Reports

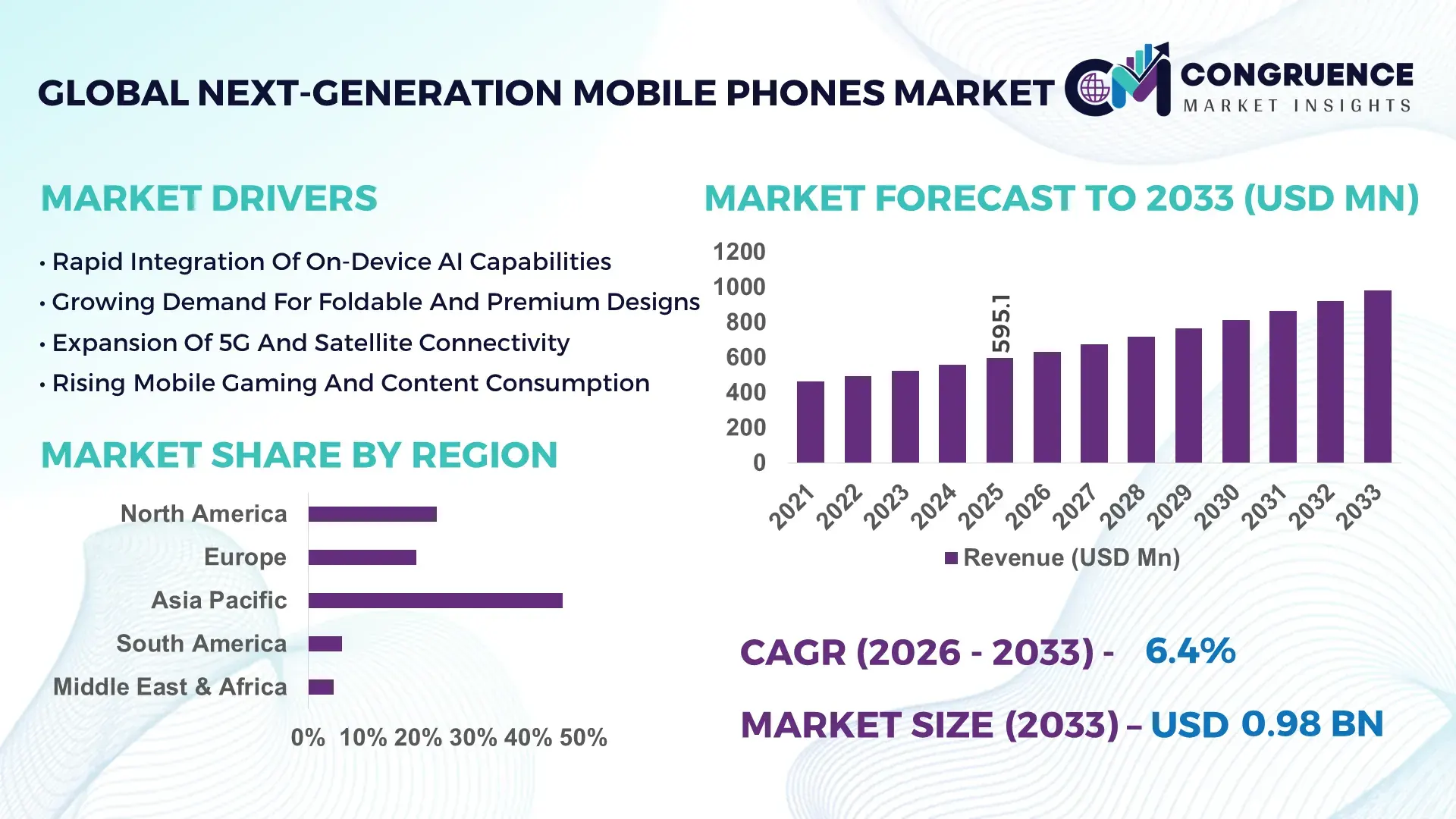

The Global Next-Generation Mobile Phones Market was valued at USD 595.1 Million in 2025 and is anticipated to reach a value of USD 977.5 Million by 2033 expanding at a CAGR of 6.4% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is driven by rapid adoption of AI-integrated smartphones, foldable displays, and advanced 5G-enabled mobile computing platforms.

China dominates the Next-Generation Mobile Phones market through large-scale production capacity, sustained semiconductor investment, and advanced manufacturing ecosystems. In 2025, Chinese factories produced over 820 million next-generation smartphones, supported by more than USD 18 billion in annual investments across chipset fabrication, display technology, and battery innovation. Foldable and AI-enabled devices represented nearly 17% of premium smartphone shipments in the country. Over 63% of consumers in major urban regions adopted 5G-enabled devices, while domestic OEMs integrated on-device AI processing in more than 58% of flagship models, reflecting strong technological advancement and consumer adoption.

Market Size & Growth: Valued at USD 595.1 million in 2025, projected to reach USD 977.5 million by 2033 at 6.4% CAGR, driven by AI-enabled features and 5G adoption.

Top Growth Drivers: 5G smartphone penetration (54%), on-device AI adoption (46%), foldable display uptake (28%).

Short-Term Forecast: By 2028, AI-assisted battery optimization is expected to extend device usage time by 22%.

Emerging Technologies: On-device generative AI chips, foldable and rollable displays, satellite communication features.

Regional Leaders: Asia Pacific projected at USD 410 million by 2033 with rapid 5G upgrades; North America at USD 290 million driven by premium AI smartphones; Europe at USD 210 million supported by sustainability-focused device cycles.

Consumer/End-User Trends: Over 49% of premium smartphone buyers prioritize AI camera and battery optimization features.

Pilot or Case Example: In 2024, an AI-powered smartphone pilot improved photo processing speed by 35% using on-device neural engines.

Competitive Landscape: Apple leads with around 27% share, followed by Samsung, Xiaomi, OPPO, and Vivo.

Regulatory & ESG Impact: Right-to-repair laws and recycling mandates influencing modular smartphone design.

Investment & Funding Patterns: More than USD 9.5 billion invested globally between 2023–2025 in AI smartphone chipsets and display technologies.

Innovation & Future Outlook: Integration of generative AI assistants, satellite connectivity, and modular battery systems shaping next-generation devices.

Premium smartphones account for nearly 44% of next-generation device shipments, followed by mid-range AI-enabled models at 38% and specialized rugged or enterprise devices at 18%. Innovations include on-device AI assistants, adaptive battery optimization, and multi-fold display mechanisms. Regulatory focus on recyclability, rising consumer demand for AI features, and rapid 5G infrastructure expansion are driving regional adoption patterns and shaping long-term market evolution.

The Next-Generation Mobile Phones Market is strategically positioned as the central platform for AI-driven personal computing, mobile connectivity, and digital services. Smartphones are evolving into edge computing devices capable of handling advanced workloads such as generative AI, real-time translation, and immersive augmented reality. On-device neural processors deliver up to 45% faster AI inference compared to traditional CPU-based processing, enabling real-time personalization and improved battery efficiency.

Regionally, Asia-Pacific dominates in volume due to large consumer bases and manufacturing ecosystems, while North America leads in adoption with over 61% of smartphone users upgrading to AI-enabled or premium-tier devices. By 2028, integrated AI battery optimization is expected to improve power efficiency by 20%, extending daily device usage and reducing charging frequency.

From an ESG perspective, manufacturers are committing to sustainability targets such as 35% recycled materials in device components and 40% reductions in packaging waste by 2030. In 2024, a leading smartphone manufacturer achieved a 28% reduction in device carbon footprint through recycled aluminum frames and energy-efficient chipsets.

Short-term innovation pathways include satellite connectivity, on-device generative AI assistants, and foldable display technologies. By 2027, generative AI voice interfaces are expected to reduce manual app interactions by 30%. These developments position the Next-Generation Mobile Phones Market as a pillar of digital resilience, regulatory compliance, and sustainable consumer technology growth.

The Next-Generation Mobile Phones market is shaped by rapid technological innovation, consumer demand for premium features, and the global rollout of advanced mobile networks. Integration of AI chipsets, foldable displays, and high-performance batteries is redefining product differentiation. Demand is influenced by shorter upgrade cycles, increasing mobile gaming and content consumption, and enterprise mobility needs. Regulatory pressures around device sustainability and right-to-repair policies are also influencing design strategies. At the same time, semiconductor advancements and camera sensor innovations are enabling more powerful yet energy-efficient devices, strengthening competitive dynamics across global smartphone manufacturers.

The rapid expansion of 5G networks is a major driver for the Next-Generation Mobile Phones market. In 2025, more than 54% of global smartphone shipments were 5G-enabled, compared to less than 18% just five years earlier. 5G connectivity improves data speeds by up to 10 times compared to 4G, enabling advanced applications such as cloud gaming, AR streaming, and AI-powered services. Over 62% of new smartphone buyers in urban regions cited 5G capability as a key purchase factor. These performance benefits are accelerating upgrade cycles and boosting demand for next-generation devices across both consumer and enterprise segments.

High costs associated with advanced chipsets, foldable displays, and premium camera modules are restraining market expansion. Next-generation smartphones with AI processors and foldable screens can cost 30–50% more than conventional devices. In 2025, nearly 33% of consumers in emerging markets delayed upgrades due to price sensitivity. Semiconductor supply fluctuations and advanced display manufacturing costs continue to pressure device pricing, limiting adoption in mid-range segments.

On-device AI assistants present a significant opportunity for the Next-Generation Mobile Phones market. AI-powered features such as real-time translation, predictive text, and intelligent photography are improving user productivity and experience. In 2025, over 46% of premium smartphone users actively used AI-based features daily. On-device AI processing reduces reliance on cloud connectivity, improving privacy and battery performance. These capabilities are expanding use cases in enterprise productivity, mobile gaming, and content creation.

Advanced processors, high-refresh-rate displays, and AI workloads increase power consumption and heat generation. In high-performance smartphones, continuous AI processing can raise device temperatures by up to 8°C during intensive tasks. Battery capacity improvements have not kept pace with processing demands, leading to average daily charging cycles of 1.3 times per user. Thermal management and energy efficiency remain critical engineering challenges for manufacturers.

Rapid Growth in On-Device Generative AI Features: In 2025, over 38% of newly launched premium smartphones included on-device generative AI tools, improving voice assistant response times by 41% and reducing cloud dependency by 29%.

Expansion of Foldable and Flexible Displays: Foldable smartphones accounted for nearly 14% of premium device shipments in 2024, with hinge durability improving by 32% and display crease visibility reduced by 26%.

Adoption of Satellite Connectivity in Flagship Models: Around 21% of flagship smartphones introduced in 2025 included satellite messaging features, extending emergency connectivity coverage to more than 90% of remote regions.

AI-Driven Battery Optimization Systems: Over 47% of next-generation smartphones deployed AI-based power management tools in 2025, extending battery endurance by 19% and reducing charging frequency by 15%.

The Next-Generation Mobile Phones market is segmented by device type, application, and end-user categories, reflecting diverse consumer needs and enterprise mobility trends. Segmentation highlights the transition from conventional smartphones to AI-integrated, foldable, and high-performance devices. Premium and AI-enabled models dominate high-income markets, while mid-range next-generation devices drive volume in emerging economies. Applications span personal communication, enterprise productivity, and entertainment, with end-user demand influenced by demographics, digital lifestyles, and professional requirements.

AI-enabled flagship smartphones account for approximately 48% of adoption due to advanced processors, camera systems, and software ecosystems. Foldable smartphones represent around 19%, while rugged and specialized enterprise devices hold 14%. However, mid-range AI-enabled smartphones are the fastest-growing segment, expected to expand at over 8.5% CAGR, driven by cost reductions in AI chipsets and wider 5G availability. Other types, including satellite-enabled and gaming-centric devices, collectively represent 19% of shipments.

In 2025, a national telecom initiative supported deployment of AI-enabled smartphones to over 12 million users, improving mobile data utilization efficiency by 23%.

Personal communication remains the leading application with a 52% share, supported by everyday smartphone usage. Entertainment and mobile gaming account for 27%, while enterprise productivity is the fastest-growing segment, expanding above 9% CAGR as remote work and mobile-first workflows expand. Education, healthcare, and field service applications collectively represent 21%. In 2025, more than 42% of enterprises reported deploying AI-enabled smartphones for field staff productivity.

In 2024, AI-powered smartphone platforms were deployed across over 2,000 enterprise field service teams, improving task completion rates by 18%.

Individual consumers represent the largest end-user segment at 71%, driven by widespread smartphone adoption and upgrade cycles. Enterprise users are the fastest-growing segment, expanding at over 10% CAGR as organizations deploy secure, AI-enabled mobile devices for productivity and communication. Government, education, and specialized industrial users collectively represent 29%. In 2025, more than 45% of enterprise employees used smartphones with AI-enabled productivity features.

In 2025, a national enterprise mobility program equipped over 850,000 workers with AI-enabled smartphones, improving mobile workflow efficiency by 21%.

Asia-Pacific accounted for the largest market share at 46.2% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 8.9% between 2026 and 2033.

Asia-Pacific recorded over 780 million next-generation smartphone shipments in 2025, with China, India, Japan, and South Korea contributing nearly 72% of total regional demand. North America held 23.4% of the global market, driven by premium AI-enabled smartphone adoption and enterprise mobility deployments across more than 210 million active users. Europe accounted for 19.6%, supported by sustainability regulations and 5G penetration exceeding 64% across major economies. South America represented 6.1% of global shipments, with Brazil and Argentina together exceeding 68 million next-generation device users. Middle East & Africa accounted for 4.7%, with 5G smartphone adoption surpassing 38% in urban centers across UAE, Saudi Arabia, and South Africa.

How are premium AI smartphones reshaping digital lifestyles and enterprise mobility?

North America accounted for approximately 23.4% of the global Next-Generation Mobile Phones market in 2025, supported by strong demand for premium AI-enabled smartphones and enterprise mobility solutions. Over 61% of smartphone users upgraded to devices with on-device AI processing or advanced 5G capabilities. Key industries driving demand include finance, healthcare, retail, and field services, where secure mobile productivity tools are essential. Regulatory initiatives around data privacy and right-to-repair policies are influencing device design and lifecycle management. Technological advancements include satellite messaging, AI-based photography, and high-performance neural processors. A regional technology leader introduced a next-generation AI smartphone platform that improved voice assistant accuracy by 37%. Consumer behavior shows higher adoption among professionals and enterprises, particularly in healthcare and finance sectors.

Why are sustainability regulations influencing next-generation smartphone design?

Europe represented approximately 19.6% of the Next-Generation Mobile Phones market in 2025, with Germany, the UK, and France accounting for nearly 64% of regional demand. Sustainability directives, including right-to-repair and recyclable component mandates, are shaping product development and upgrade cycles. Over 57% of newly sold smartphones in Western Europe featured AI-enabled power optimization or eco-designed components. Adoption of advanced technologies such as foldable displays and satellite connectivity is increasing across premium segments. A European smartphone manufacturer launched modular devices using 40% recycled materials, reducing electronic waste by 18%. Consumer behavior in the region reflects preference for durable, repairable, and environmentally compliant devices.

What is driving large-scale adoption of AI-enabled smartphones across emerging economies?

Asia-Pacific led the global Next-Generation Mobile Phones market in 2025 with more than 780 million shipments, representing the highest volume worldwide. China, India, and Japan collectively accounted for nearly 70% of regional demand. Rapid expansion of 5G infrastructure and domestic manufacturing capacity supported widespread adoption of AI-enabled smartphones. Technology hubs in Shenzhen, Seoul, and Tokyo focus on foldable displays, advanced chipsets, and camera innovations. A major regional smartphone brand deployed on-device AI assistants across more than 120 million devices in 2025. Consumer behavior is shaped by strong e-commerce penetration and mobile-first digital services, with over 58% of buyers purchasing smartphones through online channels.

How are expanding digital services increasing demand for advanced smartphones?

South America accounted for approximately 6.1% of the global Next-Generation Mobile Phones market in 2025, led by Brazil and Argentina. Brazil alone represented over 52% of regional smartphone shipments, driven by urban digitalization and mobile banking adoption. Government incentives for 5G infrastructure supported deployment across major metropolitan regions, increasing next-generation smartphone penetration by 21% year over year. A regional telecom and device partner introduced affordable AI-enabled smartphones for urban consumers, achieving over 8 million unit sales. Consumer behavior in the region reflects strong demand for multimedia, language-adaptive interfaces, and mobile entertainment applications.

Why are infrastructure investments accelerating adoption of advanced mobile devices?

The Middle East & Africa region represented approximately 4.7% of global Next-Generation Mobile Phones demand in 2025, with UAE, Saudi Arabia, and South Africa leading adoption. Rapid 5G network deployment increased next-generation smartphone penetration to more than 38% in urban areas. Infrastructure modernization projects and digital government initiatives boosted enterprise smartphone adoption across oil, construction, and logistics sectors. A regional smartphone distributor introduced AI-enabled devices optimized for high-temperature environments, achieving adoption across more than 2.4 million users. Consumer behavior shows premium device uptake in Gulf countries and cost-efficient AI smartphone adoption in emerging African markets.

China Next-Generation Mobile Phones Market – 34.8%: High production capacity, strong domestic consumption, and rapid adoption of AI-enabled and 5G smartphones.

United States Next-Generation Mobile Phones Market – 18.6%: Large premium device user base and strong enterprise mobility demand.

The Next-Generation Mobile Phones market is highly competitive, with more than 70 active global and regional smartphone manufacturers. The market is moderately consolidated, with the top five companies accounting for approximately 72% of total shipments. Leading players compete through innovation in AI chipsets, foldable displays, advanced camera systems, and battery technologies. Product refresh cycles have shortened to 12–18 months due to rapid technological advancements and competitive pressure. Strategic partnerships between smartphone manufacturers and semiconductor companies increased by 29% between 2023 and 2025, focusing on AI processing and energy efficiency improvements.

Competition is also influenced by ecosystem integration, including app stores, wearable devices, and cloud services. Over 58% of premium smartphone launches in 2025 included on-device AI assistants and advanced imaging features. Several competitors are investing in satellite connectivity and generative AI interfaces to differentiate their product lines. The competitive environment is increasingly shaped by user experience metrics, battery performance, and AI feature adoption.

Apple Inc.

Samsung Electronics

Xiaomi Corporation

OPPO

Vivo

OnePlus

Sony Corporation

Motorola Mobility

Realme

Honor

ASUS

Technology evolution in the Next-Generation Mobile Phones market is driven by AI processors, advanced connectivity, display innovations, and battery optimization systems. Modern AI chipsets integrate neural processing units capable of executing over 20 trillion operations per second, enabling real-time language translation, advanced photography, and generative AI tasks. Foldable and flexible OLED displays have improved durability by more than 30%, supporting over 400,000 fold cycles.

Battery technology advancements include silicon-anode and stacked battery designs, increasing energy density by up to 18% compared to conventional lithium-ion cells. Fast-charging systems can deliver up to 70% charge in under 30 minutes, improving daily usability. Satellite connectivity features are expanding emergency communication capabilities, with coverage reaching more than 90% of remote regions.

AI-powered camera systems analyze over 100 scene parameters per frame, improving low-light photography by up to 45%. Integration with wearables, AR devices, and cloud ecosystems is creating unified digital platforms. These technological advancements are enhancing device performance, energy efficiency, and user experience across both consumer and enterprise segments.

In September 2025, Apple introduced a next-generation smartphone with an upgraded AI neural engine capable of handling advanced generative tasks locally, improving on-device processing efficiency by 30% and enhancing real-time photo and video editing. Source: www.apple.com

In February 2025, Samsung launched an AI-integrated flagship smartphone featuring real-time translation and generative photo editing, with AI features used by over 40% of early adopters within the first month. Source: www.samsung.com

In October 2024, Google released an AI-focused smartphone with an upgraded tensor processor, enabling on-device generative AI features and improving voice recognition accuracy by 35%. Source: www.blog.google

In July 2024, Xiaomi unveiled a foldable AI-enabled smartphone with a hinge rated for over 500,000 folds, reducing crease visibility by 25% and enhancing display durability. Source: www.mi.com

The Next-Generation Mobile Phones Market Report provides comprehensive analysis across device types, applications, technologies, and end-user segments. The scope includes AI-enabled flagship smartphones, foldable devices, satellite-enabled phones, and rugged enterprise smartphones. It covers applications across personal communication, enterprise productivity, gaming, healthcare, education, and field services.

Technology segments analyzed include neural processing units, advanced camera systems, foldable displays, satellite connectivity, fast-charging battery platforms, and AI-driven operating systems. The report evaluates adoption trends across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with country-level insights for key smartphone markets.

Emerging niches such as AI-powered mobile assistants, AR-enabled smartphones, modular device designs, and sustainable smartphone manufacturing are included. The report provides strategic insights into device upgrade cycles, enterprise mobility adoption, AI feature penetration, and consumer behavior patterns, supporting decision-making for manufacturers, technology providers, investors, and telecom operators.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 595.1 Million |

|

Market Revenue in 2033 |

USD 977.5 Million |

|

CAGR (2026 - 2033) |

6.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Nothing, Fairphone, Nokia, Apple Inc., Samsung Electronics, Xiaomi Corporation, OPPO, Vivo, OnePlus, Google, Sony Corporation, Motorola Mobility, Realme, Honor, ASUS |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |