Reports

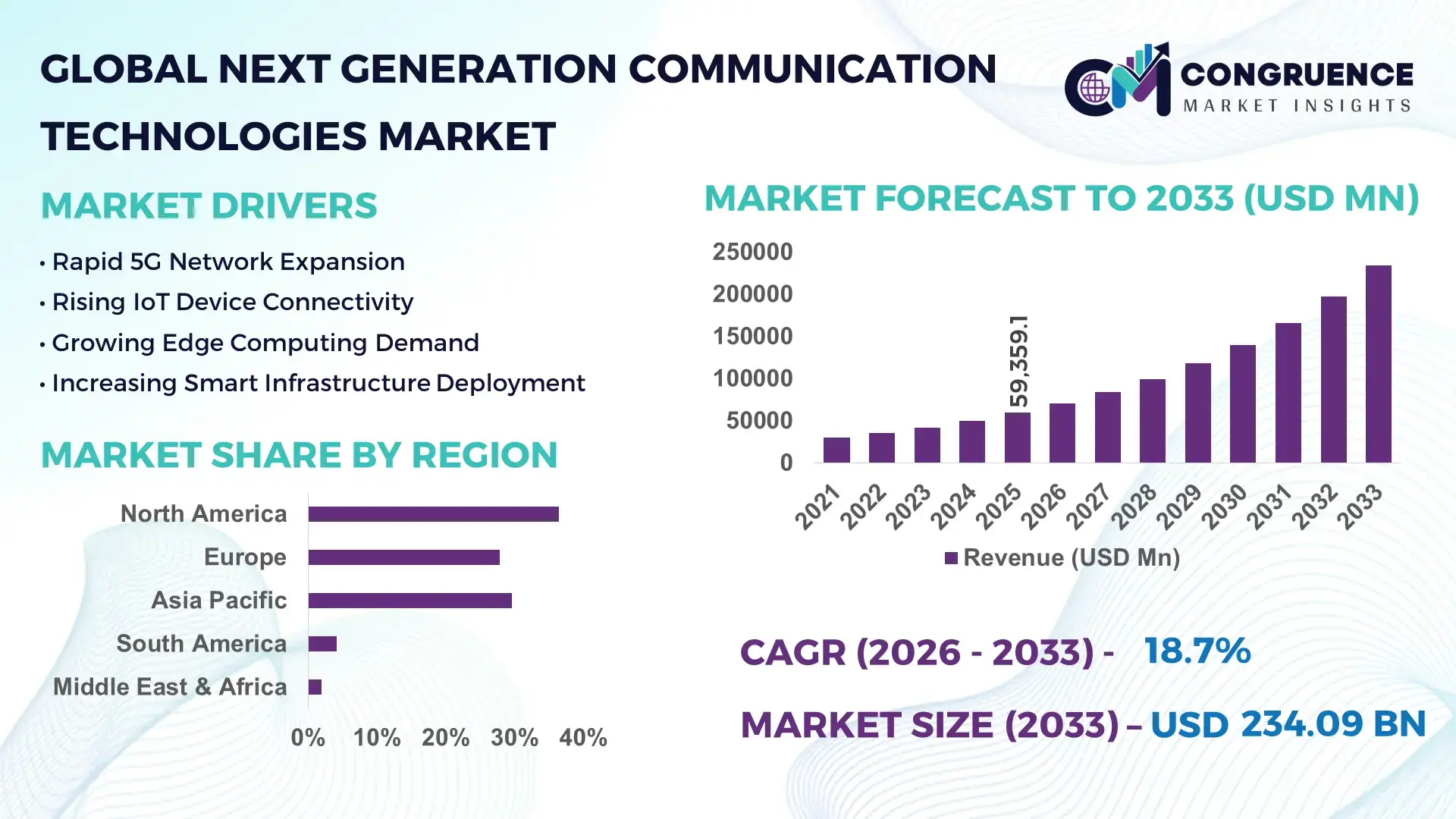

The Global Next Generation Communication Technologies Market was valued at USD 59,359.1 Million in 2025 and is anticipated to reach a value of USD 2,34,091.6 Million by 2033 expanding at a CAGR of 18.71% between 2026 and 2033. Rapid deployment of standalone 5G networks, AI-driven network automation, Open RAN adoption, satellite communication integration, and enterprise digital infrastructure modernization are accelerating next-generation communication technology implementation across industries.

The United States dominates the global market with approximately 34% share, supported by nationwide 5G expansion, AI-enabled telecom infrastructure, and multi-billion-dollar investments under the CHIPS and Science Act. The country operates one of the world's largest commercial 5G footprints, while China, with nearly 31% market share, leads in installed 5G base stations and industrial connectivity deployments across manufacturing, logistics, and smart cities, strengthening global technology leadership through large-scale infrastructure execution.

Organizations prioritizing scalable, secure, and software-defined communication ecosystems are positioned to strengthen digital resilience, operational efficiency, and long-term competitive advantage.

Market Size & Growth: USD 59,359.1 Million in 2025, reaching USD 2,34,091.6 Million by 2033 at 18.71% CAGR, driven by advanced 5G, AI-powered networking, and cloud-native infrastructure.

Top Growth Drivers: Standalone 5G adoption (+38%), AI-enabled network automation (+32%), and industrial IoT connectivity expansion (+29%).

Short-Term Forecast: By 2028, intelligent network operations are expected to reduce maintenance costs by 25% while improving service availability by 30%.

Emerging Technologies: AI-based network orchestration, Open RAN, edge computing, and satellite-terrestrial integration are reshaping global communication ecosystems.

Regional Leaders: North America (~USD 82 Billion), Asia-Pacific (~USD 76 Billion), and Europe (~USD 48 Billion) lead through telecom modernization, industrial digitization, and secure infrastructure deployment.

Consumer/End-User Trends: More than 68% of large enterprises are prioritizing private 5G and intelligent wireless connectivity for mission-critical operations.

Pilot/Case Example: In 2024, AI-enabled telecom network optimization improved spectrum efficiency by approximately 22% in large-scale commercial deployments.

Competitive Landscape: Leading vendors collectively hold nearly 46% market share, led by Huawei, Ericsson, Nokia, Cisco Systems, and Qualcomm.

Regulatory & ESG Impact: Energy-efficient network modernization lowers infrastructure power consumption by nearly 20%, supported by expanding digital infrastructure policies.

Investment & Funding: More than USD 55 Billion in annual infrastructure investments support Open RAN partnerships, fiber expansion, and advanced wireless deployments amid global supply-chain diversification.

Innovation & Future Outlook: AI-native networks, 6G research, integrated satellite connectivity, and autonomous network management are defining the next phase of high-growth communication infrastructure.

Next Generation Communication Technologies Market is rapidly expanding across smart manufacturing, autonomous transportation, healthcare connectivity, defense communications, and enterprise digital transformation. AI-native networking, Open RAN platforms, and integrated satellite communication solutions continue improving network flexibility and service quality. Nearly 60% of telecom operators are increasing investments in cloud-native architectures, while resilient semiconductor supply chains and evolving telecom regulations continue shaping deployment priorities, setting the foundation for broader strategic transformation.

Next Generation Communication Technologies have become a strategic foundation for digital economies as governments, telecom operators, manufacturers, and cloud providers modernize critical infrastructure. Infrastructure modernization, expanding edge computing, and increasing enterprise digital adoption are redefining competitive positioning across industries. Ongoing supply-chain restructuring and national digital infrastructure initiatives are encouraging regional manufacturing capacity, stronger cybersecurity frameworks, and greater network resilience.

Compared with traditional network architectures, AI-driven autonomous communication platforms reduce network management effort by nearly 35% while improving fault detection accuracy by approximately 40% through predictive analytics and intelligent automation. North America continues leading software-defined networking innovation and enterprise deployment, whereas Asia-Pacific excels in large-scale infrastructure rollout, industrial 5G implementation, and smart city integration. Over the next two to three years, private wireless deployments and intelligent edge infrastructure are expected to become standard across high-value industrial operations.

Telecom vendors are strengthening partnerships with cloud providers, semiconductor companies, and enterprise solution integrators to accelerate deployment speed and improve service flexibility. For example, manufacturers are integrating private 5G with automated production facilities to enable low-latency machine communication and real-time operational monitoring. Organizations investing early in AI-enabled, secure, and scalable communication ecosystems will establish stronger operational resilience, faster innovation cycles, and sustainable long-term competitive differentiation.

Enterprise migration toward AI-native communication infrastructure and software-defined networking is accelerating deployment of next-generation communication technologies across telecom, manufacturing, healthcare, and logistics. More than 68% of large enterprises are prioritizing private 5G deployment, while AI-driven network automation reduces operational intervention by nearly 35% and improves fault prediction accuracy by over 40%. The United States continues expanding digital infrastructure under national semiconductor and connectivity initiatives, encouraging telecom operators to modernize core networks. This structural shift improves spectrum utilization, network resilience, and application performance. In response, leading vendors are expanding Open RAN ecosystems, investing in cloud-native platforms, and forming strategic alliances with hyperscale cloud providers to deliver scalable, intelligent communication architectures. Companies integrating automation with edge intelligence are gaining faster deployment cycles and stronger enterprise customer retention.

Large-scale deployment remains constrained by high infrastructure modernization costs, fragmented network standards, and dependence on advanced semiconductor components. Upgrading legacy telecom infrastructure can increase capital expenditure by 25–35%, while nearly 30% of operators continue facing interoperability challenges between multi-vendor equipment. Semiconductor supply fluctuations and advanced chip manufacturing concentration continue affecting procurement timelines, particularly outside the United States and Taiwan. These structural constraints delay network rollouts, increase integration complexity, and reduce operational flexibility for smaller telecom providers. To mitigate exposure, communication technology companies are diversifying supplier networks, localizing equipment manufacturing, adopting virtualized network functions, and negotiating long-term procurement agreements that improve component availability while reducing deployment uncertainty.

Industrial digitalization is creating high-value opportunities beyond conventional telecom services through intelligent edge computing, autonomous operations, and mission-critical connectivity. More than 60% of industrial enterprises are increasing investments in edge-enabled communication platforms, while AI-assisted network optimization improves application response time by approximately 30%. India's expanding digital infrastructure initiatives and manufacturing modernization programs are accelerating adoption across factories, transportation networks, and smart utilities. The emergence of integrated non-terrestrial networks, private wireless ecosystems, and early 6G research is opening new commercial models for enterprise connectivity and low-latency services. Companies are strengthening R&D investments, building developer ecosystems, and partnering with industrial automation providers to create sector-specific communication platforms that generate recurring service revenue and operational differentiation.

Managing increasingly distributed communication ecosystems introduces significant execution complexity as AI, edge computing, cloud platforms, and connected devices operate simultaneously across multiple environments. Industry assessments indicate that connected endpoint volumes continue expanding by over 18% annually, while nearly 45% of telecom organizations identify cybersecurity resilience as a top operational priority. In Japan, advanced industrial automation requires ultra-reliable communication with minimal service interruption, making network resilience essential for production continuity. Integration across legacy infrastructure, cloud-native platforms, and multi-vendor environments increases configuration complexity and skilled workforce requirements. Companies must strengthen zero-trust security frameworks, invest in AI-powered threat detection, expand workforce capabilities, and establish collaborative cybersecurity partnerships to ensure long-term deployment consistency, operational reliability, and competitive differentiation.

AI-Native Network Automation Expands: Telecom operators are accelerating AI-driven network orchestration, with more than 65% of large operators deploying intelligent automation and nearly 35% reductions in manual network operations. The transition toward autonomous network management improves fault prediction, resource allocation, and service continuity. Following increasing network complexity and rising cybersecurity requirements, companies are expanding AI software partnerships and integrating machine learning into core network operations to improve efficiency and lower operating expenses.

Private 5G Industrial Adoption Accelerates: Industrial enterprises continue expanding private 5G deployments, with approximately 60% of large manufacturers increasing investment in dedicated wireless infrastructure and connected production environments. Smart factories report productivity improvements exceeding 25% through low-latency communication and real-time automation. Manufacturing modernization initiatives in Germany and Japan are encouraging vendors to scale industrial connectivity platforms through partnerships with automation providers and cloud infrastructure companies.

Satellite-Terrestrial Network Integration Grows: Hybrid communication architectures combining terrestrial and non-terrestrial networks are becoming mainstream for enterprise resilience. Satellite-enabled connectivity improves remote network availability by nearly 30%, while multi-network routing enhances service continuity by approximately 20% during infrastructure disruptions. Increasing digital inclusion programs and resilient communication requirements are driving operators to strengthen partnerships with satellite providers and integrate unified connectivity management platforms.

Open RAN Ecosystems Reshape Deployment: Open RAN adoption continues expanding as operators seek flexible multi-vendor environments and reduced infrastructure dependence. Open interfaces lower network integration costs by nearly 20% while shortening deployment cycles by approximately 18% through software-based architectures. Semiconductor supply-chain diversification and telecom infrastructure modernization are encouraging equipment manufacturers to expand interoperable product portfolios, strengthen ecosystem alliances, and accelerate cloud-native radio access deployments across enterprise and carrier networks.

AI-Driven Network & Software-Defined Networking (SDN) Solutions represent the leading segment because enterprises increasingly prioritize intelligent traffic management, automated network optimization, and software-defined infrastructure over traditional hardware-centric architectures. This segment accounts for an estimated 31% of technology adoption owing to its scalability, centralized management, and seamless cloud integration. Vendors continue embedding AI into network orchestration platforms to improve fault prediction, reduce manual intervention, and optimize bandwidth utilization. 5G Technologies remain the second-largest segment due to expanding standalone network deployments, while Optical Fiber & High-Speed Broadband Technologies continue supporting high-capacity backhaul infrastructure for enterprise and consumer connectivity. Satellite Communication Technologies (NTN) are emerging as the fastest-growing segment as governments and enterprises seek resilient communication across remote and underserved locations. Adoption of integrated satellite and terrestrial connectivity has increased by nearly 28%, while enterprise investment in hybrid communication platforms continues expanding. Wi-Fi 6 & Wi-Fi 6E strengthen indoor high-density networking, whereas Edge Computing Communication Platforms enable real-time industrial applications. Companies are responding through AI integration, Open RAN compatibility, and strategic partnerships that combine terrestrial, cloud, and satellite communication ecosystems.

Telecommunications remains the dominant application because network operators continue investing heavily in infrastructure modernization, intelligent network management, and advanced wireless connectivity. Approximately 36% of total deployments are concentrated within telecom operations, supported by nationwide 5G expansion, cloud-native core networks, and AI-driven service optimization. Operators increasingly integrate automation to reduce operational complexity while improving service quality. Smart Cities & Public Infrastructure and Consumer Electronics continue generating consistent demand as connected devices and intelligent urban infrastructure become operational priorities. Manufacturing & Industry 4.0 is the fastest-growing application segment as factories adopt private wireless networks, industrial IoT, and edge computing to support autonomous production. Industrial communication deployments have increased by nearly 30%, while low-latency wireless networks improve production efficiency by approximately 25%. Healthcare, Transportation & Logistics, Defense & Aerospace, and Energy & Utilities are also expanding through mission-critical communication requirements, remote monitoring, and intelligent operational control. Technology providers continue tailoring vertical-specific solutions, integrating AI analytics, and expanding ecosystem partnerships to strengthen industry-focused deployments.

Telecom Service Providers represent the largest end-user segment due to continuous investment in nationwide network expansion, spectrum utilization, and AI-enabled communication platforms. They account for approximately 39% of market demand as operators modernize infrastructure, deploy Open RAN architectures, and expand enterprise connectivity services. Large carriers continue strengthening partnerships with cloud providers and semiconductor companies to improve network flexibility and operational performance. Government & Public Sector organizations also remain significant buyers through digital infrastructure modernization and national connectivity initiatives. Enterprises are the fastest-growing end-user segment as organizations increasingly deploy private wireless networks, intelligent edge infrastructure, and cloud-native communication platforms. Enterprise adoption has expanded by nearly 32%, while AI-assisted network operations reduce infrastructure management effort by approximately 35%. Manufacturing Companies, Healthcare Organizations, Transportation & Logistics Companies, Energy & Utility Providers, and Defense & Security Organizations continue accelerating investment to improve operational resilience and real-time communication capabilities. Vendors are responding through customized industry platforms, managed connectivity services, flexible pricing models, and strategic ecosystem partnerships designed to support mission-critical digital transformation.

North America accounted for the largest market share at 36.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 20.4% CAGRbetween 2026 and 2033.

North America maintains the leading position through advanced telecom infrastructure, widespread standalone 5G deployment, cloud-native network transformation, and strong enterprise digitalization. The region contributes approximately 36.4% of global demand, supported by hyperscale cloud investments, AI-powered network automation, and extensive fiber modernization. More than 70% of large enterprises are evaluating or deploying private wireless networks to support industrial automation and mission-critical connectivity. Telecom operators continue expanding Open RAN deployments while strengthening partnerships with semiconductor and cloud providers. Government-backed digital infrastructure initiatives and cybersecurity investments further accelerate software-defined networking, edge computing integration, and intelligent communication ecosystem development across multiple industries.

United States Market Outlook: The United States remains the largest national market because of its advanced telecom ecosystem, semiconductor innovation, and enterprise technology adoption. Nationwide 5G expansion, AI-enabled network management, and extensive cloud infrastructure continue strengthening deployment capacity. More than 340 commercial 5G-enabled enterprise projects are actively supporting manufacturing, healthcare, logistics, and defense applications. Strong investment in AI networking, data centers, and secure communication platforms enables technology providers to commercialize next-generation communication solutions faster while supporting long-term digital infrastructure modernization.

Europe continues strengthening its market position through industrial automation, cybersecurity modernization, and coordinated digital infrastructure development. The region represents approximately 27.8% of global demand, driven by manufacturing digitization, private wireless deployments, and expanding fiber connectivity. Industrial enterprises increasingly integrate AI-enabled communication systems to improve production visibility and operational resilience. Open RAN collaboration and cross-border telecom modernization projects continue enhancing network interoperability while reducing infrastructure dependence. Sustainability-focused network upgrades and energy-efficient communication equipment are also becoming standard procurement priorities across enterprise and public-sector infrastructure projects.

Germany Market Outlook: Germany leads the European market through its advanced industrial manufacturing ecosystem and Industry 4.0 implementation. Automotive, industrial automation, and engineering companies continue integrating private 5G, intelligent edge computing, and software-defined networking into production facilities. More than 60% of large industrial manufacturers have accelerated digital communication investments supporting autonomous manufacturing operations. Close collaboration between telecom providers, automation companies, and research institutions strengthens commercial deployment while maintaining Europe's technology competitiveness.

Asia-Pacific is emerging as the fastest-expanding regional market due to aggressive telecom infrastructure development, electronics manufacturing capacity, and government-backed digital transformation initiatives. The region accounts for approximately 29.6% of global demand while leading worldwide deployment of advanced communication infrastructure. Large-scale industrial digitization, expanding semiconductor manufacturing, and smart city investments continue strengthening enterprise adoption. Telecom operators are accelerating AI-powered network optimization and cloud-native architecture implementation to support rapidly growing industrial and consumer connectivity requirements. Domestic equipment manufacturing further enhances deployment speed and supply-chain resilience across multiple technology segments.

China Market Outlook: China remains the region's most influential market because of its unmatched communication infrastructure scale, domestic equipment manufacturing, and industrial digitalization programs. The country operates more than 4 million 5G base stations supporting smart manufacturing, logistics automation, and connected public infrastructure. Continuous investment in AI-enabled telecom management, semiconductor production, and industrial internet platforms enables rapid commercialization of next-generation communication technologies while strengthening global technology competitiveness.

South America is steadily expanding through enterprise digital transformation, mobile broadband modernization, and increasing cloud adoption despite infrastructure disparities across several countries. The region contributes approximately 4.2% of global demand, supported by telecom network upgrades and enterprise connectivity investments. Fiber expansion, private wireless deployments, and intelligent logistics communication solutions are improving operational efficiency across industrial sectors. Telecom operators continue forming infrastructure-sharing partnerships to reduce deployment costs while expanding network coverage. Limited rural connectivity and spectrum allocation timelines remain execution challenges, encouraging greater investment in software-defined communication architectures.

Brazil Market Outlook: Brazil leads the regional market through nationwide telecom modernization, expanding cloud infrastructure, and industrial connectivity investments. Manufacturing, agriculture, financial services, and logistics organizations continue adopting intelligent communication platforms to improve operational performance. Commercial 5G deployment continues expanding across major metropolitan areas, while enterprise investment in AI-enabled networking and edge infrastructure supports digital transformation initiatives across both public and private sectors.

The Middle East & Africa market is advancing through strategic telecom modernization, smart city initiatives, and expanding digital infrastructure investment. The region accounts for approximately 2.0% of global demand while demonstrating increasing deployment of advanced wireless networks and cloud-based communication platforms. National digital transformation strategies continue encouraging investment in AI-enabled networking, edge computing, and secure communication infrastructure. Telecom operators are strengthening international technology partnerships and accelerating fiber deployment to improve enterprise connectivity. Energy, logistics, and government sectors remain primary adopters of intelligent communication technologies supporting operational modernization.

United Arab Emirates Market Outlook: The United Arab Emirates serves as the region's technology leader through ambitious smart city programs, advanced telecom infrastructure, and strong digital economy initiatives. National investments in AI, cloud computing, and intelligent communication systems continue supporting enterprise innovation across transportation, finance, healthcare, and public services. Nationwide high-speed network availability and continued expansion of digital infrastructure position the country as a regional hub for advanced communication technology deployment and international technology partnerships.

The competitive landscape is led by global infrastructure vendors including Huawei, Ericsson, Nokia, Cisco Systems, and Qualcomm, which collectively control approximately 46% of the market, while regional telecom equipment suppliers and software-defined networking specialists compete through localized deployment and cost optimization. Global leaders compete on AI-native networking, Open RAN, private 5G, and cloud integration, whereas regional vendors emphasize customization and implementation speed. Nearly 70% of enterprise tenders prioritize technology performance and cybersecurity over purchase price, while AI-driven network automation reduces operating costs by around 30%, making software capabilities a decisive differentiator. Companies are expanding through strategic partnerships with hyperscale cloud providers, semiconductor manufacturers, and industrial automation firms while increasing investment in edge computing and satellite integration. Competition is shifting from hardware-centric offerings toward intelligent software platforms and ecosystem control. High R&D requirements, intellectual property portfolios, and telecom certification standards remain significant entry barriers. Success increasingly depends on delivering secure, interoperable, AI-enabled communication ecosystems with rapid deployment and lifecycle support.

Ericsson

Nokia

Cisco Systems

Qualcomm

Samsung Electronics

ZTE Corporation

Intel Corporation

Fujitsu Limited

NEC Corporation

Juniper Networks

Ciena Corporation

Mavenir

CommScope

AI-native networking, Open RAN architectures, and cloud-native core networks are redefining communication infrastructure by replacing hardware-centric operations with intelligent software control. More than 65% of leading telecom operators are deploying AI-assisted network management, while predictive automation reduces operational effort by approximately 35%. Open interfaces enable faster integration between multi-vendor environments, strengthening deployment flexibility and reducing long-term infrastructure dependency.

Edge computing, private 5G, integrated satellite communication, and software-defined networking are becoming standard enterprise technologies supporting manufacturing, healthcare, logistics, and smart infrastructure. Compared with conventional network management, AI-driven autonomous networks improve fault detection accuracy by nearly 40% while lowering service restoration time by approximately 30%. Large telecom operators, hyperscale cloud providers, and industrial enterprises benefit most because intelligent communication platforms enable real-time automation, secure connectivity, and scalable digital operations across distributed environments.

Between 2026 and 2028, early commercial 6G research, AI-native radio access networks, integrated sensing and communication, and non-terrestrial network convergence will reshape competitive positioning. Organizations accelerating investment in programmable networks, advanced semiconductors, cybersecurity, and edge intelligence will strengthen operational resilience while shortening service deployment cycles. Businesses delaying modernization risk higher operating costs, slower innovation, and reduced competitiveness as intelligent communication ecosystems become the foundation for enterprise digital infrastructure.

November 2024 – Nokia secured a major Open RAN agreement with Deutsche Telekom covering more than 3,000 mobile sites in Germany, replacing legacy Huawei equipment and accelerating multi-vendor cloud-based network deployment across Europe's largest telecom market. Source: www.reuters.com

September 2025 – Ericsson highlighted autonomous AI networking, integrated sensing, and quantum-ready mobile technologies, identifying four major technology transitions designed to improve network scalability, energy efficiency, and programmable service delivery for next-generation mobile infrastructure.

February 2026 – Ericsson and Qualcomm jointly validated foundational 6G radio technologies using prototype platforms, including a 400 MHz component carrier aligned with 3GPP Release 20 studies, accelerating the path toward AI-native commercial 6G ecosystems.

March 2026 – Ericsson announced expanded collaborations with NVIDIA, Qualcomm, and Linux Foundation partners to advance AI-native 6G platforms and open wireless architectures, strengthening ecosystem readiness for commercial next-generation communication infrastructure.

The report provides comprehensive analysis of communication technologies spanning AI-driven networking, 5G, Wi-Fi 6/6E, satellite communication, edge computing, optical networking, and software-defined infrastructure. It evaluates deployment across telecommunications, manufacturing, healthcare, transportation, smart cities, defense, consumer electronics, and energy sectors while assessing demand from telecom operators, enterprises, government organizations, industrial manufacturers, and critical infrastructure providers. Regional assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, representing virtually 100% of global commercial deployment activity.

The study examines competitive positioning, technology adoption patterns, deployment strategies, digital infrastructure modernization, supply-chain developments, and enterprise investment priorities between 2026 and 2033. It includes evaluation of AI-native communication platforms, Open RAN, private wireless networks, edge intelligence, and emerging 6G technologies while supporting investment planning, expansion strategy, product positioning, partnership development, and long-term competitive decision-making through detailed segmentation, regional benchmarking, technology assessment, and company-level strategic analysis.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 59,359.1 Million |

| Market Revenue (2033) | USD 234,091.6 Million |

| CAGR (2026–2033) | 18.71% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Huawei Technologies; Ericsson; Nokia; Cisco Systems; Qualcomm; Samsung Electronics; ZTE Corporation; Intel Corporation; Fujitsu Limited; NEC Corporation; Juniper Networks; Ciena Corporation; Mavenir; CommScope |

| Customization & Pricing | Available on Request (10% Customization Free) |