Reports

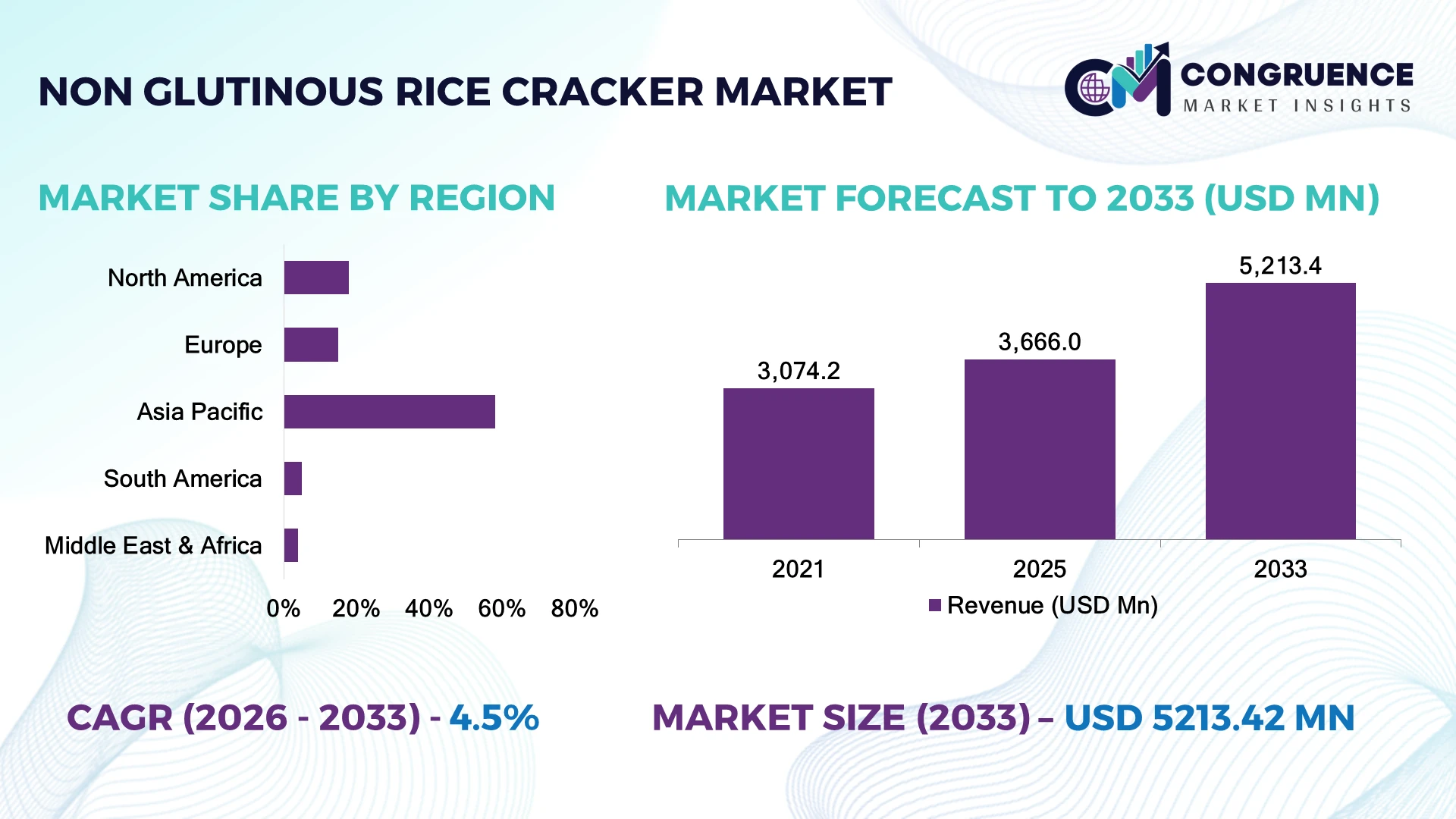

The Global Non-Glutinous Rice Cracker Market was valued at USD 3,666.0 Million in 2025 and is anticipated to reach a value of USD 5,213.4 Million by 2033 expanding at a CAGR of 4.5% between 2026 and 2033. Growth is driven by rising gluten-free food adoption, expansion of automated rice processing facilities, and demand for clean-label snack products with improved shelf stability.

Japan dominates the market with approximately 32% share, supported by advanced rice processing infrastructure, premium snack manufacturing, and investments in automated production lines exceeding USD 1 billion annually across food processing segments. China follows with over 25% share, benefiting from large-scale rice cultivation and export-oriented manufacturing, while India’s rice-based snack sector expands through regional brands and modern retail adoption. Japan’s production efficiency remains nearly 20% higher than several emerging Asian markets due to automation integration.

The strategic implication is that manufacturers prioritizing automation, regional sourcing, and premium product innovation will strengthen competitive positioning.

Market Size & Growth: USD 3,666.0 Million in 2025 to USD 5,213.4 Million by 2033 at 4.5% CAGR, driven by automated snack manufacturing and gluten-free product expansion.

Top Growth Drivers: Gluten-free consumption (+35%), premium snack demand (+28%), and online food retail penetration (+22%) are accelerating market momentum.

Short-Term Forecast: By 2028, automated production adoption improves manufacturing efficiency by 15% and reduces processing waste by 10%.

Emerging Technologies: AI-based quality inspection, robotic packaging systems, and advanced rice milling technologies are transforming production operations.

Regional Leaders: Asia Pacific reaches USD 3.1 billion with rice-based innovation; North America reaches USD 1.0 billion with health-snack adoption; Europe reaches USD 850 million with clean-label trends.

Consumer/End-User Trends: Over 45% of urban snack consumers prefer gluten-free or reduced-allergen alternatives, increasing demand for rice-based products.

Pilot/Case Example: In 2024, Japanese snack manufacturers implemented AI sorting systems, achieving approximately 18% defect reduction in rice cracker production.

Competitive Landscape: Japan-based producers lead with nearly 30% market influence, alongside key players including Kameda Seika, Sanko Seika, Want Want Holdings, and Calbee.

Regulatory & ESG Impact: Sustainable packaging initiatives reduce plastic usage by nearly 20% as food companies align with global environmental regulations.

Investment & Funding: More than USD 500 million is directed toward food automation, production expansion, and sustainable packaging partnerships across Asia-Pacific.

Innovation & Future Outlook: Next-generation flavors, functional ingredients, and digitally optimized manufacturing will redefine global non-glutinous rice cracker competition.

Non-glutinous rice crackers are gaining traction across health-focused retail channels, convenience stores, and premium snack categories due to innovations in seasoning technology, reduced-sodium formulations, and functional ingredient integration. Approximately 40% of new product launches emphasize healthier positioning, while manufacturers are adapting supply chains amid global grain price fluctuations and evolving food safety requirements. These shifts are creating new opportunities for differentiated product strategies and regional expansion.

The Non-Glutinous Rice Cracker Market is becoming strategically important as food manufacturers shift toward healthier snack portfolios, resilient ingredient sourcing, and automated production ecosystems. Rising consumer preference for allergen-friendly foods, combined with supply-chain restructuring after global grain disruptions, is encouraging companies to secure local rice supplies and strengthen processing capabilities.

Advanced manufacturing technologies are improving operational performance compared with traditional production systems. AI-enabled inspection and automated packaging reduce quality-control errors by nearly 15% and improve throughput efficiency by around 20% compared with manual operations. Japan and South Korea maintain leadership through high automation adoption, while Southeast Asian markets are expanding through lower-cost production bases and increasing export capacity.

Companies are investing in smart factories, sustainable packaging, and strategic partnerships to improve competitiveness. For example, major snack producers are deploying digital monitoring systems to optimize moisture control and product consistency across facilities. Over the next 2–3 years, operational efficiency, premium product diversification, and supply-chain localization will become decisive factors. Businesses that combine technology adoption with consumer-focused innovation will secure stronger long-term market relevance and competitive advantage.

Rising demand for gluten-free and clean-label snacks is accelerating investment in non-glutinous rice cracker production, with approximately 35% of new snack launches emphasizing allergen-free positioning and nearly 40% of consumers prioritizing healthier alternatives. Japan and South Korea are expanding automated rice processing facilities to improve consistency and reduce labor dependency. Recent food manufacturing shifts toward AI-based quality inspection have lowered production defects by around 15%, enabling companies to enhance product reliability. Leading manufacturers are responding through capacity expansion, flavor innovation, and partnerships with retail chains to capture premium snack segments while strengthening supply resilience.

Non-glutinous rice cracker producers face structural pressure from fluctuating rice prices, packaging costs, and dependence on regional agricultural cycles. Global rice supply disruptions have contributed to raw material price variations of nearly 20%, while packaging expenses have increased by approximately 15% in several manufacturing markets. Countries such as Japan rely heavily on stable domestic rice availability, creating cost challenges during unfavorable harvest periods. These pressures directly affect production margins and pricing flexibility. Companies are reducing exposure through multi-country sourcing strategies, long-term supplier contracts, and investments in efficient milling technologies that optimize raw material utilization.

Advanced manufacturing and product diversification are creating new opportunities for non-glutinous rice cracker companies, particularly through automation, functional ingredients, and digital supply-chain systems. Automated production lines can improve operational efficiency by nearly 20%, while premium snack categories are seeing more than 30% growth in demand for fortified, low-sodium, and organic formulations. India and Southeast Asian markets present opportunities through expanding modern retail networks and local rice-processing ecosystems. Companies are investing in R&D partnerships, sustainable packaging solutions, and direct-to-consumer channels to capture emerging consumer segments. A key strategic opportunity lies in combining traditional rice-based products with functional nutrition positioning.

Manufacturers face execution challenges in maintaining uniform texture, flavor consistency, and food safety compliance while scaling production across international markets. Approximately 25% of producers still rely on semi-automated processes, creating efficiency gaps compared with fully digitized facilities. Increasing regulatory scrutiny on labeling, additives, and packaging sustainability is adding operational complexity, particularly in export markets such as the United States and European countries. Workforce shortages in advanced food processing hubs further pressure production continuity. Companies must address these barriers through smart factory investments, workforce training programs, and integrated quality-management systems to maintain competitiveness and ensure consistent global deployment.

AI Quality Optimization Food manufacturers are integrating AI-based inspection systems and automated sorting technologies to improve production consistency, with adoption increasing by nearly 20% among advanced snack processors. Japanese producers are using machine vision to reduce product defects by around 15% and accelerate quality checks. This workflow transition is helping companies lower waste, improve batch accuracy, and maintain export-grade standards amid stricter food safety requirements.

Sustainable Packaging Shift Non-glutinous rice cracker companies are restructuring packaging operations as environmental regulations increase pressure on single-use plastics. Approximately 30% of new snack packaging initiatives focus on recyclable or lightweight materials, reducing packaging material consumption by nearly 15%. Manufacturers in Japan and Europe are partnering with sustainable packaging suppliers to improve ESG compliance while controlling logistics costs through lighter packaging formats.

Premium Flavor Innovation Snack producers are expanding beyond traditional rice crackers through functional ingredients, low-sodium formulations, and regional flavor customization. Nearly 40% of new product launches emphasize health-oriented attributes, while premium snack demand is increasing through online retail channels. Companies are investing in R&D collaborations to introduce fortified products targeting urban consumers seeking convenient nutrition-focused snacks.

Digital Supply Chain Integration Food companies are adopting digital inventory monitoring and predictive supply-chain systems to manage rice sourcing volatility. Around 25% of larger manufacturers have increased investment in supply-chain analytics to improve forecasting accuracy and reduce operational disruptions. Rising labor costs in Japan and South Korea are accelerating automation adoption, enabling producers to maintain output efficiency and strengthen supplier coordination.

Traditional non-glutinous rice crackers represent the leading segment, accounting for approximately 55% of the market due to established consumer preference, scalable manufacturing processes, and strong distribution networks in Japan, China, and South Korea. Their long shelf life, cost efficiency, and compatibility with automated production lines continue to support dominance. Premium flavored varieties hold around 25% share and are expanding as companies introduce seafood, vegetable, spice, and functional ingredient-based formulations. The fastest-growing segment is organic and functional non-glutinous rice crackers, supported by increasing demand for healthier snack alternatives and clean-label products. This category is growing as manufacturers focus on reduced sodium, added nutrients, and sustainable ingredient sourcing. Conventional varieties remain important for mass-market consumption, while specialty products attract higher-value consumers. Companies are increasing R&D investment and forming retail partnerships to expand premium product portfolios.

Retail snack consumption represents the leading application segment with approximately 60% market share, supported by supermarkets, convenience stores, and e-commerce platforms across Japan, China, and the United States. Packaged rice crackers remain highly preferred due to portability, affordability, and long shelf stability. Foodservice applications account for nearly 20% share, supported by restaurants and hospitality businesses incorporating rice-based snacks into menus. The fastest-growing application is online and direct-to-consumer sales, expanding as digital grocery adoption increases. Approximately 30% of premium snack purchases now involve online channels in major urban markets, allowing brands to reach niche consumers more efficiently. Institutional applications, including schools and workplace catering, continue developing through demand for allergen-friendly snack options. Companies are strengthening digital marketing, improving packaging formats, and expanding distribution partnerships to capture changing purchasing behavior.

Household consumers represent the leading end-user group with approximately 65% market share, driven by frequent snack consumption, convenience preferences, and growing awareness of gluten-free food choices. Japan maintains strong household demand due to established rice snack culture, while China and India are expanding consumption through modern retail channels. Commercial food manufacturers account for nearly 20% share as they incorporate rice crackers into packaged food offerings and private-label products. The fastest-growing end-user segment is health-conscious urban consumers, supported by increasing demand for functional snacks and premium ingredients. This group is expanding as approximately 40% of younger consumers actively seek healthier snack alternatives. Foodservice operators and institutional buyers are also increasing adoption through customized snack solutions. Companies are responding with targeted product lines, regional flavor strategies, and partnerships with retailers to strengthen consumer engagement.

Asia-Pacific accounted for the largest market share at 58% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

North America is strengthening its position through rising gluten-free food adoption, premium snack innovation, and expanded retail availability. The region contributes approximately 18% of global demand, supported by strong distribution networks in the United States and Canada. Major food companies are increasing investments in clean-label product lines, with gluten-free snack categories accounting for nearly 30% of new health-oriented launches. E-commerce platforms and private-label retail expansion are improving product accessibility, while automated packaging systems are helping manufacturers reduce labor dependency. Companies are responding through partnerships with retailers, localized production strategies, and investments in sustainable packaging formats to capture evolving consumer preferences.

United States Market Outlook: The United States represents the largest North American market, supported by advanced food processing infrastructure and strong demand from health-conscious consumers. More than 40% of urban snack buyers actively seek allergen-friendly products, encouraging manufacturers to expand rice-based snack portfolios. Companies are increasing domestic production capabilities and introducing functional varieties targeting premium retail channels.

Europe is experiencing increased adoption of non-glutinous rice crackers through demand for organic, low-allergen, and environmentally responsible snacks. The region represents nearly 15% of global consumption, with Germany, the United Kingdom, and France serving as key markets. Regulatory emphasis on sustainable packaging and transparent ingredient labeling is influencing product development strategies. Approximately 35% of new snack launches in major European markets include health-focused claims, encouraging manufacturers to reformulate products. Companies are investing in recyclable packaging technologies, regional supplier partnerships, and premium product extensions to improve competitiveness. Digital grocery platforms are also expanding access to specialty rice-based snacks across urban markets.

Germany Market Outlook: Germany leads European adoption due to strong food processing capabilities, advanced retail networks, and sustainability-focused consumer behavior. Nearly 30% of German snack consumers prioritize products with clean ingredient profiles, driving manufacturers to introduce organic and reduced-sodium rice crackers. Companies are strengthening partnerships with supermarkets and investing in sustainable production systems to meet evolving regulatory expectations.

Asia-Pacific dominates the non-glutinous rice cracker market with approximately 58% share, supported by established rice cultivation, large-scale manufacturing, and strong consumer familiarity. Japan, China, and South Korea account for major production capacity, with Japan recognized for advanced processing technologies and premium product innovation. More than 50% of global rice cracker manufacturing activity is concentrated within Asian supply chains. Companies are deploying automated production lines, improving packaging efficiency, and expanding export networks to address international demand. Rising investment in food automation and digital manufacturing systems is improving production consistency and reducing operational costs across major facilities.

Japan Market Outlook: Japan remains the strategic leader due to its mature rice cracker industry, advanced automation adoption, and strong domestic brand ecosystem. Over 60% of premium rice cracker manufacturers utilize advanced processing and quality-control technologies to maintain product consistency. Companies are focusing on functional ingredients, export expansion, and sustainable packaging innovation to strengthen global competitiveness.

South America is developing as an emerging market supported by expanding processed food industries and increasing demand for healthier snack alternatives. The region contributes approximately 5% of global demand, with Brazil and Argentina representing key consumption centers. Local manufacturers are improving rice processing capabilities and expanding modern retail distribution networks. Approximately 20% of urban consumers in major markets are shifting toward healthier packaged snacks, creating opportunities for rice-based products. Companies are forming distribution partnerships and improving domestic production efficiency to reduce dependence on imported specialty snacks. Infrastructure limitations and uneven retail penetration remain operational considerations for expansion.

Brazil Market Outlook: Brazil holds the strongest position in South America due to its large agricultural base and expanding packaged food sector. The country’s rice production infrastructure supports local snack manufacturing, while urban retail channels continue adopting healthier product categories. Companies are investing in localized processing facilities and partnerships with supermarkets to improve market penetration.

Middle East & Africa represents a developing market supported by food diversification strategies, increasing imported snack availability, and modernization of retail infrastructure. The region accounts for approximately 4% of global demand, with the United Arab Emirates, Saudi Arabia, and South Africa showing stronger adoption. Growing investment in food processing facilities and logistics infrastructure is improving specialty snack distribution. Around 25% of premium packaged food growth in major urban centers is linked to healthier and international snack categories. Companies are expanding through distributor partnerships, localized packaging solutions, and retail collaborations to address changing consumer preferences.

United Arab Emirates Market Outlook: The United Arab Emirates is emerging as the leading market due to advanced retail infrastructure, high imported food consumption, and strong premium snack demand. More than 35% of urban consumers demonstrate preference for international health-oriented food products. Companies are using the UAE as a regional distribution hub while developing partnerships with retailers and hospitality operators.

The Non-Glutinous Rice Cracker Market features global leaders such as Kameda Seika, Calbee, and Want Want competing with regional manufacturers focused on pricing and distribution strength. Top five players collectively control approximately 35% share, creating a moderately fragmented structure. Competition centers on product innovation, supply reliability, flavor customization, and automation, with premium launches increasing nearly 25% and automated processing improving efficiency by 15%. Global brands compete through technology upgrades and export expansion, while regional players leverage cost advantages and local taste preferences. Companies are forming retail partnerships, improving packaging systems, and integrating production capabilities to secure margins. The competitive shift is moving toward functional ingredients, sustainable packaging, and digital manufacturing. High-quality rice sourcing and established distribution networks remain major entry barriers. Winning players will combine operational efficiency, consumer-focused innovation, and resilient supply chains to outperform established competitors.

Calbee, Inc.

Want Want Holdings Limited

Sanko Seika Co., Ltd.

Koikeya Inc.

Iwatsuka Confectionery Co., Ltd.

Bourbon Corporation

Liwayway Marketing Corporation

Yuki & Love Co., Ltd.

Edward & Sons Trading Company

Lundberg Family Farms

Hapi Snacks

TH Foods, Inc.

Manufacturers are adopting AI-powered inspection, robotic packaging, and digital production monitoring to improve consistency and reduce waste. AI vision systems improve defect detection accuracy by around 15%, while automated packaging reduces labor requirements by nearly 20%. Adoption is strongest among Japanese and South Korean producers seeking higher throughput.

Advanced rice processing technologies, including precision milling and controlled baking systems, are replacing traditional manual operations. Modern facilities achieve approximately 20% higher production efficiency compared with conventional lines. Large manufacturers benefit through improved quality control, faster product customization, and reduced operational downtime.

Between 2026 and 2028, smart factory integration, sustainable packaging automation, and data-driven supply chains will become major competitive differentiators. Companies investing early in connected manufacturing will gain advantages in cost control and scalability, while smaller producers face pressure to modernize. Functional ingredient processing and digital traceability systems will also support premium product development and stronger consumer trust.

March 2025 Kameda Seika official news introduced new rice-based snack innovations, including premium and functional product extensions such as “Kameda no Usuyaki Rich Ume Zarame,” strengthening its portfolio diversification strategy. The company expanded flavor customization to address premium snack demand and improve consumer engagement.

April 2025 Kameda Seika official release launched “Kameda no Kakino Tane Dry Natto-iri” through 21,743 Seven-Eleven Japan stores, combining rice crackers with freeze-dried natto ingredients. The product expansion targeted functional snacking demand and strengthened convenience-channel penetration through hybrid food innovation. Source: www.kamedaseika.co.jp

July 2025 Calbee official news release launched the limited-edition “Kappa Ebisen Nori Shio Flavor,” expanding seasoning innovation through dual seaweed flavor technology. The company increased product differentiation through limited-time launches, supporting brand engagement and faster response to changing snack preferences. Source: www.calbee.co.jp

September 2025 Sanko Seika official news portal expanded sustainability initiatives and manufacturing improvement activities, including research collaboration on optimizing heat energy flow during rice cracker production. The initiative focused on improving production efficiency and strengthening environmentally responsible manufacturing practices. Source: www.sanko-seika.co.jp

The Non-Glutinous Rice Cracker Market Report covers market segmentation by type, application, and end-user, analyzing traditional crackers, premium variants, retail channels, foodservice usage, and household consumption patterns. The study evaluates major markets across North America, Europe, Asia-Pacific, South America, and Middle East & Africa with focus on manufacturing capacity, technology adoption, and competitive positioning.

The report examines automation, AI-based quality systems, sustainable packaging, and advanced processing technologies shaping industry transformation. It provides strategic insights into supplier networks, consumer trends, investment priorities, and expansion opportunities. Analysis includes leading companies, emerging product categories, operational challenges, and future positioning strategies to support business planning and competitive decision-making between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 3,666.0 Million |

| Market Revenue (2033) | USD 5,213.4 Million |

| CAGR (2026–2033) | 4.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Kameda Seika Co., Ltd.; Calbee, Inc.; Want Want Holdings Limited; Sanko Seika Co., Ltd.; Koikeya Inc.; Iwatsuka Confectionery Co., Ltd.; Bourbon Corporation; Liwayway Marketing Corporation; Yuki & Love Co., Ltd.; Edward & Sons Trading Company; Lundberg Family Farms; Hapi Snacks; TH Foods, Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |