Reports

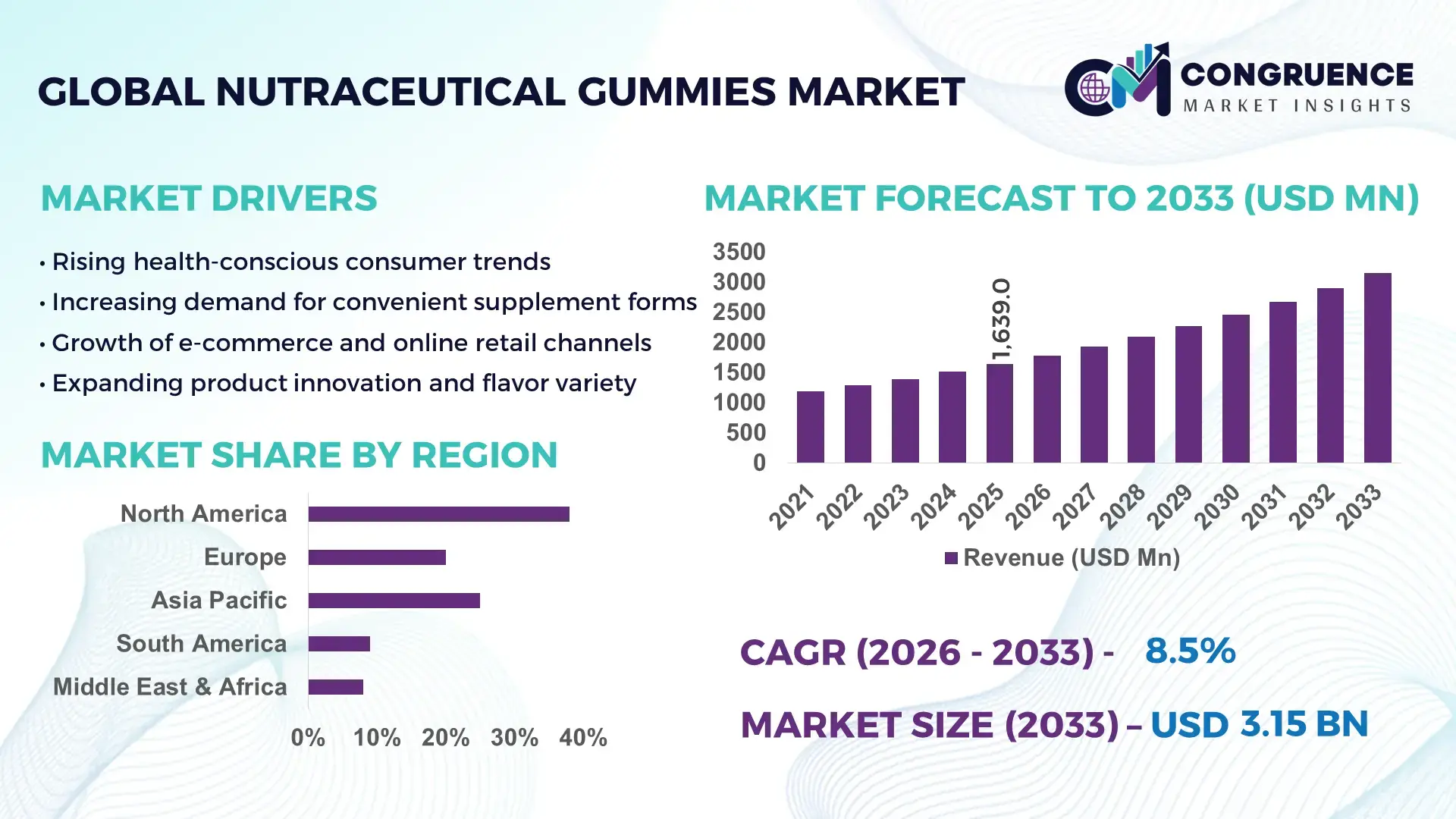

The Global Nutraceutical Gummies Market was valued at USD 1639 Million in 2025 and is anticipated to reach a value of USD 3147.87 Million by 2033 expanding at a CAGR of 8.5% between 2026 and 2033. Rising consumer preference for convenient, palatable, and functional dietary supplements is accelerating demand across developed and emerging economies.

The United States continues to lead the global nutraceutical gummies market with advanced manufacturing infrastructure and strong private-label production capacity exceeding 120,000 metric tons annually. More than 35% of dietary supplement launches in the country now include gummy formulations, reflecting widespread consumer adoption across adult and pediatric segments. Investment in automated pectin-based production lines and sugar-free formulation technologies has increased by over 18% in the last three years. Functional applications such as immunity support, beauty-from-within supplements, and sleep enhancement collectively account for over 60% of gummy-based nutraceutical consumption. High retail penetration across pharmacies, e-commerce platforms, and mass merchandisers further strengthens domestic production scalability and innovation intensity.

Market Size & Growth: Valued at USD 1639 Million in 2025, projected to reach USD 3147.87 Million by 2033 at a CAGR of 8.5%, driven by growing demand for convenient functional supplements and clean-label formulations.

Top Growth Drivers: Adult supplement adoption rate above 62%, sugar-free gummy preference growth of 28%, and immunity-focused product demand increase of 34%.

Short-Term Forecast: By 2028, advanced manufacturing automation is expected to improve production efficiency by 15% and reduce per-unit formulation costs by 10%.

Emerging Technologies: Plant-based pectin stabilization, microencapsulation for enhanced nutrient bioavailability, and AI-driven flavor optimization platforms are transforming premium nutraceutical gummy development.

Regional Leaders: North America projected to reach USD 1.2 Billion by 2033 with strong OTC penetration; Europe expected at USD 860 Million supported by clean-label demand; Asia-Pacific forecast at USD 740 Million driven by urban health awareness.

Consumer/End-User Trends: Adults account for over 55% of consumption, followed by pediatric nutrition at 30%, with rising demand for vegan, non-GMO, and low-sugar functional gummies.

Pilot or Case Example: In 2024, a U.S.-based supplement manufacturer implemented automated starchless molding, improving batch output by 18% and reducing material waste by 12%.

Competitive Landscape: The market leader holds approximately 14% share, followed by major players including Church & Dwight, Bayer, Amway, Haleon, and Nestlé Health Science.

Regulatory & ESG Impact: Increasing compliance with dietary supplement labeling standards and sustainable sourcing mandates has accelerated adoption of biodegradable packaging and sugar-reduction initiatives.

Investment & Funding Patterns: Over USD 450 Million in recent investments directed toward capacity expansion, vegan gummy lines, and bioavailability-enhancing technologies.

Innovation & Future Outlook: Growth is supported by personalized nutrition platforms, functional botanical infusions, and hybrid nutraceutical-cosmeceutical gummy formats targeting preventive healthcare markets.

The nutraceutical gummies market serves key sectors including dietary supplements (approximately 65% contribution), functional foods (20%), and pediatric health formulations (15%). Recent innovation trends include collagen-infused beauty gummies, probiotic-stable formulations with enhanced shelf life, and sugar-alternative sweetening systems reducing caloric content by up to 40%. Regulatory emphasis on accurate labeling and ingredient transparency is shaping product reformulation strategies, while sustainability goals are driving plant-based gelatin substitutes and eco-friendly packaging adoption. Regionally, North America and Europe demonstrate high per capita consumption, whereas Asia-Pacific shows accelerated growth due to expanding middle-class health awareness and digital retail penetration. The future outlook indicates steady expansion supported by personalized nutrition, preventive healthcare spending, and advanced nutrient delivery technologies.

The Nutraceutical Gummies Market holds strategic relevance within the broader functional nutrition and preventive healthcare ecosystem, driven by its alignment with consumer-centric product design, advanced nutrient delivery systems, and scalable manufacturing capabilities. As more than 70% of global supplement consumers prioritize convenience and taste, gummy formulations are increasingly positioned as high-retention delivery formats for vitamins, minerals, botanicals, collagen, and probiotics. Strategic expansion plans are focused on automation, clean-label innovation, and region-specific product customization to capture diversified demographic segments.

Technological benchmarking indicates that microencapsulation-based nutrient stabilization delivers 25% improvement in bioavailability compared to conventional compression tablet standards. Starchless molding technology further enhances production precision and reduces material waste by approximately 15% compared to traditional starch-based systems. North America dominates in volume due to established supplement consumption patterns, while Asia-Pacific leads in adoption with nearly 48% of urban health-conscious consumers actively purchasing gummy-based dietary supplements through digital channels.

By 2028, AI-enabled demand forecasting and smart production analytics are expected to improve inventory turnover efficiency by 18% while cutting supply chain lead times by 12%. Firms are committing to ESG-driven transformation metrics such as 30% reduction in single-use plastic packaging and 20% increase in plant-based ingredient sourcing by 2030. In 2024, a U.S.-based nutraceutical manufacturer achieved a 16% improvement in batch consistency through AI-powered quality monitoring systems integrated into automated production lines. With expanding regulatory oversight, sustainable ingredient innovation, and personalized nutrition platforms, the Nutraceutical Gummies Market is increasingly positioned as a pillar of resilience, compliance, and sustainable growth within the global health and wellness industry.

Growing demand for convenient, palatable dietary supplements is significantly driving the Nutraceutical Gummies Market. Surveys indicate that over 60% of supplement users prefer gummy formats over capsules due to improved taste and ease of consumption. Adult-focused formulations now account for more than half of total gummy supplement purchases, reflecting broader lifestyle-driven health management trends. Immunity, hair and skin health, and sleep support remain leading functional categories, collectively representing over 55% of product demand. Retail expansion across pharmacies, supermarkets, and online marketplaces has improved product accessibility, while sugar-reduction technologies enabling up to 35% lower caloric content have broadened appeal among health-conscious consumers. These combined factors are accelerating product innovation cycles and strengthening repeat purchase behavior across multiple demographics.

Regulatory complexities and nutritional scrutiny present measurable restraints for the Nutraceutical Gummies Market. Authorities across major economies are tightening labeling requirements, mandating precise nutrient disclosure and limiting unverified health claims. Compliance costs have increased by approximately 12% for mid-sized manufacturers due to enhanced documentation and testing requirements. Additionally, sugar content concerns pose formulation challenges, as traditional gummy products may contain 2–4 grams of sugar per serving. Public health campaigns targeting sugar reduction have influenced consumer perception, prompting reformulation investments. Stability issues related to heat-sensitive active ingredients further complicate manufacturing processes, often requiring specialized encapsulation technologies. These regulatory and formulation constraints can extend product development timelines and increase operational expenditure for manufacturers.

Personalized nutrition and plant-based formulation trends offer significant expansion opportunities for the Nutraceutical Gummies Market. Digital health platforms enabling customized vitamin blends are gaining traction, with nearly 45% of online supplement buyers expressing interest in tailored formulations. Vegan and gelatin-free gummies have witnessed adoption growth exceeding 30% in urban markets, driven by ethical and dietary preferences. Advances in probiotic stabilization technologies now extend shelf life by up to 20%, enabling broader distribution across temperature-variable regions. Functional ingredient diversification, including adaptogens and collagen peptides, is expanding category penetration into beauty and stress-management segments. These emerging product innovations create scalable entry points for premium positioning and value-added differentiation within competitive global markets.

Volatility in raw material pricing and supply chain disruptions present ongoing challenges for the Nutraceutical Gummies Market. Prices of key inputs such as pectin, gelatin substitutes, and certain botanical extracts have fluctuated by 15–25% over recent years due to agricultural variability and global trade constraints. Transportation and logistics expenses have also increased, impacting international ingredient sourcing strategies. Maintaining nutrient stability in high-humidity and high-temperature environments requires controlled storage systems, raising warehousing costs. Furthermore, competitive pricing pressure from private-label brands intensifies margin constraints for established manufacturers. These operational and cost-related barriers require strategic sourcing diversification, automation investment, and long-term supplier agreements to maintain product quality and profitability.

• Sugar-Free and Low-Calorie Formulations Expanding Beyond 40% of New Product Launches: Health-conscious consumers are driving reformulation strategies, with more than 42% of newly introduced nutraceutical gummies featuring reduced-sugar or sugar-free claims. Advanced sweetening systems using stevia and monk fruit extracts have enabled up to 35% calorie reduction per serving. Manufacturers report a 20% increase in repeat purchase rates for low-sugar variants compared to traditional gelatin-based gummies, particularly in adult wellness categories. This shift is influencing procurement strategies for alternative sweeteners and plant-based gelling agents across North America and Europe.

• Plant-Based and Vegan Gummies Surpassing 30% Category Penetration in Urban Markets: Vegan nutraceutical gummies now account for over 30% of total gummy supplement offerings in metropolitan retail channels. Pectin-based formulations have replaced gelatin in nearly 48% of newly commissioned production lines. Consumer preference surveys indicate that 52% of millennial buyers actively seek plant-based supplement options. This measurable shift has led to a 25% increase in investment toward non-animal-derived raw materials, supporting ESG alignment and expanding export opportunities in regions with strict dietary compliance standards.

• Functional Diversification Driving 50% Growth in Beauty and Cognitive Segments: Beauty-from-within and cognitive health gummies collectively represent more than 50% of innovation pipelines in 2025. Collagen-infused gummies demonstrate absorption enhancement of approximately 22% through microencapsulation technologies. Probiotic gummy stability improvements have extended shelf life by 18% in controlled packaging environments. Retail shelf allocation for specialty functional gummies has expanded by 15% year-over-year, reflecting strong consumer demand for targeted health outcomes beyond basic multivitamin supplementation.

• Automation and Smart Manufacturing Improving Production Efficiency by 18%: Deployment of AI-enabled quality monitoring and starchless molding technologies has improved batch consistency by 16% while reducing material waste by 12%. Fully automated lines now handle nearly 60% of high-volume nutraceutical gummy production in advanced manufacturing facilities. Real-time data analytics integration has shortened production cycle times by 14%, enhancing scalability and inventory optimization. These measurable operational improvements are strengthening supply chain resilience and enabling faster response to evolving consumer demand patterns.

The Nutraceutical Gummies Market is strategically segmented by type, application, and end-user, reflecting diversified consumer health priorities and evolving delivery technologies. By type, vitamin-based gummies dominate overall consumption due to established preventive healthcare usage patterns, while botanical and specialty formulations are gaining traction in premium segments. Application-wise, general wellness and immunity remain the largest categories, supported by sustained demand across adult populations. However, beauty, cognitive, and digestive health applications are rapidly expanding as targeted supplementation becomes mainstream. From an end-user perspective, adults account for the majority of product uptake, followed by pediatric and geriatric users seeking convenient dosage formats. Digital retail penetration exceeding 35% of supplement purchases is influencing segmentation dynamics, enabling personalized offerings and subscription-based distribution models. This segmentation structure enables manufacturers to refine portfolio positioning, optimize supply chains, and align product innovation with measurable demographic demand patterns.

Vitamin-based nutraceutical gummies represent the leading product type, accounting for approximately 46% of total category consumption due to strong demand for multivitamins, vitamin C, vitamin D, and B-complex formulations. Their dominance is reinforced by preventive healthcare adoption, with over 60% of adult supplement users regularly consuming vitamin-based products. Mineral-enriched gummies hold nearly 18% share, primarily driven by calcium, magnesium, and zinc fortification. Botanical and herbal gummies, including elderberry and ashwagandha variants, account for about 21% of the market, supported by a 9.8% CAGR as consumers shift toward plant-derived wellness solutions. Probiotic and specialty formulations collectively contribute the remaining 15%, focusing on digestive health and targeted therapeutic benefits.

While vitamin-based gummies currently account for 46% of adoption and mineral formats hold 18%, botanical and herbal variants are rising fastest and are expected to exceed 25% category penetration by 2033 due to clean-label positioning and immune-support demand.

General wellness and immunity applications lead the Nutraceutical Gummies Market, accounting for approximately 52% of total product utilization. Immunity-support gummies featuring vitamin C, zinc, and elderberry remain top-selling SKUs, reflecting heightened preventive health awareness. Digestive health applications represent around 19% of adoption, supported by increased probiotic incorporation and gut-health campaigns. Beauty and skin health gummies hold nearly 17% share, driven by collagen and biotin fortification trends. Cognitive and sleep-support applications collectively contribute about 12%, targeting stress management and mental performance.

While general wellness applications currently account for 52% of adoption and digestive health holds 19%, beauty-focused gummies are expanding fastest, registering a 10.6% CAGR due to rising demand for ingestible cosmetic supplements among consumers aged 25–45.

Adults represent the leading end-user segment, contributing approximately 57% of total Nutraceutical Gummies Market demand. High adoption is linked to preventive health routines, with more than 65% of supplement users aged 25–55 preferring chewable formats over tablets. Pediatric users account for roughly 28% of market volume, supported by parental preference for flavored, easy-to-administer vitamin products. Geriatric consumers represent about 10%, benefiting from improved swallowability and taste masking. Specialty user groups, including athletes and wellness-focused professionals, contribute the remaining 5% through performance-enhancing and stress-support formulations.

While adult consumers account for 57% of usage and pediatric segments hold 28%, the geriatric segment is growing fastest with an 8.9% CAGR, driven by aging populations and increased vitamin D and calcium supplementation.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.7% between 2026 and 2033.

North America’s dominance is supported by high dietary supplement penetration, with over 75% of adults consuming vitamins or nutraceutical products annually. Europe follows with approximately 27% market share, driven by stringent labeling compliance and clean-label adoption exceeding 45% of new product launches. Asia-Pacific currently holds nearly 24% share, fueled by urbanization rates above 55% and rising middle-class health expenditure. South America contributes about 6%, while the Middle East & Africa collectively account for nearly 5%, supported by expanding pharmacy retail networks and cross-border e-commerce growth of more than 20% annually. Regional manufacturing hubs in the United States, Germany, China, and India collectively produce over 65% of global nutraceutical gummy volumes, reflecting concentrated production capacity and technology integration.

North America holds approximately 38% share of the global Nutraceutical Gummies Market, supported by mature dietary supplement infrastructure and strong retail distribution networks. The United States accounts for nearly 82% of regional demand, with over 70% of households purchasing functional supplements annually. Key industries driving demand include preventive healthcare, beauty and wellness, and sports nutrition. Regulatory oversight under structured dietary supplement labeling frameworks has enhanced consumer confidence and accelerated compliance investments, with nearly 60% of manufacturers adopting third-party quality certifications. Technological advancements such as AI-based production monitoring and automated starchless molding lines have improved batch efficiency by 15%. A leading regional player, Church & Dwight, continues expanding gummy vitamin portfolios with sugar-free variants, strengthening retail penetration across pharmacy and mass-market chains. Consumer behavior shows higher adoption among working professionals and health-focused millennials, with digital subscription models contributing to over 30% of repeat purchases.

Europe accounts for approximately 27% of the Nutraceutical Gummies Market, with Germany, the United Kingdom, and France collectively representing over 65% of regional consumption. Strict food safety and supplement labeling regulations have driven demand for traceable ingredients and non-GMO formulations, with nearly 48% of new product launches emphasizing plant-based claims. Sustainability initiatives under regional environmental frameworks have prompted over 35% of manufacturers to shift toward recyclable packaging materials. Advanced pectin-based production technologies now represent nearly 50% of manufacturing upgrades within the region. Bayer, headquartered in Germany, has expanded its gummy supplement portfolio targeting immunity and pediatric health segments. Consumer behavior trends indicate strong preference for sugar-reduced and vegan-certified options, with more than 40% of buyers actively reviewing ingredient transparency before purchase.

Asia-Pacific represents nearly 24% of the global Nutraceutical Gummies Market and ranks as the fastest-growing regional cluster. China, India, and Japan collectively account for over 70% of regional consumption volume. Rapid urbanization exceeding 55% and expanding middle-class populations are driving preventive healthcare spending. Manufacturing infrastructure investments have increased by more than 20% in key hubs across China and India, strengthening local production capabilities. E-commerce platforms contribute over 45% of supplement sales in metropolitan areas, reflecting digital-first purchasing behavior. Nestlé Health Science has expanded gummy-based functional nutrition lines in Japan and Southeast Asia, targeting beauty and gut health segments. Consumer trends show higher demand among younger demographics, with nearly 50% of urban buyers aged 20–40 preferring chewable supplement formats over capsules.

South America contributes approximately 6% of the global Nutraceutical Gummies Market, with Brazil and Argentina accounting for over 70% of regional consumption. Expanding pharmacy chains and supermarket retail infrastructure have increased product accessibility by nearly 18% in urban centers. Government trade policies supporting nutritional product imports have reduced tariff barriers on key raw materials, facilitating diversified product portfolios. Local manufacturing investments have risen by approximately 12% to reduce dependence on imports. Regional players are introducing vitamin C and collagen gummies tailored to local dietary preferences. Consumer behavior indicates rising awareness of immune-support supplements, with over 45% of surveyed buyers prioritizing affordable, family-oriented wellness products.

The Middle East & Africa account for nearly 5% of the Nutraceutical Gummies Market, with the United Arab Emirates and South Africa representing more than 60% of regional sales. Rising lifestyle-related health concerns have increased supplement consumption by approximately 14% in urban populations. Modern retail expansion, including pharmacy chains and health specialty stores, has grown by nearly 20% over the past three years. Trade partnerships facilitating ingredient imports have enhanced product diversity. Technological modernization in packaging and climate-controlled storage supports product stability in high-temperature environments. Consumer preferences show strong demand for halal-certified and sugar-reduced formulations, particularly in Gulf countries, reflecting region-specific compliance and dietary considerations.

United States – 32% market share: Strong production capacity, high adult supplement adoption exceeding 70%, and advanced automated manufacturing infrastructure sustain leadership in the Nutraceutical Gummies Market.

Germany – 9% market share: Robust regulatory compliance framework, high clean-label demand, and established pharmaceutical-grade production facilities reinforce Germany’s leading position in the Nutraceutical Gummies Market.

The Nutraceutical Gummies Market is moderately fragmented, with more than 120 active manufacturers operating across global and regional levels. The top five companies collectively account for approximately 42% of total market share, indicating competitive concentration balanced by strong private-label and mid-sized brand participation. Leading players compete through diversified portfolios spanning multivitamin, probiotic, collagen, and botanical gummy formulations. Over 35% of new product launches in 2025 focused on sugar-free or plant-based innovations, intensifying differentiation strategies.

Strategic initiatives include capacity expansion, automated starchless molding investments, and cross-border distribution partnerships. Nearly 28% of established manufacturers have entered co-manufacturing agreements to optimize production efficiency and reduce lead times by up to 15%. Mergers and acquisitions activity increased by approximately 12% year-over-year, primarily targeting niche clean-label brands and personalized nutrition startups. Digital transformation is reshaping competition, with over 40% of premium brands adopting direct-to-consumer subscription models supported by AI-driven demand forecasting tools.

Innovation intensity remains high, as more than 30% of competitive spending is directed toward R&D for enhanced bioavailability technologies and microencapsulation systems delivering up to 25% improved nutrient stability. ESG compliance is emerging as a competitive differentiator, with 33% of leading companies committing to recyclable packaging targets exceeding 50% by 2030. This dynamic landscape underscores strategic positioning based on formulation innovation, supply chain resilience, regulatory compliance, and digital retail penetration.

Nestlé Health Science

Haleon plc

Nature’s Way Products, LLC

SmartyPants Vitamins

Olly Public Benefit Corporation

Pharmavite LLC

Hero Nutritionals

Garden of Life

The Nutraceutical Gummies Market is undergoing rapid technological evolution, driven by innovations that enhance production efficiency, product performance, and consumer relevance. Automation technologies such as AI-enabled quality monitoring systems and smart manufacturing lines have been adopted by over 60% of large-scale producers, improving batch consistency by up to 16% and reducing material waste by approximately 12%. Starchless molding systems have replaced traditional starch-based processes in nearly 45% of modern facilities, enabling more precise gummy shapes, uniform active distribution, and shorter cycle times. Robotics integration is also streamlining packaging operations, with automated pick-and-place systems handling up to 2,000 units per hour in high-volume plants.

Emerging nutrient delivery technologies are reshaping product differentiation. Microencapsulation techniques for vitamins, probiotics, and botanical extracts now enhance nutrient stability and bioavailability by as much as 25% compared to conventional gummy matrices. Recent advancements in pectin cross-linking chemistry have increased shelf life stability by roughly 18% in ambient storage conditions, supporting broader retail distribution without refrigeration. Plant-based gelling agents and novel polysaccharide blends are addressing consumer demand for vegan, non-GMO, and allergen-free formulations, with nearly 38% of new product developments incorporating these technologies.

Digital transformation is playing a critical role in demand forecasting and inventory optimization. Machine learning models applied to historical purchase data have improved forecast accuracy by above 20%, reducing stockouts and overstock costs. Traceability platforms leveraging blockchain frameworks are being piloted by approximately 22% of manufacturers to enhance supply chain transparency and ingredient provenance verification. Additionally, AI-driven flavor optimization analytics are enabling formulation teams to refine taste profiles based on consumer preference data, reducing flavor iteration cycles by up to 30%. These integrated technology trends are shaping the competitive landscape, strengthening operational resilience, and enabling faster time-to-market for innovative nutraceutical gummy products.

• In February 2024, Haleon expanded its Centrum portfolio in the United States with new sugar-free multivitamin gummies formulated without artificial flavors or sweeteners. The launch targeted adult immunity and energy support segments, strengthening its presence in chewable supplement formats. Source: www.haleon.com

• In April 2024, Bayer introduced One A Day Kids Multi Gummies with reformulated low-sugar content and updated labeling aligned with enhanced dietary supplement transparency guidelines in North America, reinforcing compliance-focused product innovation within pediatric nutrition. Source: www.bayer.com

• In September 2024, Nestlé Health Science expanded its Nature’s Bounty gummy line with collagen and beauty-support formulations across select Asia-Pacific markets, leveraging plant-based pectin technology to address rising demand for vegan-certified supplements. Source: www.nestlehealthscience.com

• In January 2025, Church & Dwight announced capacity expansion for its Vitafusion gummy production facilities in the United States, integrating automated starchless molding lines to improve manufacturing efficiency and support growing demand for sugar-free and specialty vitamin gummies. Source: www.churchdwight.com

The Nutraceutical Gummies Market Report provides a comprehensive evaluation of product types, application segments, end-user demographics, technology integration, and geographic distribution across five major regions. The report covers vitamin-based, mineral-enriched, botanical, probiotic, collagen, and specialty functional gummies, collectively representing over 100 active product categories across global retail channels. It assesses formulation trends such as sugar-free variants, which account for more than 40% of new product developments, and plant-based gummies exceeding 30% penetration in urban markets.

Geographically, the report examines performance across North America (38% share), Europe (27%), Asia-Pacific (24%), South America (6%), and the Middle East & Africa (5%), highlighting manufacturing hubs that produce over 65% of global volumes. Application analysis spans immunity (over 50% adoption), digestive health (nearly 20%), beauty-focused supplements (approximately 17%), and cognitive and sleep-support categories (around 12%).

Technological evaluation includes automation adoption rates above 60% in large facilities, microencapsulation techniques improving nutrient stability by up to 25%, and digital forecasting tools enhancing supply chain accuracy by more than 20%. The report further addresses regulatory compliance standards, ESG-driven packaging initiatives targeting over 50% recyclable content by 2030, and distribution channels where e-commerce contributes above 35% of total supplement purchases. Emerging niche segments such as personalized gummy blends and condition-specific pediatric formulations are also analyzed to provide forward-looking strategic insights for manufacturers, investors, and healthcare stakeholders.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

8.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Church & Dwight Co., Inc., Bayer AG, Amway Corp., Nestlé Health Science, Haleon plc, Nature’s Way Products, LLC, SmartyPants Vitamins, Olly Public Benefit Corporation, Pharmavite LLC, Hero Nutritionals, Garden of Life |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |