Reports

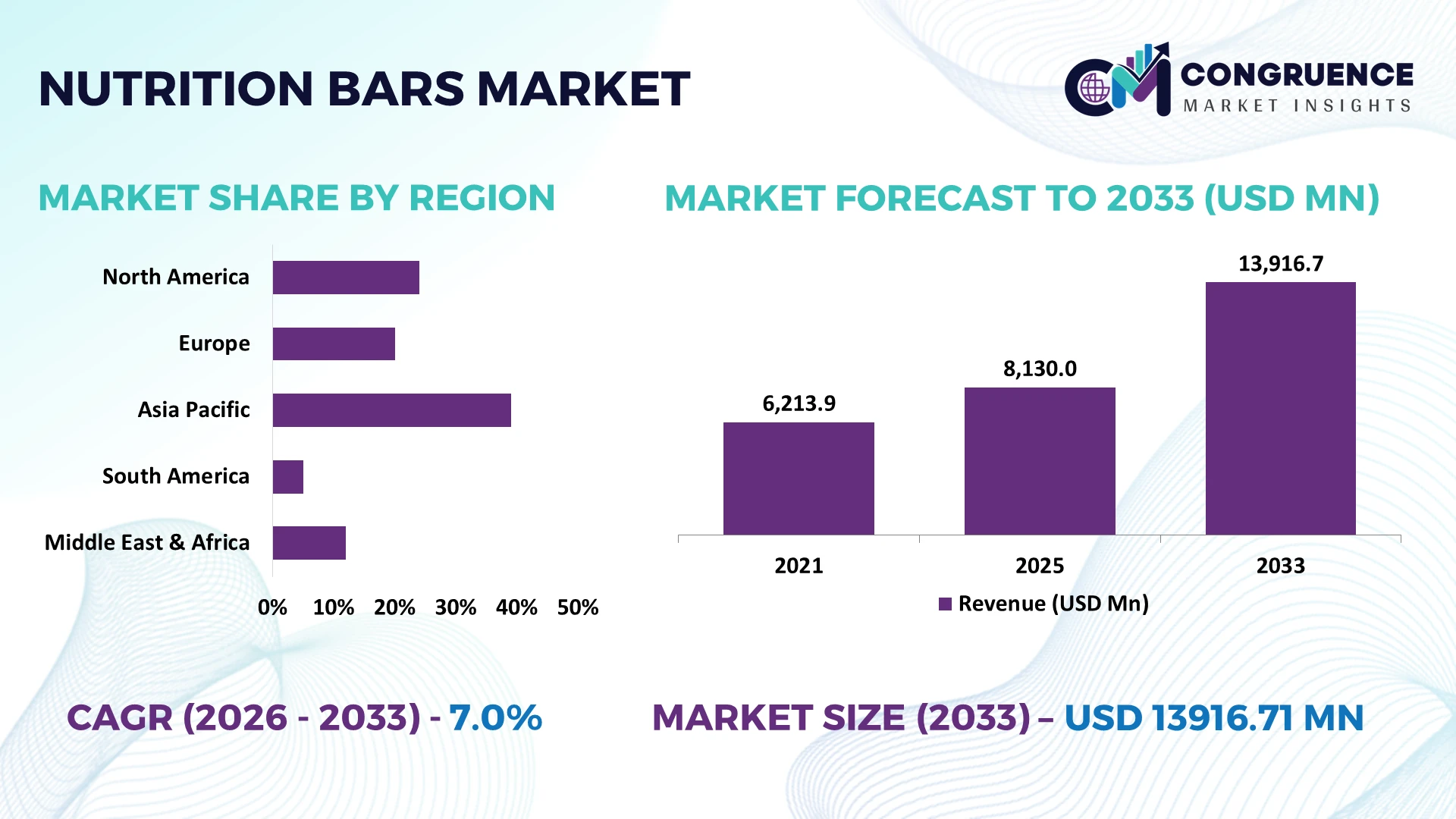

The Global Nutrition Bars Market was valued at USD 8130 Million in 2025 and is anticipated to reach a value of USD 13916.71 Million by 2033 expanding at a CAGR of 6.95% between 2026 and 2033. Increasing demand for protein-enriched snacks, clean-label formulations, functional ingredients, and convenient on-the-go nutrition continues to accelerate product innovation and premium portfolio expansion across global food and beverage manufacturers.

The United States dominates the global Nutrition Bars Market with approximately 34% market share, supported by advanced food manufacturing, high functional food adoption, and investments exceeding USD 1.2 billion in nutrition-focused product development and automated production facilities. Compared with Germany, where clean-label and plant-based nutrition bars are expanding rapidly, the U.S. maintains stronger retail penetration and manufacturing scale despite continued Red Sea shipping disruptions affecting ingredient logistics in 2026.

Strategic focus on premium formulations, diversified ingredient sourcing, and regional manufacturing expansion strengthens long-term competitiveness across the global Nutrition Bars Market.

Market Size & Growth: USD 8130 Million in 2025, projected to reach USD 13916.71 Million by 2033 at a CAGR of 6.95%, supported by functional ingredient innovation and premium nutrition product expansion.

Top Growth Drivers: Protein snack consumption increased 24%, clean-label product demand rose 21%, and sports nutrition purchases expanded 18% globally.

Short-Term Forecast: By 2028, automated production systems are expected to improve manufacturing efficiency by 15% while reducing production waste by 10%.

Emerging Technologies: AI-driven formulation, automated quality inspection, and precision ingredient blending shorten product development cycles by approximately 20%.

Regional Leaders: North America exceeds USD 4.8 billion, Europe reaches USD 3.7 billion, and Asia-Pacific surpasses USD 3.2 billion, driven by premium nutrition adoption and regional manufacturing expansion.

Consumer/End-User Trends: More than 42% of active consumers regularly choose nutrition bars as convenient meal replacements or post-workout snacks.

Pilot/Case Example: In 2026, automated packaging upgrades improved production throughput by 16% while reducing material waste by 11% in commercial nutrition bar manufacturing.

Competitive Landscape: The leading manufacturer holds approximately 14% global market share, with competition driven by General Mills, Mondelēz International, Mars Incorporated, Kellogg Company, and Nestlé.

Regulatory & ESG Impact: Sustainable packaging initiatives reduced plastic usage by approximately 18%, while stricter nutritional labeling standards strengthened product transparency across major markets.

Investment & Funding: More than USD 900 million in investments supported manufacturing expansion, strategic partnerships, and advanced functional ingredient development amid regional supply-chain diversification.

Innovation & Future Outlook: High-protein, plant-based, personalized nutrition, and microbiome-focused formulations are reshaping competitive strategies as manufacturers expand premium product portfolios.

The Nutrition Bars Market is witnessing strong demand across sports nutrition, meal replacement, clinical nutrition, and healthy snacking applications as manufacturers introduce high-protein, low-sugar, and plant-based formulations. AI-assisted product development and precision ingredient optimization are accelerating innovation, while clean-label products account for over 40% of new launches. Regional ingredient sourcing and resilient supply-chain strategies continue strengthening operational efficiency, setting the stage for the strategic market discussion.

The Nutrition Bars Market has become strategically important as food manufacturers compete through functional nutrition, premium ingredients, and diversified product portfolios rather than conventional snack offerings. Rising consumer preference for protein-rich, low-sugar, and clean-label products is reshaping investment priorities, while supply-chain restructuring following continued global logistics disruptions is encouraging localized ingredient sourcing and manufacturing resilience. Companies are increasingly integrating digital quality management and automated production to improve consistency and accelerate product commercialization.

AI-enabled formulation platforms reduce new product development time by nearly 20% compared with traditional trial-and-error methods, while automated packaging lines improve throughput by approximately 15% and minimize material waste. The United States continues to lead in large-scale commercial production and product innovation, whereas Japan is advancing high-value functional formulations supported by precision nutrition research and aging-population demand. During the next two to three years, automated production is expected to expand across more than 35% of newly upgraded manufacturing facilities.

Manufacturers are deploying robotic packaging systems and digital traceability platforms to strengthen product quality and inventory visibility while expanding partnerships with ingredient suppliers for stable protein and fiber sourcing. Companies are prioritizing localized production, premium formulations, and innovation-focused collaborations, reinforcing competitive positioning through operational efficiency, faster product launches, and stronger resilience against future supply disruptions.

Growing consumer preference for functional nutrition continues to reshape the Nutrition Bars Market as demand shifts toward high-protein, fiber-rich, and clean-label formulations. More than 42% of health-conscious consumers actively purchase functional snack products, while protein-enriched launches increased by approximately 24% across major food manufacturers. The United States has accelerated investments in advanced food processing and automated production following supply-chain restructuring that encouraged regional ingredient sourcing. Manufacturers are expanding production capacity, partnering with plant-protein suppliers, and introducing clinically supported formulations. This transition strengthens brand differentiation, improves manufacturing flexibility, and enables companies to capture premium retail positioning while responding more efficiently to evolving nutritional preferences.

Price fluctuations in protein isolates, nuts, cocoa, and specialty grains continue to pressure manufacturing economics across the Nutrition Bars Market. Raw material procurement costs have fluctuated by nearly 18%, while transportation and packaging expenses remain around 12% above pre-disruption levels in several global trade corridors. Dependence on imported functional ingredients exposes manufacturers to logistics delays and procurement uncertainty, particularly following continued Red Sea shipping disruptions. Companies are reducing operational risk through multi-country sourcing strategies, localized procurement contracts, and reformulation using alternative protein ingredients. These measures improve supply continuity but require additional validation, procurement coordination, and manufacturing adjustments before achieving full-scale operational efficiency.

Personalized nutrition is creating high-value opportunities as consumers seek products aligned with fitness, wellness, and preventive healthcare objectives. AI-assisted formulation platforms reduce development cycles by approximately 20%, while demand for plant-based functional snacks has expanded by more than 22% in premium retail channels. Japan and South Korea are accelerating investments in precision nutrition supported by digital health ecosystems and advanced food science research. Manufacturers are expanding R&D partnerships, integrating data-driven product design, and introducing microbiome-supporting and customized nutrition bar portfolios. These initiatives strengthen product differentiation, improve premium pricing potential, and unlock underserved consumer segments beyond traditional sports nutrition markets.

Commercializing advanced nutrition bar formulations at global scale remains challenging due to manufacturing complexity, formulation consistency, and regulatory compliance across multiple markets. Approximately 30% of new functional ingredients require extended validation before commercial deployment, while automated production upgrades increase initial capital requirements by nearly 25%. The United States and Canada continue strengthening food labeling and ingredient transparency requirements, increasing operational complexity for multinational manufacturers. Companies must invest in digital quality systems, workforce training, supplier integration, and flexible manufacturing infrastructure to maintain consistent product quality. Successfully balancing innovation speed with regulatory compliance and scalable production will determine long-term competitive advantage in the Nutrition Bars Market.

AI-Enabled Product Development: Manufacturers are integrating AI-assisted formulation platforms to reduce product development cycles by approximately 20% while improving ingredient optimization by nearly 15%. Stricter nutrition labeling requirements are accelerating digital formulation workflows, enabling faster regulatory compliance and quicker product commercialization. Companies are expanding technology partnerships and modernizing R&D processes to improve innovation speed and strengthen premium product differentiation.

Localized Ingredient Supply Networks: Ongoing supply-chain restructuring has encouraged manufacturers to diversify procurement and regionalize ingredient sourcing. More than 32% of leading nutrition bar producers have expanded multi-country supplier networks, reducing procurement lead times by around 18%. U.S. manufacturers are increasing domestic protein sourcing through long-term supplier agreements, improving production continuity, inventory stability, and resilience against logistics disruptions.

Premium Functional Formulations: High-protein, low-sugar, gut-health, and plant-based nutrition bars now account for over 40% of premium product launches, while plant-based ingredient adoption has increased by approximately 22%. Consumer demand for multifunctional nutrition continues reshaping product portfolios. Companies are scaling premium manufacturing, expanding biotechnology collaborations, and introducing specialized formulations targeting active lifestyles and preventive health.

Smart Factory Modernization: Automated packaging, robotic material handling, and digital quality inspection systems have improved manufacturing throughput by approximately 16% while reducing packaging defects by nearly 12%. Labor shortages across advanced food manufacturing markets continue accelerating factory automation. Companies are investing in predictive maintenance, connected production systems, and digital quality management to improve operational efficiency, product consistency, and long-term manufacturing competitiveness.

Protein Bars account for approximately 38% of the Nutrition Bars Market, maintaining leadership through strong consumer preference for high-protein functional snacks, scalable manufacturing, and broad retail availability. Energy Bars continue serving endurance and outdoor nutrition needs, while Cereal Bars retain stable demand through affordable pricing and mass-market distribution. Fiber Bars strengthen their market position by supporting digestive wellness and clean-label product strategies.

Meal Replacement Bars are the fastest-growing segment as demand rises for nutritionally balanced, convenient food solutions among busy professionals and health-conscious consumers. Premium formulations featuring complete proteins, vitamins, and reduced sugar have increased by approximately 26%, while functional ingredient integration has expanded by nearly 19% across new launches. Companies are increasing production capacity, strengthening ingredient partnerships, and prioritizing premium product innovation to improve portfolio competitiveness and long-term market positioning.

Healthy Snacking represents approximately 41% of application demand, supported by increasing consumption of convenient, nutrient-rich snacks across supermarkets, convenience stores, and digital retail channels. Sports Nutrition continues benefiting from expanding fitness participation, while Weight Management supports demand for portion-controlled and reduced-sugar products. Clinical Nutrition maintains strategic relevance through specialized dietary support across healthcare settings.

Meal Replacement is the fastest-growing application as consumers increasingly substitute conventional meals with balanced nutrition bars during work, travel, and active lifestyles. Adoption has increased by approximately 24%, while high-protein meal replacement products account for nearly 45% of newly introduced premium formulations. Companies are expanding automated manufacturing, collaborating with nutrition experts, and optimizing product portfolios to improve nutritional quality and strengthen consumer engagement.

Retail Consumers hold approximately 64% of total end-user demand, supported by extensive supermarket availability, expanding e-commerce penetration, and increasing daily consumption of functional nutrition products. Foodservice maintains consistent institutional demand, Hospitals continue utilizing specialized nutrition bars within dietary programs, and Sports Academies are expanding structured nutrition strategies to improve athlete performance and recovery.

Fitness Centers are the fastest-growing end-user segment as nutrition products become increasingly integrated into wellness memberships and professional fitness programs. Adoption across commercial fitness facilities has increased by approximately 21%, while branded retail partnerships have expanded by nearly 18%. Companies are introducing exclusive gym-focused product portfolios, strengthening partnerships with fitness chains, and expanding direct distribution networks to improve recurring commercial sales.

North America accounted for the largest market share at 37% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2026 and 2033.

Advanced Manufacturing and Premium Nutrition Leadership

North America remains the largest regional market due to its mature functional food industry, extensive retail infrastructure, and strong adoption of protein-rich convenience foods. The region contributes approximately 37% of global demand, supported by advanced manufacturing facilities, digital quality management, and large-scale contract production. More than 70% of premium nutrition bar launches incorporate clean-label or high-protein formulations, reflecting evolving consumer preferences. Automated production systems have improved manufacturing efficiency by nearly 15%, enabling companies to accelerate product launches while maintaining quality consistency. Leading manufacturers continue expanding domestic production capacity, strengthening supplier partnerships, and investing in localized ingredient sourcing to improve operational resilience against supply-chain disruptions.

United States Market Outlook: The United States leads regional consumption through advanced food processing infrastructure, extensive supermarket distribution, and a highly developed sports nutrition ecosystem. More than 75% of premium nutrition bar sales are concentrated within organized retail and digital commerce channels. Companies continue investing in automated manufacturing, product innovation, and long-term protein ingredient agreements, strengthening production flexibility and improving response to changing consumer demand.

Clean-Label Innovation and Sustainable Manufacturing

Europe maintains a strong market position through premium product innovation, strict nutritional standards, and increasing consumer preference for functional snacks. Approximately 28% of global nutrition bar demand originates from the region, supported by established food manufacturers and advanced processing technologies. Sustainable packaging adoption has expanded by nearly 20%, while manufacturers continue reformulating products with natural sweeteners and plant-based ingredients. Investments in efficient production technologies and recyclable packaging are strengthening operational competitiveness. Companies are also increasing collaboration with regional ingredient suppliers to improve sourcing stability and regulatory compliance.

Germany Market Outlook: Germany serves as the regional manufacturing and innovation hub due to its advanced food processing capabilities and strong emphasis on functional nutrition. Plant-based nutrition bar launches have increased by approximately 24%, supported by growing investments in clean-label product development. Manufacturers continue modernizing production facilities and expanding premium product portfolios to strengthen export competitiveness across European markets.

Manufacturing Scale and Consumer Expansion

Asia-Pacific is becoming the fastest-expanding regional market as urbanization, rising disposable incomes, and increasing health awareness accelerate nutrition bar adoption. The region contributes approximately 24% of global demand while accounting for one of the fastest-growing manufacturing bases for functional foods. Production capacity has expanded by nearly 18% through investments in automated food processing and regional manufacturing facilities. Expanding e-commerce platforms and organized retail networks are improving product accessibility across major consumer markets. Companies continue strengthening regional partnerships and localized production strategies to support increasing demand while improving supply-chain responsiveness.

China Market Outlook: China remains the region's largest production and consumption market due to its extensive food manufacturing infrastructure and rapidly expanding health and wellness sector. Digital retail channels account for more than 35% of premium nutrition bar purchases, supporting faster market penetration. Manufacturers are expanding smart production facilities, strengthening domestic ingredient sourcing, and investing in premium functional formulations to improve competitiveness across both domestic and export markets.

Health-Conscious Consumption Drives Expansion

South America continues strengthening its position as health awareness and modern retail infrastructure expand across major economies. The region accounts for approximately 7% of global demand, supported by growing consumer interest in convenient functional foods and protein-enriched snacks. Retail distribution has expanded by nearly 14% through supermarket modernization and digital commerce growth. However, raw material price fluctuations and logistics limitations continue affecting manufacturing efficiency. Companies are responding by expanding local production, strengthening regional distribution partnerships, and introducing competitively priced product portfolios tailored to domestic purchasing patterns.

Brazil Market Outlook: Brazil represents the largest market within South America due to its well-established food manufacturing industry and expanding sports nutrition sector. Functional snack consumption has increased by approximately 19% across urban consumers, encouraging manufacturers to invest in localized production and premium product innovation. Strategic partnerships with national retail chains continue improving product availability and strengthening long-term market penetration.

Retail Modernization and Investment Momentum

The Middle East & Africa market is expanding through retail modernization, growing health awareness, and increasing investment in food manufacturing infrastructure. The region contributes approximately 4% of global demand while premium nutrition products continue gaining visibility across organized retail channels. Modern food processing investments have increased by nearly 16%, supporting improved domestic manufacturing capabilities. International brands are expanding distribution partnerships while regional producers continue strengthening localized product development to improve market competitiveness and reduce import dependency.

United Arab Emirates Market Outlook: The United Arab Emirates remains the region's leading commercial hub due to advanced logistics infrastructure, premium retail networks, and a rapidly expanding wellness industry. More than 60% of premium nutrition products are distributed through organized retail and specialty health stores. Companies continue investing in regional distribution centers, strategic import partnerships, and premium product launches, positioning the country as a key gateway for nutrition bar expansion across the Middle East.

Global brands including Mondelēz International (CLIF), Mars (KIND), General Mills, Kellanova (RXBAR), and Simply Good Foods (Quest) compete directly with premium functional nutrition specialists and regional clean-label manufacturers. The top five players collectively control approximately 48% of the market, creating a moderately consolidated competitive structure. Competition is driven by formulation innovation, ingredient transparency, manufacturing efficiency, and distribution reach rather than price alone. Automated production improves manufacturing efficiency by nearly 15%, while AI-assisted product development reduces formulation cycles by approximately 20%. Premium functional products command price premiums of around 18% over conventional snack bars, reinforcing brand differentiation. Companies are expanding manufacturing capacity, securing long-term protein ingredient contracts, pursuing strategic partnerships, and vertically integrating selected supply chains to strengthen resilience. Competitive momentum is shifting toward personalized nutrition, clean-label formulations, and localized sourcing as supply control becomes increasingly important. High regulatory compliance requirements, premium ingredient sourcing, and established retail relationships remain significant entry barriers. Winning requires continuous innovation, resilient supply networks, rapid commercialization, and premium brand credibility.

General Mills, Inc.

Mondelēz International, Inc.

Mars, Incorporated

Kellanova

The Simply Good Foods Company

Post Holdings, Inc.

PepsiCo, Inc.

Nestlé S.A.

Hormel Foods Corporation

Glanbia plc

Otsuka Pharmaceutical Co., Ltd.

Lotus Bakeries NV

Manufacturers are increasingly deploying AI-assisted formulation, digital quality management, and automated ingredient dosing to improve production precision and accelerate product development. AI-based formulation platforms reduce development time by approximately 20%, while automated batching improves ingredient consistency by nearly 15%. Around 45% of large-scale manufacturers have adopted digital production monitoring, enabling faster product validation and reducing formulation variability. These technologies improve operational efficiency while supporting premium clean-label and functional product development.

Emerging technologies include machine vision quality inspection, robotic packaging, and predictive maintenance integrated through Industrial IoT platforms. Compared with conventional manual inspection, AI-enabled vision systems reduce packaging defects by approximately 18% while increasing inspection speed by nearly 25%. Large multinational manufacturers benefit most because integrated production systems improve throughput, inventory visibility, and regulatory compliance across multiple manufacturing locations. Companies are expanding smart factories to strengthen production flexibility and reduce operational disruptions.

Between 2026 and 2028, precision nutrition technologies, digital twin manufacturing, and advanced ingredient traceability are expected to reshape competitive performance. More than 35% of premium production facilities are projected to deploy connected manufacturing platforms supporting real-time process optimization. Companies investing early in intelligent manufacturing, sustainable processing, and data-driven product innovation will strengthen operational resilience, accelerate commercialization, and maintain competitive leadership through superior manufacturing agility and product quality.

January 2025 – CLIF BAR (Mondelēz International) launched its "Raise Your Bar" platform alongside a new Cookies & Creme energy bar containing 11g of plant protein, strengthening consumer engagement and reinforcing premium product differentiation across the performance nutrition segment.

May 2025 – CLIF BUILDERS introduced three new high-protein bar innovations, including OREO-flavored and Reduced Sugar Crispy variants, expanding its performance nutrition portfolio and addressing rising demand for lower-sugar functional products through broader product diversification.

December 2025 – RXBAR expanded beyond traditional nutrition bars with Protein Energy Bites packaged in two portioned servings per pouch, broadening its snacking portfolio and strengthening its position in convenient, high-protein, on-the-go nutrition. Source: Kellanova News

March 2026 – CLIF introduced Energy Bites and a limited-edition Chocolate Berry Energy Bar, expanding its energy portfolio with bite-sized formats designed for running, hiking, and endurance activities, strengthening innovation-led product diversification across active lifestyle consumers. Source: Mondelēz International

The report delivers comprehensive analysis across Protein Bars, Energy Bars, Meal Replacement Bars, Cereal Bars, and Fiber Bars while evaluating demand across Sports Nutrition, Weight Management, Meal Replacement, Healthy Snacking, and Clinical Nutrition applications. It further assesses Retail Consumers, Fitness Centers, Hospitals, Sports Academies, and Foodservice as primary end-user segments. The study covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, representing more than 95% of global market activity and highlighting regional manufacturing, distribution, and consumption dynamics.

The report also evaluates emerging technologies including AI-assisted formulation, automated manufacturing, smart quality inspection, digital traceability, and sustainable packaging solutions. Strategic assessment includes competitive positioning, product innovation, supply-chain optimization, regional expansion, partnership activity, and investment priorities between 2026 and 2033. With analysis spanning more than 10 leading companies and multiple functional nutrition categories, the report supports business expansion, product portfolio optimization, market entry evaluation, and long-term competitive decision-making.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 8130 Million |

Market Revenue in 2033 | USD 13916.71 Million |

CAGR (2026 - 2033) | 6.95% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | General Mills, Inc., Mondelēz International, Inc., Mars, Incorporated, Kellanova, The Simply Good Foods Company, Post Holdings, Inc., PepsiCo, Inc., Nestlé S.A., Hormel Foods Corporation, Glanbia plc, Otsuka Pharmaceutical Co., Ltd., Lotus Bakeries NV |

Customization & Pricing | Available on Request (10% Customization is Free) |