Reports

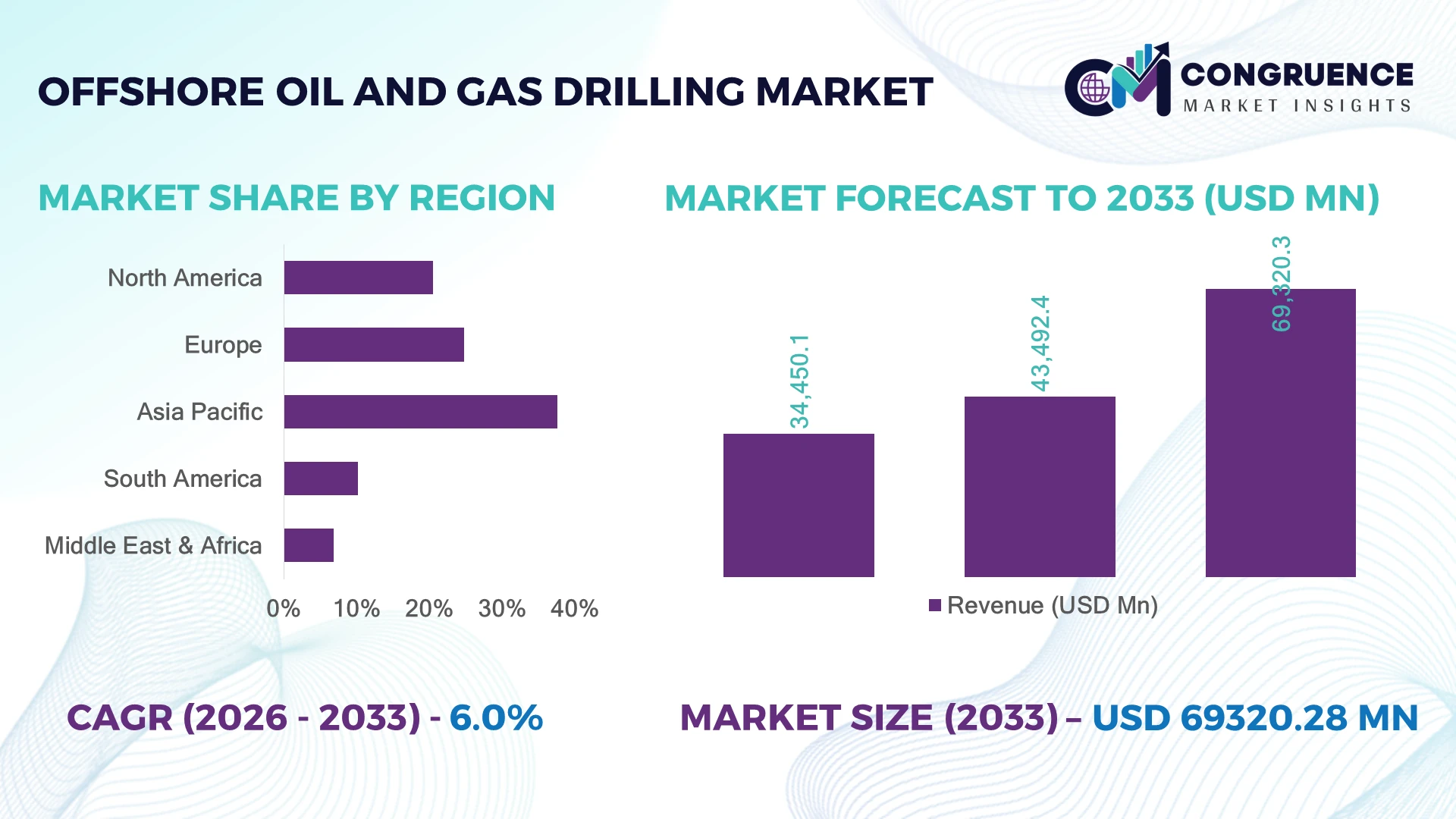

The Global Offshore Oil and Gas Drilling Market was valued at USD 43,492.4 Million in 2025 and is anticipated to reach a value of USD 69,320.3 Million by 2033 expanding at a CAGR of 6.0% between 2026 and 2033. Growth is being driven by sustained deepwater exploration investments, increasing offshore field redevelopment, higher floating rig utilization, and digital drilling technologies improving operational efficiency.

Norway remains one of the dominant countries in advanced offshore drilling, accounting for approximately 18% of global floating production activity and operating more than 90 producing offshore fields supported by extensive subsea infrastructure. Compared with Brazil, where ultra-deepwater developments exceed 2,000 meters, Norway leads in digital offshore operations and low-emission drilling technologies. Continued geopolitical emphasis on European energy security following recent supply-chain realignment has accelerated offshore licensing and infrastructure investments, strengthening long-term production resilience.

The market increasingly rewards operators capable of combining high-efficiency drilling assets with digital operations and lower-emission offshore production strategies.

Market Size & Growth: USD 43,492.4 Million (2025) to USD 69,320.3 Million (2033) at 6.0% CAGR, supported by deepwater investments and offshore field redevelopment.

Top Growth Drivers: Deepwater exploration (58%), floating rig utilization (49%), digital drilling adoption (36%).

Short-Term Forecast: By 2028, AI-assisted drilling is expected to reduce non-productive time by 22%.

Emerging Technologies: Autonomous drilling, digital twins, predictive maintenance, and advanced subsea robotics.

Regional Leaders: Asia-Pacific (~USD 20 Billion), Europe (~USD 18 Billion), North America (~USD 15 Billion) with expanding offshore investments.

End-User Trends: Nearly 61% of offshore operators prioritize intelligent drilling analytics over conventional monitoring.

Operational Example: A 2025 offshore drilling optimization program improved rig utilization by 18%.

Competitive Landscape: Transocean leads with approximately 15% market presence, followed by Valaris, Noble Corporation, Seadrill, and COSL.

Regulatory & ESG: Offshore methane reduction initiatives improved operational efficiency by nearly 19%.

Investment Activity: More than USD 75 billion committed globally toward offshore upstream developments since 2024.

Innovation Outlook: Automated drilling systems and remote offshore operations continue reshaping competitive positioning.

The Offshore Oil and Gas Drilling Market continues expanding across deepwater, ultra-deepwater, and mature offshore basins as operators modernize rigs, improve subsea connectivity, and integrate predictive maintenance technologies. Nearly 43% of newly sanctioned offshore developments now incorporate digital drilling platforms, while energy security priorities continue supporting long-cycle offshore investment, naturally leading into the market's evolving strategic landscape.

The Offshore Oil and Gas Drilling Market continues to strengthen its strategic position as governments and energy companies prioritize long-term hydrocarbon security, reserve replacement, and production resilience. Offshore developments are increasingly preferred for their large recoverable reserves and stable production profiles, particularly as mature onshore assets experience declining output. Following global energy supply realignment and expanding offshore licensing activity, operators are accelerating investment in deepwater assets supported by modern floating production systems, digital well planning, and integrated subsea infrastructure.

Advanced automated drilling systems improve drilling efficiency by approximately 24% compared with conventional manual drilling methods while reducing non-productive time by nearly 20% through predictive analytics and continuous equipment monitoring. Norway leads digital offshore field operations with high levels of automation, whereas Brazil continues expanding ultra-deepwater developments supported by large FPSO deployments and extensive subsea production networks. By 2028, remote drilling operations and AI-assisted decision support are expected to reduce drilling intervention requirements by approximately 18%, improving operational continuity across offshore assets.

Major offshore contractors are increasing investment in seventh-generation drillships, intelligent well monitoring, and strategic technology partnerships to improve drilling precision and asset utilization. National oil companies are simultaneously expanding offshore licensing rounds and strengthening collaborations with drilling contractors to accelerate field development while improving environmental performance. As offshore operations become increasingly digital and capital-intensive, competitive advantage will depend on operational efficiency, technological integration, and the ability to consistently deliver complex offshore projects with lower emissions and improved production reliability.

The Offshore Oil and Gas Drilling Market is undergoing structural transformation as energy companies prioritize high-productivity offshore assets capable of delivering stable long-term production with improved operational efficiency. Digital drilling platforms, intelligent well construction, automated rig operations, and advanced subsea technologies are reshaping offshore project economics across deepwater and ultra-deepwater developments. Governments continue supporting offshore licensing to strengthen domestic energy security, while operators increasingly modernize drilling fleets to improve safety, reliability, and environmental performance. Competition is steadily shifting toward technology-enabled execution, operational uptime, and lifecycle cost optimization rather than drilling capacity alone.

Deepwater field development remains the primary growth engine for the Offshore Oil and Gas Drilling Market. Approximately 57% of recently sanctioned offshore projects target deepwater and ultra-deepwater reservoirs, while seventh-generation drillships improve drilling efficiency by nearly 26% compared with legacy offshore fleets. Brazil and Guyana continue expanding offshore developments, encouraging drilling contractors to reactivate premium assets and secure multi-year contracts. Equipment suppliers are responding through automated drilling systems, advanced blowout preventers, and predictive maintenance technologies that improve equipment reliability. A notable strategic shift is the industry's growing preference for high-specification rigs capable of supporting longer drilling campaigns with reduced downtime and lower operating costs.

Offshore drilling projects continue facing structural pressure from rising equipment costs, constrained shipyard availability, and extended procurement cycles for specialized subsea components. Nearly 46% of offshore operators identify long equipment lead times as a significant execution constraint, while premium offshore rig day rates have increased by approximately 32% compared with pre-2022 levels. In the United Kingdom, stricter offshore equipment certification requirements have further lengthened project schedules for selected developments. Companies are reducing operational exposure through localized sourcing strategies, long-term supply agreements, and standardized engineering solutions that improve procurement efficiency while reducing project execution risk.

Digital transformation presents one of the largest long-term opportunities across the Offshore Oil and Gas Drilling Market. Nearly 62% of newly approved offshore developments now incorporate AI-assisted drilling analytics, while predictive maintenance platforms reduce unplanned equipment failures by approximately 21%. Norway and Saudi Arabia continue investing in intelligent offshore infrastructure integrating remote operations, subsea monitoring, and digital asset management systems. Offshore contractors are expanding software partnerships, autonomous inspection capabilities, and robotics deployment to improve operational efficiency. A significant competitive opportunity lies in continuous drilling optimization using real-time operational data, enabling measurable improvements in well performance, equipment utilization, and overall field productivity.

The increasing technical complexity of offshore developments presents a major execution challenge for drilling contractors and operators. Nearly 41% of offshore companies report shortages of experienced drilling engineers and subsea specialists, while modern offshore projects integrate approximately 30% more digital control systems than conventional developments. In the Gulf of Mexico, modernization of aging offshore infrastructure continues to increase project coordination requirements and maintenance intensity. Companies are responding through digital twin implementation, workforce training, remote operations centers, and automated inspection technologies that improve operational consistency. Long-term competitiveness increasingly depends on combining engineering expertise with digital capability to safely execute technologically sophisticated offshore developments at commercial scale.

Digital Rig Intelligence Expansion Offshore operators are rapidly integrating intelligent drilling platforms, with approximately 59% of premium rigs utilizing real-time drilling analytics and automated performance optimization. These technologies improve drilling efficiency by nearly 23% while reducing non-productive time by approximately 19%. Contractors continue upgrading fleets with AI-assisted monitoring systems and centralized remote operation centers to maximize asset utilization and drilling consistency.

Floating Production Deployment Growth Floating production systems continue gaining momentum alongside new deepwater discoveries. Approximately 52% of recently sanctioned offshore developments now incorporate FPSO infrastructure, reducing field development timelines by nearly 18% compared with conventional fixed-platform projects. Brazil and Guyana remain the principal deployment markets, encouraging engineering contractors to expand fabrication capacity and strengthen long-term subsea integration partnerships.

Autonomous Inspection Adoption Offshore operators are expanding the use of autonomous underwater vehicles and robotic inspection systems across mature offshore assets. Robotic inspection programs have reduced manual offshore inspection requirements by approximately 27% while improving equipment anomaly detection by nearly 22%. Growing workforce constraints and stricter offshore safety regulations are accelerating investment in autonomous asset integrity management technologies.

Lower-Emission Offshore Operations Carbon management has become an operational priority as offshore producers modernize drilling fleets and production facilities. Nearly 38% of newly upgraded offshore rigs now incorporate hybrid power systems or energy-efficiency improvements capable of reducing fuel consumption by approximately 15%. Operators continue investing in electrification projects, digital energy management, and lower-emission drilling technologies to improve environmental performance while maintaining production efficiency.

The Offshore Oil and Gas Drilling Market is segmented by type, application, and end-user, reflecting differences in reservoir depth, operational complexity, production objectives, and investment strategies. Operators increasingly prioritize drilling technologies that maximize well productivity while reducing operating costs and environmental impact. Advanced floating assets, automated drilling systems, and intelligent well management continue reshaping capital allocation across offshore developments. Nearly 61% of newly sanctioned offshore projects now incorporate digital drilling technologies, while integrated subsea production systems have become standard across large deepwater developments. Segmentation trends indicate a clear transition toward technically advanced offshore projects requiring higher-specification rigs, greater automation, and long-term production optimization.

The Offshore Oil and Gas Drilling Market is segmented into Jack-up Rigs, Semi-submersible Rigs, Drillships, and Others.

Jack-up rigs remain the largest segment, accounting for approximately 42% of global drilling activity due to their cost efficiency, operational flexibility, and suitability for shallow-water developments across the Middle East, Southeast Asia, and the North Sea. Their comparatively lower mobilization costs and established operating history continue supporting demand for development drilling, workover operations, and infill wells. Contractors continue upgrading existing jack-up fleets with automated pipe handling systems and digital drilling controls to improve operational productivity and safety.

Drillships represent the fastest-growing segment as operators increasingly prioritize deepwater and ultra-deepwater exploration. Expected to expand at approximately 7.8% annually through the forecast period, drillships benefit from dynamic positioning systems, extended drilling capability, and superior mobility. Semi-submersible rigs continue serving harsh-environment offshore projects, while other specialized offshore drilling assets maintain strategic importance across mature producing basins. Companies continue investing in seventh-generation drillships, automated drilling technologies, and fleet modernization to capture increasing demand from deepwater developments.

According to the International Association of Drilling Contractors' 2025 fleet assessment, utilization of premium offshore drilling units remained significantly higher than older-generation rigs as operators increasingly favored technically advanced assets for complex offshore developments.

The Offshore Oil and Gas Drilling Market is segmented into Exploration Drilling, Development Drilling, and Production Drilling.

Development Drilling represents the largest application segment with approximately 46% of offshore activity as operators prioritize maximizing output from proven offshore reserves. Growing investment in brownfield optimization, field expansion, and enhanced reservoir recovery continues supporting long-term demand. Digital well planning, automated directional drilling, and real-time formation evaluation improve drilling precision while reducing non-productive time by nearly 19%, enabling operators to achieve higher recovery efficiency from existing offshore assets.

Exploration Drilling is the fastest-growing application as national oil companies and international operators expand exploration activity across frontier offshore basins in South America, Africa, and the Eastern Mediterranean. Production Drilling continues supporting mature offshore fields through infill wells and reservoir maintenance programs. Operators increasingly integrate AI-assisted well planning, predictive maintenance, and remote drilling centers to improve project execution while maintaining operational discipline under increasingly complex offshore conditions.

Findings published by the International Energy Agency during 2025 indicated that offshore upstream investment continued shifting toward long-life producing assets, with development drilling accounting for the largest share of newly sanctioned offshore capital expenditure.

The Offshore Oil and Gas Drilling Market is segmented into National Oil Companies (NOCs), International Oil Companies (IOCs), and Independent Oil & Gas Companies.

National Oil Companies remain the dominant end-user group, accounting for approximately 49% of offshore drilling demand due to large offshore lease holdings, long-term production strategies, and sustained capital investment programs. National operators across Saudi Arabia, Brazil, Abu Dhabi, and Norway continue expanding offshore developments supported by integrated infrastructure and multi-year drilling campaigns. Nearly 63% of recently awarded long-term offshore drilling contracts involve NOC-led projects, reinforcing their influence over fleet utilization and contractor investment decisions.

International Oil Companies represent the fastest-growing end-user segment as global energy companies increase deepwater exploration, floating production developments, and offshore reserve replacement activities. Independent operators continue focusing on niche offshore opportunities, particularly in mature producing regions where smaller field developments remain commercially attractive. Drilling contractors are responding through customized contract structures, integrated drilling services, strategic technology partnerships, and performance-based operating models designed to improve long-term customer retention and operational efficiency.

According to the 2026 Offshore Energy industry outlook, National Oil Companies continued leading offshore capital allocation, while International Oil Companies accelerated investment in high-productivity deepwater developments supported by advanced drilling technologies.

Asia-Pacific accounted for the largest market share at 37.6% in 2025 however, South America is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

Asia-Pacific remains the largest offshore drilling market owing to extensive offshore production across China, Malaysia, Indonesia, Australia, and India, supported by continuous investments in deepwater developments and offshore infrastructure. Europe accounted for approximately 24.8% of global activity through mature North Sea operations and ongoing field redevelopment, while North America represented nearly 20.5% driven by sustained drilling activity in the Gulf of Mexico. South America is witnessing the strongest investment momentum as Brazil and Guyana continue expanding ultra-deepwater production capacity. The Middle East & Africa continue strengthening offshore exploration through new licensing rounds and offshore gas developments. Approximately 64% of newly sanctioned offshore projects are concentrated within Asia-Pacific and South America, reflecting the industry's continued transition toward high-productivity offshore basins supported by modern drilling technologies and long-term capital investment.

High-Specification Fleet Modernization Strengthens Offshore Operations

North America accounts for approximately 20.5% of the global Offshore Oil and Gas Drilling Market, supported primarily by sustained drilling activity in the Gulf of Mexico and increasing investment in high-specification offshore assets. Operators continue prioritizing long-life deepwater projects capable of delivering stable production while maximizing operational efficiency through digital drilling systems and predictive maintenance platforms. Nearly 68% of active floating drilling units operating in the Gulf of Mexico are sixth- or seventh-generation rigs equipped with automated drilling technologies. Contractors continue strengthening strategic partnerships with technology providers to improve drilling performance, reduce operational downtime, and enhance offshore safety through intelligent asset monitoring.

United States Market Outlook: The United States dominates regional offshore drilling activity through extensive Gulf of Mexico infrastructure, advanced drilling technology, and mature offshore service capabilities. More than 90% of domestic offshore crude production originates from deepwater developments, while operators continue investing in digital drilling platforms, subsea production systems, and floating production infrastructure to maximize recovery from existing offshore assets and newly sanctioned developments.

Mature Basin Optimization Drives Operational Efficiency

Europe represents approximately 24.8% of the Offshore Oil and Gas Drilling Market, supported by continued investment in North Sea field redevelopment, offshore gas production, and lower-emission offshore operations. Norway and the United Kingdom account for nearly 76% of regional offshore drilling activity through advanced subsea infrastructure and high levels of drilling automation. Operators increasingly focus on extending field life using intelligent well management, enhanced recovery techniques, and digital asset optimization. More than 52% of active offshore developments now incorporate remote operations and predictive maintenance technologies, improving production reliability while reducing offshore intervention requirements.

Norway Market Outlook: Norway remains Europe's leading offshore drilling market through its technologically advanced continental shelf, extensive subsea production systems, and strong regulatory framework supporting efficient offshore development. Approximately 70% of producing offshore fields utilize integrated digital monitoring platforms, while continued investment in electrification, carbon management, and intelligent drilling technologies reinforces the country's leadership in sustainable offshore production.

Large Offshore Resource Base Supports Long-Term Expansion

Asia-Pacific leads the global Offshore Oil and Gas Drilling Market with approximately 37.6% of worldwide activity, driven by expanding offshore exploration, increasing natural gas production, and continued investment in deepwater infrastructure. China, Australia, Malaysia, Indonesia, and India collectively account for nearly 81% of regional offshore drilling operations. National energy companies continue prioritizing offshore developments to strengthen domestic energy security while reducing import dependency. Nearly 47% of newly commissioned offshore support vessels globally are deployed across Asia-Pacific, reflecting the region's extensive offshore development pipeline and growing subsea engineering capacity.

China Market Outlook: China remains the largest offshore drilling market within Asia-Pacific through continuous offshore exploration in the Bohai Bay, South China Sea, and East China Sea. Offshore production infrastructure continues expanding alongside advanced domestic drilling capabilities, while national energy companies invest heavily in intelligent drilling systems, offshore gas developments, and floating production technologies to strengthen long-term energy independence.

Deepwater Discoveries Accelerate Offshore Investment

South America accounts for approximately 10.2% of the global Offshore Oil and Gas Drilling Market and continues recording the strongest investment momentum through large-scale offshore discoveries and production expansion. Brazil and Guyana together represent more than 84% of regional offshore capital expenditure, supported by world-class pre-salt reservoirs and floating production developments. Operators continue deploying high-specification drillships, subsea production equipment, and advanced reservoir monitoring technologies. Nearly 56% of recently awarded ultra-deepwater drilling contracts globally are associated with projects across these two countries, highlighting their growing importance within the global offshore industry.

Brazil Market Outlook: Brazil dominates the regional market through extensive pre-salt developments supported by large floating production systems and advanced deepwater drilling expertise. National and international operators continue expanding long-term drilling programs while integrating digital reservoir management, subsea processing technologies, and automated drilling systems that improve operational efficiency across ultra-deepwater assets.

Offshore Gas Development Reshapes Regional Investment

The Middle East & Africa account for approximately 6.9% of the Offshore Oil and Gas Drilling Market as governments accelerate offshore gas exploration, production diversification, and infrastructure modernization. Saudi Arabia, the United Arab Emirates, Qatar, Egypt, Angola, and Nigeria continue investing in offshore developments to strengthen export capacity and domestic energy supply. More than 43% of recently announced offshore gas projects within the region involve integrated subsea production systems and advanced offshore processing infrastructure. Operators increasingly adopt digital drilling technologies, intelligent well monitoring, and predictive maintenance platforms to improve project economics while supporting long-term production growth.

Saudi Arabia Market Outlook: Saudi Arabia continues expanding offshore production capacity through significant investment in offshore oil and natural gas developments across the Arabian Gulf. National energy companies are strengthening offshore drilling capability by deploying advanced jack-up rigs, intelligent drilling systems, and integrated digital field management platforms that improve drilling efficiency while supporting long-term production optimization.

The Offshore Oil and Gas Drilling Market is characterized by competition between global offshore drilling contractors such as Transocean, Valaris, Noble Corporation, Seadrill, and China Oilfield Services (COSL), alongside regional drilling companies and integrated oilfield service providers. Premium fleet owners compete on drilling capability, automation, and operational reliability, while regional contractors focus on cost-efficient shallow-water operations and localized service delivery. The top five companies collectively account for approximately 48% of the global offshore drilling fleet. Competition increasingly centers on high-specification rig availability, digital drilling performance, contract duration, and operational efficiency rather than pricing alone. Seventh-generation drillships improve drilling productivity by nearly 24%, while predictive maintenance platforms reduce unplanned downtime by approximately 20%. Contractors continue expanding through fleet reactivations, long-term charter agreements, strategic technology partnerships, and selective acquisitions. High capital requirements, stringent safety regulations, and limited premium rig availability remain significant entry barriers. Sustainable competitive leadership increasingly depends on technologically advanced fleets, execution consistency, and long-term customer relationships.

Seadrill Limited

China Oilfield Services Limited (COSL)

Borr Drilling Limited

Shelf Drilling Ltd.

Saipem S.p.A.

ADNOC Drilling Company PJSC

KCA Deutag

Nabors Industries Ltd.

Stena Drilling Ltd.

Diamond Offshore Drilling Inc.

Japan Drilling Co., Ltd.

Digital technologies are fundamentally transforming offshore drilling operations by improving drilling precision, equipment reliability, and asset utilization. Automated drilling systems, AI-assisted well planning, digital twins, predictive maintenance, and advanced real-time analytics have become standard across premium offshore drilling fleets. Nearly 62% of newly contracted offshore rigs now incorporate intelligent drilling control systems capable of reducing non-productive time by approximately 22% while improving drilling consistency under complex geological conditions. Remote operations centers further enhance operational visibility by integrating drilling, production, and maintenance data into centralized decision-making platforms.

Advanced subsea technologies are also reshaping offshore field development. Autonomous underwater vehicles, remotely operated vehicles, intelligent blowout preventers, and permanently installed subsea monitoring systems improve inspection efficiency by nearly 28% while reducing manual offshore intervention requirements by approximately 24%. Compared with conventional inspection programs, AI-enabled predictive maintenance allows operators to identify equipment degradation earlier, lowering maintenance costs and extending asset life. Major offshore contractors and national oil companies benefit most from these technologies because improved equipment availability directly enhances contract performance and field productivity.

Between 2026 and 2028, autonomous drilling, robotics-assisted subsea intervention, hybrid-powered offshore rigs, and edge-based operational analytics are expected to become mainstream across large offshore developments. Compared with conventional drilling workflows, fully integrated digital drilling ecosystems are projected to improve operational efficiency by approximately 30% while reducing fuel consumption by nearly 15%. Companies investing early in intelligent drilling platforms, digital infrastructure, and low-emission offshore technologies will strengthen competitiveness as offshore projects become increasingly automated, data-driven, and operationally optimized.

May 2025 – Transocean Ltd. secured a drilling contract for the Deepwater Aquila drillship in the U.S. Gulf of Mexico valued at approximately USD 232 million, extending fleet utilization through 2028 and strengthening long-term offshore backlog visibility. Source: https://www.deepwater.com

February 2025 – Valaris Limited received a contract award for the drillship VALARIS DS-15 offshore West Africa, adding approximately USD 135 million to contracted backlog while reinforcing demand for seventh-generation deepwater drilling assets. Source: https://www.valaris.com

September 2024 – ADNOC Drilling completed the acquisition of an additional stake in Gordon Technologies to expand advanced drilling technology capabilities, strengthening integrated drilling services and accelerating deployment of intelligent drilling systems across offshore operations. Source: https://www.adnocdrilling.ae

July 2024 – Noble Corporation secured multiple offshore drilling awards in the Middle East, increasing contracted fleet utilization while extending long-term partnerships with regional operators. The awards support deployment of premium jack-up rigs across strategically important offshore developments. Source: https://www.noblecorp.com

The Offshore Oil and Gas Drilling Market Report provides a comprehensive assessment of global offshore exploration and production activities across shallow-water, deepwater, and ultra-deepwater environments. The study evaluates market performance by rig type, application, and end-user while covering operational trends across more than 20 offshore-producing countries in North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The report analyzes drilling technologies including jack-up rigs, semi-submersibles, drillships, automated drilling systems, digital well planning, subsea production infrastructure, predictive maintenance, and intelligent offshore asset management. More than 60% of newly sanctioned offshore developments now incorporate digital drilling technologies, reflecting the industry's transition toward highly automated offshore operations.

The report further examines competitive positioning, fleet modernization strategies, offshore licensing activity, supply-chain developments, capital investment priorities, and technology adoption influencing industry performance between 2026 and 2033. Strategic insights cover contractor capabilities, national oil company investments, floating production deployment, subsea engineering trends, offshore decarbonization initiatives, and digital transformation across offshore assets. The analysis supports drilling contractors, operators, investors, equipment manufacturers, engineering companies, and policymakers in identifying investment opportunities, benchmarking competitive performance, optimizing offshore development strategies, and preparing for the next phase of technologically advanced offshore energy production.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 43,492.4 Million |

|

Market Revenue in 2033 |

USD 69,320.3 Million |

|

CAGR (2026 - 2033) |

6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Transocean Ltd., Valaris Limited, Noble Corporation plc, Seadrill Limited, China Oilfield Services Limited (COSL), Borr Drilling Limited, Shelf Drilling Ltd., Saipem S.p.A., ADNOC Drilling Company PJSC, KCA Deutag, Nabors Industries Ltd., Stena Drilling Ltd., Diamond Offshore Drilling Inc., Japan Drilling Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |