Reports

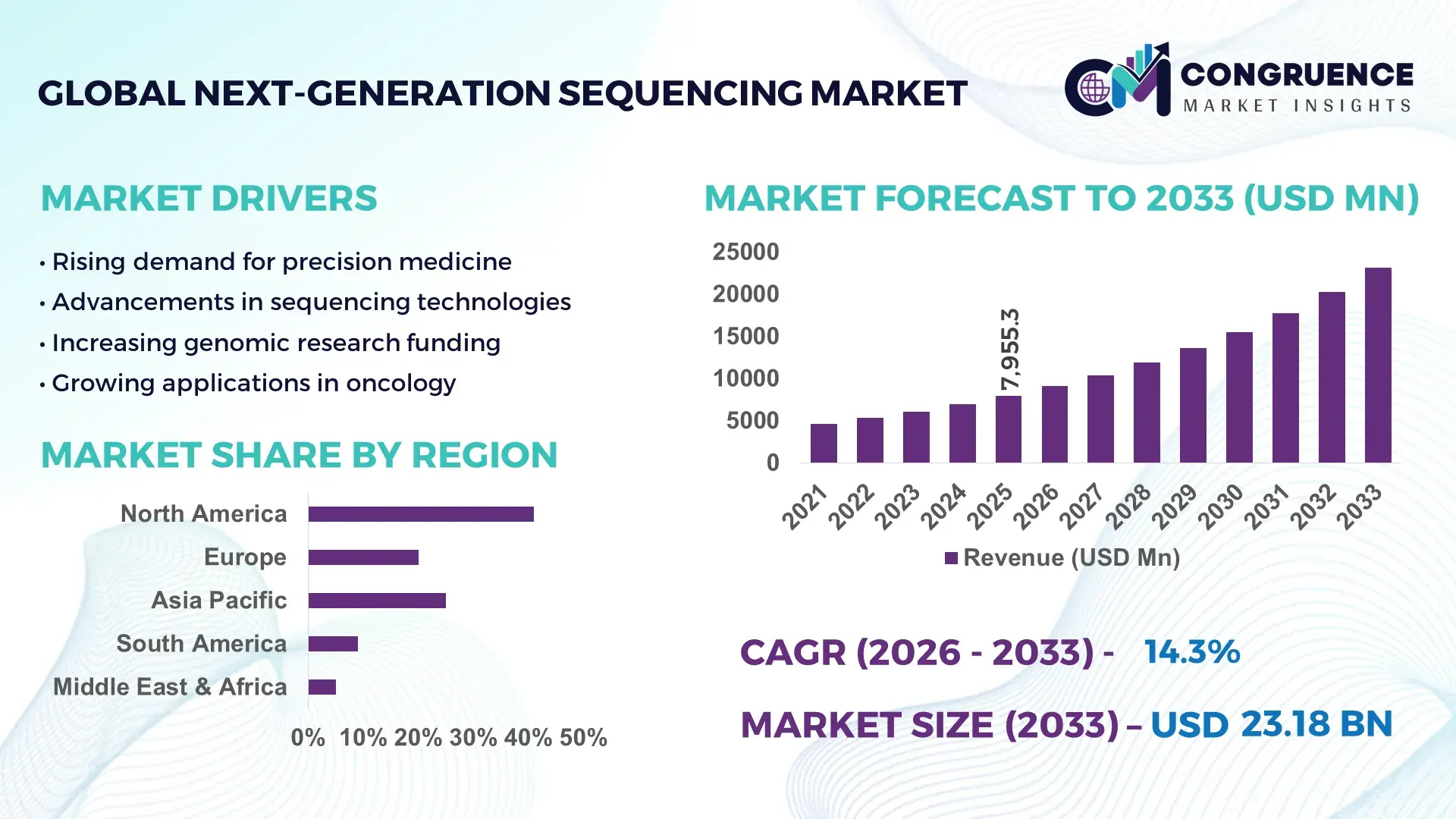

The Global Next-Generation Sequencing Market was valued at USD 7955.28 Million in 2025 and is anticipated to reach a value of USD 23175.29 Million by 2033 expanding at a CAGR of 14.3% between 2026 and 2033. This growth is primarily driven by increasing demand for precision medicine and advanced genomic diagnostics.

The United States continues to lead the next-generation sequencing market with robust infrastructure, extensive research funding, and large-scale clinical adoption. The country hosts over 40% of global sequencing facilities and processes millions of genomic samples annually across oncology, rare disease diagnostics, and population genomics. Federal initiatives have allocated over USD 3 billion toward genomics research programs, while more than 60% of major pharmaceutical companies integrate sequencing technologies into drug discovery pipelines. Additionally, over 75% of leading clinical laboratories in the U.S. have adopted high-throughput sequencing platforms, enabling rapid genome analysis with turnaround times reduced by nearly 50% over the past decade.

Market Size & Growth: Valued at USD 7955.28 Million in 2025, projected to reach USD 23175.29 Million by 2033 at a CAGR of 14.3%, driven by rising genomic research and clinical diagnostics demand.

Top Growth Drivers: Clinical adoption increased by 38%, sequencing cost reduction improved efficiency by 45%, and bioinformatics integration boosted workflow productivity by 32%.

Short-Term Forecast: By 2028, sequencing costs are expected to decline by 25%, enhancing accessibility across mid-scale laboratories.

Emerging Technologies: Single-cell sequencing, nanopore sequencing, and AI-powered genomic analytics are reshaping data accuracy and speed.

Regional Leaders: North America projected at USD 9.8 Billion by 2033 with strong clinical adoption; Europe at USD 6.5 Billion driven by research funding; Asia-Pacific at USD 5.7 Billion with expanding genomic programs.

Consumer/End-User Trends: Hospitals and research institutes account for over 65% usage, with increasing adoption in diagnostics and personalized treatment planning.

Pilot or Case Example: In 2024, a large-scale genomics project reduced disease diagnosis time by 40% using automated sequencing pipelines.

Competitive Landscape: Market leader holds approximately 35% share, followed by major players including Thermo Fisher Scientific, BGI Group, Agilent Technologies, and Pacific Biosciences.

Regulatory & ESG Impact: Governments are implementing genomic data privacy frameworks and promoting sustainable lab practices reducing waste by 20%.

Investment & Funding Patterns: Over USD 10 billion invested globally in genomics startups and sequencing infrastructure over the past three years.

Innovation & Future Outlook: Integration of AI, cloud computing, and real-time sequencing is expected to drive next-phase growth and operational scalability.

The next-generation sequencing market is shaped by strong contributions from oncology, infectious disease diagnostics, and agricultural genomics, with oncology alone accounting for over 35% of sequencing applications. Technological innovations such as high-throughput sequencers and automated sample preparation systems are reducing processing time by up to 60%. Regulatory frameworks supporting genomic testing and increased funding for precision medicine are accelerating adoption across developed and emerging markets. Asia-Pacific is witnessing rapid growth due to expanding healthcare infrastructure and government-backed genome projects, while Europe emphasizes data governance and ethical sequencing practices. Future trends include integration of artificial intelligence for predictive genomics and expansion of decentralized sequencing models.

The next-generation sequencing market holds strategic importance as a foundational technology enabling precision medicine, advanced diagnostics, and large-scale genomic research. Organizations are increasingly aligning sequencing capabilities with healthcare digitization strategies, resulting in measurable efficiency gains and improved patient outcomes. Advanced sequencing platforms deliver up to 70% faster genome analysis compared to traditional Sanger sequencing, significantly enhancing throughput and accuracy for clinical and research applications. North America dominates in volume due to extensive infrastructure and research funding, while Asia-Pacific leads in adoption with over 55% of new laboratories integrating sequencing technologies into diagnostic workflows. By 2028, artificial intelligence-driven genomic analytics is expected to improve data interpretation efficiency by 40%, reducing manual intervention and accelerating clinical decision-making processes.

Firms are committing to sustainability and compliance metrics, including a 30% reduction in laboratory waste and energy-efficient sequencing systems by 2030. In 2024, China achieved a 35% improvement in sequencing turnaround time through AI-enabled genomic platforms deployed in national research centers. Such initiatives demonstrate how technology integration enhances operational efficiency and scalability. Strategically, companies are focusing on partnerships, automation, and cloud-based genomic platforms to enhance accessibility and reduce costs. The next-generation sequencing market is evolving as a critical pillar supporting healthcare resilience, regulatory compliance, and sustainable growth across global biomedical ecosystems.

The increasing emphasis on precision medicine is a primary driver of the next-generation sequencing market, as healthcare systems shift toward individualized treatment approaches. Over 60% of oncology treatment protocols now incorporate genomic profiling to identify targeted therapies, significantly improving patient outcomes. Sequencing technologies enable rapid identification of genetic mutations, reducing diagnostic timelines by up to 50%. Pharmaceutical companies are increasingly using genomic data to streamline drug development, with more than 70% of new drug pipelines incorporating sequencing insights. Additionally, population genomics initiatives involving millions of participants are expanding the application scope of sequencing technologies, further boosting demand across clinical and research sectors.

High capital investment requirements for sequencing platforms and associated infrastructure present a significant restraint for the next-generation sequencing market. Advanced sequencing systems can cost several hundred thousand dollars, making them less accessible to smaller laboratories and healthcare facilities. Additionally, operational costs, including skilled personnel, data storage, and maintenance, add to the financial burden. Data analysis requires specialized bioinformatics expertise, with training costs and resource constraints limiting widespread adoption. Furthermore, the complexity of integrating sequencing workflows into existing healthcare systems creates operational challenges, particularly in developing regions where infrastructure and technical expertise remain limited.

The growing adoption of next-generation sequencing in clinical diagnostics presents significant opportunities, particularly in early disease detection and preventive healthcare. Sequencing technologies are increasingly used for non-invasive prenatal testing, cancer screening, and infectious disease surveillance, with diagnostic applications accounting for a rapidly expanding share of total usage. Advances in portable sequencing devices and automation are enabling point-of-care genomic testing, improving accessibility in remote and underserved regions. Additionally, government-backed genome projects and precision medicine initiatives are creating large-scale opportunities for sequencing providers, while partnerships between healthcare institutions and technology companies are accelerating innovation and market penetration.

The exponential growth of genomic data generated by next-generation sequencing presents significant challenges in storage, analysis, and regulatory compliance. A single human genome sequence can generate over 100 gigabytes of raw data, requiring advanced storage infrastructure and secure data management systems. Ensuring data privacy and compliance with evolving regulatory frameworks adds further complexity, particularly in regions with stringent data protection laws. Additionally, standardization of sequencing protocols and interpretation guidelines remains inconsistent across markets, creating barriers to interoperability. These challenges necessitate continuous investment in bioinformatics, cybersecurity, and regulatory alignment to support sustainable market growth.

• Accelerated Cost Reduction and High-Throughput Efficiency Gains: Sequencing costs have declined by over 60% in the past decade, with whole genome sequencing now achievable for under USD 600 in high-volume laboratories. Modern high-throughput platforms can process more than 20,000 samples annually per system, representing a 45% improvement in operational efficiency. This significant reduction in cost per genome is enabling broader clinical adoption, with over 70% of large diagnostic labs integrating cost-optimized sequencing workflows to enhance scalability and patient access.

• Integration of Artificial Intelligence in Genomic Data Analysis: AI-driven bioinformatics tools are improving genomic data interpretation speed by nearly 40%, reducing manual analysis time from days to hours. Approximately 65% of advanced sequencing facilities now use machine learning algorithms to detect genetic variants with up to 30% higher accuracy compared to traditional computational methods. These AI integrations are also reducing error rates in sequencing outputs by 25%, significantly enhancing diagnostic reliability in oncology and rare disease applications.

• Expansion of Clinical Diagnostics and Population Genomics Programs: Clinical applications now account for over 55% of sequencing usage, driven by increasing adoption in cancer diagnostics, prenatal testing, and infectious disease surveillance. Large-scale population genomics initiatives are sequencing millions of genomes, with some national programs targeting over 1 million participants. This expansion has improved early disease detection rates by approximately 35% and reduced diagnostic turnaround times by 40%, reinforcing the role of sequencing in preventive healthcare strategies.

• Growth in Portable and Real-Time Sequencing Technologies: Portable sequencing devices have witnessed adoption growth of over 50% in the last five years, particularly in field-based diagnostics and remote healthcare settings. Real-time sequencing solutions can deliver actionable genomic insights within 6–12 hours, compared to 48–72 hours with conventional methods. These advancements are driving adoption in emergency response scenarios and infectious disease outbreaks, where rapid genomic analysis improves containment efficiency by up to 30%.

The next-generation sequencing market is segmented across types, applications, and end-user categories, each contributing uniquely to overall market expansion. By type, sequencing technologies such as sequencing by synthesis, ion semiconductor sequencing, and single-molecule real-time sequencing dominate due to their varying throughput and accuracy capabilities. In terms of application, clinical diagnostics represents the largest segment, accounting for over 50% of total usage, followed by research applications in genomics and drug discovery. End-user segmentation highlights hospitals, research institutes, and pharmaceutical companies as primary adopters, collectively contributing more than 70% of total demand. Increasing integration of sequencing technologies across precision medicine, agriculture, and environmental studies is further diversifying market opportunities and expanding adoption globally.

The next-generation sequencing market by type is primarily segmented into sequencing by synthesis (SBS), ion semiconductor sequencing, single-molecule real-time (SMRT) sequencing, and nanopore sequencing technologies. Sequencing by synthesis leads the segment, accounting for approximately 48% of total adoption due to its high accuracy, scalability, and compatibility with large-scale genomic projects. Ion semiconductor sequencing holds around 22% share, offering faster turnaround times and lower operational complexity, particularly in clinical diagnostics.

Single-molecule real-time sequencing is the fastest-growing segment, expanding at an estimated CAGR of 17.8%, driven by its ability to produce longer read lengths exceeding 10,000 base pairs, which improves structural variant detection by nearly 35%. Nanopore sequencing is also gaining traction, contributing to nearly 15% of the market, especially in portable and real-time sequencing applications. The remaining technologies collectively account for about 15%, serving niche research and specialized genomic analysis needs.

The application landscape of the next-generation sequencing market is dominated by clinical diagnostics, research and development, drug discovery, and agricultural genomics. Clinical diagnostics leads with a share of approximately 52%, driven by increasing adoption in oncology, prenatal screening, and infectious disease testing. Research and development accounts for nearly 28% of applications, supporting genomic studies, biomarker discovery, and evolutionary biology research.

Drug discovery is the fastest-growing application segment, expanding at an estimated CAGR of 16.5%, as pharmaceutical companies increasingly rely on genomic insights to identify novel drug targets and reduce development timelines by up to 30%. Agricultural genomics contributes around 10%, focusing on crop improvement and livestock genetics, while other applications collectively hold about 10% share.

The next-generation sequencing market by end-user is segmented into hospitals and clinical laboratories, research institutes, pharmaceutical and biotechnology companies, and others. Hospitals and clinical laboratories dominate the segment with approximately 46% share, driven by the increasing use of sequencing in diagnostics and personalized medicine. Research institutes account for around 27%, focusing on large-scale genomic studies and innovation in sequencing technologies.

Pharmaceutical and biotechnology companies represent the fastest-growing end-user segment, expanding at an estimated CAGR of 15.9%, fueled by the integration of sequencing in drug discovery pipelines and clinical trials, where genomic data improves success rates by nearly 25%. Other end-users, including academic institutions and agricultural organizations, collectively contribute about 27% of the market, supporting diverse applications from education to environmental genomics.

Region North America accounted for the largest market share at 41% in 2025 however, Region Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 16.8% between 2026 and 2033.

North America processed over 45 million sequencing samples annually, supported by more than 500 advanced genomic laboratories and over 70% adoption in clinical diagnostics. Europe held approximately 27% share, driven by over 200 national genomics programs and increasing regulatory frameworks for precision medicine. Asia-Pacific accounted for nearly 22% of the market, with China and Japan contributing over 60% of regional sequencing volume and India witnessing a 35% rise in genomic testing adoption. South America represented around 6%, led by Brazil with over 120 sequencing facilities, while the Middle East & Africa held close to 4%, with UAE and South Africa investing heavily in genomic infrastructure, increasing regional sequencing capacity by over 30% in the last five years.

North America dominates the next-generation sequencing market with an estimated 41% share, driven by strong demand from healthcare, pharmaceuticals, and biotechnology industries. Over 75% of hospitals and diagnostic labs have integrated sequencing technologies into clinical workflows, particularly in oncology and rare disease diagnostics. Government initiatives supporting precision medicine and genomic research have resulted in more than 300 active genome projects. Regulatory frameworks emphasize data security and patient privacy, with over 80% compliance adoption across institutions. Technological advancements such as AI-integrated sequencing platforms have improved data processing efficiency by 40%. A key regional player has expanded automated sequencing systems capable of processing over 10,000 samples per week, enhancing scalability. Consumer behavior reflects high adoption in healthcare and research sectors, with over 65% enterprise utilization across clinical applications.

Europe holds approximately 27% of the next-generation sequencing market, led by Germany, the UK, and France, which collectively contribute over 60% of regional demand. The region emphasizes strict regulatory compliance, with over 70% of sequencing labs adhering to standardized genomic data governance policies. Sustainability initiatives have reduced laboratory waste by nearly 20%, aligning with environmental goals. Adoption of advanced sequencing technologies, including single-cell and long-read sequencing, has increased by 35% across research institutions. A leading regional genomics organization has implemented large-scale sequencing programs covering more than 500,000 participants, significantly enhancing population genomics research. Consumer behavior in the region shows a strong preference for explainable and compliant sequencing solutions, with over 55% of organizations prioritizing transparency in genomic data analysis.

Asia-Pacific ranks as the fastest-growing region in the next-generation sequencing market, accounting for nearly 22% of global volume. China, Japan, and India are the top consuming countries, contributing over 70% of regional sequencing demand. Infrastructure expansion has led to the establishment of more than 300 new sequencing laboratories in the past five years. Government-backed genome projects have increased sequencing adoption by 40%, while advancements in cost-efficient technologies have reduced sequencing costs by 30%. A major regional player has deployed high-throughput sequencing systems capable of analyzing over 1 million genomes annually, significantly boosting research output. Consumer behavior reflects strong growth in healthcare and research sectors, with increasing adoption driven by mobile health applications and digital diagnostics platforms.

South America accounts for approximately 6% of the next-generation sequencing market, with Brazil and Argentina leading regional adoption. Brazil alone contributes over 50% of the regional sequencing volume, supported by expanding healthcare infrastructure and research initiatives. Government incentives promoting biotechnology and genomic research have increased investment by nearly 25% over recent years. Infrastructure improvements, including the establishment of over 100 sequencing facilities, have enhanced regional capabilities. A regional genomics institute has implemented sequencing programs for infectious disease monitoring, processing over 500,000 samples annually. Consumer behavior shows rising demand for diagnostic applications, particularly in urban healthcare systems, where adoption rates have increased by 30%.

The Middle East & Africa region holds around 4% of the next-generation sequencing market, with UAE and South Africa emerging as key growth countries. Demand is driven by healthcare modernization and investments in advanced diagnostic technologies, with regional sequencing capacity increasing by over 30% in recent years. Governments are forming strategic partnerships to enhance genomic research infrastructure, with more than 50 collaborative projects launched across the region. Technological modernization includes the adoption of cloud-based genomic platforms, improving data processing efficiency by 35%. A regional healthcare initiative has deployed sequencing technologies across multiple hospitals, enabling analysis of over 200,000 samples annually. Consumer behavior reflects increasing interest in precision medicine, particularly in urban centers with advanced healthcare facilities.

United States – 38% share in the Next-Generation Sequencing market, driven by advanced research infrastructure and high clinical adoption rates.

China – 21% share in the Next-Generation Sequencing market, supported by large-scale genome projects and strong government investment in biotechnology.

The next-generation sequencing market is moderately consolidated, with over 25 active global competitors and a strong presence of regional players. The top five companies collectively account for approximately 68% of the total market share, reflecting a competitive yet innovation-driven landscape. Leading players are focusing on strategic partnerships, product innovation, and geographic expansion to strengthen their market positions. Over 40 new sequencing platforms and upgrades have been launched in the past three years, enhancing throughput and reducing operational complexity by up to 35%.

Mergers and acquisitions remain a key strategy, with more than 15 significant deals completed recently to expand technological capabilities and product portfolios. Companies are investing heavily in AI integration and cloud-based genomic solutions, improving data analysis efficiency by nearly 40%. Additionally, collaborations between sequencing companies and healthcare institutions have increased by over 30%, accelerating clinical adoption. The market is characterized by continuous innovation, with over 60% of companies focusing on developing next-generation platforms with improved accuracy and reduced turnaround times, ensuring sustained competitive intensity.

Illumina, Inc.

Thermo Fisher Scientific Inc.

BGI Group

Agilent Technologies, Inc.

Pacific Biosciences of California, Inc.

Oxford Nanopore Technologies plc

QIAGEN N.V.

PerkinElmer, Inc.

F. Hoffmann-La Roche Ltd

Eurofins Scientific

Illumina, Inc.

Thermo Fisher Scientific Inc.

Oxford Nanopore Technologies plc

The next-generation sequencing market is undergoing rapid technological transformation driven by innovations in sequencing chemistry, automation, and computational genomics. High-throughput sequencing platforms now achieve read outputs exceeding 6 terabases per run, enabling large-scale genomic projects to process thousands of samples simultaneously. Sequencing by synthesis technology continues to dominate due to its accuracy levels exceeding 99.9%, while advancements in reagent chemistry have reduced error rates by nearly 20% over the past five years.

Long-read sequencing technologies, including single-molecule real-time and nanopore sequencing, are gaining traction for their ability to generate reads longer than 10,000 base pairs, significantly improving structural variant detection and genome assembly. These technologies have demonstrated up to 30% higher accuracy in identifying complex genomic regions compared to short-read methods. Additionally, portable sequencing devices are enabling real-time genomic analysis, delivering results within 6–12 hours, which is critical for infectious disease monitoring and field-based diagnostics.

Automation and robotics are transforming laboratory workflows, with automated sample preparation systems reducing manual handling time by over 50% and minimizing human error. Integration of artificial intelligence and machine learning algorithms into bioinformatics pipelines is further enhancing data analysis efficiency by approximately 40%, enabling faster interpretation of large genomic datasets. Cloud-based genomic platforms now support storage and processing of datasets exceeding 100 terabytes, ensuring scalability and remote accessibility for research institutions and clinical laboratories.

Emerging technologies such as single-cell sequencing and spatial transcriptomics are expanding the scope of genomic analysis, allowing researchers to study gene expression at cellular resolution. Single-cell sequencing adoption has increased by more than 35% in research applications, while spatial genomics is improving tissue-level analysis accuracy by nearly 25%. These advancements are positioning next-generation sequencing as a cornerstone technology in precision medicine, drug discovery, and population genomics initiatives.

• In January 2025, Illumina, Inc. launched the NovaSeq X Series upgrades, enhancing throughput capacity by over 20% and reducing sequencing turnaround time by nearly 25%, enabling large-scale genomic projects to process up to 20,000 genomes annually with improved energy efficiency. Source: www.illumina.com

• In March 2025, Oxford Nanopore Technologies introduced an advanced nanopore sequencing chemistry update that improved raw read accuracy to over 99%, marking a significant milestone in long-read sequencing reliability and expanding its application in clinical-grade genomic analysis.

• In September 2024, Pacific Biosciences of California, Inc. expanded its Revio sequencing system deployment across global research centers, enabling high-fidelity long-read sequencing with accuracy improvements of approximately 15% and supporting large-scale genome assembly projects exceeding 1,000 samples per month. Source: www.pacb.com

• In November 2024, Thermo Fisher Scientific Inc. enhanced its Ion Torrent sequencing platform with upgraded semiconductor chips, increasing sequencing speed by 30% and enabling more efficient targeted sequencing workflows for oncology and infectious disease diagnostics. Source: www.thermofisher.com

The Next-Generation Sequencing Market Report provides a comprehensive evaluation of the global landscape, covering a wide spectrum of technologies, applications, and end-user segments. The report analyzes key sequencing technologies, including sequencing by synthesis, ion semiconductor sequencing, and long-read sequencing platforms, which collectively account for over 80% of total industry adoption. It also examines emerging innovations such as single-cell sequencing and spatial genomics, which are expanding research capabilities and contributing to more than 25% growth in advanced genomic applications.

From an application perspective, the report encompasses clinical diagnostics, research and development, drug discovery, and agricultural genomics. Clinical diagnostics remains the largest application segment, accounting for over 50% of total usage, while research applications contribute significantly to innovation pipelines. The report also explores niche segments such as microbiome analysis and environmental genomics, which are gaining traction with adoption rates increasing by over 20% annually in specialized research domains.

Geographically, the report provides in-depth insights across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, collectively representing 100% of global market activity. It highlights regional variations in sequencing infrastructure, with North America hosting over 40% of global sequencing facilities, while Asia-Pacific demonstrates the fastest expansion in laboratory capacity, with over 300 new facilities established in recent years.

The scope further includes analysis of end-user industries such as hospitals, research institutes, and pharmaceutical companies, which together account for more than 70% of total demand. Additionally, the report evaluates regulatory frameworks, technological advancements, and investment trends shaping the market, offering a holistic view for decision-makers seeking to understand current dynamics and future growth opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

14.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Illumina, Inc., Thermo Fisher Scientific Inc., BGI Group, Agilent Technologies, Inc., Pacific Biosciences of California, Inc., Oxford Nanopore Technologies plc, QIAGEN N.V., PerkinElmer, Inc., F. Hoffmann-La Roche Ltd, Eurofins Scientific, Illumina, Inc., Thermo Fisher Scientific Inc., Oxford Nanopore Technologies plc |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |