduce unplanned downtime by nearly 20%. The United Kingdom and Denmark are expanding offshore wind infrastructure programs that require specialized support vessels, creating demand beyond traditional oil and gas operations. More than 40% of large offshore operators are increasing investment in digital asset management capabilities to improve scheduling accuracy and resource allocation. Companies are responding through technology partnerships, fleet retrofits, and development of multi-purpose support vessels capable of serving both hydrocarbon and renewable projects. A non-obvious strategic opportunity lies in integrating offshore wind logistics with conventional offshore support networks, allowing operators to improve vessel utilization across multiple energy sectors.

Managing increasingly sophisticated offshore operations remains a significant long-term challenge. Advanced vessels equipped with automation, digital diagnostics, and hybrid propulsion systems require specialized technical expertise, yet skilled maritime workforce availability remains constrained in key markets. Training requirements for advanced vessel crews have increased by approximately 15%, while digital system integration complexity has grown by more than 20% as operators deploy connected technologies across fleets. In Norway and the United Kingdom, cybersecurity requirements for connected offshore assets are becoming more stringent, increasing compliance and monitoring obligations. Failure to address these challenges can reduce deployment consistency, operational reliability, and competitive differentiation. Companies are investing in workforce development programs, cybersecurity infrastructure, and technology partnerships. A critical strategic insight is that operational excellence increasingly depends on human-capital readiness as much as vessel technology advancement.

• Hybrid Fleet Deployment Accelerates Hybrid and low-emission propulsion systems are moving from pilot programs to mainstream fleet upgrades. Nearly 35% of newly contracted high-specification vessels now incorporate hybrid technologies, while fuel consumption reductions of 15–20% are being achieved during offshore operations. Stricter emissions regulations in Norway and the United Kingdom are accelerating adoption. Vessel owners are responding through retrofit programs, technology partnerships, and fleet renewal strategies that improve charter competitiveness and operational efficiency.

• Digital Vessel Operations Expand Fleet operators are rapidly integrating predictive maintenance, remote diagnostics, and AI-enabled route optimization platforms. Digital monitoring adoption has increased by approximately 30% among advanced offshore fleets, reducing unplanned downtime by nearly 18% and improving vessel utilization rates. Labor constraints and operational complexity are driving this transition. Companies are restructuring maintenance workflows and deploying centralized fleet management systems to enhance scheduling precision and lower lifecycle operating costs.

• Offshore Wind Logistics Diversify Offshore wind construction activity is creating new deployment models for support vessels beyond traditional oil and gas operations. Demand for specialized logistics support has increased by more than 25%, while multi-mission vessel utilization has improved by roughly 12%. Denmark and the United Kingdom continue expanding offshore wind infrastructure, prompting vessel operators to scale renewable-energy service portfolios and develop long-term partnerships with project developers.

• Multi-Purpose Vessel Preference Grows Operators increasingly favor versatile vessels capable of supporting drilling, cargo transport, subsea activities, and renewable energy projects from a single platform. Fleet flexibility requirements have risen by nearly 20%, while vessel redeployment efficiency has improved by approximately 15%. A non-obvious shift is the growing emphasis on contract adaptability rather than vessel specialization. Companies are investing in modular equipment configurations and integrated service offerings to maximize utilization across changing offshore project cycles.

Platform Supply Vessels (PSVs) remain the leading segment, accounting for approximately 40% of offshore support deployments due to their critical role in transporting equipment, fuel, water, and supplies to offshore installations. Their dominance is supported by high utilization rates, operational flexibility, and lower per-mission logistics costs compared with specialized vessel classes. Multipurpose Support Vessels represent the fastest-growing segment, with demand increasing by nearly 18% as operators seek flexible assets capable of serving offshore wind, subsea, and energy infrastructure projects. Anchor Handling Vessels continue to play a vital role in rig positioning and towing operations, particularly in Brazil and the North Sea. Crew Boats remain essential for personnel movement, while Seismic Vessels support offshore resource assessment and field development planning. In response to evolving offshore requirements, vessel operators are investing in hybrid propulsion systems, modular deck configurations, and digital fleet management capabilities. Investment priorities increasingly favor flexible, multi-role vessel platforms capable of supporting multiple offshore industries while maintaining strong utilization levels.

Drilling Support remains the dominant application segment, representing nearly 35% of vessel deployment activity due to continuous requirements for rig supply, equipment transportation, anchoring assistance, and operational logistics. Offshore exploration programs in Brazil, Norway, and the Gulf of Mexico continue sustaining demand concentration within this segment. Subsea Operations is emerging as the fastest-growing application, supported by rising investments in underwater infrastructure, inspection services, and field maintenance activities, with deployment demand increasing by approximately 17%. Cargo Transport remains a mature but essential segment supporting production continuity and supply-chain efficiency. Crew Transfer services continue expanding alongside offshore wind developments, while Survey Services are gaining importance through advanced seabed mapping and resource assessment technologies. Operators are responding by expanding specialized capabilities, integrating digital navigation systems, and deploying multi-functional vessels. Demand is increasingly shifting toward applications that combine logistics efficiency with technical offshore service capabilities, creating higher-value operational contracts.

Oil and Gas Companies remain the dominant end-user segment, accounting for approximately 55% of offshore vessel demand due to extensive drilling, production support, logistics, and maintenance requirements across offshore fields. Their operational intensity and infrastructure dependency continue driving long-term vessel utilization. Offshore Wind Operators represent the fastest-growing buyer group, with procurement activity increasing by nearly 20% as large-scale offshore renewable projects require installation support, crew transfer, and maintenance logistics. Marine Service Providers maintain strong demand through contract-based offshore support operations and integrated vessel management services. Government Agencies continue utilizing specialized vessels for maritime infrastructure and emergency response missions, while the Defense Sector increasingly deploys support vessels for offshore surveillance and strategic maritime operations. Companies are adapting through customized vessel offerings, long-term service agreements, and renewable-energy-focused fleet expansion programs. Future demand is gradually shifting toward diversified offshore energy applications, encouraging operators to position fleets for both traditional hydrocarbon and renewable infrastructure support.

Europe accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.4% between 2026 and 2033.

Deepwater Operations and Fleet Modernization Drive Demand

North America represents approximately 24% of global Offshore Supply Vessel (OSV) activity, supported by sustained offshore exploration and production programs in the Gulf of Mexico. High-specification platform supply vessels and anchor handling units remain heavily utilized due to increasing deepwater project complexity and longer operational cycles. Digital fleet management adoption has surpassed 30% among leading operators, improving scheduling efficiency and vessel utilization. Fleet modernization programs, including hybrid propulsion retrofits and predictive maintenance technologies, are gaining momentum as operators focus on operational reliability and compliance requirements. Strategic partnerships between offshore service providers and energy companies continue strengthening long-term vessel deployment visibility while supporting offshore infrastructure expansion.

United States Market Outlook: The United States remains the operational center of the North American market due to its concentration of offshore production assets, advanced port infrastructure, and established maritime service ecosystem. Gulf Coast logistics hubs support a substantial share of offshore vessel deployments, while investment in digital fleet optimization continues accelerating. More than 60% of offshore support activity in the region is linked to U.S. offshore developments, creating sustained demand for technologically advanced vessels and integrated support services.

Low-Emission Fleet Transition Reshapes Operations

Europe maintains the largest market position with approximately 34% share, supported by extensive offshore energy infrastructure and advanced maritime capabilities. The region is leading the transition toward hybrid-powered and low-emission support vessels, driven by stringent environmental regulations and offshore sustainability initiatives. More than 35% of newly contracted high-specification vessels incorporate hybrid technologies. Offshore wind developments across the North Sea continue expanding vessel deployment requirements, while digital fleet monitoring systems are improving operational efficiency. Companies are investing in vessel electrification, emissions reduction technologies, and multi-purpose support platforms capable of serving both hydrocarbon and renewable energy sectors.

Norway Market Outlook: Norway remains the most strategically significant market due to its advanced offshore ecosystem, strong shipbuilding expertise, and leadership in maritime decarbonization. The country operates one of the world's most technologically sophisticated OSV fleets, with hybrid vessel adoption significantly exceeding global averages. Government-backed innovation initiatives and strong offshore investment pipelines continue supporting fleet upgrades, autonomous vessel testing, and next-generation propulsion system deployment across offshore operations.

Offshore Expansion and Shipbuilding Strength Accelerate Growth

Asia-Pacific accounts for approximately 27% of market activity and represents the fastest-evolving offshore vessel landscape. Offshore developments in Southeast Asia, Australia, and emerging energy corridors are increasing vessel demand, while the region's shipbuilding capacity strengthens fleet availability. Shipyards in major maritime economies continue expanding production capabilities, supporting both domestic deployment and export demand. Infrastructure investments linked to offshore gas projects and renewable energy installations have increased vessel utilization rates by nearly 15% in key markets. Operators are prioritizing fleet expansion, operational digitization, and advanced vessel configurations to support increasingly complex offshore requirements.

China Market Outlook: China benefits from substantial shipbuilding capacity, integrated maritime supply chains, and expanding offshore energy investments. The country plays a critical role in vessel construction and fleet modernization, supporting both domestic and international demand. Large-scale port infrastructure and industrial manufacturing capabilities provide cost and scale advantages. Offshore wind deployment programs and offshore energy infrastructure development continue creating sustained demand for support vessel services and specialized offshore logistics operations.

Pre-Salt Development Sustains Vessel Demand

South America holds approximately 9% of global market activity, with offshore vessel demand heavily concentrated around deepwater hydrocarbon developments. Large-scale offshore projects continue driving deployment of platform supply vessels, anchor handling vessels, and subsea support units. Vessel utilization levels in key offshore basins frequently exceed 80%, reflecting strong operational requirements. Infrastructure limitations and periodic fleet availability constraints remain challenges, yet continued offshore investment supports stable deployment activity. Companies are expanding regional partnerships, strengthening maintenance capabilities, and enhancing local support infrastructure to improve operational responsiveness.

Brazil Market Outlook: Brazil dominates regional offshore vessel demand due to extensive pre-salt field developments and long-term offshore production programs. The country's offshore sector requires continuous logistics support, specialized vessel services, and advanced subsea operations. Deepwater project activity continues supporting high vessel deployment rates, while investments in offshore infrastructure and local maritime capabilities strengthen operational resilience. Brazil remains the primary strategic market for fleet operators seeking sustained offshore contract opportunities.

Energy Infrastructure Investments Support Modernization

The Middle East & Africa region accounts for approximately 6% of global market activity and is increasingly shaped by offshore infrastructure modernization initiatives. Expanding offshore production capacity, maritime logistics investments, and vessel support requirements are driving demand for advanced offshore services. Several offshore developments have increased support vessel deployment needs by more than 12% over recent years. Operators are investing in fleet capability upgrades, operational efficiency improvements, and integrated offshore support solutions. Infrastructure expansion programs and strategic maritime investments continue strengthening the region's offshore service ecosystem.

Saudi Arabia Market Outlook: Saudi Arabia represents the most influential market within the region due to extensive offshore energy infrastructure, long-term production programs, and ongoing maritime investment initiatives. Offshore field development projects continue generating demand for logistics support, maintenance services, and specialized vessel deployment. Investments in port modernization, offshore industrial facilities, and operational efficiency programs are enhancing the country's offshore support capabilities while creating opportunities for advanced vessel operators and service providers.

The Offshore Supply Vessel (OSV) Market is led by operators such as Tidewater, Edison Chouest Offshore, Bourbon, Solstad Offshore, and DOF Group, competing against regional fleet owners and specialized offshore service providers. The top five players collectively control approximately 32–36% of global fleet capacity. Competition is centered on vessel availability, fuel efficiency, digital fleet management, and contract execution reliability rather than price alone. Hybrid-powered vessels can lower fuel consumption by 15–20%, while digital monitoring systems improve utilization rates by nearly 12%, creating measurable competitive advantages. Global leaders compete through fleet modernization, offshore wind expansion strategies, long-term charter agreements, and strategic partnerships with energy companies. Regional operators focus on local infrastructure access and cost-efficient deployment models. Market competition is shifting toward technologically advanced multi-purpose vessels and integrated service offerings. High capital requirements, vessel construction lead times, and regulatory compliance obligations remain significant entry barriers. Success increasingly depends on fleet quality, operational flexibility, technology integration, and long-term customer relationships.

Tidewater Inc.

Edison Chouest Offshore

Bourbon Corporation

Solstad Offshore ASA

DOF Group ASA

SEACOR Marine Holdings Inc.

Hornbeck Offshore Services

Havila Shipping ASA

Siem Offshore Inc.

Swire Pacific Offshore

Vroon Offshore Services

GulfMark Offshore

Atlantic Offshore

PACC Offshore Services Holdings (POSH)

Digital fleet management platforms, predictive maintenance systems, and hybrid propulsion technologies represent the most influential technologies currently shaping the Offshore Supply Vessel (OSV) Market. More than 35% of newly contracted high-specification vessels now integrate hybrid power systems, reducing fuel consumption by 15–20% and lowering maintenance costs by approximately 10%. Predictive maintenance adoption has surpassed 30% among advanced fleets, helping operators reduce unplanned downtime by nearly 18%. These technologies are improving vessel utilization, contract performance, and operational reliability in increasingly competitive offshore environments.

Emerging technologies are centered on AI-enabled route optimization, remote vessel monitoring, and advanced subsea robotics integration. AI-assisted navigation platforms improve voyage efficiency by 8–12% compared with conventional planning methods, while digital operational centers enhance fleet visibility across multiple offshore assets. Multipurpose vessels equipped with integrated ROV and autonomous inspection capabilities are seeing increased deployment. Operators in Norway, Brazil, and the United Kingdom are scaling technology partnerships and fleet retrofits to strengthen operational flexibility and support more complex offshore energy projects.

Disruptive innovation is increasingly focused on autonomous vessel operations, uncrewed inspection systems, and low-emission maritime technologies. Compared with traditional diesel-powered vessels, hybrid-enabled platforms deliver up to 20% greater operational efficiency under dynamic offshore conditions. Between 2026 and 2028, autonomous monitoring deployments are expected to exceed 25% of advanced offshore fleets. Early adopters gain stronger asset utilization, lower operating costs, and enhanced contract competitiveness, creating a clear advantage over operators relying on conventional vessel architectures.

July 2024 – DOF Group announced the acquisition of Maersk Supply Service for approximately USD 1.11 billion, adding 22 vessels and strengthening offshore wind, subsea, and energy service capabilities. The transaction significantly expanded global fleet scale and operational reach. Source: dof.com

May 2025 – Omega Subsea and Solstad Offshore awarded a contract for 12 new remotely operated vehicle systems, including 8 units dedicated to Solstad-supported projects. The deployment increased subsea intervention capacity and enhanced offshore project execution capabilities. Source: solstad.com

June 2025 – Solstad Offshore secured a four-year contract with Petrobras for the CSV Normand Flower. The long-term award strengthened vessel utilization visibility, expanded Brazilian offshore activity, and reinforced the company’s position in deepwater support operations.

August 2025 – Solstad Offshore received a four-year Petrobras contract for the CSV Normand Commander valued at approximately USD 108 million excluding ROV services. The award increased offshore construction support capacity and improved long-term contract-backed fleet deployment.

This report provides a comprehensive assessment of the Offshore Supply Vessel (OSV) Market across key vessel categories including Platform Supply Vessels, Anchor Handling Vessels, Crew Boats, Multipurpose Support Vessels, and Seismic Vessels. The analysis evaluates critical applications such as drilling support, cargo transport, crew transfer, subsea operations, and survey services, while examining demand patterns across oil and gas companies, offshore wind operators, marine service providers, government agencies, and defense organizations. More than 40% of recent fleet modernization activity is linked to digitalization, hybrid propulsion adoption, and operational efficiency initiatives.

The study delivers detailed regional insights covering North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting deployment concentration, infrastructure investments, and technology adoption trends. It evaluates competitive positioning, fleet expansion strategies, offshore energy transitions, and emerging opportunities in offshore wind logistics, autonomous operations, and subsea service integration. The report supports investment planning, market entry decisions, partnership development, fleet optimization strategies, and long-term competitive positioning through 2026–2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 14269.19 Million |

|

Market Revenue in 2033 |

USD 24701.03 Million |

|

CAGR (2026 - 2033) |

7.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Tidewater Inc., Edison Chouest Offshore, Bourbon Corporation, Solstad Offshore ASA, DOF Group ASA, SEACOR Marine Holdings Inc., Hornbeck Offshore Services, Havila Shipping ASA, Siem Offshore Inc., Swire Pacific Offshore, Vroon Offshore Services, GulfMark Offshore, Atlantic Offshore, PACC Offshore Services Holdings (POSH) |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |