Reports

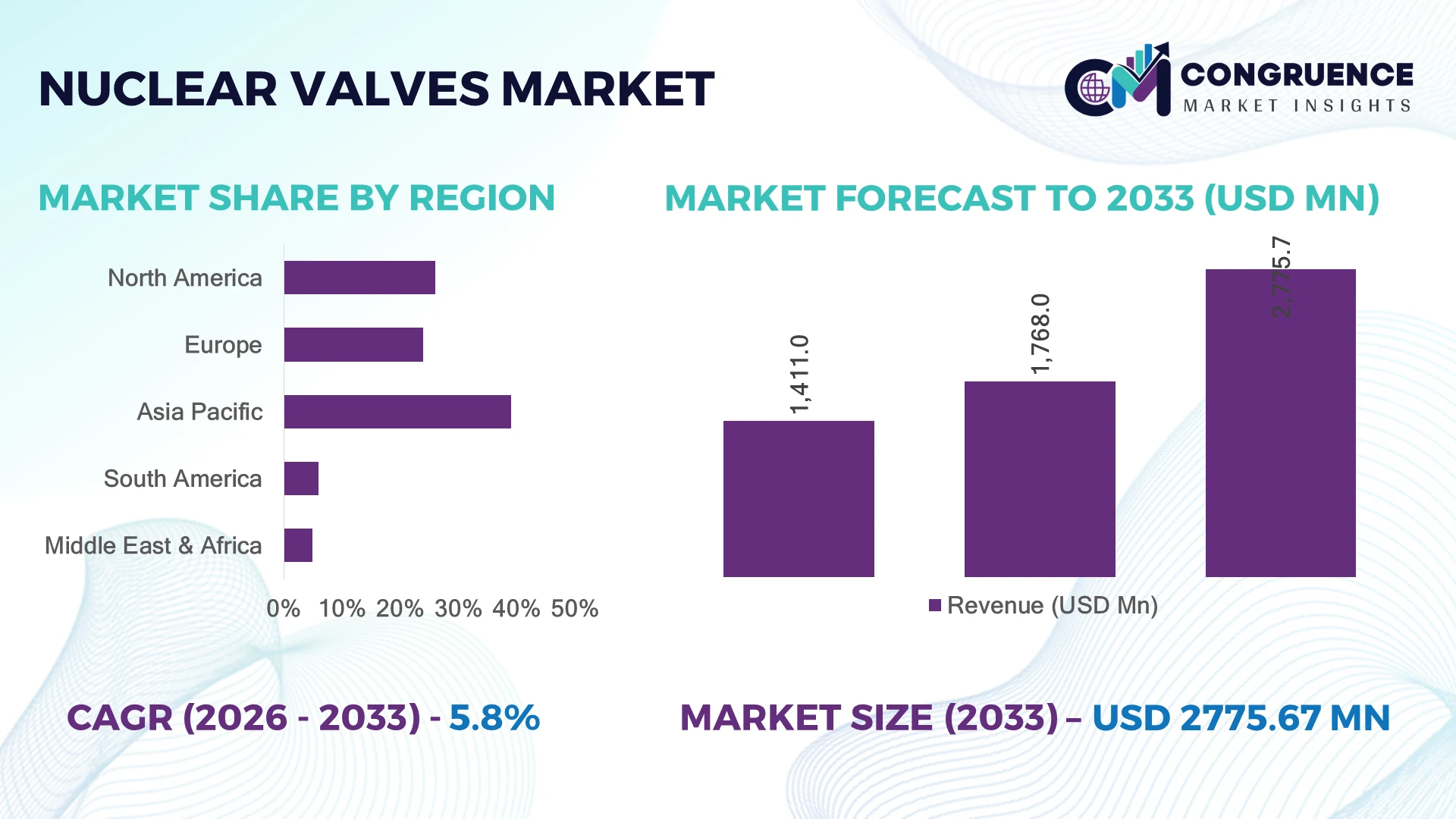

The Global Nuclear Valves Market was valued at USD 1768 Million in 2025 and is anticipated to reach a value of USD 2775.66 Million by 2033 expanding at a CAGR of 5.8% between 2026 and 2033. Growth is accelerating through nuclear reactor life-extension programs, Generation III+ reactor deployments, rising safety retrofits, and increased adoption of corrosion-resistant smart valve systems across pressurized water reactor infrastructure.

China dominates the global nuclear valves market with nearly 28% of active nuclear reactor construction capacity in 2026, supported by over USD 30 billion in ongoing nuclear infrastructure investments and localized high-performance valve manufacturing. France maintains one of the highest nuclear electricity dependency rates globally at approximately 65%, driving steady replacement demand for safety-class valves, while the United States leads in digital monitoring integration with over 40% of upgraded plants deploying predictive valve diagnostics after intensified energy security priorities following the Russia-Ukraine geopolitical disruption.

Manufacturers prioritizing nuclear-grade automation, ASME-certified production capacity, and regional supply chain localization are securing stronger long-term procurement positioning across high-growth reactor modernization programs.

Market Size & Growth: USD 1768 million in 2025 rising to USD 2775.66 million by 2033, driven by advanced reactor upgrades, containment safety retrofits, and global nuclear asset modernization.

Top Growth Drivers: Reactor life-extension projects contribute 34% demand growth, AP1000 and EPR deployments add 29%, while digital valve monitoring adoption rises 22% globally.

Short-Term Forecast: By 2028, predictive maintenance integration reduces unplanned valve downtime by 18% and improves nuclear plant operational efficiency by 14%.

Emerging Technologies: AI-enabled diagnostics, smart actuators, and nickel-alloy corrosion-resistant valves improve maintenance response rates by 26% across advanced nuclear facilities.

Regional Leaders: Asia-Pacific exceeds USD 980 million with rapid reactor expansion, Europe surpasses USD 720 million through refurbishment programs, and North America crosses USD 610 million via digital plant upgrades.

Consumer/End-User Trends: Over 48% of nuclear operators prioritize automated isolation valves to strengthen compliance, remote monitoring, and plant safety performance.

Pilot/Case Example: In 2026, advanced valve automation deployment in a South Korean nuclear facility improved fault detection efficiency by 21% and reduced maintenance cycles by 16%.

Competitive Landscape: The top five manufacturers control nearly 46% market share, led by integrated industrial valve suppliers focused on high-pressure nuclear-grade systems.

Regulatory & ESG Impact: Carbon-neutral energy policies increase nuclear infrastructure approvals by 19%, while stricter safety regulations accelerate certified valve replacement demand globally.

Investment & Funding: More than USD 12 billion in nuclear infrastructure and supply-chain expansion investments strengthen localized component manufacturing across Asia and Europe.

Innovation & Future Outlook: Small modular reactor deployment, digital twin integration, and high-temperature sealing technologies are reshaping long-term procurement and engineering strategies.

The Nuclear Valves Market is advancing through rising deployment of automated safety isolation valves, high-temperature alloy components, and predictive maintenance platforms across commercial reactor fleets. More than 41% of newly commissioned nuclear projects in 2026 integrated digital valve diagnostics to improve operational reliability and reduce inspection intervals. Supply-chain localization initiatives and stricter nuclear safety compliance standards are accelerating procurement modernization, setting the stage for deeper strategic investments and competitive technology differentiation.

The Nuclear Valves Market is becoming strategically critical as governments accelerate reactor modernization, energy-security programs, and low-carbon baseload power deployment after ongoing geopolitical fuel instability reshaped long-term infrastructure priorities. Nuclear operators are restructuring procurement toward localized, safety-certified valve supply chains to reduce dependency on cross-border component sourcing. More than 37% of nuclear facilities scheduled for refurbishment in 2026 include digital valve automation upgrades to improve predictive maintenance accuracy, operational continuity, and compliance efficiency across aging reactor fleets.

Smart actuator-integrated nuclear valves are delivering nearly 22% faster fault response times compared with legacy manually monitored systems while lowering unplanned maintenance interventions by approximately 16%. China continues scaling high-volume reactor construction and domestic valve manufacturing capacity, whereas France and the United States prioritize life-extension retrofits and cybersecurity-integrated control architectures. In South Korea, deployment of AI-assisted valve diagnostics in pressurized water reactors reduced inspection downtime by 19%, strengthening plant utilization rates and operational stability.

Over the next three years, small modular reactor deployment, advanced sealing materials, and digital twin integration are expected to reshape procurement standards and aftermarket service models. Leading manufacturers are expanding nuclear-grade machining facilities, securing long-term utility partnerships, and investing in localized engineering support to strengthen competitive positioning in highly regulated infrastructure programs.

Reactor refurbishment and life-extension initiatives are driving sustained demand for advanced nuclear-grade valves across pressure control, isolation, and coolant management systems. Nearly 44% of operating reactors globally are over 30 years old, increasing replacement demand for corrosion-resistant and automated valve assemblies. In the United States, modernization spending on nuclear infrastructure increased by approximately 18% in 2026 as utilities prioritized safety compliance and digital monitoring upgrades. China simultaneously accelerated domestic valve manufacturing localization to reduce external procurement exposure and shorten delivery timelines by nearly 21%. This structural shift is pushing manufacturers toward ASME-certified production expansion, predictive maintenance integration, and long-term engineering service agreements. Companies investing in localized machining capacity and high-temperature alloy innovation are securing stronger procurement positioning in strategic reactor upgrade programs.

Stringent nuclear certification standards and limited specialized material availability continue constraining production scalability and deployment speed. Nuclear-grade valve qualification cycles typically extend project lead times by 20%–28%, while nickel-alloy and forged steel cost volatility increased component procurement expenses by nearly 17% during recent supply-chain disruptions. France and Japan faced extended maintenance scheduling pressure due to dependency on a limited pool of certified precision component suppliers. These constraints directly affect project profitability, spare-part availability, and maintenance planning consistency for reactor operators. In response, manufacturers are expanding localized forging partnerships, diversifying alloy sourcing strategies, and increasing inventory buffers for mission-critical valve assemblies. Companies capable of integrating vertically controlled supply chains are improving delivery reliability and strengthening long-term utility contract retention.

The transition toward small modular reactors and intelligent plant infrastructure is creating high-value opportunities for advanced valve automation and lifecycle monitoring systems. More than 32% of next-generation reactor projects entering engineering phases in 2026 include AI-enabled valve diagnostics and remote actuator management platforms. Smart valve systems are improving maintenance efficiency by nearly 24% while reducing manual inspection frequency across high-radiation environments. Canada and the United Kingdom are expanding SMR development programs that require compact, digitally integrated flow-control architectures with enhanced cybersecurity protection. Manufacturers are increasing investment in digital twin platforms, sensor-integrated actuators, and predictive analytics partnerships to capture long-term aftermarket service revenue. A non-obvious competitive advantage is emerging around data-driven maintenance contracts, where operational intelligence is becoming as valuable as the valve hardware itself.

Long-term market execution remains constrained by nuclear engineering workforce shortages and growing integration complexity between legacy reactor infrastructure and modern digital valve systems. Nearly 35% of experienced nuclear maintenance specialists in North America are expected to approach retirement within the next decade, increasing operational knowledge-transfer pressure. At the same time, cybersecurity compliance requirements for digitally connected plant systems increased by approximately 23% following stricter industrial control regulations introduced across multiple nuclear-operating economies. Integrating smart valves into decades-old reactor architectures often creates compatibility and calibration challenges that extend commissioning timelines and elevate operational risk. Companies must increase investment in specialized workforce training, cybersecurity-certified automation platforms, and utility collaboration programs to maintain deployment consistency and long-term infrastructure reliability in highly regulated nuclear environments.

Digital Predictive Maintenance Expansion Nuclear operators are accelerating deployment of AI-enabled monitoring systems to reduce unplanned shutdowns and maintenance inefficiencies. Nearly 42% of upgraded reactor facilities in 2026 integrated predictive valve diagnostics, while remote actuator monitoring reduced manual inspection cycles by 18%. Utilities in the United States and South Korea are restructuring maintenance workflows through centralized digital control systems, enabling faster anomaly detection and lower servicing costs. Valve manufacturers are responding through software partnerships, embedded sensor integration, and lifecycle-based service contracts.

Localized Nuclear Supply Chains Ongoing geopolitical trade instability and stricter procurement compliance standards are pushing utilities toward domestic sourcing strategies. China increased localized nuclear valve component procurement by approximately 27%, while France expanded certified forging partnerships to stabilize lead times. Companies are shifting production closer to reactor construction hubs to reduce logistics exposure and improve replacement-part availability. A non-obvious outcome is the rise of regional testing and certification ecosystems that shorten approval cycles for nuclear-grade valve assemblies.

Advanced Alloy Material Adoption High-temperature nickel-alloy and corrosion-resistant valve systems are gaining traction as reactor operators extend plant operating life beyond 60 years. Advanced material deployment improved valve durability by nearly 24% and reduced replacement frequency by 15% in high-pressure coolant systems. Japanese and Canadian operators are prioritizing erosion-resistant trim technologies for aging infrastructure modernization programs. Manufacturers are increasing metallurgical R&D investments and expanding precision machining capabilities to support long-duration reactor performance requirements.

Compact Valve Designs Emerging Small modular reactor development is driving demand for compact, lightweight, and digitally integrated valve architectures optimized for modular deployment environments. More than 31% of next-generation reactor engineering projects now specify compact automated valve systems with integrated cybersecurity features. Companies are redesigning valve assemblies to improve installation speed, reduce maintenance footprint, and simplify remote operations. Strategic alliances between automation firms and nuclear equipment suppliers are accelerating standardization across modular reactor component ecosystems.

Gate Valves continue dominating the Nuclear Valves Market due to their strong sealing performance, durability under high-pressure reactor conditions, and extensive deployment across coolant isolation applications. Nearly 38% of installed nuclear valve infrastructure in 2026 consisted of gate valve systems because of their reliability in critical shutoff operations and long operational lifespan. Globe Valves maintain strong adoption across steam regulation functions where precision flow control remains operationally critical. Meanwhile, Ball Valves are emerging as the fastest-growing segment, supported by rising demand for compact automated systems and faster actuation efficiency in digitally upgraded facilities.

Butterfly Valves are gaining traction in large-diameter cooling circuits due to approximately 16% lower installation weight and simplified maintenance access compared with traditional valve assemblies. Check Valves remain strategically important for backflow prevention and safety compliance in high-pressure reactor environments. Manufacturers are increasing investment in smart actuator compatibility, corrosion-resistant alloys, and modular valve engineering to align with reactor modernization priorities. Procurement strategies are shifting toward low-maintenance and digitally monitored valve configurations as utilities prioritize operational continuity and lifecycle optimization.

Reactor Systems remain the leading application segment due to continuous demand for high-pressure flow regulation, coolant isolation, and reactor safety management infrastructure. Approximately 41% of nuclear valve installations in 2026 were concentrated within primary reactor systems because of strict operational reliability requirements and intensive maintenance cycles. Safety Systems are emerging as the fastest-growing application area as utilities accelerate automated shutdown capability upgrades and digitally integrated emergency response mechanisms. Utilities in the United States and France expanded deployment of smart isolation valves to strengthen compliance with evolving nuclear safety protocols.

Steam Systems continue generating stable procurement demand through turbine efficiency optimization and pressure-control applications, while Cooling Systems are gaining importance as aging plants undergo thermal management modernization. Water Treatment Systems are also expanding steadily with increased emphasis on contamination control and chemical processing precision. Companies are responding through integrated monitoring platforms, predictive maintenance software deployment, and specialized high-temperature valve engineering. Demand concentration is increasingly shifting toward applications capable of reducing downtime and improving long-term plant utilization efficiency.

Safety Systems represent the dominant end-user segment due to their direct role in reactor shutdown operations, emergency isolation functions, and regulatory compliance requirements. Nearly 36% of nuclear valve procurement activity in 2026 was linked to safety-critical infrastructure upgrades as operators prioritized operational resilience and automated fault response. Reactor Systems continue driving large-scale purchasing volumes because of infrastructure dependency across coolant circulation and containment processes. Utilities are increasingly adopting digitally integrated valve assemblies capable of improving response precision and reducing manual intervention in mission-critical environments.

Cooling Systems are emerging as the fastest-growing end-user category as aging facilities modernize thermal efficiency infrastructure and deploy corrosion-resistant flow-control technologies. Steam Systems maintain steady replacement demand tied to turbine optimization programs, while Water Treatment Systems are expanding through stricter contamination-control standards and chemical management automation. Manufacturers are targeting these end-users through customized actuator platforms, lifecycle service agreements, and long-term maintenance partnerships. Competitive positioning is increasingly shaped by certification capabilities, digital integration expertise, and localized engineering support near major reactor-operating hubs.

Asia-Pacific accounted for the largest market share at 39% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2026 and 2033.

Digital Retrofit Programs Reshape Nuclear Infrastructure

North America maintains strong market positioning through extensive reactor modernization projects, advanced automation deployment, and established nuclear engineering capabilities. The region represented nearly 26% of global nuclear valve demand in 2025, supported by large-scale refurbishment programs across aging reactor fleets in the United States and Canada. Utilities are prioritizing smart actuator integration, predictive maintenance systems, and cybersecurity-compliant valve architectures to improve operational reliability. In 2026, multiple U.S. nuclear facilities expanded digital valve monitoring deployments, reducing manual inspection cycles by approximately 18%. Manufacturers are strengthening localized service partnerships and expanding certified machining capacity to support long-duration reactor operation strategies and faster aftermarket response times.

United States Market Outlook: The United States leads regional demand through extensive reactor life-extension initiatives, high adoption of digitally integrated plant infrastructure, and strong domestic engineering capabilities. More than 40% of operating reactors undergoing modernization projects in 2026 incorporated automated valve control upgrades for safety and coolant management systems. Utilities are increasing investment in predictive diagnostics, while suppliers are expanding ASME-certified production and lifecycle maintenance services to secure long-term procurement contracts across strategic energy infrastructure programs.

Life-Extension Investments Strengthen Replacement Demand

Europe remains a strategically important nuclear valves market due to aggressive reactor refurbishment programs, strict safety compliance frameworks, and advanced manufacturing expertise. The region contributed approximately 24% of global demand in 2025, driven by modernization projects in France, the United Kingdom, and Eastern Europe. Utilities are replacing aging flow-control infrastructure with corrosion-resistant and digitally monitored valve systems to improve long-term operational stability. Regulatory pressure surrounding energy security and low-carbon electricity generation accelerated replacement activity across pressurized water reactor facilities. Companies are investing in localized forging partnerships and specialized sealing technologies, while long-term maintenance agreements are becoming increasingly central to competitive positioning in high-compliance nuclear environments.

France Market Outlook: France remains the region’s operational center due to its high nuclear electricity dependency and extensive reactor infrastructure network. Approximately 65% of national electricity generation continues to rely on nuclear energy, creating sustained replacement demand for safety-class valve systems. Utilities are prioritizing high-temperature alloy valves, automated isolation systems, and digital monitoring integration to support reactor life-extension programs. Domestic engineering firms are expanding precision manufacturing and certification capabilities to strengthen procurement resilience and reduce dependency on imported nuclear-grade components.

Large-Scale Reactor Construction Accelerates Procurement

Asia-Pacific dominates the Nuclear Valves Market through aggressive reactor deployment pipelines, localized manufacturing expansion, and rising investment in advanced nuclear infrastructure. The region accounted for nearly 39% of global demand in 2025, supported by extensive construction activity across China, India, and South Korea. China alone represented over 45% of active global nuclear reactor construction projects in 2026, increasing procurement demand for high-pressure isolation and coolant control valves. Regional manufacturers are scaling automated machining capacity and advanced metallurgy production to improve delivery speed and reduce import dependency. Utilities are increasingly adopting digitally integrated valve systems to strengthen operational efficiency across next-generation reactor facilities and modular deployment programs.

China Market Outlook: China leads global deployment activity through rapid nuclear infrastructure expansion, vertically integrated manufacturing ecosystems, and strong government-backed industrial investment. More than 20 reactors remained under active construction during 2026, creating sustained procurement requirements for nuclear-grade valves and automated flow-control systems. Domestic suppliers are increasing localization of smart actuator technologies and corrosion-resistant alloy production while expanding export capabilities. Chinese enterprises are also strengthening partnerships with automation technology providers to improve predictive maintenance integration and long-term reactor operational efficiency.

Selective Infrastructure Expansion Supports Demand

South America represents a smaller but strategically developing market supported by targeted nuclear infrastructure modernization and energy diversification efforts. The region contributed close to 6% of global nuclear valve demand in 2025, with procurement activity concentrated primarily in Brazil and Argentina. Utilities are focusing on upgrading cooling systems, safety valves, and steam management infrastructure within existing reactor facilities rather than large-scale new reactor deployment. In Brazil, operational modernization initiatives improved maintenance efficiency by approximately 14% through partial automation upgrades. However, limited domestic manufacturing capacity and extended certification timelines continue constraining faster scalability. Suppliers are responding through localized service agreements, technical partnerships, and regional maintenance support expansion to strengthen long-term project continuity.

Brazil Market Outlook: Brazil remains the most strategically important market in South America due to its established nuclear generation infrastructure and ongoing reactor modernization priorities. Utilities are increasing investment in digitally monitored valve assemblies and corrosion-resistant cooling system components to improve operational reliability. National energy diversification strategies are also supporting incremental nuclear infrastructure upgrades. Engineering firms are expanding technical servicing capabilities and forming partnerships with international nuclear equipment providers to improve spare-part availability and reduce maintenance turnaround time across critical reactor systems.

Nuclear Diversification Programs Drive New Investments

Middle East & Africa is emerging as the fastest-transforming nuclear valves market due to growing energy diversification strategies, large-scale infrastructure investments, and increasing deployment of advanced reactor technologies. The region represented approximately 5% of global demand in 2025 but is rapidly strengthening its procurement footprint through new nuclear generation projects. The United Arab Emirates expanded operational optimization initiatives across its nuclear facilities in 2026, increasing automated valve deployment within safety and coolant management systems. Governments are prioritizing localized maintenance ecosystems and strategic technology transfer agreements to reduce long-term operational dependency. Suppliers are responding through regional engineering partnerships, workforce training programs, and certified service-center expansion near high-value nuclear infrastructure hubs.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional market momentum through advanced nuclear infrastructure deployment and strong operational investment capabilities. The country’s multi-reactor nuclear program has accelerated demand for digitally integrated safety valves, cooling-system controls, and predictive maintenance technologies. Utilities are emphasizing operational continuity and cybersecurity-compliant automation platforms to optimize reactor performance. International suppliers are establishing long-term technical partnerships and localized engineering support operations to strengthen service responsiveness and align with expanding nuclear energy diversification initiatives.

The Nuclear Valves Market is controlled by global industrial valve leaders including Emerson Electric, Flowserve, IMI, Velan, and Curtiss-Wright competing against specialized regional nuclear equipment manufacturers and low-cost Asian suppliers. The top five players collectively account for nearly 48% of global procurement activity, driven by certification strength, nuclear-grade manufacturing capacity, and long-term utility relationships. Competition increasingly centers on digital monitoring integration, corrosion-resistant metallurgy, delivery speed, and lifecycle servicing capabilities rather than pricing alone. Automated smart-valve systems improved maintenance efficiency by approximately 20%, pushing technology-focused suppliers ahead of conventional component manufacturers. Companies are expanding localized machining facilities, securing strategic utility partnerships, and vertically integrating actuator and diagnostics technologies to stabilize supply chains after recent geopolitical disruptions. Entry barriers remain high due to ASME qualification requirements, multi-year certification timelines, and strict reactor safety compliance standards. Winning market share now requires advanced engineering support, digital integration expertise, and highly reliable localized aftermarket servicing capabilities.

Emerson Electric Co.

Flowserve Corporation

IMI plc

Velan Inc.

Curtiss-Wright Corporation

KSB SE & Co. KGaA

KITZ Corporation

Crane Company

Baker Hughes

CIRCOR International

Weir Group PLC

Neway Valve (Suzhou) Co., Ltd.

Samson AG

Schlumberger Limited

Digital diagnostics and smart actuator technologies are transforming nuclear valve operations through predictive maintenance and real-time condition monitoring. Nearly 43% of upgraded nuclear facilities in 2026 integrated sensor-enabled valve systems linked with centralized control platforms, improving fault detection efficiency by approximately 21%. Compared with legacy manually inspected assemblies, AI-assisted valve diagnostics reduced unplanned maintenance downtime by nearly 18% and accelerated outage planning cycles. Utilities operating aging pressurized water reactors are prioritizing automated isolation systems to strengthen compliance, operational continuity, and workforce efficiency under tightening inspection schedules.

Advanced metallurgy and additive manufacturing technologies are accelerating deployment of high-performance nuclear-grade valves designed for extreme pressure and thermal conditions. Nickel-alloy valve components improved corrosion resistance by roughly 24% compared with conventional stainless-steel assemblies, extending maintenance intervals across coolant and steam systems. More than 31% of next-generation reactor projects entering engineering stages between 2026 and 2028 specify compact modular valve architectures optimized for small modular reactors. Manufacturers in China, France, and South Korea are expanding precision forging and digital machining capabilities to shorten delivery timelines and reduce supply-chain exposure.

Cybersecurity-integrated automation platforms are emerging as a disruptive competitive differentiator across nuclear infrastructure modernization programs. Suppliers combining predictive analytics, digital twin integration, and remote diagnostics are securing stronger long-term utility contracts through lifecycle-based service models and operational performance guarantees.

February 2026 – Flowserve Corporation announced the acquisition of Trillium Flow Technologies’ Valves Division for USD 490 million, adding over 200,000 installed valve units across 115 operating nuclear reactors. The move strengthens aftermarket servicing scale and small modular reactor positioning. Source: Valve World

February 2025 – Emerson Electric expanded its North American Impact Partner Network with 18 certified service partners supporting valve diagnostics, automation, and outage servicing operations. The initiative increased localized instrumentation support coverage across the United States and Canada, improving operational responsiveness and maintenance execution efficiency. Source: Emerson

February 2026 – Flowserve Corporation strengthened nuclear lifecycle engineering services through expanded deployment of ASME-certified valve and actuator systems supporting more than 300 reactors worldwide. The company increased focus on Generation IV and small modular reactor-ready flow-control infrastructure to support long-term nuclear modernization programs. Source: Flowserve

January 2026 – Flowserve Corporation showcased advanced motor-operated and severe-service nuclear valve technologies at AUG MUG 2026, highlighting digitally integrated systems designed to improve operational reliability and maintenance efficiency across nuclear power facilities. The deployment focus strengthened automation-led positioning within high-compliance reactor infrastructure environments. Source: Flowserve Events

The Nuclear Valves Market Report delivers comprehensive analysis across valve types including gate valves, globe valves, ball valves, butterfly valves, and check valves, with detailed evaluation of deployment trends across reactor systems, steam systems, cooling systems, water treatment systems, and safety systems. The study covers operational demand patterns across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting infrastructure modernization activity, localization strategies, and digital automation adoption. Nearly 40% of analyzed procurement activity is linked to reactor refurbishment and safety-system upgrades between 2026 and 2033.

The report evaluates smart actuator integration, predictive maintenance platforms, corrosion-resistant alloys, compact modular valve architectures, and cybersecurity-integrated automation systems shaping next-generation nuclear infrastructure. It includes competitive benchmarking of leading manufacturers, utility procurement priorities, aftermarket servicing trends, and certification-driven supply-chain dynamics. More than 45% of assessed enterprise strategies focus on digital monitoring integration and localized manufacturing expansion, supporting investment planning, technology positioning, operational optimization, and long-term infrastructure deployment strategies across advanced nuclear energy ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1768 Million |

|

Market Revenue in 2033 |

USD 2775.66 Million |

|

CAGR (2026 - 2033) |

5.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Emerson Electric Co., Flowserve Corporation, IMI plc, Velan Inc., Curtiss-Wright Corporation, KSB SE & Co. KGaA, KITZ Corporation, Crane Company, Baker Hughes, CIRCOR International, Weir Group PLC, Neway Valve (Suzhou) Co., Ltd., Samson AG, Schlumberger Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |