Reports

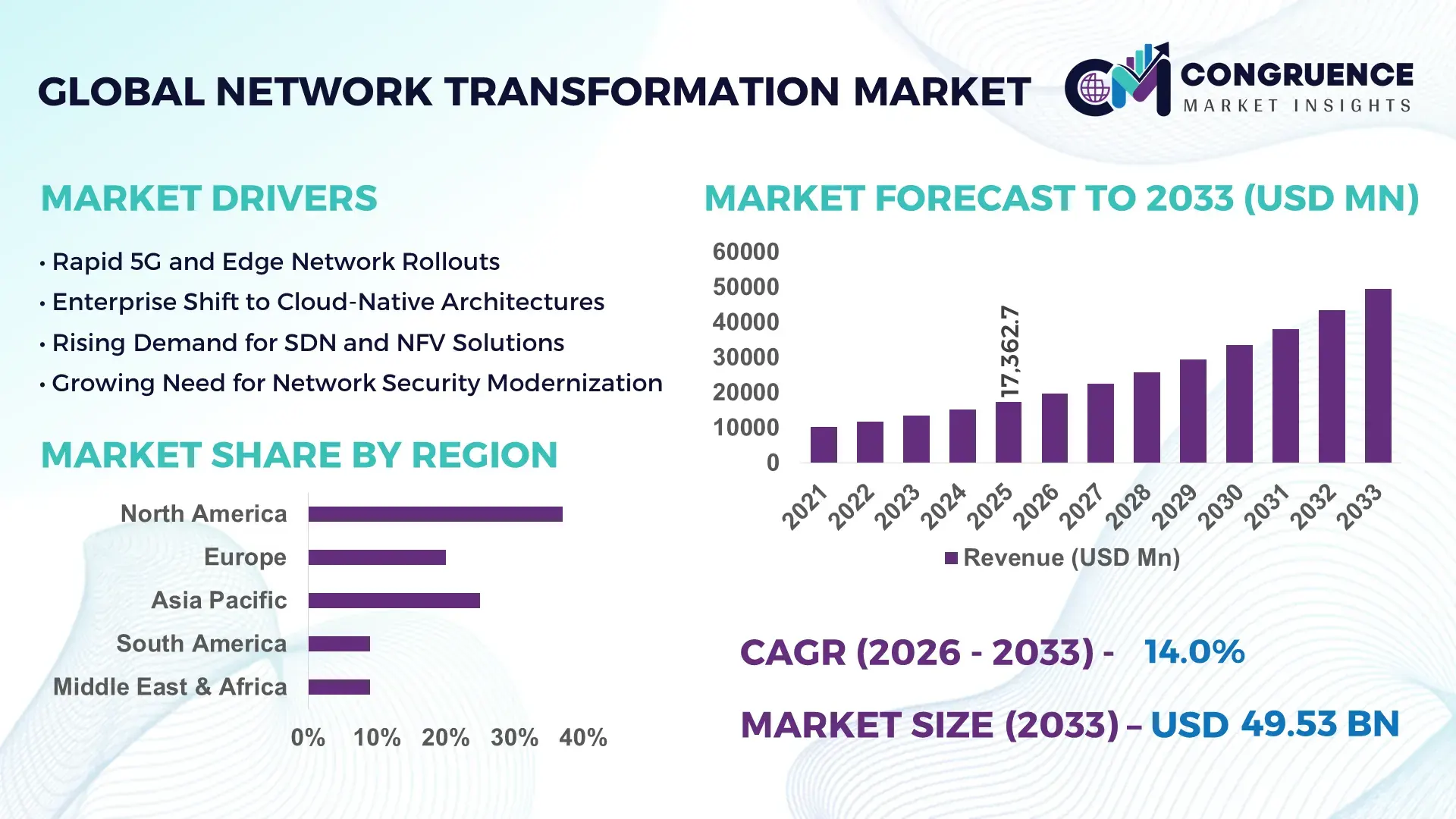

The Global Network Transformation Market was valued at USD 17362.65 Million in 2025 and is anticipated to reach a value of USD 49528.47 Million by 2033 expanding at a CAGR of 14% between 2026 and 2033. This growth trajectory reflects rising enterprise demand for agile, software-defined, and cloud-integrated network infrastructures capable of supporting high-bandwidth applications, distributed workforces, and real-time digital services.

The United States represents a central hub for network transformation activity, supported by large-scale 5G infrastructure rollouts exceeding 300,000 active cellular sites and continued fiber network expansion covering over 60% of urban households. Enterprise investment in network modernization, including SD-WAN and network automation platforms, has surpassed multi-billion-dollar annual budgets among leading telecom operators and hyperscale cloud providers. Key applications span financial services for secure digital transactions, healthcare for telehealth and data interoperability, and manufacturing for industrial IoT. Advanced deployment of AI-based network analytics, edge data centers, and virtualization technologies underscores the country’s strong technological depth and commercialization capability.

Market Size & Growth: USD 17.36 Billion (2025) to USD 49.53 Billion (2033), CAGR 14%, driven by enterprise digital transformation and high-speed connectivity demand.

Top Growth Drivers: 5G adoption 42%, cloud network migration 38%, automation efficiency gains 29%.

Short-Term Forecast: By 2028, network operating costs may decline 28% while performance efficiency improves 35%.

Emerging Technologies: AI-driven network orchestration, SD-WAN/NFV convergence, edge-enabled network architectures.

Regional Leaders: North America USD 90 Billion by 2033 with strong cloud integration; Asia Pacific USD 48 Billion driven by mobile broadband scale; Europe USD 35 Billion emphasizing secure, compliant infrastructure.

Consumer/End-User Trends: Large enterprises lead adoption; BFSI and healthcare prioritize secure, scalable, low-latency networks.

Pilot or Case Example: 2027 SD-WAN enterprise pilot reduced downtime 40% and increased throughput 25%.

Competitive Landscape: Cisco ~15% share; key players include Juniper Networks, HPE, Huawei, IBM.

Regulatory & ESG Impact: Data protection mandates and energy-efficient network standards shaping architecture upgrades.

Investment & Funding Patterns: Over USD 18 Billion in modernization programs and venture-backed network intelligence firms.

Innovation & Future Outlook: Expansion of zero-trust networking, programmable fabrics, and AI-integrated network operations.

The Network Transformation market is shaped by IT & telecom contributing over 35% of deployment demand, followed by BFSI near 20% and healthcare exceeding 15% due to secure data exchange and remote service models. Innovations in virtualized core networks, open RAN architectures, and AI-enabled traffic management are redefining infrastructure efficiency. Regulatory emphasis on data sovereignty, cybersecurity, and energy-efficient networks is accelerating modernization cycles. Asia-Pacific shows rapid consumption growth linked to urban digitalization and 5G expansion, while Europe emphasizes secure cross-border connectivity. Future growth is expected from edge computing integration, autonomous network management, and cloud-native network functions supporting ultra-low latency services.

Network Transformation has become a strategic imperative for enterprises and service providers seeking to modernize legacy infrastructure, enhance digital service delivery, and ensure operational resilience. Organizations are increasingly shifting toward software-defined and cloud-native networking frameworks to support distributed operations, edge computing, and data-intensive applications. Software-Defined Wide Area Networking (SD-WAN) delivers nearly 35% improvement in network utilization efficiency compared to traditional MPLS-based architectures, enabling faster provisioning and cost optimization. The strategic value lies in improved agility, enhanced cybersecurity postures, and the ability to support real-time analytics and automation across multi-cloud environments.

Regionally, Asia-Pacific dominates in deployment volume due to large-scale telecom infrastructure rollouts and expanding broadband networks, while North America leads in adoption intensity with over 65% of large enterprises implementing software-defined or virtualized networking frameworks. This divergence highlights how infrastructure scale and enterprise digitization maturity shape transformation pathways.

In the short term, by 2028, AI-driven network automation is expected to reduce network fault resolution time by nearly 40%, significantly improving service reliability. From a compliance and ESG perspective, firms are committing to energy-efficiency targets such as 30% reduction in network power consumption by 2030 through virtualization and optimized data routing. In 2026, a leading telecom operator in South Korea achieved 25% latency reduction through edge-enabled 5G core deployment integrated with AI traffic management. Collectively, these pathways position the Network Transformation Market as a foundational pillar of digital resilience, regulatory alignment, and sustainable, long-term enterprise growth.

Enterprise digital transformation is a primary catalyst for Network Transformation as organizations modernize IT infrastructure to support cloud platforms, SaaS applications, and remote operations. Over 70% of enterprises now operate in hybrid or multi-cloud environments, demanding dynamic bandwidth allocation and secure connectivity. Adoption of SDN and NFV enables centralized control and automation, reducing manual configuration errors by nearly 50%. Industries such as BFSI and healthcare require low-latency, secure data exchange to support digital payments, telemedicine, and data analytics. The proliferation of IoT devices—expected to exceed 30 billion connected endpoints globally within a few years—places additional performance demands on enterprise networks. These operational shifts compel organizations to invest in scalable, software-driven network frameworks capable of supporting continuous digital service delivery.

A significant restraint in the Network Transformation market is the complexity of integrating modern software-defined solutions with legacy network infrastructure. Many enterprises still operate hardware-centric systems deployed over a decade ago, lacking compatibility with virtualization and automation platforms. Migration processes can lead to temporary service disruptions and require specialized expertise, increasing operational risk. Studies indicate that nearly 40% of IT teams cite interoperability issues as a barrier to modernization. Additionally, workforce skill gaps in cloud networking and automation technologies slow deployment timelines. Security concerns during transition phases, including misconfigurations and exposure of network endpoints, further complicate implementation. These factors collectively create hesitancy among organizations with highly customized or mission-critical legacy environments.

The rise of edge computing presents substantial opportunities for Network Transformation by enabling low-latency processing closer to end users. Applications such as autonomous systems, smart manufacturing, and AR/VR require response times below 10 milliseconds, which centralized data centers cannot consistently provide. Deployment of edge nodes integrated with 5G networks supports real-time analytics and localized data processing. Enterprises adopting edge-enabled architectures report up to 30% improvement in application performance and reduced backhaul traffic. Smart city initiatives, industrial IoT networks, and connected healthcare systems are accelerating demand for distributed network frameworks. This evolution encourages investment in programmable, software-driven infrastructure that seamlessly connects core, cloud, and edge environments.

As networks become more software-defined and distributed, the attack surface expands significantly, creating complex cybersecurity challenges. Organizations managing multi-cloud and hybrid networks face thousands of potential endpoints, increasing vulnerability to breaches and ransomware attacks. Global cyber incidents have risen by more than 30% annually in recent years, compelling stricter security controls. Implementing zero-trust architectures and continuous monitoring requires advanced tools and skilled personnel, increasing operational complexity. Regulatory compliance obligations around data protection further raise accountability for network integrity. Balancing openness for interoperability with stringent security controls remains difficult, especially for enterprises undergoing rapid transformation, making cybersecurity a critical challenge influencing Network Transformation strategies.

• AI-Driven Network Automation Adoption Surpassing 60% in Tier-1 Enterprises: Enterprises are rapidly deploying AI-based orchestration platforms to automate traffic routing, fault detection, and performance optimization. Over 60% of large organizations have integrated AI-enabled network management tools, resulting in nearly 45% faster incident resolution and 30% lower manual configuration workloads. Predictive analytics models now process millions of network events per hour, enabling proactive congestion control and service assurance across hybrid infrastructures.

• Edge-Integrated Network Architectures Expanding by Over 50% in Industrial Use Cases: Manufacturing, logistics, and energy sectors are adopting edge-enabled networks to support latency-sensitive applications. More than 50% of new industrial digitalization projects now include edge networking components, achieving up to 35% reduction in data transit delays and 25% improvement in operational response times. Deployment of localized micro data centers and 5G edge nodes is increasing device connectivity density beyond 1 million devices per square kilometer in smart facility environments.

• Transition to Open and Virtualized Network Frameworks Exceeding 65% Deployment: Service providers are accelerating migration from proprietary hardware to open, virtualized architectures. Over 65% of new network rollouts incorporate NFV and open-standard interfaces, improving interoperability and reducing equipment dependency. Virtualized network functions have demonstrated up to 40% reduction in hardware footprint and 32% improvement in scalability, enabling faster service deployment cycles and flexible network slicing for enterprise applications.

• Energy-Efficient Networking Technologies Cutting Power Consumption by 30%: Sustainability-driven modernization is pushing adoption of energy-optimized routing and hardware virtualization. Intelligent traffic engineering and dynamic resource allocation have reduced network energy usage by approximately 30% in upgraded facilities. Telecom operators are deploying liquid-cooled data center racks and AI-based power management systems, supporting ESG commitments while maintaining high-capacity throughput exceeding multiple terabits per second in core networks.

The Network Transformation market is segmented by type, application, and end-user, reflecting varied modernization requirements across digital infrastructure ecosystems. By type, enterprises increasingly deploy software-defined and virtualized architectures to replace hardware-centric environments, with more than 60% of new enterprise network rollouts now involving cloud-managed or virtualized frameworks. Application segmentation is shaped by data center upgrades, branch connectivity optimization, and edge networking expansion for IoT and analytics. Over 70% of enterprises operate hybrid or multi-cloud systems, directly influencing network design priorities. From an end-user perspective, telecom operators and large enterprises remain primary adopters, while public sector and industrial organizations expand implementation in critical infrastructure. Regulatory compliance, cybersecurity frameworks, and energy-efficiency mandates continue to influence segmentation trends and technology selection across all categories.

Network Transformation technologies include SD-WAN, Network Function Virtualization (NFV), Software-Defined Networking (SDN), and network automation/orchestration platforms. SD-WAN leads with approximately 38% adoption share due to its ability to optimize branch connectivity, improve application routing, and lower bandwidth overhead by nearly 30% compared to conventional WAN systems.

Network automation and AI-driven orchestration represent the fastest-growing type, expanding at an estimated 18% CAGR as enterprises address operational complexity across hybrid networks. Automated provisioning reduces manual errors by about 50% and shortens deployment timelines significantly. NFV and SDN together account for roughly 44% of remaining implementations, supporting telecom core virtualization and programmable data center networking.

Major applications include enterprise branch networking, telecom core modernization, data center transformation, and edge networking for IoT. Enterprise branch networking leads with close to 36% adoption, as distributed operations and cloud services demand resilient and secure connectivity. Advanced SD-WAN frameworks improve application response times by nearly 35% in multi-site organizations.

Edge networking for IoT and real-time analytics is the fastest-growing application, rising at around 19% CAGR, supported by smart manufacturing, logistics automation, and connected healthcare systems. Data center transformation and telecom core upgrades together contribute about 45% of application usage, enabling cloud interconnectivity and high-capacity traffic handling.

Telecom operators constitute the leading end-user group with nearly 40% adoption, driven by the need to support increasing mobile and broadband traffic, which has grown more than 25% annually. Their modernization strategies emphasize virtualized cores, automation, and open-standard infrastructure to ensure scalability and service continuity.

Large enterprises are the fastest-growing end-user segment, expanding at an estimated 17% CAGR due to digital transformation and cloud integration. BFSI, healthcare, and manufacturing together account for about 35% of enterprise demand, leveraging modern networks for secure transactions, telehealth services, and industrial IoT. Government, education, and transportation sectors make up the remaining 25%, focusing on resilient and compliant infrastructure.

North America accounted for the largest market share at 37% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 16% between 2026 and 2033.

In 2025, North America had over 12,500 enterprise SD-WAN deployments and more than 8,200 virtualized core network instances, driven by healthcare, BFSI, and IT sectors. Asia-Pacific recorded nearly 9,800 active digital transformation projects in telecom and industrial networks, with China, India, and Japan contributing over 70% of deployments. Europe held a 23% regional share with Germany, the UK, and France leading adoption. South America and the Middle East & Africa combined accounted for 15% of global deployments, with significant uptake in energy, e-commerce, and smart city projects. Across regions, over 65% of large enterprises have integrated network automation tools, while edge computing adoption reached 48% in industrial and manufacturing segments.

How are enterprises modernizing connectivity and digital networks across industries?

North America holds a 37% market share in the Network Transformation market, supported by large-scale adoption in healthcare, BFSI, and IT enterprises. Regulatory initiatives such as NIST cybersecurity frameworks and federal broadband expansion programs encourage digital infrastructure modernization. Technological advancements include AI-based network orchestration, SD-WAN proliferation, and virtualized core deployments across telecom and enterprise networks. U.S. players such as Cisco Systems are implementing AI-driven traffic optimization tools, enabling up to 40% reduction in network downtime. Enterprise adoption is highest in finance and healthcare, with over 70% of hospitals and banks integrating software-defined networking for secure, scalable connectivity. Consumer behavior shows a preference for automated, cloud-managed solutions enabling real-time collaboration and low-latency digital services.

What factors are shaping secure and sustainable networking in major European markets?

Europe accounts for approximately 23% of the Network Transformation market, with Germany, the UK, and France leading deployments. Regulatory pressure from the European Union, including GDPR compliance and energy-efficiency mandates, drives demand for secure, explainable network solutions. Emerging technologies such as SDN, NFV, and AI-powered network analytics are being integrated in corporate and telecom infrastructures. Local players like Deutsche Telekom are rolling out edge-enabled, software-defined core networks to improve service efficiency and reduce latency by 30%. Enterprises across Europe increasingly prioritize regulatory-aligned solutions, with adoption highest in finance, manufacturing, and smart city initiatives. Regional consumer behavior emphasizes compliance, sustainability, and scalable network performance.

How is rapid digitalization fueling next-generation network deployment in the region?

Asia-Pacific ranks second in market volume and is the fastest-growing region for Network Transformation, with China, India, and Japan consuming over 70% of regional deployments. Telecom modernization, 5G infrastructure rollout, and industrial IoT expansion are key growth drivers. Companies are integrating AI-driven SD-WAN, edge computing, and NFV solutions, supported by national digitalization initiatives. Local players like Huawei are expanding cloud-managed network services, achieving nearly 35% improvement in network latency for enterprise clients. Consumer behavior trends show strong adoption in e-commerce, mobile AI applications, and smart manufacturing, reflecting the region’s focus on high-speed connectivity and digital service innovation.

What is driving enterprise and telecom network modernization across South America?

South America contributes roughly 9% of the global Network Transformation market, with Brazil and Argentina as leading countries. Growth is fueled by telecommunications upgrades, energy sector digitization, and increasing industrial automation. Government incentives, including tax breaks for digital infrastructure projects and trade partnerships, support enterprise adoption. Regional players like TIM Brasil are deploying SD-WAN solutions across commercial and municipal networks, reducing network downtime by 28%. Consumer behavior is focused on media streaming, language localization, and mobile-first services, with enterprises adopting secure, scalable networks to support digital payments and IoT initiatives.

How are digital initiatives transforming network infrastructure in emerging markets?

The Middle East & Africa accounts for 6% of the Network Transformation market, with UAE and South Africa leading in deployment volume. The oil & gas, construction, and public sector are key demand drivers, investing in software-defined and automated network platforms. Technological modernization includes AI traffic management, edge computing, and virtualization of telecom cores. Local operators, such as Etisalat, are expanding cloud-managed SD-WAN services across urban and industrial zones, improving network efficiency by 25%. Regional adoption reflects enterprise needs for secure, resilient infrastructure and growing reliance on smart city and industrial IoT applications.

United States – 28% market share; high production capacity, advanced R&D, and strong enterprise adoption drive leadership in software-defined and automated network solutions.

China – 21% market share; aggressive telecom modernization, large-scale 5G deployments, and robust industrial IoT adoption underpin its dominant position in Network Transformation initiatives.

The Network Transformation market is moderately consolidated, with over 120 active competitors operating globally, including telecom operators, IT solution providers, and specialized software vendors. The top five companies—Cisco Systems, Huawei, Juniper Networks, HPE, and IBM—collectively account for approximately 52% of the total market, underscoring significant concentration in enterprise and telecom segments. Competitive strategies focus on technology innovation, strategic partnerships, and targeted product launches; for instance, AI-driven network orchestration, SD-WAN integration, and edge computing solutions are now core differentiators. In 2025 alone, over 35 new AI-enabled network products were introduced across major regions, while several partnerships were formed to deploy cloud-managed network services for multi-site enterprises. Mergers and acquisitions are also reshaping competitive positioning, with over 12 deals executed globally to enhance capabilities in virtualization and automation. Innovation trends, such as programmable fabrics, zero-trust security frameworks, and hybrid cloud orchestration, are driving companies to differentiate while meeting enterprise demand for scalable, resilient, and secure network solutions. Regional competition is particularly intense in North America and Asia-Pacific, with over 45% of new deployments concentrated in these regions.

HPE

IBM

Nokia

Ericsson

VMware

Fortinet

Arista Networks

The Network Transformation market is experiencing a rapid technological evolution driven by software-defined, cloud-native, and AI-integrated networking solutions. SD-WAN remains a foundational technology, deployed in over 62% of large enterprises in North America and Europe to improve branch connectivity, reduce latency, and optimize bandwidth utilization by up to 30%. Network Function Virtualization (NFV) has been implemented in more than 8,000 telecom core networks globally, enabling dynamic service provisioning, flexible scaling, and reduced dependency on proprietary hardware.

Artificial intelligence and machine learning are increasingly embedded in network orchestration platforms, allowing predictive analytics for congestion management, fault detection, and security threat mitigation. AI-driven systems can process over 1 million network events per hour, reducing incident response time by nearly 45% and improving operational efficiency across multi-cloud and hybrid networks. Edge computing is also gaining traction, with more than 48% of industrial IoT deployments integrating edge nodes to support latency-sensitive applications such as autonomous manufacturing, smart logistics, and telemedicine. These implementations have reduced data transit delays by up to 35% in industrial environments.

Software-Defined Networking (SDN) and programmable network fabrics are enabling centralized control and automation of complex enterprise and telecom infrastructures. Open-standard virtualization and zero-trust security frameworks are being widely adopted, with over 70% of enterprise networks now integrating automated threat detection and compliance monitoring. In addition, 5G-enabled network architectures are being deployed across more than 300,000 active sites in Asia-Pacific and North America, enhancing bandwidth capacity, mobility support, and low-latency services for emerging applications such as augmented reality, AI-driven analytics, and cloud gaming. The convergence of these technologies positions Network Transformation as a critical enabler for resilient, secure, and high-performance digital infrastructure.

• In July 2025, Hewlett Packard Enterprise successfully completed its $14 billion acquisition of Juniper Networks, combining Juniper’s AI‑native networking portfolio with HPE’s cloud and edge capabilities to create an integrated networking stack designed for automated, scalable network operations for enterprise and telecom customers. (hpe.com)

• In late 2025, HPE unveiled enhanced AI‑Ops networking innovations across its unified Aruba and Juniper platforms, introducing consistent self‑driving AIOps features and expanded observability for network automation and performance optimization in hybrid cloud and edge deployments. (hpe.com)

• In early 2025, Nokia reorganized its business structure, splitting off its AI‑driven mobile business into distinct Network Infrastructure and Mobile Infrastructure units to accelerate development of AI‑powered network transformation solutions and 6G readiness while targeting significant operational efficiency improvements by 2028. (TechRadar)

• In 2025, IEEE and ETSI introduced updated SD‑WAN and NFV specifications, including ETSI NFV Release 5.2.1 with enhanced container networking and Telco Cloud analytics frameworks, marking key industry alignment on advanced virtualization and orchestration capabilities for next‑generation network transformation.

The Network Transformation Market Report encompasses a comprehensive assessment of market segments, geographic regions, application verticals, and enabling technologies, providing decision‑makers with detailed insights into how digital infrastructure is evolving globally. Coverage includes segmentation by network solution types such as SD‑WAN, SDN, NFV, and AI‑driven orchestration platforms, detailing how each type is deployed across enterprise, telecom, and industrial sectors. The report evaluates key application areas including data center transformation, branch connectivity modernization, 5G core integration, and edge networking for IoT and real‑time analytics. Geographic scope spans major regions—North America, Europe, Asia‑Pacific, South America, and Middle East & Africa—highlighting regional production capacities, technology adoption patterns, and regulatory environments influencing network transformation programs.

In addition to core segments, the report considers niche and emerging topics such as cloud‑native network functions, intent‑based networking, zero‑trust security integration, and network automation for AI workloads. Industry focus areas include telecom operators modernizing legacy cores, large enterprises optimizing distributed operations, and public sector initiatives integrating secure, scalable connectivity for critical services. Technical evaluation covers hardware, software, and services components, examining innovation trends in edge computing, programmable fabrics, and machine‑driven network management. The report also discusses ecosystem dynamics, including partnerships, standards alignment, and vendor strategies shaping competitive positioning. This broad scope enables professionals to understand current capabilities, future pathways, and strategic implications of network transformation investments.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

14% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Cisco Systems, Huawei, Juniper Networks, HPE, IBM, Nokia, Ericsson, VMware, Fortinet, Arista Networks |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |