Reports

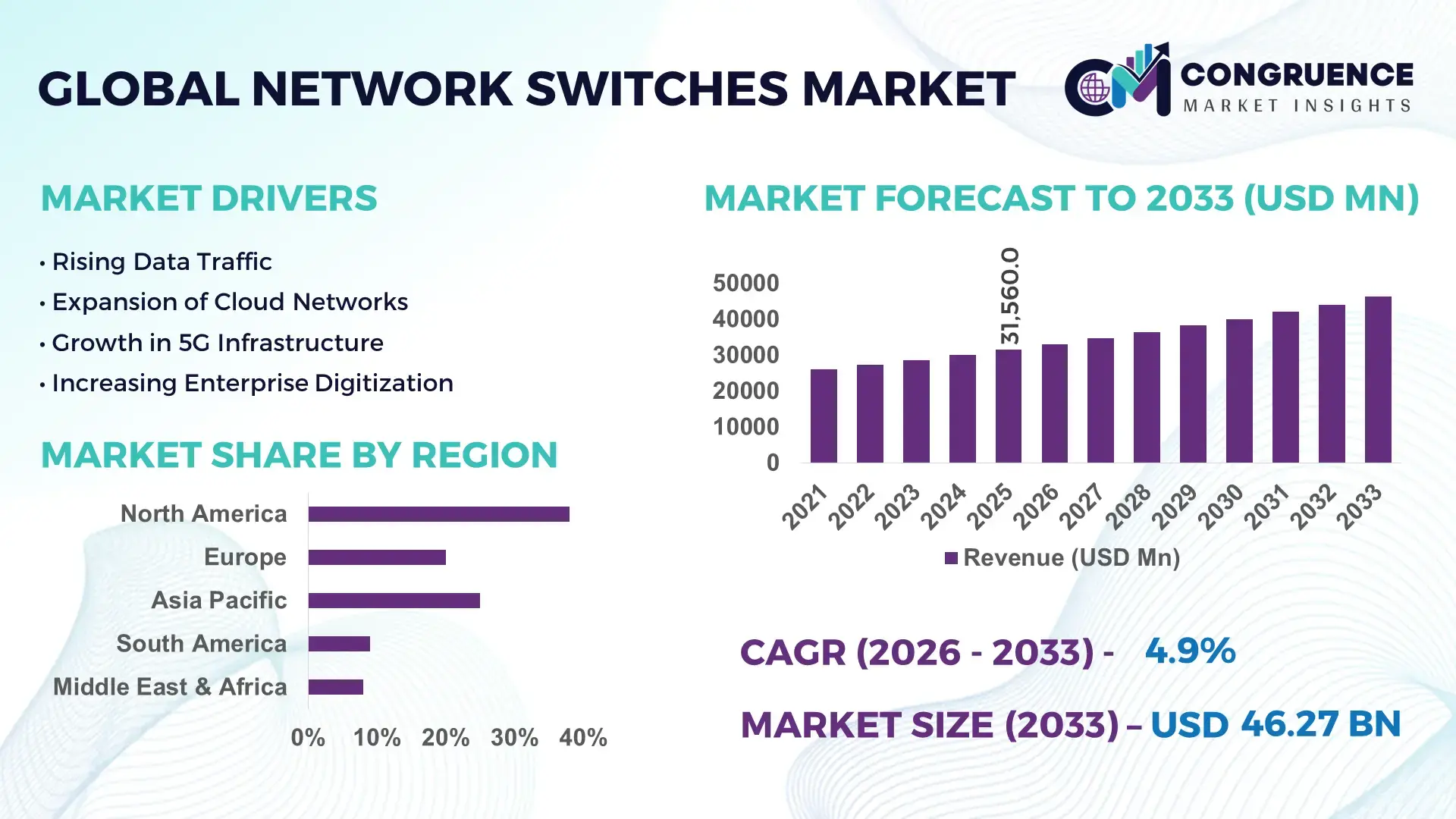

The Global Network Switches Market was valued at USD 31560 Million in 2025 and is anticipated to reach a value of USD 46274.41 Million by 2033 expanding at a CAGR of 4.9% between 2026 and 2033.

Enterprise migration toward AI-ready data center infrastructure, 400G Ethernet deployment, and hyperscale cloud expansion is accelerating demand for high-capacity, low-latency network switching platforms, with advanced Layer 3 switches reducing network congestion by over 28% compared to legacy architectures. Between 2024 and 2026, semiconductor supply normalization, rising digital sovereignty policies across Europe and Asia, and U.S.-China technology restrictions reshaped procurement strategies, driving regional manufacturing diversification and increasing investments in domestic networking hardware ecosystems.

The United States remains the dominant country in the global network switches market, accounting for nearly 34% of total enterprise-grade switching deployments in 2026, supported by large-scale investments from hyperscale cloud providers, telecom operators, and AI infrastructure developers. More than USD 18 billion has been allocated toward next-generation data center modernization and edge network expansion across sectors including BFSI, healthcare, and defense. Compared to emerging Asian markets, U.S. enterprises demonstrate over 40% higher adoption of 400G and AI-optimized switching solutions, while network automation penetration exceeded 52% across Tier-1 facilities in 2026, reinforcing operational efficiency and lower latency performance requirements.

Manufacturers prioritizing software-defined networking integration, regional supply resilience, and energy-efficient switch architectures are positioned to secure stronger enterprise contracts and long-term infrastructure partnerships.

Market Size & Growth: USD 31.56 billion in 2025 rising to USD 46.27 billion by 2033, supported by AI data center expansion, hyperscale cloud traffic growth, and enterprise edge networking modernization at 4.9% CAGR.

Top Growth Drivers: AI-driven traffic volumes increased 31%, enterprise cloud migration surpassed 64%, and 400G Ethernet deployments expanded 27% across advanced digital infrastructure environments.

Short-Term Forecast: By 2027, automated network orchestration is projected to reduce enterprise downtime by 22% while improving traffic management efficiency by 18%.

Emerging Technologies: AI-powered switching, software-defined networking, and 800G Ethernet adoption accelerated, with smart traffic optimization improving latency performance by nearly 30%.

Regional Leaders: North America exceeded USD 13 billion with hyperscale adoption growth, Asia-Pacific crossed USD 11 billion through telecom expansion, and Europe approached USD 8 billion driven by sovereign cloud investments.

Consumer/End-User Trends: More than 58% of enterprises shifted toward cloud-managed switches, while edge computing deployments expanded 24% across manufacturing and healthcare facilities.

Pilot/Case Example: In 2025, a major hyperscale operator upgraded AI-ready switching infrastructure, reducing internal data transfer bottlenecks by 35% and power consumption by 14%.

Competitive Landscape: Leading vendors controlled nearly 46% of global enterprise deployments, with competition centered around AI networking, automation software, and low-latency architecture innovation.

Regulatory & ESG Impact: Energy-efficiency regulations and carbon reduction targets improved adoption of low-power switches, lowering enterprise networking energy usage by approximately 16%.

Investment & Funding: Global investments surpassed USD 9 billion between 2024 and 2026, fueled by telecom partnerships, regional manufacturing expansion, and AI infrastructure supply chain diversification.

Innovation & Future Outlook: Next-generation AI fabrics, intelligent edge switching, and software-centric architectures are strengthening autonomous network management and real-time enterprise analytics capabilities.

Enterprise data centers contributed nearly 41% of total network switch deployments in 2026, followed by telecom infrastructure at 28% and cloud service providers at 22%, reflecting strong digital infrastructure expansion. AI-integrated traffic management and 800G-ready switching platforms improved network efficiency by more than 25%, while automated configuration tools reduced operational intervention by 19%. North America maintained the highest demand concentration, while Asia-Pacific recorded the fastest infrastructure rollout due to telecom modernization and regional manufacturing investments. Increasing localization policies and semiconductor supply diversification are accelerating demand for software-driven, energy-efficient network architectures, setting the foundation for more intelligent and autonomous enterprise connectivity strategies.

The network switches market is rapidly transforming into a strategic infrastructure battleground as AI computing, hyperscale cloud expansion, and edge connectivity redefine enterprise network performance requirements. Organizations are accelerating investments in high-bandwidth, low-latency switching systems to support real-time analytics, autonomous operations, and multi-cloud architectures. Global enterprises deploying AI-driven traffic orchestration reported nearly 32% faster workload processing and 21% lower network downtime across large-scale data environments in 2026. Simultaneously, supply chain regionalization and stricter cybersecurity regulations are forcing procurement shifts toward domestically manufactured and software-secured networking equipment, reshaping vendor selection strategies across North America, Europe, and Asia-Pacific.

AI-powered intelligent switching platforms are transforming network economics, as software-defined automation improves efficiency by 35% while reducing operational costs by 24% compared to legacy hardware-centric systems. Asia-Pacific leads in shipment volume due to telecom infrastructure expansion and manufacturing scale, while North America leads in adoption and innovation with over 54% penetration of AI-integrated data center switching solutions. Over the next three years, enterprise migration toward 400G and 800G Ethernet architectures is projected to improve network throughput efficiency by 29%, particularly across finance, cloud services, and defense sectors. Energy-efficient switching designs are also creating ESG-driven competitive advantages by reducing data center power consumption by nearly 18%, strengthening compliance positioning and lowering long-term infrastructure costs.

In 2025, a hyperscale cloud operator modernized its AI networking backbone using programmable switches, reducing latency by 31% and improving workload balancing efficiency by 27% across distributed facilities. Leading vendors are shifting capital allocation toward AI-native networking software, edge infrastructure partnerships, and regional manufacturing expansion to secure long-term enterprise contracts amid geopolitical technology fragmentation. Companies capable of optimizing intelligent automation, supply resilience, and scalable high-speed architectures are strengthening competitive positioning as network performance becomes directly tied to digital business execution and AI infrastructure leadership.

The rapid expansion of AI infrastructure, hyperscale cloud facilities, and edge computing ecosystems is accelerating demand for advanced network switching systems capable of managing ultra-high data traffic with low latency and automated orchestration. Enterprise AI workloads increased by more than 36% in 2026, while global deployment of 400G Ethernet switching platforms expanded nearly 28% across hyperscale data centers. Simultaneously, telecom operators increased edge network investments by 24% to support 5G backhaul capacity and real-time industrial connectivity. U.S.-China technology restrictions and semiconductor supply restructuring are forcing enterprises to diversify supplier networks and accelerate regional manufacturing investments, particularly across Southeast Asia and North America. This shift is directly increasing procurement of programmable, software-defined switches with stronger cybersecurity integration and traffic optimization capabilities. In response, major networking companies are expanding manufacturing capacity, strengthening semiconductor partnerships, and accelerating AI-integrated product launches to capture enterprise modernization demand. Strategic alliances between cloud providers and networking vendors are also reshaping infrastructure procurement cycles, enabling faster deployment of scalable and automated switching architectures across high-growth digital industries.

The network switches market remains heavily constrained by semiconductor dependency, rising infrastructure complexity, and volatile component pricing, creating operational pressure across enterprise and telecom deployments. Advanced networking chipsets experienced cost fluctuations exceeding 19% between 2024 and 2026 due to concentrated semiconductor manufacturing capacity and geopolitical trade restrictions. At the same time, deployment costs for high-speed 800G switching infrastructure increased nearly 22% because of cooling requirements, fiber upgrades, and power-intensive data center configurations. Emerging economies continue facing infrastructure gaps, with less than 38% of mid-sized enterprises fully equipped for AI-ready network integration. These constraints are extending procurement timelines and slowing migration from legacy architectures, particularly in cost-sensitive industrial sectors. Companies are mitigating risks through long-term semiconductor agreements, regional supplier diversification, and increased investment in modular switch designs that reduce upgrade costs. Several manufacturers are also integrating power-efficient silicon technologies and automated network management software to offset operational expenditure pressures while improving scalability across distributed enterprise environments.

AI-native networking, intelligent edge infrastructure, and software-centric network management are redefining growth opportunities across the global network switches market. Enterprise adoption of cloud-managed switching platforms surpassed 57% in 2026 as businesses prioritized automation, predictive traffic optimization, and decentralized connectivity. Demand for edge-ready switching solutions increased by 33% across manufacturing, logistics, and healthcare sectors due to rising deployment of real-time analytics and industrial IoT systems. A major future signal is the accelerating transition toward autonomous networking environments where AI engines independently manage traffic balancing, cybersecurity response, and bandwidth allocation. This transformation is generating non-obvious advantages through lower operational intervention, nearly 26% faster fault detection, and stronger network uptime performance. Companies are positioning aggressively through R&D expansion, AI software acquisitions, and ecosystem partnerships integrating cloud, cybersecurity, and edge computing capabilities. Vendors investing early in programmable architectures and energy-efficient switching systems are securing stronger positioning in government digitalization projects, sovereign cloud initiatives, and AI-focused enterprise infrastructure modernization programs.

The network switches market faces mounting execution challenges linked to scalability limitations, cybersecurity complexity, and increasing power density requirements across AI-driven infrastructure environments. High-performance switching systems supporting AI clusters consume nearly 17% more energy than traditional enterprise networking configurations, intensifying pressure on data center cooling and power management systems. At the same time, cybersecurity attacks targeting enterprise network infrastructure increased by over 29% between 2024 and 2026, forcing companies to redesign switching architectures with embedded threat intelligence and zero-trust security frameworks. Infrastructure readiness also remains uneven, with many regional telecom and industrial operators lacking the fiber density and automation capabilities required for large-scale 800G adoption. These barriers are constraining deployment consistency and increasing integration costs across multi-cloud environments. To remain competitive, companies must accelerate investment in secure programmable silicon, advanced thermal management, and AI-driven network orchestration platforms. Strategic partnerships with cloud providers, semiconductor manufacturers, and cybersecurity firms are becoming essential to sustain performance reliability, operational resilience, and long-term infrastructure scalability in an increasingly complex digital ecosystem.

AI-Driven Switching Deployment Expanded 34% Across Enterprise Data Centers in 2026 as organizations shifted toward programmable, low-latency switching fabrics to support AI workloads and real-time analytics. Automated traffic optimization reduced manual network intervention by 26% while improving bandwidth allocation efficiency by 21%. Enterprises are restructuring network operations around AI-native orchestration platforms, forcing vendors to scale software-centric switch portfolios and embedded analytics capabilities.

Cloud-Managed Switching Adoption Surpassed 58% Across Multi-Site Enterprise Networks as businesses prioritized centralized visibility, remote configuration, and lower maintenance overhead. Deployment times declined by 31%, while operational troubleshooting efficiency improved by 24% through AI-assisted diagnostics. Rising cybersecurity compliance requirements and distributed workforce models are reshaping procurement decisions, pushing networking companies toward subscription-driven management platforms and integrated security partnerships.

Asia-Pacific Manufacturing Expansion Increased Regional Switch Production Capacity by 29% as vendors diversified supply chains away from concentrated semiconductor sourcing hubs. Southeast Asian assembly operations accelerated due to tariff pressures and geopolitical technology restrictions, reducing lead-time volatility by nearly 18%. A non-obvious shift is emerging where manufacturers are prioritizing regional component redundancy over short-term cost optimization to strengthen long-term enterprise contract reliability.

PoE and Edge-Optimized Switching Installations Grew 27% Across Industrial and Smart Campus Environments as enterprises integrated IoT sensors, surveillance systems, and connected automation infrastructure. Energy-efficient switch configurations lowered facility-level power consumption by 14%, while edge traffic processing improved response speed by 23%. Companies are rapidly expanding strategic partnerships with industrial automation providers to optimize edge connectivity performance and secure recurring infrastructure upgrade cycles.

The network switches market is segmented by type, application, and end-user, with demand increasingly concentrated around intelligent, software-driven, and high-speed networking environments. Managed switches continue dominating enterprise and cloud deployments due to scalability and centralized control advantages, while PoE and smart switches are gaining traction in industrial automation and smart infrastructure projects. By application, enterprise networking and data centers collectively account for more than 60% of deployment demand as organizations prioritize AI-ready connectivity and traffic optimization. Cloud computing and industrial networking are experiencing faster adoption shifts due to edge infrastructure expansion and real-time operational requirements. From an end-user perspective, IT and telecom remain the largest consumers of advanced switching systems, while healthcare and manufacturing are accelerating procurement through digital transformation initiatives and connected infrastructure investments. Regional demand is shifting toward Asia-Pacific for manufacturing scale and North America for AI-driven deployment intensity, forcing vendors to balance production localization, automation integration, and software-centric product innovation strategies.

Managed switches dominate the network switches market with approximately 48% share due to their scalability, centralized traffic management, advanced cybersecurity integration, and compatibility with AI-driven enterprise networking environments. Large enterprises and hyperscale data centers increasingly prioritize managed infrastructure because automated monitoring and software-defined controls reduce downtime by nearly 24% while improving network visibility across distributed operations. PoE switches are emerging as the fastest-growing segment, expanding by nearly 26% in deployment volume as smart buildings, industrial IoT systems, and connected surveillance infrastructure accelerate globally. Compared to unmanaged switches, PoE-enabled systems significantly improve installation flexibility and reduce cabling costs by nearly 18%, making them strategically attractive for large-scale smart infrastructure projects. Smart and unmanaged switches collectively account for around 34% of market demand, maintaining relevance in cost-sensitive SME environments and low-complexity networking operations where deployment simplicity remains a priority. However, demand is steadily shifting toward software-managed and power-efficient switching platforms as enterprises modernize digital infrastructure. In response, manufacturers are accelerating product development around cloud-managed systems, AI-integrated traffic orchestration, and modular PoE architectures to capture expanding edge networking and intelligent infrastructure opportunities.

“According to a 2025 report by the International Telecommunication Union, managed switching technology was adopted by over 61% of enterprise-grade network operators, resulting in nearly 27% improvement in traffic optimization efficiency and reduced operational downtime, reinforcing its growing strategic importance.”

Enterprise networking remains the leading application segment, accounting for nearly 36% of total network switch deployments due to rising demand for secure, scalable, and cloud-connected enterprise infrastructure. Large organizations are rapidly modernizing campus and branch connectivity environments to support hybrid work models, AI-driven analytics, and real-time collaboration systems. Data centers represent the fastest-growing application area, with deployment activity increasing by approximately 31% as hyperscale cloud operators and AI infrastructure providers expand high-density networking architectures. Compared to traditional enterprise networking environments, modern AI-ready data centers require significantly higher bandwidth capacity and low-latency switching performance, redefining infrastructure priorities across global digital ecosystems. Cloud computing, industrial networking, and campus networking collectively contribute around 44% of market demand, driven by edge computing integration, industrial automation expansion, and centralized digital infrastructure management. Usage patterns are shifting toward intelligent traffic orchestration and software-defined networking as businesses seek lower operational complexity and higher scalability. Vendors are responding by expanding AI-optimized switch portfolios, strengthening cloud platform partnerships, and accelerating deployment-ready edge networking solutions to capture high-performance enterprise and industrial networking demand.

“According to a 2025 report by the Institute of Electrical and Electronics Engineers, advanced data center switching infrastructure was deployed across over 4,500 large-scale digital facilities, improving workload processing efficiency by 33% and reducing internal network latency by 21%, highlighting its rapid operational adoption.”

IT and telecom dominate the network switches market with nearly 42% share due to massive bandwidth consumption, hyperscale infrastructure expansion, and continuous network modernization initiatives. Telecom operators and cloud service providers require advanced switching architectures capable of handling ultra-high traffic density, AI-enabled routing, and low-latency data transmission across distributed digital ecosystems. Healthcare is emerging as the fastest-growing end-user segment, with network infrastructure deployment increasing by approximately 25% as hospitals and diagnostic facilities integrate connected medical devices, AI-assisted diagnostics, and real-time patient monitoring systems. Compared to traditional government procurement cycles, healthcare organizations are adopting network automation and secure switching systems at a significantly faster pace to improve operational responsiveness and cybersecurity resilience. BFSI, government, and manufacturing collectively account for around 46% of demand, driven by digital banking expansion, smart governance projects, and industrial automation integration. Buying behavior is increasingly shifting toward customized, cybersecurity-focused, and cloud-managed networking solutions. In response, companies are expanding vertical-specific product offerings, introducing flexible subscription pricing models, and strengthening strategic partnerships with telecom carriers, healthcare system integrators, and industrial automation providers to capture evolving infrastructure modernization demand.

“According to a 2025 report by the World Economic Forum, adoption among healthcare organizations increased by 24%, with over 18,000 facilities implementing intelligent network switching solutions, leading to nearly 22% improvement in operational efficiency and faster real-time data accessibility, indicating a strong shift in demand dynamics.”

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.3% between 2026 and 2033.

North America maintains demand concentration through hyperscale cloud expansion, AI infrastructure deployment, and enterprise network modernization, with more than 54% of large enterprises integrating AI-enabled switching platforms. Asia-Pacific contributes over 34% of global production capacity and is accelerating through telecom infrastructure expansion, localized semiconductor assembly, and industrial digitalization initiatives across China, India, Japan, and Southeast Asia. Europe holds nearly 22% market share and leads in energy-efficient and compliance-driven networking adoption due to stricter cybersecurity and sustainability regulations. A major structural shift is emerging as vendors diversify supply chains beyond concentrated semiconductor hubs to reduce geopolitical risk and improve delivery stability. Global companies are increasingly prioritizing Asia-Pacific for manufacturing scale, North America for advanced deployment partnerships, and Europe for regulatory-driven innovation and premium infrastructure integration.

North America represents nearly 38% of global network switch demand, supported by hyperscale cloud infrastructure, AI data center expansion, and aggressive enterprise network modernization programs. The United States dominates regional deployment activity, with more than 57% of large enterprises transitioning toward software-defined and AI-managed switching architectures. Rising cybersecurity regulations and domestic semiconductor investment incentives are structurally reshaping procurement strategies, forcing enterprises to prioritize secure, low-latency, and energy-efficient switching platforms. Deployment of 400G and 800G Ethernet infrastructure increased by approximately 29% in 2026 as cloud operators expanded AI processing capacity. Enterprises increasingly prefer scalable cloud-managed systems that reduce operational intervention and improve network resilience. Vendors are accelerating regional manufacturing expansion and AI networking partnerships, making North America a priority market for premium infrastructure deployment and long-term enterprise contracts.

Europe accounts for nearly 22% of the global network switches market, with Germany, the United Kingdom, and France leading enterprise infrastructure modernization and sovereign cloud integration. Strict cybersecurity directives and energy-efficiency regulations are forcing enterprises to replace legacy switching systems with low-power, software-secured alternatives capable of reducing infrastructure energy consumption by nearly 17%. More than 46% of large European enterprises prioritized cloud-managed networking deployments in 2026 to strengthen compliance visibility and operational resilience. Companies are accelerating deployment of AI-assisted network monitoring and automated traffic optimization to meet sustainability and data sovereignty requirements simultaneously. Enterprise buyers in the region consistently favor quality-focused, regulation-compliant solutions over low-cost hardware alternatives. This environment is pushing global vendors to redesign product architectures around ESG performance, cybersecurity certification, and energy-efficient digital infrastructure innovation.

Asia-Pacific ranks as the fastest-scaling regional market, contributing more than 34% of global network switch production and deployment activity. China, India, Japan, and South Korea are driving demand through hyperscale data center expansion, telecom modernization, and industrial automation initiatives. Regional manufacturing advantages and localized semiconductor assembly operations reduced equipment lead times by nearly 19% between 2024 and 2026, strengthening supply chain competitiveness. Enterprise deployment of cloud-managed and AI-integrated switching systems expanded by approximately 31% as businesses accelerated digital transformation and edge infrastructure integration. Organizations across the region prioritize deployment speed, scalability, and cost-efficient networking performance over premium customization models. Major vendors are expanding assembly facilities, strengthening telecom partnerships, and localizing product ecosystems, making Asia-Pacific critical for production scale, high-volume adoption, and long-term infrastructure expansion strategies.

South America contributes nearly 8% of global network switch demand, led by Brazil, Argentina, and Chile through telecom modernization and enterprise digitalization projects. Growth is primarily supported by rising cloud connectivity adoption and industrial network expansion across logistics, mining, and financial services sectors. However, infrastructure limitations, currency volatility, and higher import dependency continue constraining advanced switching deployment, increasing procurement costs by nearly 14% in several enterprise projects. Despite these barriers, cloud-managed network installations increased by approximately 21% in 2026 as businesses prioritized lower maintenance complexity and scalable remote operations. Enterprises remain highly price-sensitive and increasingly favor modular, upgrade-ready switching systems over premium high-density architectures. Vendors are responding through localized distribution partnerships and flexible deployment models, positioning South America as a strategic expansion opportunity with moderate operational risk and strong long-term digital infrastructure potential.

The Middle East & Africa region accounts for approximately 7% of global network switch demand, supported by smart city initiatives, telecom expansion, and large-scale infrastructure modernization programs across the UAE, Saudi Arabia, and South Africa. Oil and gas operations, transportation systems, and public infrastructure projects are accelerating deployment of secure and high-capacity switching systems capable of supporting connected industrial environments. Regional digital infrastructure investment increased by nearly 26% between 2024 and 2026, while cloud-integrated enterprise networking adoption expanded by approximately 18%. Governments and enterprises are increasingly prioritizing scalable, energy-efficient, and cybersecurity-focused networking platforms to support long-term economic diversification strategies. Vendors are strengthening regional partnerships, expanding technical service networks, and localizing deployment operations, positioning the region as an emerging infrastructure transformation market with increasing strategic relevance for global network technology providers.

United States – 34% market share in the Network Switches market, driven by hyperscale cloud infrastructure expansion, AI-ready data center deployments, and strong enterprise adoption of software-defined networking systems.

China – 21% market share in the Network Switches market, supported by large-scale telecom infrastructure investment, localized manufacturing capacity, and rapid industrial digitalization initiatives.

The network switches market is dominated by competition between global networking leaders, AI-focused infrastructure innovators, and cost-competitive regional manufacturers. Companies such as Cisco Systems, Huawei Technologies, Arista Networks, Juniper Networks, and HPE Aruba Networking collectively control nearly 61% of enterprise-grade switching deployments, competing aggressively across hyperscale cloud infrastructure, AI networking, telecom modernization, and edge computing environments. Competition is increasingly defined by software-driven automation, low-latency switching performance, cybersecurity integration, and supply chain responsiveness rather than hardware pricing alone. AI-enabled traffic orchestration platforms improved enterprise network efficiency by nearly 28%, while cloud-managed switching systems reduced deployment complexity by approximately 24%, forcing vendors to accelerate software-centric innovation strategies. Companies are expanding regional manufacturing operations, strengthening semiconductor partnerships, and pursuing vertical integration to stabilize component access amid geopolitical supply chain restructuring. Strategic acquisitions and cloud ecosystem alliances are also reshaping market positioning as enterprises prioritize scalable and AI-ready networking environments. High R&D intensity, advanced semiconductor dependency, and enterprise certification requirements continue creating significant entry barriers. Winning in this market increasingly depends on delivering intelligent automation, supply resilience, cybersecurity performance, and scalable infrastructure integration simultaneously.

Cisco Systems

Huawei Technologies

Arista Networks

Juniper Networks

HPE Aruba Networking

Dell Technologies

Extreme Networks

NETGEAR

D-Link Corporation

TP-Link Technologies

Nokia

ZTE Corporation

Allied Telesis

Fortinet

AI-native switching platforms, software-defined networking, and 400G/800G Ethernet architectures are redefining enterprise and hyperscale infrastructure operations across the network switches market. In 2026, more than 54% of large cloud and enterprise operators deployed AI-assisted traffic orchestration systems to optimize bandwidth utilization and reduce latency bottlenecks. AI-powered switching environments improved network efficiency by nearly 32% while lowering manual operational intervention by 24%. Compared to traditional hardware-centric switching systems, programmable AI-integrated platforms deliver approximately 35% faster traffic balancing and nearly 21% lower infrastructure management costs, making them critical for large-scale AI and cloud deployments.

Emerging technologies including autonomous network management, Ultra Ethernet frameworks, and intelligent edge switching are accelerating operational transformation across telecom, industrial, and cloud environments. Deployment of cloud-managed switching platforms surpassed 58% across distributed enterprise networks as organizations prioritized centralized visibility and automated fault detection. Advanced Ethernet fabrics supporting AI clusters improved workload completion performance by nearly 28% while reducing packet congestion through predictive load balancing capabilities. Vendors are integrating AI observability tools, programmable silicon, and energy-efficient architectures to strengthen low-latency performance and cybersecurity resilience simultaneously.

Disruptive technologies between 2026 and 2028 are centered on 1.6T switching, AI-driven self-healing networks, and open Ethernet standards replacing proprietary infrastructure ecosystems. Hyperscale operators and AI infrastructure providers are aggressively adopting open, multi-vendor Ethernet environments to reduce deployment complexity and strengthen supply chain flexibility. Companies investing early in autonomous switching intelligence, high-density AI fabrics, and energy-optimized networking systems are securing operational advantages through lower downtime, faster scalability, and stronger infrastructure adaptability. The competitive edge is rapidly shifting toward vendors capable of combining intelligent automation, open architecture compatibility, and scalable AI networking performance at enterprise scale.

October 2025 – Arista Networks introduced its R4 Series 800G AI and data center switching platforms featuring 3.2 Tbps HyperPorts and enhanced AI workload optimization capabilities. The launch improved network scalability and reduced AI job completion latency across high-density cloud environments. [AI Fabric Expansion] Source: Arista Networks Press Release

March 2025 – Arista Networks launched the EOS Smart AI Suite with Cluster Load Balancing and AI observability tools, improving AI workload traffic efficiency and enabling monitoring at 100-microsecond intervals. The development strengthened Ethernet-based AI networking competitiveness against proprietary interconnect systems. [AI Traffic Optimization] Source: Arista Newsroom

December 2025 – Arista Networks expanded its Cognitive Campus portfolio with VESPA mobility architecture and AVA agentic AI capabilities, enabling support for over 500,000 connected clients with sub-second failover performance. The rollout accelerated large-scale campus and IoT network automation deployments. [Campus AI Scaling] Source: Arista Networks Investor Relations

November 2025 – Broadcom introduced the Thor Ultra 800G AI Ethernet NIC with PCIe Gen6 integration and advanced congestion management capabilities for AI-focused data centers. The technology improved ultra-high throughput networking performance and strengthened open Ethernet adoption in AI infrastructure environments. [Ultra Ethernet Push] Source: TechRadar Pro

This report provides comprehensive coverage of the global network switches market across product types, applications, end-user industries, regional dynamics, and emerging networking technologies shaping enterprise infrastructure modernization. The analysis covers managed, unmanaged, smart, and PoE switches alongside critical applications including enterprise networking, data centers, industrial networking, cloud computing, and campus infrastructure. End-user evaluation spans IT and telecom, BFSI, healthcare, government, and manufacturing sectors, with strategic regional assessment across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The report also examines next-generation technologies including AI-native switching, software-defined networking, autonomous traffic orchestration, 800G Ethernet, and intelligent edge networking ecosystems.

The study evaluates more than 10 major market participants and analyzes multiple deployment trends, operational shifts, and infrastructure adoption patterns influencing competitive positioning between 2026 and 2033. Enterprise adoption of cloud-managed switching platforms exceeded 58%, while AI-integrated networking deployments expanded by nearly 31% across hyperscale and industrial environments. The report delivers strategic insights into supply chain restructuring, semiconductor dependency, cybersecurity integration, energy-efficient networking architectures, and regional production diversification. Decision-makers gain actionable intelligence for infrastructure investment, geographic expansion, partnership strategy, product innovation, and competitive benchmarking across rapidly evolving digital networking ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 31560 Million |

|

Market Revenue in 2033 |

USD 46274.41 Million |

|

CAGR (2026 - 2033) |

4.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Cisco Systems, Huawei Technologies, Arista Networks, Juniper Networks, HPE Aruba Networking, Dell Technologies, Extreme Networks, NETGEAR, D-Link Corporation, TP-Link Technologies, Nokia, ZTE Corporation, Allied Telesis, Fortinet |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |