Reports

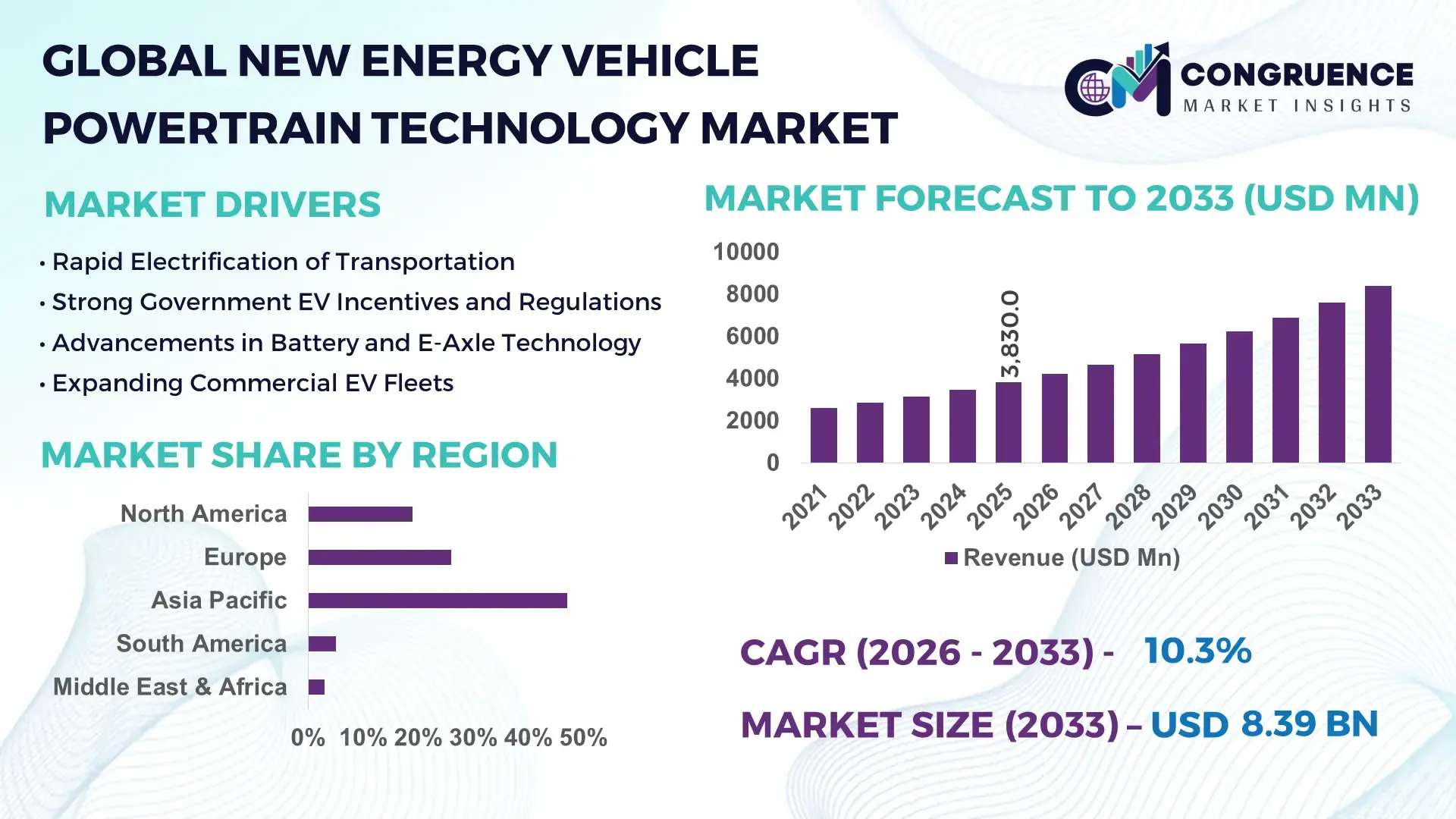

The Global New Energy Vehicle Powertrain Technology Market was valued at USD 3,830.0 Million in 2025 and is anticipated to reach USD 8,390.8 Million by 2033, expanding at a CAGR of 10.3% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is being propelled by rapid electrification of mobility, tighter emissions standards, and accelerating investments in battery–motor integration and high-efficiency drivetrains.

China, the dominant country in the global New Energy Vehicle (NEV) powertrain ecosystem, has built a vertically integrated industrial base spanning batteries, electric motors, power electronics, and transmission systems. The country operates more than 300 large-scale lithium-ion battery gigafactories in various stages of production or planning, with annual battery manufacturing capacity exceeding 1,500 GWh by mid-decade. Chinese automakers and suppliers invested over USD 70–80 billion in 2023–2024 in electrification-related manufacturing, R&D, and supply chains. Applications extend beyond passenger cars into buses, heavy trucks, delivery vans, and two-wheelers, where high-torque e-axles and integrated motor-inverter units are increasingly standard. Technologically, China leads in silicon-carbide (SiC) power modules, 800V architectures, and integrated drive units, with more than 40 domestic OEM models already using 800V platforms. Local governments have also funded pilot programs for smart powertrains using AI-based thermal management and predictive maintenance across 10+ major metropolitan regions.

Market Size & Growth: Valued at USD 3.83 billion in 2025 and projected to reach USD 8.39 billion by 2033 with ~10.3% CAGR, driven by faster adoption of high-voltage and integrated e-drive systems.

Top Growth Drivers: 65% rise in EV penetration in major cities; 18% efficiency gain from 800V systems; 22% reduction in drivetrain weight via integration.

Short-Term Forecast: By 2028, average powertrain cost per kWh is expected to drop 12–15% through modular designs and scale.

Emerging Technologies: Silicon-carbide (SiC) inverters, integrated motor–inverter–gearbox units, and AI-based thermal optimization.

Regional Leaders (2033): China ~USD 3.2B (fast 800V rollout); Europe ~USD 2.1B (regulatory-led adoption); North America ~USD 1.7B (OEM platform consolidation).

Consumer/End-User Trends: Fleet operators prioritize durability and energy efficiency; private buyers favor fast-charging compatibility.

Pilot/Case Example: In 2024, a leading Chinese OEM cut thermal losses by 14% using AI-driven cooling in its integrated drive unit.

Competitive Landscape: Market leader ~28–32% share, followed by Bosch, BYD, ZF, and Nidec.

Regulatory & ESG Impact: Stricter CO₂ rules in EU/China and battery recycling mandates are accelerating adoption.

Investment & Funding Patterns: Over USD 25B invested globally in e-powertrain plants, with rising public–private financing.

Innovation & Future Outlook: Shift toward 1,000V-ready systems, lightweight materials, and software-defined powertrains.

The New Energy Vehicle Powertrain Technology Market is increasingly shaped by passenger EVs and commercial fleets, which together account for the bulk of demand for e-axles, inverters, and traction motors. Recent innovations include oil-cooled motors, compact gear reductions, and software-controlled torque vectoring that improves safety and range. Stricter emissions rules in Europe and China, along with industrial policies such as IRA incentives in North America, are reshaping regional supply chains. Asia–Pacific leads consumption, while Europe shows the fastest regulatory-driven upgrades toward 800V platforms. Looking ahead, greater modularity, higher-voltage architectures, and smarter thermal systems will define competitive advantage.

The New Energy Vehicle Powertrain Technology Market sits at the core of global decarbonization and industrial competitiveness strategies. Powertrains determine vehicle efficiency, charging speed, lifecycle emissions, and total cost of ownership—making them a strategic asset for automakers, battery suppliers, utilities, and governments. As countries tighten carbon standards and phase out internal combustion engines, control over next-generation e-powertrain platforms has become as critical as control over battery supply chains.

Technologically, 800V SiC-based powertrains deliver ~8–12% efficiency improvement compared to older 400V IGBT systems, enabling faster charging and longer range without larger batteries. This benchmark shift is pushing OEMs to redesign vehicle architectures around integrated drive units that combine motor, inverter, and gearbox into a single lightweight module, cutting drivetrain mass by roughly 15–25%.

Regionally, China dominates in production volume, supported by massive domestic battery and component capacity, while Europe leads in adoption, with roughly 55–60% of major OEM portfolios now committed to 800V-ready platforms by 2030. North America is catching up through platform consolidation and localized manufacturing under industrial incentives.

In the short term, by 2028, AI-driven thermal management and predictive control systems are expected to improve real-world drivetrain efficiency by 10–15% while reducing warranty failures through smarter monitoring of motors, inverters, and bearings.

From an ESG perspective, firms are committing to 20–30% reductions in powertrain manufacturing emissions by 2030, alongside battery and motor recycling targets exceeding 70% material recovery in leading markets.

A concrete micro-scenario illustrates this trajectory: in 2024, a Chinese commercial-vehicle manufacturer reduced energy losses by 18% across its electric truck fleet by deploying software-optimized powertrain controls and advanced cooling.

Looking forward, the New Energy Vehicle Powertrain Technology Market will be a pillar of resilient, compliant, and sustainable mobility systems—linking clean energy, smart manufacturing, and digital control into a single integrated ecosystem for the next generation of transport.

The New Energy Vehicle Powertrain Technology Market is being shaped by the convergence of electrification, digitalization, and supply-chain localization. Rapid deployment of 800V architectures, silicon-carbide power electronics, and integrated e-axles is redefining performance benchmarks for efficiency, torque density, and thermal stability. Automakers are shifting from component sourcing to system-level integration, favoring suppliers that can deliver compact, software-defined drivetrains rather than standalone motors or inverters. Simultaneously, battery advancements—particularly high-nickel chemistries and structural packs—are influencing powertrain design requirements around cooling, packaging, and durability. Government policies on zero-emission vehicles, urban air-quality standards, and industrial incentives are accelerating demand while encouraging domestic manufacturing. At the same time, supply constraints in critical minerals, grid readiness for fast charging, and the need for recycling-compatible designs are introducing new complexities. Competition is intensifying among tier-1 suppliers, battery firms, and OEM in-house units, leading to faster innovation cycles, strategic partnerships, and vertical integration across the powertrain value chain.

The transition from traditional 400V systems to 800V architectures is fundamentally reshaping the New Energy Vehicle Powertrain Technology Market. Higher voltage platforms reduce current requirements for the same power output, cutting resistive losses in cables, inverters, and motors. This enables smaller wiring harnesses, lighter vehicles, and improved energy efficiency, which is particularly critical for long-range electric cars and heavy commercial EVs. Major automakers have already launched more than 30 models globally based on 800V platforms, and the number is expected to rise sharply as charging infrastructure upgrades. Fast-charging networks are increasingly optimized for high-voltage vehicles, allowing charging speeds of 250–350 kW at compatible stations. Silicon-carbide inverters, which perform better at higher voltages, are seeing adoption rates climb above 40% in premium EV segments. Fleet operators benefit from reduced downtime due to faster charging and lower heat generation, which extends component life. As suppliers scale SiC manufacturing and costs decline, 800V systems are moving from luxury to mainstream vehicles, making this shift a central driver of market evolution.

The expansion of the New Energy Vehicle Powertrain Technology Market is being constrained by volatility in critical raw materials used in batteries and power electronics. Lithium, nickel, cobalt, and rare earth elements for electric motors face supply bottlenecks due to geographically concentrated mining and processing capacities. For example, over 70% of global lithium refining capacity is located in a small number of countries, creating geopolitical and price risks for manufacturers. Price fluctuations in lithium carbonate have led to unpredictable production costs, discouraging long-term investment in some regions. Additionally, shortages of silicon carbide wafers have slowed the rollout of high-efficiency inverters, as wafer production remains limited and capital-intensive. Recycling infrastructure is still immature in many markets, meaning end-of-life materials are not yet reliably reintegrated into supply chains. Smaller suppliers struggle to secure stable contracts for key inputs, putting them at a disadvantage compared to vertically integrated firms. These material constraints increase lead times, raise manufacturing costs, and create uncertainty that restrains the pace of large-scale powertrain deployment.

Integrated e-axles—combining motor, inverter, and gearbox into a single unit—represent a major opportunity for the New Energy Vehicle Powertrain Technology Market. These systems reduce component count by up to 30%, simplifying assembly, lowering weight, and improving reliability. Automakers are increasingly favoring modular powertrain platforms that can be scaled across multiple vehicle segments, from compact cars to SUVs and light trucks. This standardization allows suppliers to achieve economies of scale while reducing development timelines. Several leading OEMs are adopting skateboard-style architectures where modular e-axles can be swapped with minimal redesign. In commercial vehicles, integrated systems enable better packaging for larger batteries and cargo space. Advanced cooling methods, such as oil-spray motor cooling, are enhancing performance and durability under heavy loads. The growing demand for all-wheel-drive EVs is further boosting dual-motor integrated solutions. As software control becomes more sophisticated, these modular units can be remotely optimized, opening new revenue streams through performance updates and predictive maintenance services.

Thermal management has emerged as one of the most significant technical challenges in the New Energy Vehicle Powertrain Technology Market. High-power motors and inverters generate substantial heat, especially during fast acceleration, high-speed driving, or rapid charging. Excessive temperatures can degrade magnetic materials, reduce efficiency, and shorten component lifespan. Traditional air-cooling methods are often insufficient for high-performance EVs, pushing manufacturers toward more complex liquid or oil-based cooling systems that add cost and engineering complexity. Integrating battery, motor, and inverter cooling into a single thermal loop increases design difficulty and risk of system failures. In cold climates, maintaining optimal operating temperatures also requires additional heating systems, which consume energy and reduce driving range. Managing thermal loads becomes even more challenging in compact integrated e-axles where space is limited. Moreover, variations in driving behavior and ambient conditions make it difficult to design a one-size-fits-all solution. These factors raise development costs, increase testing requirements, and slow product cycles across the market.

Rise in Modular and Prefabricated Powertrain Manufacturing: Modular powertrain assembly is transforming how NEV drivetrains are produced, with roughly 55% of new EV programs now using pre-assembled e-axle modules instead of line-by-line integration. Off-site fabrication of motor–inverter units using automated tooling has cut factory labor intensity by 20–25% while reducing assembly time per vehicle by 8–10 hours. European and North American plants are increasingly adopting plug-and-play e-drive modules to accelerate model launches and reduce retooling costs.

Rapid Shift to 800V SiC Systems: The share of SiC-based inverters in premium EVs has climbed to about 40–45% in 2024, enabling charging speeds above 300 kW on compatible networks. Automakers report 8–12% real-world efficiency gains, allowing range extensions of 40–70 km without increasing battery size. Supplier capacity for SiC wafers is expanding by more than 30% annually, signaling mainstream adoption through 2030.

Software-Defined Powertrains and AI Control: More than 25% of new EV models in 2025 are deploying AI-assisted thermal and torque management systems. Early fleet pilots show 10–15% reductions in energy losses and 12% fewer drivetrain failures through predictive monitoring of motors and inverters. Over-the-air updates are becoming standard, turning powertrains into continuously improving digital products.

Integration of High-Density Motors and Lightweight Materials: New-generation hairpin-wound motors and advanced laminations have lifted power density by 15–20% while cutting motor mass by 10–18%. Several OEMs are moving to aluminum casings and composite housings, trimming drivetrain weight by 25–35 kg per vehicle, which directly improves efficiency and handling across passenger and commercial EV segments.

The New Energy Vehicle Powertrain Technology Market is structured around evolving propulsion architectures, diverse vehicle applications, and a widening range of end-users that increasingly treat the powertrain as a strategic differentiator rather than a commodity component. By type, the market spans battery-electric, plug-in hybrid, fuel-cell, and hybrid/range-extender systems—each optimized for distinct performance, cost, and infrastructure conditions. Application-wise, demand is anchored by passenger cars but is rapidly broadening into commercial fleets, buses, light trucks, and two-wheelers as electrification moves beyond urban mobility. From an end-user perspective, original equipment manufacturers (OEMs) remain the primary buyers, yet tier-1 suppliers, fleet operators, public transit agencies, and specialized vehicle makers are gaining influence as modular, software-defined drivetrains enable faster deployment across platforms. Across all segments, common themes include higher voltage architectures, tighter integration of motor–inverter–gearbox units, and growing reliance on digital control and predictive maintenance to improve durability, efficiency, and lifecycle performance.

Battery Electric Vehicle (BEV) powertrains dominate the market, accounting for ~58% of current adoption due to superior energy efficiency, simpler mechanical design, and the fastest-expanding charging infrastructure. BEV systems increasingly rely on integrated e-axles, 800V architectures, and silicon-carbide inverters that reduce losses and improve thermal stability—making them the preferred choice for both passenger cars and heavy electric trucks.

In comparison, plug-in hybrid electric (PHEV) powertrains hold about 22% of the market, benefiting from their ability to bridge electric and conventional mobility in regions with uneven charging coverage. PHEVs remain attractive for long-distance travel and fleet applications where range anxiety persists, though their mechanical complexity limits long-term scalability.

Fuel-cell electric vehicle (FCEV) powertrains represent roughly 12% today but are the fastest-growing type, expanding at around 18% CAGR. Growth is driven by hydrogen corridor investments, zero-emission mandates for heavy-duty transport, and rising demand for rapid refueling in logistics and long-haul trucking.

Other configurations—including mild hybrids, range-extender systems, and experimental solid-state hybrid drivetrains—collectively contribute about 8% of the market, serving niche urban mobility, specialty vehicles, and pilot programs where ultra-lightweight or ultra-compact systems are required.

• In 2025, the International Energy Agency reported that several European trucking pilots deployed hydrogen fuel-cell powertrains across cross-border freight routes, demonstrating continuous 24-hour operations with refueling times under 20 minutes.

Passenger cars are the leading application, representing about 55% of demand as automakers prioritize high-efficiency, high-voltage powertrains to extend range, reduce charging time, and comply with tightening emissions standards. Mass-market platforms are increasingly standardized around modular e-axles, enabling scale and faster model rollouts.

Commercial vehicles—buses, delivery vans, and electric trucks—account for roughly 25% of adoption today, but they are the fastest-growing application at around 16% CAGR, propelled by urban zero-emission zones, fleet electrification mandates, and lower total cost of ownership from regenerative braking and predictive maintenance.

Two-wheelers and light mobility represent around 10%, driven by battery swapping ecosystems in Asia and rising demand for last-mile delivery vehicles. Off-highway and specialty vehicles (construction, mining, and agriculture) make up the remaining 10%, where electric drivetrains are gaining traction due to lower noise, reduced emissions, and improved torque control.

In 2025, more than 38% of global enterprises reported piloting advanced electric powertrain systems for fleet optimization and energy management. Additionally, surveys indicate that over 60% of urban Gen Z consumers prefer brands that offer fast-charging, software-upgradable electric vehicles.

• In 2025, a major European city transit authority documented that electric buses using integrated e-axle systems reduced depot charging time by 22% while cutting maintenance-related downtime across its fleet.

OEMs remain the leading end-user group with about 50% of demand, as vehicle manufacturers increasingly design proprietary or co-developed powertrain platforms to secure performance differentiation and supply-chain control. Many OEMs are vertically integrating motors, inverters, and software to reduce dependence on external suppliers.

Tier-1 suppliers—holding roughly 22% of the market—are the fastest-growing end-users at about 15% CAGR, fueled by rising demand for turnkey integrated e-axles, thermal systems, and power electronics that can be deployed across multiple vehicle brands.

Fleet operators and logistics companies together account for 13%, prioritizing durability, energy efficiency, and predictive diagnostics to minimize downtime and operating costs. Public transit agencies contribute about 8%, rapidly electrifying bus networks with standardized powertrain modules. The remaining 7% comes from specialty vehicle makers, aftermarket integrators, and industrial equipment providers experimenting with electric propulsion.

In 2025, nearly 42% of large commercial fleets in North America were testing AI-enabled electric powertrains that integrate vehicle data with route planning and energy management systems. Meanwhile, more than 35% of global public transit agencies announced plans to fully electrify new vehicle purchases by 2030.

• A 2025 United Nations Environment Programme assessment found that municipal bus electrification programs in Asia deployed standardized electric powertrains across more than 120 cities, significantly reducing urban particulate emissions.

Asia-Pacific accounted for the largest market share at 47% in 2025; however, North America is expected to register the fastest growth, expanding at a CAGR of 12.1% between 2026 and 2033.

Asia-Pacific’s leadership is supported by large-scale electric vehicle production hubs, with over 18 million NEVs manufactured annually, extensive battery and motor supply chains, and strong domestic demand. Europe follows with 26% market share, driven by regulatory mandates and high penetration of advanced 800V powertrain architectures. North America holds 19% share, supported by accelerating EV platform launches and federal incentives tied to domestic manufacturing. South America and Middle East & Africa together account for the remaining 8%, where adoption is concentrated in urban fleets and pilot programs. Regionally, more than 60% of global fast-charging-compatible powertrains are deployed across Asia-Pacific and Europe, highlighting infrastructure-led technology adoption differences.

North America represents 19% of the global New Energy Vehicle Powertrain Technology Market, supported by strong demand from passenger EVs, electric pickups, and commercial delivery fleets. Automotive manufacturing, logistics, and public transportation are the key industries driving adoption. Federal and state-level incentives encourage domestic production of electric motors, inverters, and battery packs, while local-content rules are reshaping supply chains. Technologically, the region shows rapid uptake of 800V architectures, silicon-carbide power electronics, and software-defined powertrains with over-the-air update capabilities. Leading OEMs are integrating AI-based thermal management to reduce drivetrain losses. A notable regional player has expanded integrated e-axle production capacity to support next-generation electric trucks. Consumer behavior shows higher acceptance of long-range EVs and fast-charging compatibility, particularly among fleet operators prioritizing uptime and durability.

Europe accounts for 26% of the global market, with Germany, the UK, and France serving as core demand centers. Stringent emissions regulations and carbon-neutral mobility targets are central to adoption, pushing automakers toward high-efficiency electric and hybrid powertrains. Sustainability initiatives emphasize lifecycle emissions reduction, recyclability, and energy efficiency. European manufacturers are early adopters of integrated drive units, advanced motor winding technologies, and digital twins for powertrain testing. Local suppliers are investing heavily in lightweight materials and oil-cooled motors to enhance performance. One leading European tier-1 supplier has standardized modular e-axles across multiple OEM platforms. Consumer behavior reflects regulatory influence, with buyers favoring vehicles compliant with low-emission zones and transparent energy-efficiency labeling.

Asia-Pacific leads the market with 47% share, ranking first globally by production volume. China, India, and Japan are the top consuming countries, collectively producing over 70% of the world’s electric vehicles. The region benefits from dense manufacturing clusters, extensive supplier networks, and rapid charging infrastructure rollout. Innovation hubs focus on high-speed motors, compact inverters, and cost-optimized integrated e-axles. Several regional players have achieved full vertical integration from battery cells to drive units. Consumer behavior is shaped by affordability and urban mobility needs, with strong uptake of compact EVs, electric two-wheelers, and shared mobility platforms.

South America holds 5% of the global market, led by Brazil and Argentina. Adoption is concentrated in public transportation, municipal fleets, and light commercial vehicles. Infrastructure development is focused on urban charging depots rather than nationwide fast-charging networks. Governments offer tax incentives and import-duty reductions for electric components to stimulate local assembly. A regional automaker has begun local assembly of electric buses using imported integrated powertrains. Consumer behavior shows gradual acceptance, with demand closely tied to fuel cost volatility and city-level clean transport initiatives.

The Middle East & Africa region accounts for 3% of the global market, with demand centered in the UAE and South Africa. Electrification is driven by diversification strategies, smart city projects, and public transport modernization. Technological modernization includes adoption of high-efficiency powertrains for electric buses and premium passenger EVs. Trade partnerships facilitate imports of advanced drivetrains, while pilot assembly projects are emerging. A regional mobility initiative has deployed electric buses using modular powertrains for urban routes. Consumer behavior is characterized by early adoption in premium segments and government-led fleet electrification.

China – 34% Market Share: Dominance supported by massive production capacity, vertically integrated supply chains, and widespread deployment across passenger and commercial EVs.

Germany – 14% Market Share: Leadership driven by advanced automotive engineering, strong regulatory push for electrification, and high adoption of integrated and high-voltage powertrain systems.

The competitive environment of the New Energy Vehicle Powertrain Technology Market is moderately consolidated, with approximately 60–70 active global competitors ranging from OEMs to specialized powertrain suppliers. The top 5 companies—comprising Tesla, Toyota, BYD, Bosch, and Volkswagen—collectively hold around 45% combined market share, reflecting strong positioning yet allowing room for niche innovators and regional players. Competition centers on integration of motor-inverter-gearbox units, high-voltage SiC power electronics, and digital energy management strategies that optimize performance and efficiency.

Leading companies are intensifying strategic initiatives such as partnerships and product launches: Tesla rolled out a next-generation integrated drive unit architecture in early 2025 to enhance thermal management and simplify drivetrain layouts; Volkswagen entered a collaboration with Northvolt in 2024 to secure advanced e-drive and battery-integrated systems; Bosch has accelerated its hydrogen and fuel-cell powertrain initiatives targeted at commercial vehicle platforms. OEM entrants and tier-1 suppliers are also pursuing strategic acquisitions of specialized powertrain tech startups to bolster intellectual property and shorten innovation cycles.

Innovation trends shaping competition include software-defined powertrains with predictive diagnostics, 800V system adoption, and scalable modular platforms that support passenger, commercial, and off-highway applications. Regional specialization remains significant: Asian players lead high-volume manufacturing and vertical integration, while European manufacturers emphasize high-efficiency systems aligned with stringent regulatory compliance. Competitive intensity is further influenced by digital transformation and partnerships with semiconductor firms to advance traction inverter and energy management technology, positioning the market as both technically dynamic and strategically contested.

Bosch GmbH

Volkswagen AG

Hyundai Motor Company

Siemens AG

Continental AG

Valeo SA

Nidec Corporation

ZF Friedrichshafen AG

BorgWarner Inc.

Magna International Inc.

KPIT Technologies

Mitsubishi Motors

Foxconn (EV powertrain collaboration)

Schaeffler AG

Technology in the New Energy Vehicle Powertrain Technology Market is advancing rapidly on multiple fronts, with current and emerging innovations reshaping system performance, reliability, and integration. 800-volt architectures and silicon-carbide (SiC) power modules are becoming mainstream in high-performance EVs, enabling lower resistive losses and faster charging support. Traction inverters built with SiC achieve peak efficiencies exceeding 96–97%, significantly reducing thermal losses and improving range without increasing battery capacity. High-efficiency permanent magnet motors with hairpin winding logistics and compact gearbox integration are enhancing power density while decreasing component size and system weight.

Integrated e-axles—combining the motor, inverter, and gearbox—are now a key focus, reducing parts count and simplifying assembly. Digitalization features such as software-defined powertrain control systems are optimizing thermal management and torque distribution in real time, improving energy utilization and operational uptime. Increasing adoption of modular electric drive platforms allows suppliers and OEMs to scale powertrain architectures across vehicle segments from compact cars to heavy trucks.

Battery integration trends intersect with powertrain innovation, with efforts to embed components like inverters directly into high-voltage battery packs to save space and enhance efficiency. Advancements in cooling technologies, including oil-based and microchannel liquid cooling, are improving thermal stability at high loads. Emerging research explores two-dimensional optimization of powertrain element placements and hybrid switched reluctance-assisted motors that deliver higher torque density and performance efficiency in compact layouts. Additionally, the convergence of electrification with energy technologies like Vehicle-to-Grid (V2G) systems is expanding the functional role of powertrains to contribute to grid stability and energy management. Collectively, these technological trajectories are central to competitive differentiation, pushing system capabilities beyond traditional mechanical designs into digitally enabled, highly efficient electrified propulsion ecosystems.

• On March 17, 2025, BYD Auto launched its Super e-Platform, a breakthrough electrification architecture featuring flash-charging batteries, a 1 000 kW (megawatt-class) charging capability, a 30 000 rpm motor, and new silicon carbide power chips. This platform enables electric vehicles to achieve up to 400 km of range in approximately 5 minutes of charging and supports peak motor outputs of 580 kW and speeds above 300 km/h. The Super e-Platform is now open for pre-order on models such as the Han L and Tang L. Source: www.byd.com

• In August 2025, Tesla Inc. officially introduced the new Model Y Performance variant, featuring an optimized dual-motor all-wheel-drive powertrain delivering approximately 460 HP with improved range and efficiency characteristics versus previous Model Y trims. The powertrain enhancements focused on maximizing performance and energy use for both European and global markets. Source: www.roadandtrack.com

• In 2025, Volkswagen Group partnered with Northvolt to secure advanced e-drive components and battery-integrated powertrain systems for its future electric vehicle platforms, boosting modularization and scalability of drive systems across multiple vehicle lines. These efforts include aligning powertrain design with battery architecture for optimized energy use.

• In 2024–2025, Bosch GmbH expanded its global electrification initiatives through a joint venture with Jiangling Motors Corporation focused on producing scalable e-drive axles for light commercial vehicles, reinforcing its commitment to electrification and modular drivetrain solutions for varied applications. This move supports localized production and technology deployment for electrified transport segments.

The New Energy Vehicle Powertrain Technology Market Report provides a comprehensive view of the evolving global powertrain landscape for electrified mobility. It covers segmentation by powertrain types—such as battery electric, plug-in hybrid, fuel cell, and range-extender systems—and assesses technology components including motors, inverters, gearboxes, and integrated e-axles. The report delves into application domains spanning passenger cars, commercial vehicles, buses, two-wheelers, and specialty vehicles, highlighting unique technical requirements and performance benchmarks across segments.

Geographically, the analysis spans Asia-Pacific, North America, Europe, South America, and Middle East & Africa, addressing regional infrastructure, manufacturing ecosystems, consumer behavior, and policy impacts. The report examines end-user profiles, detailing how original equipment manufacturers, tier-1 suppliers, fleet operators, and transit agencies engage with powertrain technologies. It identifies innovation vectors such as high-voltage architectures, silicon-carbide power electronics, software-defined powertrain control, and digital thermal management systems. Special emphasis is placed on integration trends like battery-pack embedded power electronics and modular platforms.

Additionally, emerging and niche areas such as hydrogen fuel cell powertrains, V2G interoperability, and advanced cooling technologies are evaluated for future relevance. The report outlines competitive positioning, strategic partnerships, R&D trajectories, and technological disruptions shaping the competitive dynamics. Overall, the scope provides decision-makers with actionable insights into market structure, technology maturity, regional opportunities, and strategic investment areas that define the electrified powertrain ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 3,830.0 Million |

| Market Revenue (2033) | USD 8,390.8 Million |

| CAGR (2026–2033) | 10.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Tesla; Toyota; BYD; Bosch; Volkswagen; Hyundai; Siemens; Continental; Valeo; Nidec; ZF Friedrichshafen; BorgWarner; Magna International; KPIT Technologies; Mitsubishi Motors; Foxconn (EV powertrain); Schaeffler |

| Customization & Pricing | Available on Request (10% Customization Free) |